Authored by Raul Ilargi Meijer via The Automatic Earth blog,

Austerity is over, proclaimed the IMF this week. And no doubt attributed that to the ‘successful’ period of ‘five years of belt tightening’ a.k.a. ‘gradual fiscal consolidation’ it has, along with its econo-religious ilk, imposed on many of the world’s people. Only, it’s not true of course. Austerity is not over. You can ask many of those same people about that. It’s certainly not true in Greece.

IMF Says Austerity Is Over

Austerity is over as governments across the rich world increased spending last year and plan to keep their wallets open for the foreseeable future. After five years of belt tightening, the IMF says the era of spending cuts that followed the financial crisis is now at an end. “Advanced economies eased their fiscal stance by one-fifth of 1pc of GDP in 2016, breaking a five-year trend of gradual fiscal consolidation,” said the IMF in its fiscal monitor.

In Greece, the government did not increase spending in 2016. Nor is the country’s era of spending cuts at an end. So did the IMF ‘forget’ about Greece? Or does it not count it as part of the rich world? Greece is a member of the EU, and the EU is absolutely part of the rich world, so that can’t be it. Something Freudian, wishful thinking perhaps?

However this may be, it’s obvious the IMF are not done with Greece yet. And neither are the rest of the Troika. They are still demanding measures that are dead certain to plunge the Greeks much further into their abyss in the future. As my friend Steve Keen put it to me recently: “Dreadful. It will become Europe’s Somalia.”

An excellent example of this is the Greek primary budget surplus. The Troika has been demanding that it reach 3.5% of GDP for the next number of years (the number changes all the time, 3, 5, 10?). Which is the worst thing it could do, at least for the Greek people and the Greek economy. Not for those who seek to buy Greek assets on the cheap.

But sure enough, the Hellenic Statistical Authority (ELSTAT) jubilantly announced on Friday that the 2016 primary surplus was 4.19% (8 times more than the 0.5% expected). This is bad news for Greeks, though they don’t know it. It is also a condition for receiving the next phase of the current bailout. Here’s what that comes down to: in order to save itself from default/bankruptcy, the country is required to destroy its economy.

And that’s not all: the surplus is a requirement to get a next bailout tranche, and debt relief, but as a reward for achieving that surplus, Greece can now expect to get less … debt relief. Because obviously they’re doing great, right?! They managed to squeeze another €7.3 billion out of their poor. So they should always be able to do that in every subsequent year.

The government in Athens sees the surplus as a ‘weapon’ that can be used in the never-ending bailout negotiations, but the Troika will simply move the goalposts again; that’s its MO.

A country in a shape as bad as Greece’s needs stimulus, not a budget surplus; a deficit would be much more helpful. You could perhaps demand that the country goes for a 0% deficit, though even that is far from ideal. But never a surplus. Every penny of the surplus should have been spent to make sure the economy doesn’t get even worse.

Greek news outlet Kathimerini gets it sort of right, though its headline should have read “Greek Primary Surplus Chokes Economy“.

Greek Primary Surplus Chokes Market

The state’s fiscal performance last year has exceeded even the most ambitious targets, as the primary budget surplus as defined by the Greek bailout program, came to 4.19% of GDP, government spokesman Dimitris Tzanakopoulos announced on Friday. It came to €7.369 billion against a target for €879 million, or just 0.5% of GDP. A little earlier, the president of the Hellenic Statistical Authority (ELSTAT), Thanos Thanopoulos, announced the primary surplus according to Eurostat rules, saying that it came to 3.9% of GDP or €6.937 billion.

The two calculations differ in methodology, but it is the surplus attained according to the bailout rules that matters for assessing the course of the program. This was also the first time since 1995 that Greece achieved a general government surplus – equal to 0.7% of GDP – which includes the cost of paying interest to the country’s creditors. There is a downside to the news, however, as the figures point to overtaxation imposed last year combined with excessive containment of expenditure.

The amount of €6-6.5 billion collected in excess of the budgeted surplus has put a chokehold on the economy, contributing to a great extent to the stagnation recorded on the GDP level in 2016. On the one hand, the impressive result could be a valuable weapon for the government in its negotiations with creditors to argue that it is on the right track to fiscal streamlining and can achieve or even exceed the agreed targets. On the other hand, however, the overperformance of the budget may weaken the argument in favor of lightening the country’s debt load.

Eurogroup head Dijsselbloem sees no shame in admitting this last point :

Dijsselbloem Sees ‘Tough’ Greek Debt Relief Talks With IMF

“That will be a tough discussion with the IMF,” said Dijsselbloem, who is also the Dutch Finance Minister in a caretaker cabinet, “There are some political constraints where we can go and where we can’t go.” The level of Greece’s primary budget surplus is key in determining the kind of debt relief it will need. The more such surplus it has, the less debt relief will be needed.

That’s just plain insane, malicious even. Greek PM Tsipras should never have accepted any such thing, neither the surplus demands nor the fact that they affect debt relief, since both assure a further demise of the economy.

Because: where does the surplus come from? Easy: from Troika-mandated pension cuts and rising tax levels. That means the Greek government is taking money OUT of the economy. And not a little bit, but a full 4% of GDP, over €7 billion. An economy from which so much has already vanished.

The €7.369 billion primary surplus, in a country of somewhere between 10 and 11 million people, means some €700 per capita has been taken out of the economy in 2016. Money that could have been used to spend inside that economy, saving jobs, and keeping people fed and sheltered. For a family of 3.5 people that means €200 per month less to spend on necessities (the only thing most Greeks can spend any money on).

I’ve listed some of the things a number of times before that have happened to Greece since the EU and IMF declared de facto financial war on the country. Here are a few (there are many more where these came from):

25-30% of working age Greeks are unemployed (and that’s just official numbers), well over 1 million people; over 50% of young people are unemployed. Only one in ten unemployed Greeks receive an unemployment benefit (€360 per month), and only for one year. 9 out of 10 get nothing.

Which means 52% of Greek households are forced to live off the pension of an elderly family member. 60% of Greek pensioners receive pensions below €700. 45% of pensioners live below the poverty line with pensions below €665. Pensions have been cut some 12 times already. More cuts are in the pipeline.

40% of -small- businesses have said they expect to close in 2017. Even if it’s just half that, imagine the number of additional jobs that will disappear.

But the Troika demands don’t stop there; they are manifold. On top of the pension cuts and the primary surplus requirement, there are the tax hikes. So the vast majority of Greeks have ever less money to spend, the government takes money out of the economy to achieve a surplus, and on top of that everything gets more expensive because of rising taxes. Did I ever mention businesses must pay their taxes up front for a full year?

The Troika is not “rebalancing Greece’s public finances in a growth-friendly manner”, as Dijsselbloem put it, it is strangling the economy. And then strangling it some more.

There may have been all sorts of things wrong in Greece, including financially. But that is true to some degree for every country. And there’s no doubt there was, and still is, a lot of corruption. But that would seem to mean the EU must help fight that corruption, not suffocate the poor.

Yes, that’s about a 30% decline in GDP since 2007

The ECB effectively closed down the Greek banking system in 2015, in a move that’s likely illegal. It asked for a legal opinion on the move but refuses to publish that opinion. As if Europeans have no right to know what the legal status is of what their central bank does.

The ECB also keeps on refusing to include Greece in its QE program. It buys bonds and securities from Germany, which doesn’t need the stimulus, and not those of Greece, which does have that need. Maybe someone should ask for a legal opinion on that too.

The surplus requirements will be the nail in the coffin that do Greece in. Our economies depend for their GDP numbers on consumer spending, to the tune of 60-70%. Since Greek ‘consumers’ can only spend on basic necessities, that number may be even higher there. And that is the number the country is required to cut even more. Where do you think GDP is headed in that scenario? And unemployment, and the economy at large?

The question must be: don’t the Troika people understand what they’re doing? It’s real basic economics. Or do they have an alternative agenda, one that is diametrically opposed to the “rebalancing Greece’s public finances in a growth-friendly manner” line? It has to be one of the two; those are all the flavors we have.

You can perhaps have an idea that a country can spend money on wrong, wasteful things. But that risk is close to zilch in Greece, where many if not most people already can’t afford the necessities. Necessities and waste are mutually exclusive. A lot more money is wasted in Dijsselbloem’s Holland than in Greece.

In a situation like the one Greece is in, deflation is a certainty, and it’s a deadly kind of deflation. What makes it worse is that this remains hidden because barely a soul knows what deflation is.

Greece’s deflation hides behind rising taxes. Which is why taxes should never be counted towards inflation; it would mean all a government has to do to raise inflation is to raise taxes; a truly dumb idea. Which is nevertheless used everywhere on a daily basis.

In reality, inflation/deflation is money/credit supply multiplied by the velocity of money. And in Greece both are falling rapidly. The primary surplus requirements make it that much worse. It really is the worst thing one could invent for the country.

For the Greek economy, for its businesses, for its people, to survive and at some point perhaps even claw back some of the 30% of GDP it lost since 2007, what is needed is a way to make sure money can flow. Not in wasteful ways, but in ways that allow for people to buy food and clothing and pay for rent and power.

If you want to do that, taking 4% of GDP out of an economy, and 3.5% annually for years to come, is the very worst thing. That can only make things worse. And if the Greek economy deteriorates further, how can the country ever repay the debts it supposedly has? Isn’t that a lesson learned from the 1919 Versailles treaty?

The economists at the IMF and the EU/ECB, and the politicians they serve, either don’t understand basic economics, or they have their eyes on some other prize.

A lot of emails are coming in asking if I have been advising Trump on the taxes since this is similar to the plan I proposed when I testified before Congress. The answer is no. If they took the tax proposals we had worked on with members of Congress back in the Nineties, who knows. They are on file and have been endorsed by many different tax reform advocates.

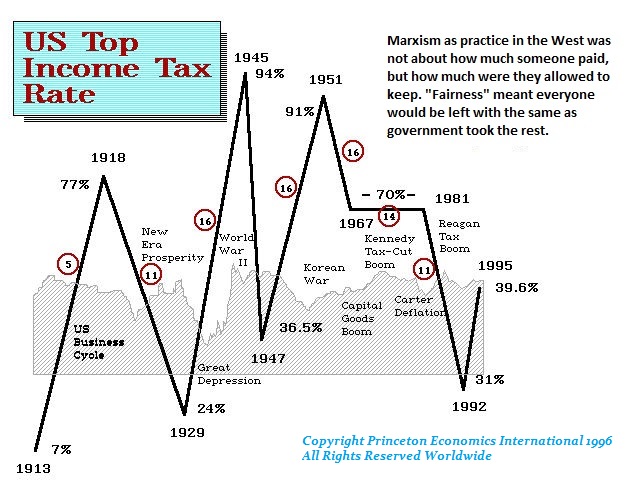

A lot of emails are coming in asking if I have been advising Trump on the taxes since this is similar to the plan I proposed when I testified before Congress. The answer is no. If they took the tax proposals we had worked on with members of Congress back in the Nineties, who knows. They are on file and have been endorsed by many different tax reform advocates. The biggest problem we face is this has to be made into a Constitutional Amendment. This is my ADVICE to Trump right now! Why, as soon as the cycle changes and the Democrats gain control, the taxes will rise again. This is why corporations level. We LACK TAX STABILITY. Taxes become a yo-yo and business cannot plan long-term when the political atmosphere keeps changing between Marxism and a Free Market. This eternal battle destroys economic growth and has ruined jobs only to reduce the standard of living for the long run. A chart of the top tax brackets look like the brainwave of a schizophrenic.

The biggest problem we face is this has to be made into a Constitutional Amendment. This is my ADVICE to Trump right now! Why, as soon as the cycle changes and the Democrats gain control, the taxes will rise again. This is why corporations level. We LACK TAX STABILITY. Taxes become a yo-yo and business cannot plan long-term when the political atmosphere keeps changing between Marxism and a Free Market. This eternal battle destroys economic growth and has ruined jobs only to reduce the standard of living for the long run. A chart of the top tax brackets look like the brainwave of a schizophrenic.

The London housing market sales has crashed to its lowest level now since 2013. We reported in

The London housing market sales has crashed to its lowest level now since 2013. We reported in