How is it possible that we can have legalized class warfare and politicians run on extorting the rich at gun point with threat of imprisonment if they do not pay their “fair share” which is somehow a higher percentage than everyone else and this miraculously does not violate Equal Protection and Justice for All? The Supreme Court dances around this issue that clearly is unconstitutional and is a Communist idea championed by Karl Marx, which is the cornerstone of leftist politics. Yet, when we peal back the veneer and we look at the same principle in other contexts, we suddenly see a conflict of law. For example. Justice Samuel Alito’s majority opinion in Knox v. Service Employees International Union, Local 1000, in which nonunion California state employees whose wages and benefits were nonetheless set through the collective bargaining process of SEIU — the state’s largest union — sued the local to get back a special dues assessment it levied in 2005 to fight two ballot measures. The union’s normal practice was to allow nonmembers to opt out of paying the roughly 44% of dues that went to matters not directly related to collective bargaining, such as election campaigns. In this instance, however, no such opt-out was allowed.

The issue before the court was whether mandating the collection of the special assessment from nonmembers violated their constitutional rights to free speech. Alito and the four other conservative justices ruled that it did, and liberal Justices Sonia Sotomayor and Ruth Bader Ginsburg agreed in a concurring opinion. The decision also made it clear that allowing nonmembers to opt out of paying dues toward union functions outside collective bargaining was unconstitutional and held that the unions “may not exact any funds from nonmembers without their affirmative consent.” In other words, unions would have to ask for nonmembers’ permission to collect political assessments and, possibly, any dues at all. “Individuals should not be compelled to subsidize private groups or private speech.” You could not charge them fees first for things they did not participate in and return them only if they complained. A distinction was made between a union that directly imposes fees on an individual for a political agenda yet in in the 2010 case Citizens United v. Federal Election Commission the court ruled that corporations could directly spend their resources on political campaigns. Shareholders have the right to sell their shares if they disagree where union member do not and are often mandated to be in unions or they are denied work.

The very idea that a person should pay a progressively higher percentage of their income based upon their God given skills flies in the face of certainly the Fifth Amendment Taking Clause, which reads:“[n]o person shall … be deprived of life, liberty, or property, without due process of law; nor shall private property be taken for public use, without just compensation.” Nowhere in the Constitution is there any hint that equal justice applies for all except if you make more than your neighbor. Progressive taxation also violated the Freedom of Religion under the First Amendment for one of the Ten Commandments is very clear on the subject;

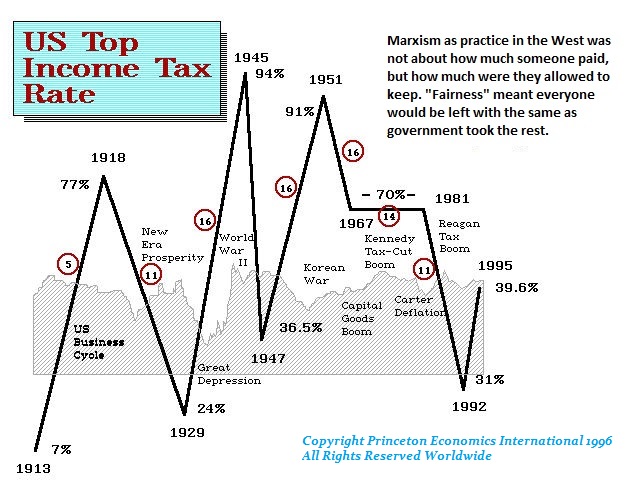

The Supreme Court has disposed of all constitutional questions about progression and had done so with remarkably little discussion during an era when Karl Marx was hail a major thinker before the Russian Communist Revolution in 1917 when it became known in practice far from the idealistic world it weaved. As is well known, the climax of the constitutional controversy in the United States over a federal income tax came in 1895 in the celebrated Pollock v. Farmers’ Loan & Trust Co., 157 U.S. 429 (1895). An income tax with explicitly graduated rates, enacted during the Civil War, was held to be constitutional in Springer v. United States, 102 U.S. 586 (i88o), however, the progressive feature of that tax was not in controversy during that case so it was not actually decided. What is usually remembered about these cases is that the Supreme Court adopted the views of taxpayers’ counsel that a tax on the income from real and personal property is a direct tax within the constitutional requirement that direct taxes be apportioned among the states, and that since these aspects of the tax were not separable the whole tax, the result was that the tax was patently unconstitutional. Nonetheless, lift the rug and we discover the origin of progressive taxation. The tax in question in 1894, had a flat rate of 2% on income but allowed each individual taxpayer an exemption of $4,ooo. Therefore, anyone earning more than $4,000 were discriminated against creating progressiveness which the public cheered as to be expected. That is the argument against democracy for it allows the majority to treat any minority unfairly.

Keep in mind this is BEFORE the Russian Revolution so Marxism is still an intellectual Utopia. In presenting their positions to the Court, counsel for the taxpayers did argue a substantial portion of their brief on the progressive nature of the tax in addition to the direct taxation argument. They maintained that the tax, because of the various progressive exemptions, violated the constitutional requirement of uniformity of indirect taxes and contravened the Due Process Clause of the Fifth Amendment. They focused on the $4,ooo exemption. On the issue of uniformity the Court divided four to four and therefore expressed no opinion. Even the dissenting opinions avoided discussing the issue. Only in the concurring opinion of Justice Field is the question or progressiveness even explored. Justice Steven Field (on bench 1863 – December 1, 1897) argued that it was indeed the arbitrariness of the exemption that would in itself have been a sufficient basis for invalidating the tax. The income tax law under consideration was marked by discriminating features which affect the whole law. It discriminated between those who receive an income of $4,ooo and those who do not. It was a blatant and arbitrary discrimination embodied within the whole legislation. Justice Field thus is the only Justice to directly address the issue whereas everyone else has avoided discussing the validity of progressive taxation because it benefits government. Justice Field wrote:

“It is difficult to conceive of a justifiable exemption law which should select single individuals or corporations, or single articles of property, and, taking them out of the class to which they belong, make them the subject of capricious legislative favor. Such favoritism could make no pretence to equality; it would lack the semblance of legitimate tax legislation.”

“It is difficult to conceive of a justifiable exemption law which should select single individuals or corporations, or single articles of property, and, taking them out of the class to which they belong, make them the subject of capricious legislative favor. Such favoritism could make no pretence to equality; it would lack the semblance of legitimate tax legislation.”

The income tax law under consideration is marked by discriminating features which affect the whole law. It discriminates between those who receive an income of four thousand dollars and those who do not. It thus vitiates, in my judgment, by this arbitrary discrimination, the whole legislation. Hamilton says in one of his papers (the Continentalist),

“the genius of liberty reprobates everything arbitrary or discretionary in taxation. It exacts that every man, by a definite and general rule, should know what proportion of his property the State demands; whatever liberty we may boast of in theory, it cannot exist in fact while [arbitrary] assessments continue.”

1 Hamilton’s Works, ed. 1885, 270. The legislation, in the discrimination it makes, is class legislation. Whenever a distinction is made in the burdens a law imposes or in the benefits it confers on any citizens by reason of their birth, or wealth, or religion, it is class legislation, and leads inevitably to oppression and abuses, and to general unrest and disturbance in society. It was hoped and believed that the great amendments to the Constitution which followed the late civil war had rendered such legislation impossible for all future time. But the objectionable legislation reappears in the act under consideration. It is the same in essential character as that of the English income statute of 1691, which taxed Protestants at a certain rate, Catholics, as a class, at double the rate of Protestants, and Jews at another and separate rate. Under wise and constitutional legislation, every citizen should contribute his proportion, however small the sum, to the support of the government, and it is no kindness to urge any of our citizens to escape from that obligation. If he contributes the smallest mite of his earnings to that purpose, he will have a greater regard for the government, and more self-respect (Page 157 U. S. 597) for himself, feeling that, though he is poor in fact, he is not a pauper of his government. And it is to be hoped that, whatever woes and embarrassments may betide our people, they may never lose their manliness and self-respect. Those qualities preserved, they will ultimately triumph over all reverses of fortune.

For the most part, there has been precious little argument that dealt directly with the issue of discrimination and the denial of justice for all. The arguments generally made were framing the issue focused upon the legislature’s discretion to set the level of exemptions and not the more challengeable principle of progressive rates from a constitutional perspective. At the federal level there are only three other relevant cases on this vital constitutional issue that supports Marxism and the denial of equal justice based upon class. In 1898 the Illinois inheritance tax came before the Supreme Court in Magoun v. Illinois Trust, 170 U.S. 283 (1898) The law provided for a graduated rate of inheritance tax applied where property was inherited by remote relatives or strangers. This discrimination in rates was challenged under the Equal Protection Clause of the Fourteenth Amendment. The Supreme Court disposed of the contention in a summary fashion, holding that since inheritance had always been regarded as a special privilege created by the state, the state was free to condition its exercise as it saw fit. The Court added that the classification according to size of inheritance seemed reasonable, saying, “When the legacies differ in substantial extent, if the rate increases, the benefit increases to greater degree. If there is unsoundness, it must be in the classification. The members of each class are treated alike — that is to say, all who inherit $10,000 are treated alike — all who inherit any other sum are treated alike” id/300. Obviously, the Court did avoided the distinction of the classes claiming everyone in each class was treated the same. In a strong dissent Justice Brewer found that the abandonment of the proportionate principle rendered the tax unequal and thus unconstitutional. He wrote: “But whatever may be the power of the legislature, Illinois had regulated the matter of descents and distributions, and had granted the right of testamentary disposition. And now, by this statute, upon property passing in accordance with its statutes, a tax is imposed — a tax unequal because not proportioned to the amount of the estate, unequal because based upon a classification purely arbitrary, to-wit, that of wealth, a tax directly and intentionally made unequal. I think the Constitution of the United States forbids such inequality” id/303. Justice Brewer also noted something very important. He also wrote: “It seems to be conceded that if this were a tax upon property, such increase in the rate of taxation could not be sustained; but, being a tax upon the succession, it is held that a different rule prevails” id/302. Here we again see that the Supreme Court has danced around the question of progressive taxation violates the Constitution.

The first landmark Equal Protection decision by the Supreme Court was Strauder v. West Virginia, 100 U.S. 303 (1879). A black man convicted of murder by an all-white jury challenged a West Virginia statute excluding blacks from serving on juries. Exclusion of blacks from juries, the Court concluded, was a denial of equal protection to black defendants, since the jury had been “drawn from a panel from which the State has expressly excluded every man of [the defendant’s] race.” At the same time, the Court explicitly allowed other types of discrimination, saying that states “may confine the selection to males, to freeholders, to citizens, to persons within certain ages, or to persons having educational qualifications. We do not believe the Fourteenth Amendment was ever intended to prohibit this. … Its aim was against discrimination because of race or color.” Keep in mind this was before the women’s right to vote which was predicated upon the Greek Democratic system where the head of a household voted as a representative (Congressman) of everyone who lived in that household. This predates the income tax and once you impose an income tax upon every citizen then the right to vote MUST attach to every citizen regardless of their race, religion, sex, or class.

Then the Supreme Court handed down the Knowlton v. Moore, 178 U.S. 41 (1900) decision upholding the federal inheritance tax of 1898 to justify the self-interest of government over the restraints intended by the Constitution. Here the tax contained graduated rates based on the amount of the inheritance. Justice White wrote the decision elaborating on the contention that the graduated rates did not violate the equal protection clause amazingly claiming that the clause required only geographical uniformity which was obviously in conflict with Strauder. Justice White wrote:

“The provision in Section 8 of Article I of the Constitution that “all duties, imports and excises shall be uniform throughout the United States” refers purely to a geographical uniformity, and is synonymous with the expression “to operate generally throughout the United States.”

Justice White’s limitation of Section 8 to geographical flies directly in the face of comments of the Framers. Take Thomas Jefferson for example, who in 1813 wrote to John Wayles Eppes (FE 9:398): “The public contributions should be as uniform as practicable from year to year, that our habits of industry and of expense may become adapted to them; and that they may be duly digested and incorporated with our annual economy.” I can find no such reference to equality was only geographical when the Constitution made it clear that the people themselves were the Sovereign – not government, i.e. “We the People”.

Justice White’s limitation of Section 8 to geographical flies directly in the face of comments of the Framers. Take Thomas Jefferson for example, who in 1813 wrote to John Wayles Eppes (FE 9:398): “The public contributions should be as uniform as practicable from year to year, that our habits of industry and of expense may become adapted to them; and that they may be duly digested and incorporated with our annual economy.” I can find no such reference to equality was only geographical when the Constitution made it clear that the people themselves were the Sovereign – not government, i.e. “We the People”.

It was argued in Knowlton that progressive tax rates were “so repugnant to fundamental principles of equality and justice, that the law should be held to be void, even although it transgressed no express limitation in the Constitution.” Justice White dismissed this point completely saying it was disposed of in the Magown case, which was simply not true. Effectively, the bottom-line was this was the prerogative of a king and left to his discretion rather than subject to judicial review. It would seem that the government would then have the power to arbitrarily claim that any individual who earns more than $1 million can be arbitrarily subjected to the confiscation of all his assets based upon class at the full discretion of the mob headed by politicians. This surely cannot be justified under the American Revolution. Even the Declaration of Independence included the complaint that the king had assented to Parliament’s laws that “impos[e] Taxes on us without our Consent.” This reflected the fact that American Colonists had no right to object in Parliament. Here we find Justice White essentially upholding the prerogative of the government to do the same since any politician represents only the majority against any minority denying them the right to consent.

After the Knowlton case it was still possible to argue that the question of the constitutionality of a progressive tax on income as contrasted to progressive death taxes had NOT been foreclosed. Nothing about progression had been decided in the Pollock case with the Magoun case turning on the complete discretion of a state to impose conditions on inheritance. The Knowlton case contained merely dictum (general language) without expressly holding the question of progressive taxation. It merely asserted that the issue of progression was a matter of economic controversy properly within the area of legislative discretion and that the uniformity clause was strangely geographical. Therefore, if the uniformity clause of Section 8 was geographical, it still prohibited arbitrary taxation saying everyone who lives in New York will pay a higher rate of taxes compared to the less rich state of Louisiana. So progressive taxation is clearly prohibited based upon where you live. While the Knowlton decision simply dismissed the argument as settled in the Magoun case, there was in fact no such discussion no less holding. This merely demonstrates how devious the Supreme Court can be to justify the whims of government against the people.

The question of an income tax progression finally came to the Supreme Court in Brushaber v. Union Pacific, 240 U.S. 1 (1916) dealing with the income tax enacted under the Sixteenth Amendment. Unfortunately, Chief Justice White once again grabbed the case and his bias is clearly visible in his writing. He delivered the decision for a unanimous court in time of War. He disposed of the question in a very curt and summary fashion once again. Justice White’s decision in the Knowlton case made it clear he would have nothing to do with a fair constitutional decision regarding taxes. In the Brushaber case, White noted that the Due Process Clause of the Fifth Amendment is not a limitation on the taxing power.

Fifth Amendment

“No person shall be held to answer for a capital, or otherwise infamous crime, unless on a presentment or indictment of a Grand Jury, except in cases arising in the land or naval forces, or in the Militia, when in actual service in time of War or public danger; nor shall any person be subject for the same offence to be twice put in jeopardy of life or limb; nor shall be compelled in any criminal case to be a witness against himself, nor be deprived of life, liberty, or property, without due process of law; nor shall private property be taken for public use, without just compensation.”

It is true that Article I, Section 8 gives Congress the power to “lay and collect taxes, duties, imports, and excises.” The Constitution allows Congress to tax in order to “provide for the common defense and general welfare.” For you see, the king had no right to tax the people without their consent. The only time the king could ask for taxation was to defend the nation in time of war. Otherwise, the king made money from fines, penalties, and indirect taxes. The Constitution was clearly establishing the same taxing structure.

Justice White ignored all references to the taking of property by the state arbitrarily. He went on to observe that there was no express constitutional provision prohibiting progressive taxation, the progressive feature of the tax causes it to transcend the conception of all taxation and to be a mere arbitrary abuse of power which must be treated as a violation of Due Process of Law, which must be equal justice for all. Justice White further disregards the fact that there was a total lack of legal reasoning to support his ruling once again claiming that was decided in Knowlton and it was foreclosed by that ruling which again was not true. Clearly, Justice White abused the power of the bench to justify whatever the government wanted to do even arbitrarily implying it was the prerogative of the legislature further denying the tripartite structure of government. His decision was a total disgrace to Due Process and denied the right to be heard by the people. Keep in mind that he was first a State Senator back in 1874 and the a Federal Senator representing Louisiana in Washington in 1891. Clearly, he was a politician before being a judge and that reflects his biased support of unbridled power of the legislature.

American Indians pay federal taxes on their income and capital gains, just as any other American does. However, American Indians do not pay taxes on moneys earned from their land allotments, since those lease fees are from the government and were negotiated as part of a treaty. While earning money on the reservation, American Indians also do not pay state, corporate, or state license fees for income or enterprises on the reservations due to the sovereign status of the reservation. While earning money off the reservation, however, American Indians are subject to state income, corporate, and licensing taxes. The Amish pay income taxes because the Bible said: “paying unto Caesar what is Caesar’s.” However, they DO NOT pay Social Security taxes and are exempt because of their religious beliefs.

Adam Smith is just about every great thinker, have written that it is a fundamental principle of government like the Tenth Commandment that it should be obvious that any system of taxation should be fair. Smith in his “An Inquiry into the Nature and Causes of the Wealth of Nations”, made it abundantly clear that “The evident justice and utility of the foregoing maxims have recommended them more or less to the attention of all nations. All nations have endeavoured, to the best of their judgment, to render their taxes as equal as they could contrive; as certain, as convenient to the contributor, both in the time and in the mode of payment, and, in proportion to the revenue which they brought to the prince, as little burdensome to the people” (Book Five, Chapter II, PART 2 Of Taxes).

Adam Smith is just about every great thinker, have written that it is a fundamental principle of government like the Tenth Commandment that it should be obvious that any system of taxation should be fair. Smith in his “An Inquiry into the Nature and Causes of the Wealth of Nations”, made it abundantly clear that “The evident justice and utility of the foregoing maxims have recommended them more or less to the attention of all nations. All nations have endeavoured, to the best of their judgment, to render their taxes as equal as they could contrive; as certain, as convenient to the contributor, both in the time and in the mode of payment, and, in proportion to the revenue which they brought to the prince, as little burdensome to the people” (Book Five, Chapter II, PART 2 Of Taxes).

The sole exception up until the mid-19th Century was Karl Marx. Clearly, it is Marx who has completely altered government, dominated the thinking of judges, and single-handedly destroyed our posterity. Once Marx justified government arbitrariness and discrimination by class pretending it is no different than in England when they taxed Catholics at twice the rate of Protestants, human rights have steadily declined. As Justice Field wrote that unfair taxation “leads inevitably to oppression and abuses, and to general unrest and disturbance in society.” Indeed, all revolutions historically are set in motion by abuse of taxation.

Unless Class Warfare is formally declared UNCONSTITUTIONAL under the First Amendment, Due Process, and Equal Protection, then it will be this battle between the left and the right that leads to devastation and blood in the streets no different than the civil war which up-ended Russia in 1917. You cannot have a system of equal justice for all as long as one group can claim they are entitled to oppress others for race, religion, or social status. It is time that a group of lawyers for once defend the principles of our nation and challenge this tax code on the grounds of Due Process and Equal Protection, but also the First Amendment whereby the Tenth Amendment prohibits coveting your neighbor’s goods. If this does not come to an end, we will ultimately see blood in the streets. The gyrations of the tax code constantly moving up and down has sent more corporations offshore simply because they need stability. Would you agree to pay rent where you landlord has the right to arbitrarily raise your rent because you got a raise?

Pollock v. Farmers’ Loan & Trust Co., 157 U.S. 429 (1895)

MR. JUSTICE FIELD.

I also desire to place my opinion on record upon some of the important questions discussed in relation to the direct and indirect taxes proposed by the income tax law of 1894.

Page 157 U. S. 587

Several suits have been instituted in state and Federal courts, both at law and in equity, to test the validity of the provisions of the law, the determination of which will necessitate careful and extended consideration.

The subject of taxation in the new government which was to be established created great interest in the convention which framed the Constitution, and was the cause of much difference of opinion among its members and earnest contention between the States. The great source of weakness of the confederation was its inability to levy taxes of any kind for the support of its government. To raise revenue, it was obliged to make requisitions upon the States, which were respected or disregarded at their pleasure. Great embarrassments followed the consequent inability to obtain the necessary funds to carry on the government. One of the principal objects of the proposed new government was to obviate this defect of the confederacy by conferring authority upon the new government by which taxes could be directly laid whenever desired. Great difficulty in accomplishing this object was found to exist. The States bordering on the ocean were unwilling to give up their right to lay duties upon imports, which were their chief source of revenue. The other States, on the other hand, were unwilling to make any agreement for the levying of taxes directly upon real and personal property, the smaller States fearing that they would be overborne by unequal burdens forced upon them by the action of the larger States. In this condition of things, great embarrassment was felt by the members of the convention. It was feared at times that the effort to form a new government would fail. But happily, a compromise was effected by an agreement that direct taxes should be laid by Congress by apportioning them among the States according to their representation. In return for this concession by some of the States, the other States bordering on navigable waters consented to relinquish to the new government the control of duties, imposts, and excises, and the regulation of commerce, with the condition that the duties, imposts, and excises should be uniform throughout the United States. So that, on the one

Page 157 U. S. 588

hand, anything like oppression or undue advantage of any one State over the others would be prevented by the apportionment of the direct taxes among the States according to their representation, and, on the other hand, anything like oppression or hardship in the levying of duties, imposts, and excises would be avoided by the provision that they should be uniform throughout the United States. This compromise was essential to the continued union and harmony of the States. It protected every State from being controlled in its taxation by the superior numbers of one or more other States.

The Constitution accordingly, when completed, divided the taxes which might be levied under the authority of Congress into those which were direct and those which were indirect. Direct taxes, in a general and large sense, may be described as taxes derived immediately from the person, or from real or personal property, without any recourse therefrom to other sources for reimbursement. In a more restricted sense, they have sometimes been confined to taxes on real property, including the rents and income derived therefrom. Such taxes are conceded to be direct taxes, however taxes on other property are designated, and they are to be apportioned among the States of the Union according to their respective numbers. The second section of article I of the Constitution declares that representatives and direct taxes shall be thus apportioned. It had been a favorite doctrine in England and in the colonies, before the adoption of the Constitution, that taxation and representation should go together. The Constitution prescribes such apportionment among the several States according to their respective numbers, to be determined by adding to the whole number of free persons, including those bound to service for a term of years, and excluding Indians not taxed, three-fifths of all other persons.

Some decisions of this court have qualified or thrown doubts upon the exact meaning of the words “direct taxes.” Thus, in Springer v. United States, 102 U. S. 586, it was held that a tax upon gains, profits, and income was an excise or duty, and not a direct tax within the meaning of the Constitution, and

Page 157 U. S. 589

that its imposition was not therefore unconstitutional. And in Pacific Insurance Co. v. Soule, 7 Wall. 433, it was held that an income tax or duty upon the amounts insured, renewed or continued by insurance companies, upon the gross amounts of premiums received by them and upon assessments made by them, and upon dividends and undistributed sums, was not a direct tax, but a duty or excise.

In the discussions on the subject of direct taxes in the British Parliament, an income tax has been generally designated as a direct tax, differing in that respect from the decision of this court in Springer v. United States. But whether the latter can be accepted as correct or otherwise, it does not affect the tax upon real property and its rents and income as a direct tax. Such a tax is by universal consent recognized to be a direct tax.

As stated, the rents and income of real property are included in the designation of direct taxes as part of the real property. Such has been the law in England for centuries, and in this country from the early settlement of the colonies, and it is strange that any member of the legal profession should, at this day, question a doctrine which has always been thus accepted by common law lawyers. It is so declared in approved treatises upon real property and in accepted authorities on particular branches of real estate law, and has been so announced in decisions in the English courts and our own courts without number. Thus, in Washburn on Real Property, it is said that

“a devise of the rents and profits of land, or the income of land, is equivalent to a devise of the land itself, and will be for life or in fee according to the limitation expressed in the devise.”

Vol. 2, p. 695, § 30.

In Jarman on Wills, Vol. 1, page 40, it is laid down that

“a devise of the rents and profits or of the income of land passes the land itself both at law and in equity; a rule, it is said, founded on the feudal law, according to which the whole beneficial interest in the land consisted in the right to take the rents and profits. And since the act 1 Vict. c. 26, such a devise carries the fee simple; but before that act, it carried no more than an estate for life unless words of inheritance were

Page 157 U. S. 590

added.”

Mr. Jarman cites numerous authorities in support of his statement. South v. Alleine, 1 Salk. 228; Doe d. Goldin v. Lakeman, 2 B. & Ad. 30, 42; Johnson v. Arnold, 1 Ves.Sen. 171; Baines v. Dixon, 1 Ves.Sen. 42; Mannox v. Greener, L.R. 14 Eq. 46; Blann v. Bell, 2 De G., M. & G. 781; Plenty v. West, 6 C.B. 201.

Coke upon Littleton says:

“If a man seised of lands in fee by his deed granteth to another the profit of those lands, to have and to hold to him and his heires, and maketh livery secundum formam chartae, the whole land itselfe doth passe; for what is the land but the profits thereof?”

Lib. 1, cap. 1, § 1, p. 4b.

In Doe d. Goldin v. Lakeman, Lord Tenterden, Chief Justice of the Court of King’s Bench, to the same effect, said: “It is an established rule that a devise of the rents and profits is a devise of the land.” And in Johnson v. Arnold, Lord Chancellor Hardwicke reiterated the doctrine that a “devise of the profits of lands is a devise of the lands themselves.”

The same rule is announced in this country; the Court of Errors of New York in Paterson v. Ellis, 11 Wend. 29, 98, holding that the

“devise of the interest or of the rents and profits is a devise of the thing itself, out of which that interest or those rents and profits may issue;”

and the Supreme Court of Massachusetts, in Reed v. Reed, 9 Mass. 372, 374, that “a devise of the income of lands is the same in its effect as a devise of the lands.” The same view of the law was expressed in Anderson v. Greble, 1 Ashmead (Penn.) 136, 138, King, the president of the court, stating: “I take it to be a well settled rule of law that, by a devise of the rent, profits, and income of land, the land itself passes.” Similar adjudications might be repeated almost indefinitely. One may have the reports of the English courts examined for several centuries without finding a single decision or even a dictum of their judges in conflict with them. And what answer do we receive to these adjudications? Those rejecting them furnish no proof that the framers of the Constitution did not follow them, as the great body of the people of the country then did. An incident which occurred in this court and room twenty

Page 157 U. S. 591

years ago may have become a precedent. To a powerful argument then being made by a distinguished counsel on a public question, one of the judges exclaimed that there was a conclusive answer to his position, and that was that the court was of a different opinion. Those who decline to recognize the adjudications cited may likewise consider that they have a conclusive answer to them in the fact that they also are of a different opinion. I do not think so. The law as expounded for centuries cannot be set aside or disregarded because some of the judges are now of a different opinion from those who, a century ago, followed it in framing our Constitution.

Hamilton, speaking on the subject, asks: “What, in fact, is property but a fiction without the beneficial use of it?” And adds: “In many cases, indeed, the income or annuity is the property itself.” 3 Hamilton’s Works, Putnam’s ed. 34.

It must be conceded that whatever affects any element that gives an article its value, in the eye of the law affects the article itself.

In Brown v. Maryland, 12 Wheat. 419, 25 U. S. 444, it was held that a tax on the occupation of an importer is the same as a tax on his imports, and, as such, was invalid. It was contended that the State might tax occupations, and that this was nothing more, but the court said, by Chief Justice Marshall (p. 25 U. S. 444):

“It is impossible to conceal from ourselves that this is varying the form without varying the substance. It is treating a prohibition which is general as if it were confined to a particular mode of doing the forbidden thing. All must perceive that a tax on the sale of an article imported only for sale is a tax on the article itself.”

In Weston v. Charleston, 2 Pet. 449, it was held that a tax upon stock issued for loans to the United States was a tax upon the loans themselves, and equally invalid. In Dobbins v. Commissioners, 16 Pet. 435, it was held that the salary of an officer of the United States could not be taxed if the office was itself exempt. In Almy v. California, 24 How. 169, it was held that a duty on a bill of lading was the same thing as a duty on the article transported. In Cook v. Pennsylvania, 97 U. S. 566 it was held that a tax upon the amount

Page 157 U. S. 592

of sales of goods made by an auctioneer was a tax upon the goods sold. In Philadelphia & Southern Steamship Co. v. Pennsylvania, 122 U. S. 326, and Leloup v. Mobile, 127 U. S. 640, 127 U. S. 648, it was held that a tax upon the income received from interstate commerce was a tax upon the commerce itself, and equally unauthorized. The same doctrine was held in People v. Commissioners of Taxes, 90 N.Y. 63; State Freight Tax, 15 Wall. 232, 82 U. S. 274; Welton v. Missouri, 91 U. S. 275, 91 U. S. 278, and in Fargo v. Michigan, 121 U. S. 230.

The law, so far as it imposes a tax upon land by taxation of the rents and income thereof, must therefore fail, as it does not follow the rule of apportionment. The Constitution is imperative in its direction on this subject, and admits of no departure from them.

But the law is not invalid merely in its disregard of the rule of apportionment of the direct tax levied. There is another and an equally cogent objection to it. In taxing incomes other than rents and profits of real estate, it disregards the rule of uniformity which is prescribed in such cases by the Constitution. The eighth section of the first article of the Constitution declares that

“the Congress shall have power to lay and collect taxes, duties, imposts, and excises, to pay the debts and provide for the common defence and general welfare of the United States; but all duties, imposts, and excises shall be uniform throughout the United States.”

Excise are a species of tax consisting generally of duties laid upon the manufacture, sale, or consumption of commodities within the country, or upon certain callings or occupations, often taking the form of exactions for licenses to pursue them. The taxes created by the law under consideration as applied to savings banks, insurance companies, whether of fire, life, or marine, to building or other associations, or to the conduct of any other kind of business, are excise taxes, and fall within the requirement, so far as they are laid by Congress, that they must be uniform throughout the United States.

The uniformity thus required is the uniformity throughout the United States of the duty, impost, and excise levied. That is, the tax levied cannot be one sum upon an article at one

Page 157 U. S. 593

place and a different sum upon the same article at another place. The duty received must be the same at all places throughout the United States, proportioned to the quantity of the article disposed of or the extent of the business done. If, for instance, one kind of wine or grain or produce has a certain duty laid upon it proportioned to its quantity in New York, it must have a like duty proportioned to its quantity when imported at Charleston or San Francisco, or if a tax be laid upon a certain kind of business proportioned to its extent at one place, it must be a like tax on the same kind of business proportioned to its extent at another place. In that sense, the duty must be uniform throughout the United States. It is contended by the government that the Constitution only requires an uniformity geographical in its character. That position would be satisfied if the same duty were laid in all the States, however variant it might be in different places of the same State. But it could not be sustained in the latter case without defeating the equality, which is an essential element of the uniformity required, so far as the same is practicable.

In United States v. Singer, 15 Wall. 111, 82 U. S. 121, a tax was imposed upon a distiller, in the nature of an excise, and the question arose whether, in its imposition upon different distillers, the uniformity of the tax was preserved, and the court said:

“The law is not in our judgment subject to any constitutional objection. The tax imposed upon the distiller is in the nature of an excise, and the only limitation upon the power of Congress in the imposition of taxes of this character is that they shall be ‘uniform throughout the United States.’ The tax here is uniform in its operation; that is, it is assessed equally upon all manufacturers of spirits wherever they are. The law does not establish one rule for one distiller and a different rule for another, but the same rule for all alike.”

In the Head Money Cases, 112 U. S. 580, 112 U. S. 594, a tax was imposed upon the owners of steam vessels for each passenger landed at New York from a foreign port, and it was objected that the tax was not levied by any rule of uniformity, but the court, by Justice Miller, replied:

“The tax is uniform when

Page 157 U. S. 594

it operates with the same force and effect in every place where the subject of it is found. The tax in this case, which, as far as it can be called a tax, is an excise duty on the business of bringing passengers from foreign countries into this by ocean navigation, is uniform, and operates precisely alike in every port of the United States where such passengers can be landed.”

In the decision in that case in the Circuit Court, 18 Fed.Rep. 135, 139, Mr. Justice Blatchford, in addition to pointing out that “the act was not passed in the exercise of the power of laying taxes,” but was a regulation of commerce, used the following language:

“Aside from this, the tax applies uniformly to all steam and sail vessels coming to all ports in the United States, from all foreign ports, with all alien passengers. The tax being a license tax on the business, the rule of uniformity is sufficiently observed if the tax extends to all persons of the class selected by Congress; that is, to all owners of such vessels. Congress has the exclusive power of selecting the class. It has regulated that particular branch of commerce which concerns the bringing of alien passengers,”

and that taxes shall be levied upon such property as shall be prescribed by law. The object of this provision was to prevent unjust discriminations. It prevents property from being classified and taxed, as classed, by different rules. All kinds of property must be taxed uniformly or be entirely exempt. The uniformity must be coextensive with the territory to which the tax applies.

Mr. Justice Miller, in his lectures on the Constitution (N.Y. 1891) pp. 240, 241, said of taxes levied by Congress:

“The tax must be uniform on the particular article, and it is uniform, within the meaning of the constitutional requirement, if it is made to bear the same percentage over all the United States. That is manifestly the meaning of this word as used in this clause. The framers of the Constitution could not have meant to say that the government, in raising its revenues, should not be allowed to discriminate between the articles which it should tax.”

In discussing generally the requirement of uniformity found in state constitutions, he said:

“The difficulties in the way of this construction have, however, been very largely obviated by the meaning of the word

Page 157 U. S. 595

‘uniform’ which has been adopted, holding that the uniformity must refer to articles of the same class. That is, different articles may be taxed at different amounts, provided the rate is uniform on the same class everywhere, with all people, and at all times.”

One of the learned counsel puts it very clearly when he says that the correct meaning of the provisions requiring duties, imposts, and excises to be “uniform throughout the United States” is that the law imposing them should “have an equal and uniform application in every part of the Union.”

If there were any doubt as to the intention of the States to make the grant of the right to impose indirect taxes subject to the condition that such taxes shall be in all respects uniform and impartial, that doubt, as said by counsel, should be resolved in the interest of justice, in favor of the taxpayer.

Exemptions from the operation of a tax always create inequalities. Those not exempted must, in the end, bear an additional burden or pay more than their share. A law containing arbitrary exemptions can in no just sense be termed uniform. In my judgment, Congress has rightfully no power, at the expense of others, owning property of a like character, to sustain private trading corporations, such as building and loan associations, savings banks, and mutual life, fire, marine, and accident insurance companies, formed under the laws of the various States, which advance no national purpose or public interest and exist solely for the pecuniary profit of their members.

Where property is exempt from taxation, the exemption, as has been justly stated, must be supported by some consideration that the public, and not private, interests will be advanced by it. Private corporations and private enterprises cannot be aided under the pretence that it is the exercise of the discretion of the legislature to exempt them. Loan Association v. Topeka, 20 Wall. 655; Parkersburg v. Brown, 106 U. S. 487; Barbour v. Louisville Board of Trade, 82 Kentucky 645, 654, 655; Lexington v. McQuillan’s Heirs, 9 Dana, 513, 516, 517, and Sutton’s Heirs v. Louisville, 5 Dana, 28, 31.

Cooley, in his treatise on Taxation (2d ed. 215), justly

Page 157 U. S. 596

observes that:

“It is difficult to conceive of a justifiable exemption law which should select single individuals or corporations, or single articles of property, and, taking them out of the class to which they belong, make them the subject of capricious legislative favor. Such favoritism could make no pretence to equality; it would lack the semblance of legitimate tax legislation.”

The income tax law under consideration is marked by discriminating features which affect the whole law. It discriminates between those who receive an income of four thousand dollars and those who do not. It thus vitiates, in my judgment, by this arbitrary discrimination, the whole legislation. Hamilton says in one of his papers (the Continentalist),

“the genius of liberty reprobates everything arbitrary or discretionary in taxation. It exacts that every man, by a definite and general rule, should know what proportion of his property the State demands; whatever liberty we may boast of in theory, it cannot exist in fact while [arbitrary] assessments continue.”

1 Hamilton’s Works, ed. 1885, 270. The legislation, in the discrimination it makes, is class legislation. Whenever a distinction is made in the burdens a law imposes or in the benefits it confers on any citizens by reason of their birth, or wealth, or religion, it is class legislation, and leads inevitably to oppression and abuses, and to general unrest and disturbance in society. It was hoped and believed that the great amendments to the Constitution which followed the late civil war had rendered such legislation impossible for all future time. But the objectionable legislation reappears in the act under consideration. It is the same in essential character as that of the English income statute of 1691, which taxed Protestants at a certain rate, Catholics, as a class, at double the rate of Protestants, and Jews at another and separate rate. Under wise and constitutional legislation, every citizen should contribute his proportion, however small the sum, to the support of the government, and it is no kindness to urge any of our citizens to escape from that obligation. If he contributes the smallest mite of his earnings to that purpose, he will have a greater regard for the government, and more self-respect

Page 157 U. S. 597

for himself, feeling that, though he is poor in fact, he is not a pauper of his government. And it is to be hoped that, whatever woes and embarrassments may betide our people, they may never lose their manliness and self-respect. Those qualities preserved, they will ultimately triumph over all reverses of fortune.

There is nothing in the nature of the corporations or associations exempted in the present act, or in their method of doing business, which can be claimed to be of a public or benevolent nature. They differ in no essential characteristic in their business from “all other corporations, companies, or associations doing business for profit in the United States.” Act of August 15, 1894, c. 349, § 32.

A few words as to some of them, the extent of their capital and business, and of the exceptions made to their taxation:

1st. A to mutual savings banks. — Under income tax laws prior to 1870, these institutions were specifically taxed. Under the new law, certain institutions of this class are exempt, provided the shareholders do not participate in the profits, and interest and dividends are only paid to the depositors. No limit is fixed to the property and income thus exempted — it may be $100,000 or $100,000,000. One of the counsel engaged in this case read to us during the argument from the report of the Comptroller of the Currency, sent by the President to Congress December 3, 1894, a statement to the effect that the total number of mutual savings banks exempted was 646, and the total number of stock savings banks was 378, and showed that they did the same character of business and took in the money of depositors for the purpose of making it bear interest, with profit upon it in the same way, and yet the 646 are exempt and the 378 are taxed. He also showed that the total deposits in savings banks were $1,748,000,000.

2d. As to mutual insurance corporations. — These companies were taxed under previous income tax laws. They do business somewhat differently from other companies, but they conduct a strictly private business in which the public has no interest, and have been often held not to be benevolent or charitable organizations.

Page 157 U. S. 598

The sole condition for exempting them under the present law is declared to be that they make loans to or divide their profits among their members, or depositors or policyholders. Every corporation is carried on, however, for the benefit of its members, whether stockholders or depositors or policyholders. If it is carried on for the benefit of its shareholders, every dollar of income is taxed; if it is carried on for the benefit of its policyholders or depositors, who are but another class of shareholders, it is wholly exempted. In the State of New York, the act exempts the income from over $1,00,000,000 of property of these companies. The leading mutual life insurance company has property exceeding 204,000,000 in value, the income of which is wholly exempted. The insertion of the exemption is stated by counsel to have saved that institution fully $200,000 a year over other insurance companies and associations having similar property and carrying on the same business, simply because such other companies or associations divide their profits among their shareholders, instead of their policyholders.

3d. As to building an loan, associations. — The property of these institutions is exempted from taxation to the extent of millions. They are in no sense benevolent or charitable institutions, and are conducted solely for the pecuniary profit of their members. Their assets exceed the capital stock of the national banks of the country. One, in Dayton, Ohio, has a capital of $10,000,000, and Pennsylvania has $65,000,000 invested in these associations. The census report submitted to Congress by the President, May 1, 1894, shows that their property in the United States amounts to over $628,000,000. Why should these institutions and their immense accumulations of property be singled out for the special favor of Congress and be freed from their just, equal, and proportionate share of taxation when others engaged under different names, in similar business, are subjected to taxation by this law? The aggregate amount of the saving to these associations, by reason of their exemption, is over $600,000 a year. If this statement of the exemptions of corporations under the law of Congress, taken from the carefully prepared briefs of counsel

Page 157 U. S. 599

and from reports to Congress, will not satisfy parties interested in this case that the act in question disregards, in almost every line and provision, the rule of uniformity required by the Constitution, then “neither will they be persuaded, though one rose from the dead.” That there should be any question or any doubt on the subject surpasses my comprehension. Take the case of mutual savings banks and stock savings banks. They do the same character of business, and in the same way use the money of depositors, loaning it at interest for profit, yet 646 of them, under the law before us, are exempt from taxation on their income, and 378 are taxed upon it. How the tax on the income of one kind of these banks can be said to be laid upon any principle of uniformity, when the other is exempt from all taxation, I repeat, surpasses my comprehension.

But there are other considerations against the law which are equally decisive. They relate to the uniformity and equality required in all taxation, national and State; to the invalidity of taxation by the United States of the income of the bonds and securities of the States and of their municipal bodies, and the invalidity of the taxation of the salaries of the judges of the United States courts.

As stated by counsel: “There is no such thing in the theory of our national government as unlimited power of taxation in Congress. There are limitations,” as he justly observes,

“of its powers arising out of the essential nature of all free governments; there are reservations of individual rights, without which society could not exist, and which are respected by every government. The right of taxation is subject to these limitations.”

Loan Association v. Topeka, 20 Wall. 635, and Parkersburg v. Brown, 106 U. S. 487.

The inherent and fundamental nature and character of a tax is that of a contribution to the support of the government, levied upon the principle of equal and uniform apportionment among the persons taxed, and any other exaction does not come within the legal definition of a tax.

This inherent limitation upon the taxing power forbids the imposition of taxes which are unequal in their operation upon

Page 157 U. S. 600

similar kinds of property, and necessarily strikes down the gross and arbitrary distinctions in the income law as passed by Congress. The law, as we have seen, distinguishes in the taxation between corporations by exempting the property of some of them from taxation and levying the tax on the property of others when the corporations do not materially differ from one another in the character of their business or in the protection required by the government. Trifling differences in their modes of business, but not in their results, are made the ground and occasion of the greatest possible differences in the amount of taxes levied upon their income, showing that the action of the legislative power upon them has been arbitrary and capricious and sometimes merely fanciful.

There was another position taken in this case which is not the least surprising to me of the many advanced by the upholders of the law, and that is that, if this court shall declare that the exemptions and exceptions from taxation extended to the various corporations mentioned, fire, life, and marine insurance companies, and to mutual savings banks, building, and loan associations violate the requirement of uniformity, and are therefore void, the tax as to such corporations can be enforced, and that the law will stand as though the exemptions had never been inserted. This position does not, in my judgment, rest upon any solid foundation of law or principle. The abrogation or repeal of an unconstitutional or illegal provision does not operate to create and give force to any enactment or part of an enactment which Congress has not sanctioned and promulgated. Seeming support of this singular position is attributed to the decision of this court in Huntington v. Worthen, 120 U. S. 97. But the examination of that case will show that it does not give the slightest sanction to such a doctrine. There, the constitution of Arkansas had provided that all property subject to taxation should be taxed according to its value, to be ascertained in such manner as the general assembly should direct, making the same equal and uniform throughout the State, and certain public property was declared by statute to be exempt from taxation, which statute was subsequently held to be unconstitutional. The court decided that the unconstitutional

Page 157 U. S. 601

part of the enactment, which was separable from the remainder, could be omitted and the remainder enforced; a doctrine undoubtedly sound, and which has never, that I am aware of, been questioned. But that is entirely different from the position here taken, that exempted things can be taxed by striking out their exemption.

The law of 1894 says there shall be assessed, levied, and collected, “except as hereinafter otherwise provided,” two percentum of the amount, etc. If the exceptions are stricken out, there is nothing to be assessed and collected except what Congress has otherwise affirmatively ordered. Nothing less can have the force of law. This court is impotent to pass any law on the subject. It has no legislative power. I am unable, therefore, to see how we can, by declaring an exemption or exception invalid, thereby give effect to provisions as though they were never exempted. The court, by declaring the exemptions invalid, cannot, by any conceivable ingenuity, give operative force as enacting clauses to the exempting provisions. That result is not within the power of man.

The law is also invalid in its provisions authorizing the taxation of the bonds and securities of the States and of their municipal bodies. It is objected that the cases pending before us do not allege any threatened attempt to tax the bonds or securities of the State, but only of municipal bodies of the States. The law applies to both kinds of bonds and securities, those of the States as well as those of municipal bodies, and the law of Congress we are examining, being of a public nature, affecting the whole community, having been brought before us and assailed as unconstitutional in some of its provisions, we are at liberty, and I think it is our duty, to refer to other unconstitutional features brought to our notice in examining the law, though the particular points of their objection may not have been mentioned by counsel. These bonds and securities are as important to the performance of the duties of the State as like bonds and securities of the United States are important to the performance of their duties, and are as exempt from the taxation of the United States as the former are exempt from the taxation of the States. As stated by Judge

Page 157 U. S. 602

Cooley in his work on the principles of constitutional law:

“The power to tax, whether by the United States or by the States, is to be construed in the light of, and limited by, the fact that the States and the Union are inseparable, and that the Constitution contemplates the perpetual maintenance of each with all its constitutional powers, unembarrassed and unimpaired by any action of the other. The taxing power of the Federal government does not therefore extend to the means or agencies through or by the employment of which the States perform their essential functions, since, if these were within its reach, they might be embarrassed, and perhaps wholly paralyzed, by the burdens it should impose.”

“That the power to tax involves the power to destroy; that the power to destroy may defeat and render useless the power to create; that there is a plain repugnance in conferring on one government a power to control the constitutional measures of another, which other, in respect to those very measures, is declared to be supreme over that which exerts the control — are propositions not to be denied.”

“It is true that taxation does not necessarily and unavoidably destroy, and that to carry it to the excess of destruction would be an abuse not to be anticipated, but the very power would take from the States a portion of their intended liberty of independent action within the sphere of their powers, and would constitute to the State a perpetual danger of embarrassment and possible annihilation. The Constitution contemplates no such shackles upon state powers, and, by implication, forbids them.”

The Internal Revenue Act of June 30, 1864, in section 122, provided that railroad and certain other companies specified, indebted for money for which bonds had been issued upon which interest was stipulated to be paid, should be subject to pay a tax of five percent on the amount of all such interest, to be paid by the corporations and by them deducted from the interest payable to the holders of such bonds, and the question arose in United States v. Railroad Co., 17 Wall. 322, 84 U. S. 327, whether the tax imposed could be thus collected from the revenues of a city owning such bonds. This court answered the question as follows:

“There is no dispute about the general

Page 157 U. S. 603

rules of the law applicable to this subject. The power of taxation by the Federal government upon the subjects and in the manner prescribed by the act we are considering is undoubted. There are, however, certain departments which are excepted from the general power. The right of the States to administer their own affairs through their legislative, executive, and judicial departments, in their own manner through their own agencies, is conceded by the uniform decisions of this court, and by the practice of the Federal government from its organization. This carries with it an exemption of those agencies and instruments from the taxing power of the Federal government. If they may be taxed lightly, they may be taxed heavily; if justly, oppressively. Their operation may be impeded and may be destroyed if any interference is permitted. Hence, the beginning of such taxation is not allowed on the one side, is not claimed on the other.”

And again:

“A municipal corporation like the city of Baltimore is a representative not only of the State, but it is a portion of its governmental power. It is one of its creatures, made for a specific purpose, to exercise within a limited sphere the powers of the State. The State may withdraw these local powers of government at pleasure, and may, through its legislature or other appointed channels, govern the local territory as it governs the State at large. It may enlarge or contract its powers or destroy its existence. As a portion of the State in the exercise of a limited portion of the powers of the State, its revenues, like those of the State, are not subject to taxation.”

In Collector v. Day, 11 Wall. 113, 78 U. S. 124, the court, speaking by Mr. Justice Nelson, said:

“The general government and the States, although both exist within the same territorial limits, are separate and distinct sovereignties, acting separately and independently of each other within their respective spheres. The former, in its appropriate sphere, is supreme, but the States, within the limits of their powers not granted or, in the language of the tenth amendment, ‘reserved,’ are as independent of the general government as that government within its sphere is independent of the States. ”

Page 157 U. S. 604

According to the census reports, the bonds and securities of the States amount to the sum of $1,243,268,000, on which the income or interest exceeds the sum of $65,000,000 per annum, and the annual tax of two percent upon this income or interest would be $1,300,000.

The law of Congress is also invalid in that it authorizes a tax upon the salaries of the judges of the courts of the United States, against the declaration of the Constitution that their compensation shall not be diminished during their continuance in office. The law declares that a tax of two percent shall be assessed, levied, and collected and paid annually upon the gains, profits, and income received in the preceding calendar year by every citizen of the United States, whether said gains, profits, or income be derived from any kind of property, rents, interest, dividends, or salaries, or from any profession, trade, employment, or vocation, carried on within the United States or elsewhere, or from any source whatever. The annual salary of a justice of the Supreme Court of the United States is ten thousand dollars, and this act levies a tax of two percent on six thousand dollars of this amount, and imposes a penalty upon those who do not make the payment or return the amount for taxation.

The same objection, as presented to a consideration of the objection to the taxation of the bonds and securities of the States as not being specially taken in the cases before us is urged here to a consideration of the objection to the taxation by the law of the salaries of the judges of the courts of the United States. The answer given to that objection may be also given to the present one. The law of Congress being of a public nature, affecting the interests of the whole community, and attacked for its unconstitutionality in certain particulars, may be considered with reference to other unconstitutional provisions called to our attention upon examining the law, though not specifically noticed in the objections taken in the records or briefs of counsel, that the Constitution may not be violated from the carelessness or oversight of counsel in any particular. See O’Neil v. Vermont, 144 U. S. 323, 144 U. S. 359.

Besides, there is a duty which this court owes to the one

Page 157 U. S. 605

hundred other United States judges who have small salaries and who, having their compensation reduced by the tax, may be seriously affected by the law.

The Constitution of the United States provides in the first section of article III that:

“The judicial power of the United States shall be vested in one Supreme Court, and in such inferior courts as the Congress may from time to time ordain and establish. The judges, both of the Supreme and inferior courts, shall hold their offices during good behavior, and shall, at stated times, receive for their services a compensation, which shall not be diminished during their continance in office.”

The act of Congress under discussion imposes, as said, a tax on six thousand dollars of this compensation, and therefore diminishes, each year, the compensation provided for every justice. How a similar law of Congress was regarded thirty years ago may be shown by the following incident in which the justices of this court were assessed at three percent upon their salaries. Against this, Chief Justice Taney protested in a letter to Mr. Chase, then Secretary of the Treasury, appealing to the above article in the Constitution, and adding:

“If it [his salary] can be diminished to that extent by the means of a tax, it may in the same way be reduced from time to time at the pleasure of the legislature.”

He explained in his letter the object of the constitutional inhibition thus:

“The judiciary is one of the three great departments of the government created and established by the Constitution. Its duties and powers are specifically set forth, and are of a character that require it to be perfectly independent of the other departments. And in order to place it beyond the reach, and above even the suspicion, of any such influence, the power to reduce their compensation is expressly withheld from Congress and excepted from their power of legislation.”

“Language could not be more plain than that used in the Constitution. It is, moreover, one of its most important and essential provisions. For the articles which limit the powers of the legislative and executive branches of the government, and those which provide safeguards for the protection of the citizen in his person and property, would be of little value

Page 157 U. S. 606

without a judiciary to uphold and maintain them which was free from every influence, direct or indirect, that might by possibility, in times of political excitement, warp their judgment.”

“Upon these grounds, I regard an act of Congress retaining in the Treasury a portion of the compensation of the judges as unconstitutional and void.”

This letter of Chief Justice Taney was addressed to Mr. Chase, then Secretary of the Treasury and afterwards the successor of Mr. Taney as Chief Justice. It was dated February 16, 1863, but, as no notice was taken of it, on the 10th of March following, at the request of the Chief Justice, the Court ordered that his letter to the Secretary of the Treasury be entered on the records of the court, and it was so entered. And in the Memoir of the Chief Justice, it is stated that the letter was, by this order, preserved “to testify to future ages that, in war, no less than in peace, Chief Justice Taney strove to protect the Constitution from violation.”

Subsequently, in 1869 and during the administration of President Grant, when Mr. Boutwell was Secretary of the Treasury and Mr. Hoar, of Massachusetts, was Attorney General, there were in several of the statutes of the United States for the assessment and collection of internal revenue provisions for taxing the salaries of all civil officers of the United States, which included, in their literal application, the salaries of the President and of the judges of the United States. The question arose whether the law which imposed such a tax upon them was constitutional. The opinion of the Attorney General thereon was requested by the Secretary of the Treasury. The Attorney General, in reply, gave an elaborate opinion advising the Secretary of the Treasury that no income tax could be lawfully assessed and collected upon the salaries of those officers who were in office at the time the statute imposing the tax was passed, holding on this subject the views expressed by Chief Justice Taney. His opinion is published in volume XIII of the Opinions of the Attorneys General, at page 161. I am informed that it has been followed

Page 157 U. S. 607

ever since without question by the department supervising or directing the collection of the public revenue.

Here I close my opinion. I could not say less in view of questions of such gravity that go down to the very foundation of the government. If the provisions of the Constitution can be set aside by an act of Congress, where is the course of usurpation to end? The present assault upon capital is but the beginning. It will be but the stepping stone to others, larger and more sweeping, till our political contests will become a war of the poor against the rich; a war constantly growing in intensity and bitterness.

“If the court sanctions the power of discriminating taxation, and nullifies the uniformity mandate of the Constitution,” as said by one who has been all his life a student of our institutions, “it will mark the hour when the sure decadence of our present government will commence.” If the purely arbitrary limitation of $4,000 in the present law can be sustained, none having less than that amount of income being assessed or taxed for the support of the government, the limitation of future Congresses may be fixed at a much larger sum, at five or ten or twenty thousand dollars, parties possessing an income of that amount alone being bound to bear the burdens of government; or the limitation may be designated at such an amount as a board of “walking delegates” may deem necessary. There is no safety in allowing the limitation to be adjusted except in strict compliance with the mandates of the Constitution which require its taxation, if imposed by direct taxes, to be apportioned among the States according to their representation, and if imposed by indirect taxes, to be uniform in operation and, so far as practicable, in proportion to their property, equal upon all citizens. Unless the rule of the Constitution governs, a majority may fix the limitation at such rate as will not include any of their own number.

I am of opinion that the whole law of 1894 should be declared void and without any binding force — that part which relates to the tax on the rents, profits or income from real estate, that is, so much as constitutes part of the direct tax, because not imposed by the rule of apportionment according

Page 157 U. S. 608

to the representation of the States, as prescribed by the Constitution — and that part which imposes a tax upon the bonds and securities of the several States, and upon the bonds and securities of their municipal bodies, and upon the salaries of judges of the courts of the United States as being beyond the power of Congress, and that part which lays duties, imposts and excises as void in not providing for the uniformity required by the Constitution in such cases.

QUESTION: Hi Martin,

QUESTION: Hi Martin,

ANSWER: Curious. I know that in Germany they do not really teach the details of the rise of Hitler. But he was the ultimate reaction to the events of the 1920s. There is a good book on the subject, but it is in German –

ANSWER: Curious. I know that in Germany they do not really teach the details of the rise of Hitler. But he was the ultimate reaction to the events of the 1920s. There is a good book on the subject, but it is in German –

There has never been actual tangible money issued by any government that was worth strictly its metal content. It was always valued greater than its intrinsic value. Even the first coins issued by any government took place in Lydia, located in modern Turkey. They used gold simply because that was the private medium of exchange. The first step was simply to create a standardized weight for in the Bible they talked about weighing the silver to make payment. When the king began to stamp his seal on money, fiat began. People used metal and wheat as a medium of exchange. The

There has never been actual tangible money issued by any government that was worth strictly its metal content. It was always valued greater than its intrinsic value. Even the first coins issued by any government took place in Lydia, located in modern Turkey. They used gold simply because that was the private medium of exchange. The first step was simply to create a standardized weight for in the Bible they talked about weighing the silver to make payment. When the king began to stamp his seal on money, fiat began. People used metal and wheat as a medium of exchange. The

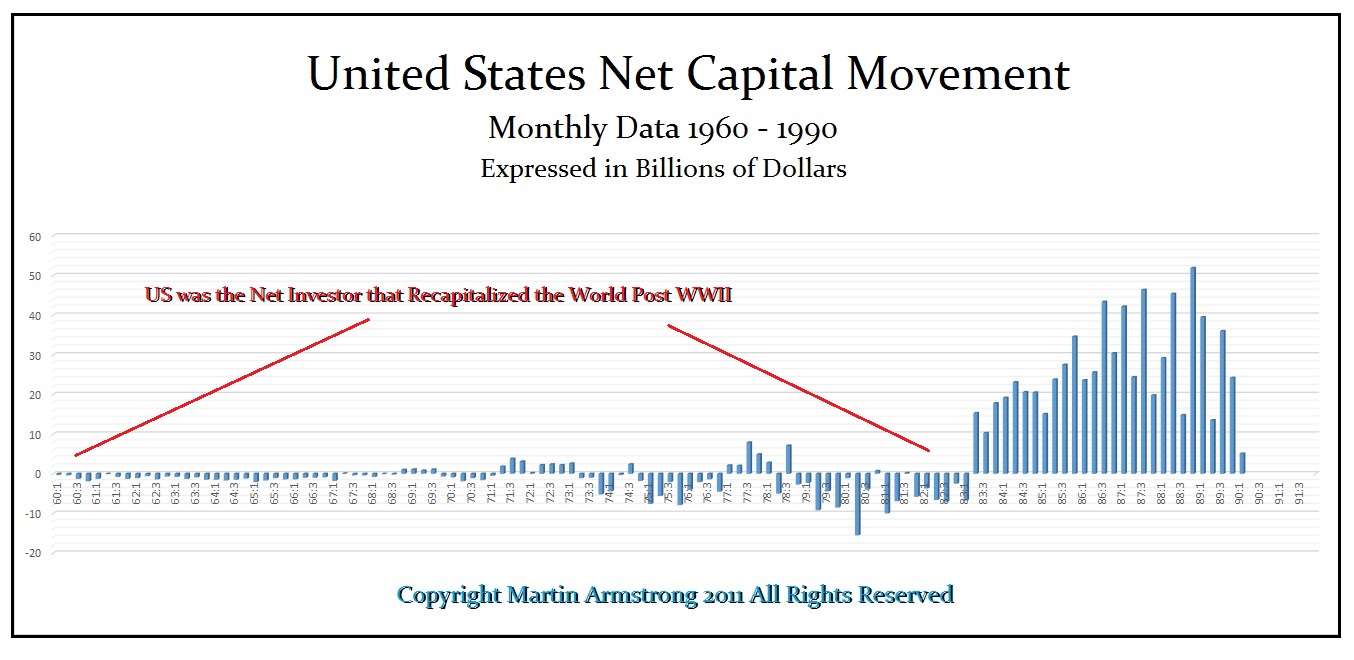

In general, Europeans are still trapped in World War II thinking that a stronger currency means economic boom. When all the currencies were wiped out by the war, politicians used the currency value in Europe as a reason to prove they were doing a good job. So the historical bias in Europe has been dominated by the perspective. The USA was a third world country during the 19th century. It was the “emerging market” for European investors. It was virtually bankrupt in 1896 and it was World War I and II that raised the USA to the richest country in the world by 1950 holding 76% of the total world gold reserves. That was accomplished not by Marxism, political economic manipulation, or anything any politician enacted. It was create SOLELY and EXCLUSIVELY by capital inflows because of Europe running around destroying itself.

In general, Europeans are still trapped in World War II thinking that a stronger currency means economic boom. When all the currencies were wiped out by the war, politicians used the currency value in Europe as a reason to prove they were doing a good job. So the historical bias in Europe has been dominated by the perspective. The USA was a third world country during the 19th century. It was the “emerging market” for European investors. It was virtually bankrupt in 1896 and it was World War I and II that raised the USA to the richest country in the world by 1950 holding 76% of the total world gold reserves. That was accomplished not by Marxism, political economic manipulation, or anything any politician enacted. It was create SOLELY and EXCLUSIVELY by capital inflows because of Europe running around destroying itself.