A bank failure of this proportion has not been seen since 2008 when Washington Mutual failed. The majority of deposits in Silicon Valley Bank (SVB) are uninsured, meaning the FDIC’s $250,000 protection does not apply. Uninsured depositors will be provided receivership certificates and should receive an advanced dividend this week. The FDIC must sell off the remaining assets of SVC to determine how much it can provide to those uninsured depositors. The FDIC is encouraging borrowers to continue paying their existing loans. The bank was said to host $209 billion in assets and $175.4 billion in deposits as of December 2022. Washington Mutual held around $307 billion in assets when it went down.

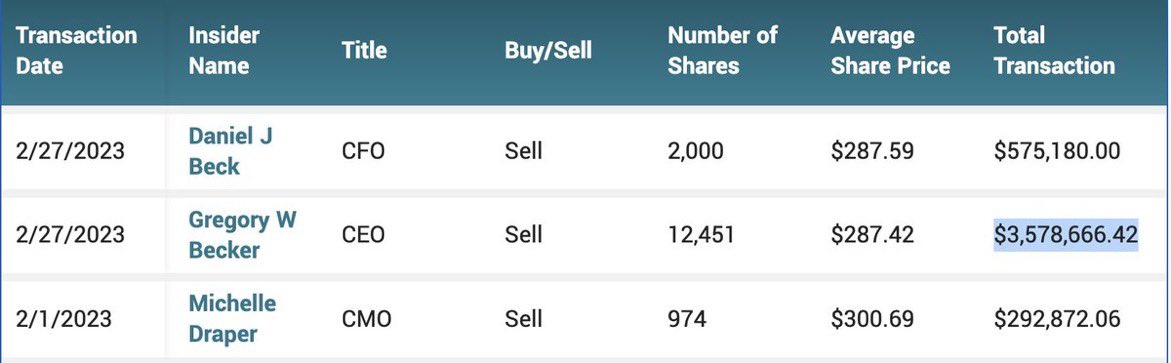

Tons of people and businesses will be completely screwed over. Who could have seen it coming? Silicon Valley Bank CEO, CFO, and CMO sold off millions in stock over the past two weeks. President and CEO Greg Becker sold 12,451 shares on February 27 for $3.6 million at $287.42 per share. Later that day, he purchased options for the same amount of shares at $105.18 a piece. He did the same thing in December 2021, as this is not an uncommon albeit unethical practice. Banks commonly trade against their own clients. Becker sold about $3.57 million worth of SVB stock over the past two weeks and is now making TV appearances saying he did not see this coming.

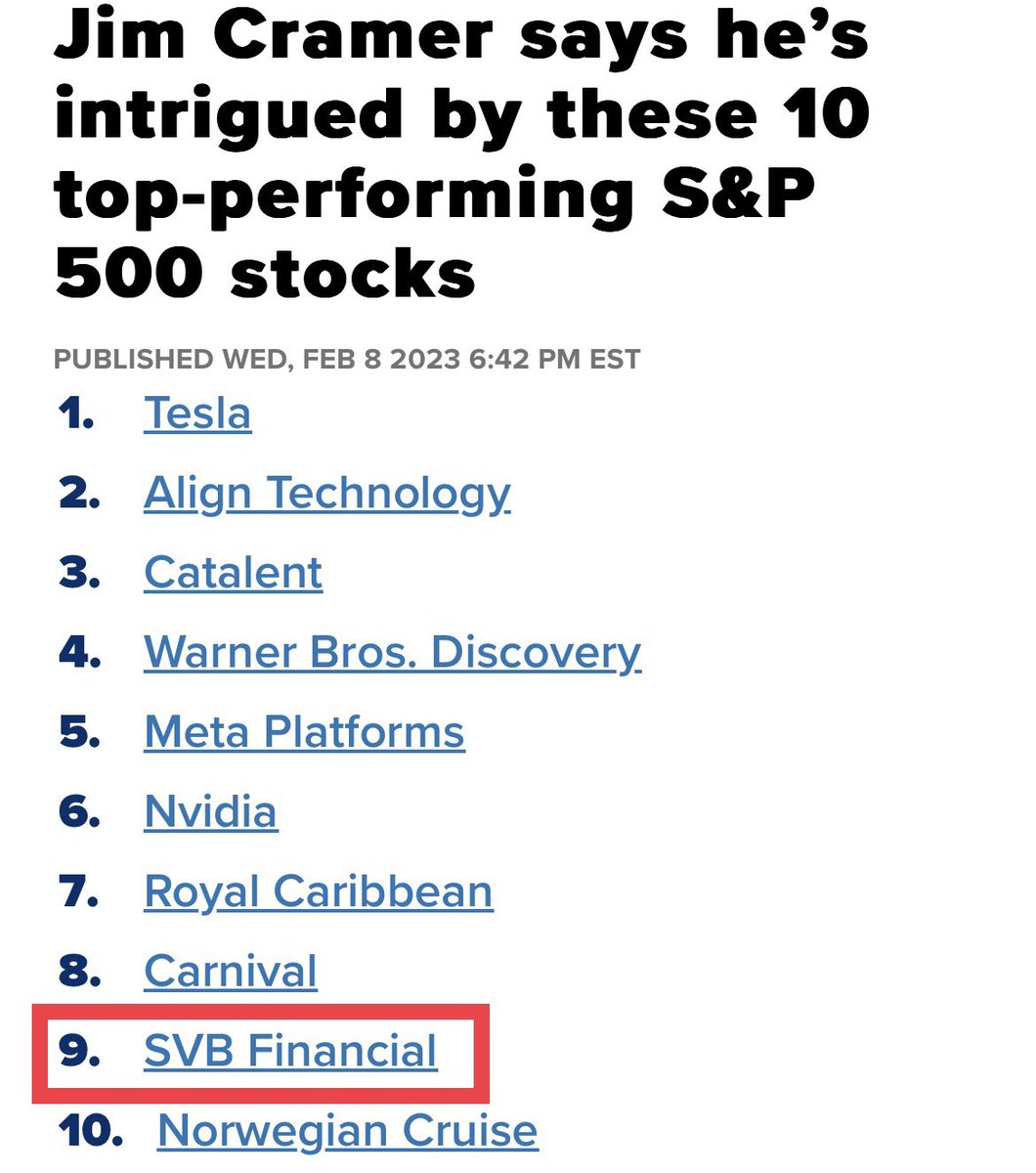

There were signs of trouble, but the talking heads said otherwise. Forbes even listed SVB Financial Group as #20 on its list of America’s Best Banks in an article published on February 14, 2023. Talking/screaming head Jim Cramer came out last month to say that SVB Financial would become one of the top performers on the S&P. This is why you cannot listen to information based on biased opinions. I hesitate to call this negligence technical analysis.

Companies are now at a complete loss, many cannot make payroll, and this situation will only worsen once the uninsured depositors realize their IOUs are worthless.

COMMENT: Marty; Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious metals markets, the US Department of Justice announced. Of course, —- —–, which is forever bullish metals, claims they moved the metals in the “direction they wanted from 2008 to 2014.” It just seems that people claim it is always manipulation when they have been wrong. They only look at gold in dollars as you have said it’s a global market. They would have to manipulate all the currencies as well.

This latest affair of so-called manipulating trades during the day proves what you have been saying. They have always been gunning for stops during the day, but they cannot manipulate the trend between a bull or bear market. Do you think people will ever understand this is a global economy?

HD

ANSWER: I know. Unless people have actually been a trader, they will never understand the market. They will blame people like this to pretend they were not wrong. The problem is that this nonsense of manipulation is driving a stake through the heart of the market. Trading is like a poker game. Do you reveal your hand before everyone starts to bet? Sometimes you bluff, but the point is if you are bluffing, you have to stand behind your bet.

The mere fact that someone is blaming this type of “manipulation” for being the reason they have been wrong demonstrates that they know nothing about investing no less trading. The DOJ is now big on calling placing large “spoof” orders as manipulation. That is absurd and it is no more than bluffing in a poker game. This is the way all the markets have always functioned. Everyone would know where the stops were anyway. Sometimes they traded ahead of them using the stops as your risk point to exit the trade, and other times they would sell or buy to push the market through the stops when it was obvious that was even possible.

When I was trading in precious metals back in the ’90s, the biggest “local” dealer on the floor was Oni Morrison. He would do “spoof” orders all the time which I called “flash” bids or offers. The difference was he was good for it if hit. I was long one time in gold and I wanted out for the computer projected a crash was coming. But if you offer a thousand lots and the market was heading lower, everyone will read that and jump in front of you. That is how the Hunts went bankrupt. The Hunts did not know how to trade. Just as in poker, you cannot show your hand and expect to trade.

Oni would do “flash” bids or offers. I told my broker not to offer anything. I told him just to watch Oni and as soon as he would do a 1,000 flash to buy – say done! Sure enough, Oni was trying to push the market back up and he did one of his famous flash bids for 1,000 lots. My broker, Emerald Trading, instantly said “DONE!” Oni did it again, and they said “DONE!” Again he did a fash for 1,000 and again they said “DONE!” That was it. Oni was full and everyone began selling as the metals tumbled.

That is the way you have to trade SIZE. This is the very foundation of trading all markets for everything is just a poker game. To now call a “spoof” trade manipulation is just wrong. It is totally different when you do not have the backing. Now that would be a fraud and trying to manipulate the market for that moment – not changing the overall trend. But when you have the backing to honor your “spoof” it is just a “flash” bid or offer that you must stand behind when hit. That is just trading.

It is total BS to pretend that these guys manipulated the entire market. That is just absurd. Not even the central bank can manipulate the economy. You cannot “manipulate” a market against the trend for everything is connected. That caused the Panic of 1893 when the Silver Democrats overpriced silver. The Europeans hit the arbitrage and dumped silver in the US and took the gold back to Europe. That led J.P. Morgan to have to arrange a $100 million gold loan to bail out the treasury. That alone proved that you CANNOT manipulate ANY market against its trend for it will be arbitraged internationally – plain & simple.

Gold trading around the world in different exchanges is arbitraged. You cannot have gold $20 high in one market v another. It will be arbitraged instantly. Those who claim this as “proof” that the metals have been manipulated so that is why they have not rallied and why they have been wrong are fools who have been separated from the money. They will never understand the markets no less be able to see beyond the end of their nose. It will be instantly arbitraged.

The collapse of the Soloman Brothers was precisely that. They were putting in bids at the Treasury Auction using other people’s names to goose the market. They got caught and the firm was taken down. I know PhiBro from the ’70s and ’80s. They took over Solomon Brothers and brought that style of trading from the commodity pits to Wall Street.

This excuse by goldbugs that the metals were actually “manipulated” in their long-term trend, shows their hopeless ignorance of the markets and how they even trade. There is NOBODY who could possibly do such a thing for everything connected. As soon as the dollar would rise, the metals in terms of foreign currency would be so overvalued they would all sell and they will end up broke the same as the Silver Democrats bankrupted the country by overvaluing silver.

Trading internationally, with clients in all currencies, we have to look at each market in terms of their currency for that will determine if they made a profit or loss. Anyone who claims the metals have been manipulated and that is why they have not rallied is obviously oblivious to the world around them.

Gold does NOT rise with inflation – that is the sales pitch of a used car salesman. Gold rises in times of UNCERTAINTY with respect to the government. In times of war, it rises because it is NEUTRAL and you are not betting on who will win.

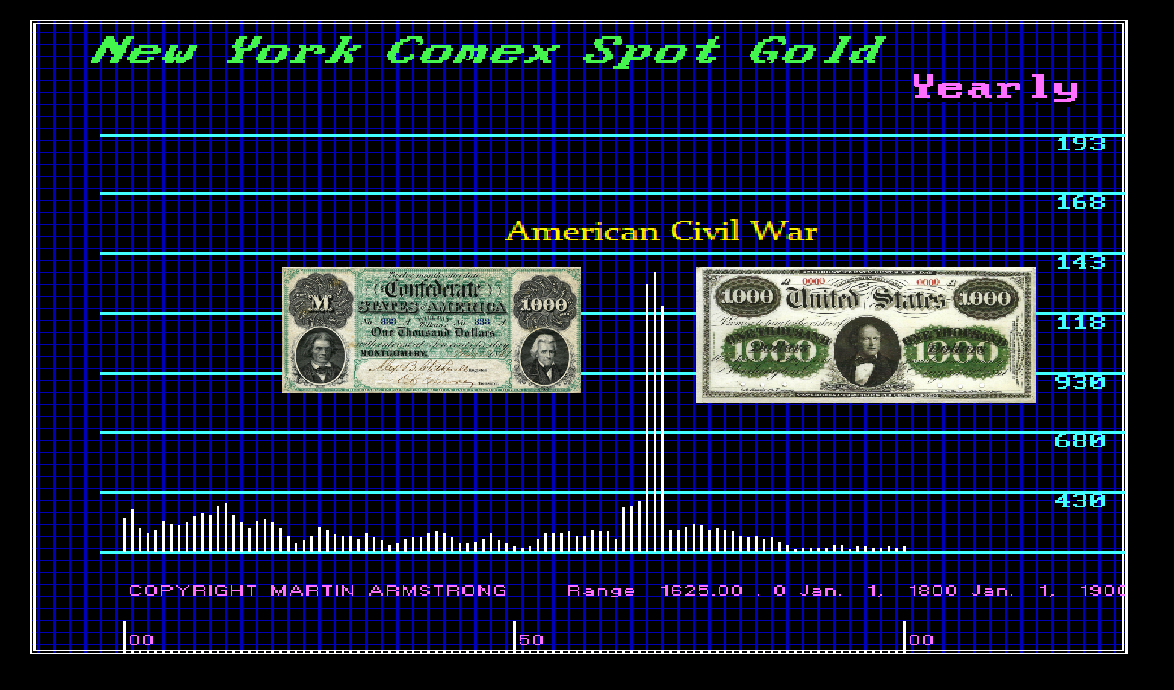

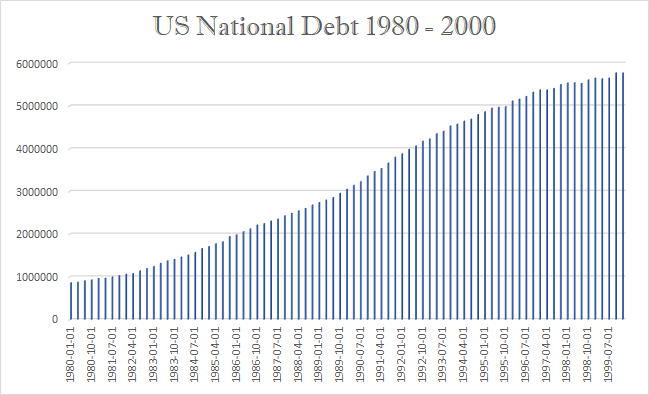

All we hear is that the debt is rising and therefore gold will explode. Once again, they offer no proof of their sophistry because there is no such proof. Gold declined for 19 years while the national debt climbed endlessly.

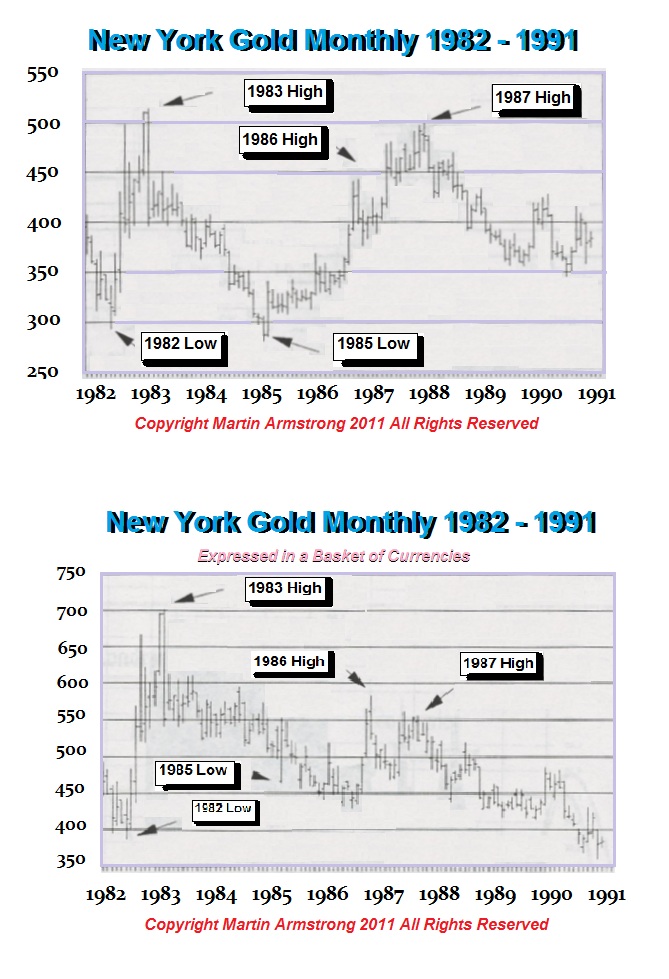

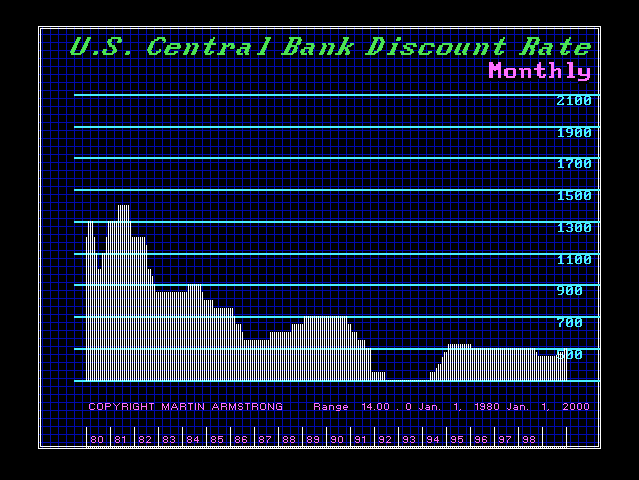

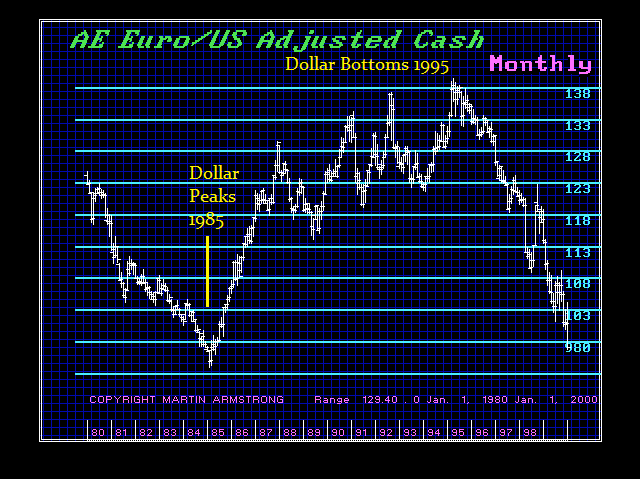

Then there is the myth about interest rates and gold that higher rates are bearish and lower rates are bullish. Well, interest rates peaked in 1981 and declined in 1994 before they began to rise marginally into 1995. Yet then contrast that myth with the performance of the dollar. There the greenback rose to a record high in 1985 but then declined for 10 years into 1995 all the while gold declined into 1999.

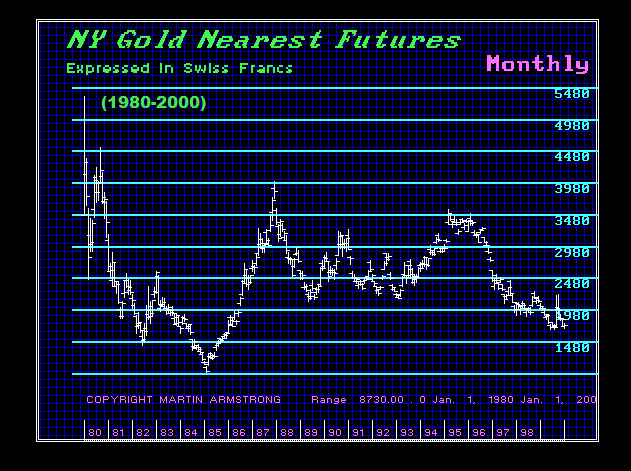

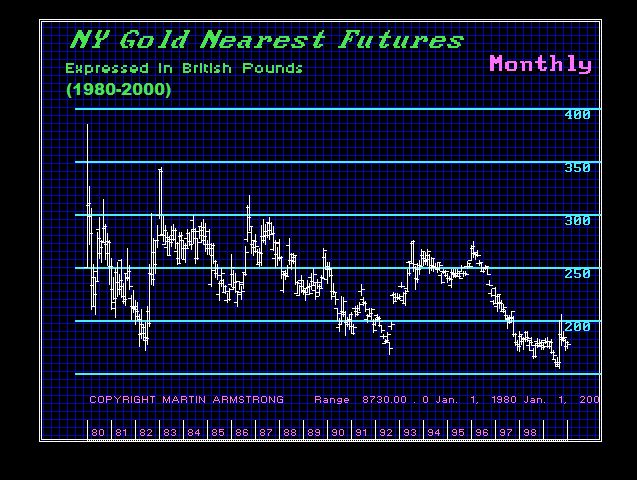

OK, so now let’s look at gold between 1980 and 200 in terms of Swiss francs and British pounds. We can instantly see that gold bottomed in 1985 in terms of the Swiss franc. In terms of British pounds, gold did not bottom until 1999.

People come up with theories all the time. However, they always try to reduce everything to a single cause and effect. They are doing that with climate change. They are telling the world it is CO2 that has changed the climate without ever addressing anything else.

The world we live in is not only complex, but it is also so dynamic it appears that no human can correctly forecast the future with an “I think” scenario. Sometimes they will be right, and others they will be wrong. Typically, they fail because they try to reduce the world to a single cause and effect.

Gold Rises with UNCERTAINTY with respect to the question of will the government survive its own madness.

COMMENT #1: Marty; Thank you so much for your warning at the WEC that we would now face a banking crisis with rising rates into 2024. You are always so far ahead of the pack. Live forever – please!

KQ

REPLY #1: Thank you, but that would sentence me to perpetual taxation indefinitely. No thanks.

COMMENT #2: Hello. I read your FREE blog because I am poor. Would you please stop posting PRIVATE stuff and post stuff that us peons can read?

Thank you kindly.

Ms. Terri

REPLY #2: My concern is since we forecast this last year, they will only blame me. That blog is only $15 a month, but it is blocked by Google so it is more free speech if you get my drift. I simple MUST be guarded in what I say publicly because they simply always view me as having too much influence.

I will offer this recommendation (publicly) for my ear is turning red from all the phone calls. As for the Biden Administration, if they DO NOT heed my warning, our forecast will be devastating. The Biden Administration MUST stand behind ALL deposits – not the $250,000 FDIC limit. If they do not, small businesses will pul; excess cash from banks, switch to 30-day T-Bills at a brokerage house, and say screw the FDIC and the Biden Administration’s anti-rich (small business which employs 70% of the workforce).

The compromise here is that we need a shotgun wedding where a larger bank takes over SVB at the raw price of the deposits. The shareholder loses, but ALL depositors are covered. Any value of the shares should be attributed to tangible assets only, not goodwill. You will penalize your “hated rich” and even the small businesses will be saved. If not, you will wipe out numerous businesses that cannot even pay employees. That will set off a contagion as you try to uphold your hatred of the “rich” while you pour money into the most corrupt government in the world at the real expense of taxpayers.

Of course, SVB can simply declare they “identify” as a Ukrainian Bank and then everything would be covered right down to the pensions of the CEO.

QUESTION: The sales pitch seems to be that there is this $2 quadrillion in global debt that overhangs everything. Paper assets, therefore, will all implode! They seem to be saying that everything has risen due to this debt bubble and it was all created with Zero interest rates. Now that they are going up, the debt bubble will burst and everything will decline. The story seems to be that this decades-long Boom Bust cycle was created over and over by the Federal Reserve.

This seems to be like you have said, they try to reduce everything to a single cause and effect.

What really happens?

PCJ

ANSWER: These people seem to keep preaching the same story but have no historical understanding whatsoever of how the monetary system has ever worked. Their focus on the Federal Reserve shows that they are not looking at the world economy and they do not even comprehend how bad things really are outside the United States. They do not comprehend what is an interest rate. It is the compensation to a lender for his anticipation of inflation plus a profit. If I think the dollar will decline by 50%, why would I lend you dollars for a year if when you pay me back it buys half of what it did when I lent it to you?

Debt can be a performing asset. I advised many of the Takeover Boys during the 1980s. We would borrow in one currency to buy the asset in another using the computer to distinguish the long-term trends. I would not recommend that to someone just operating on a gut feeling.

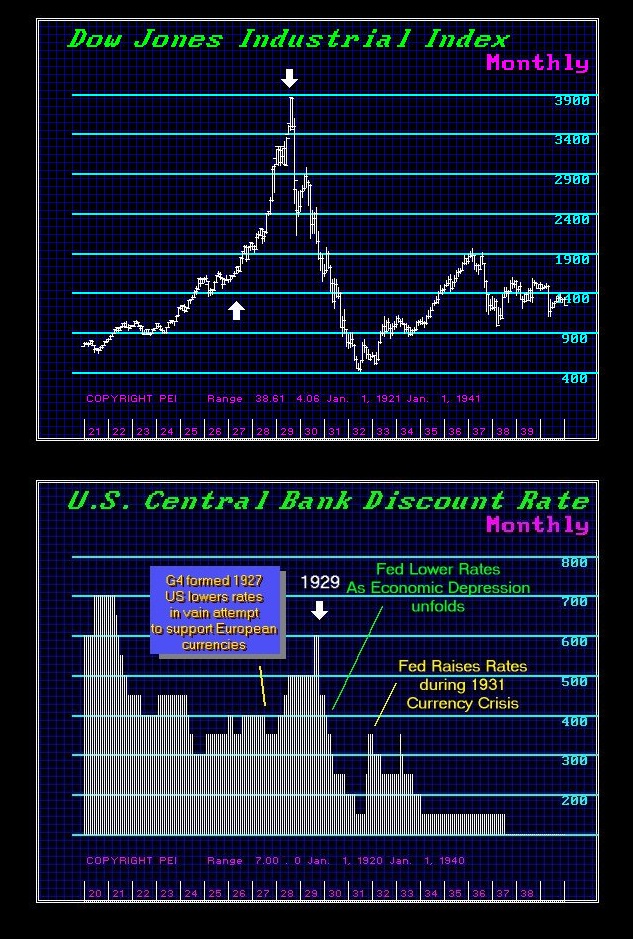

We were also advising on real values, which Hollywood distorted and based the movie Wall Street with Michael Douglas and his famous speech on greed. What they did not really understand was that after a Public Wave that peaked in 1981, stocks were suppressed and the full-faith in government created the broadly supported bond market. Hence – bonds were conservative and stocks were risky. There were two aspects that were behind the entire Takeover Boom.

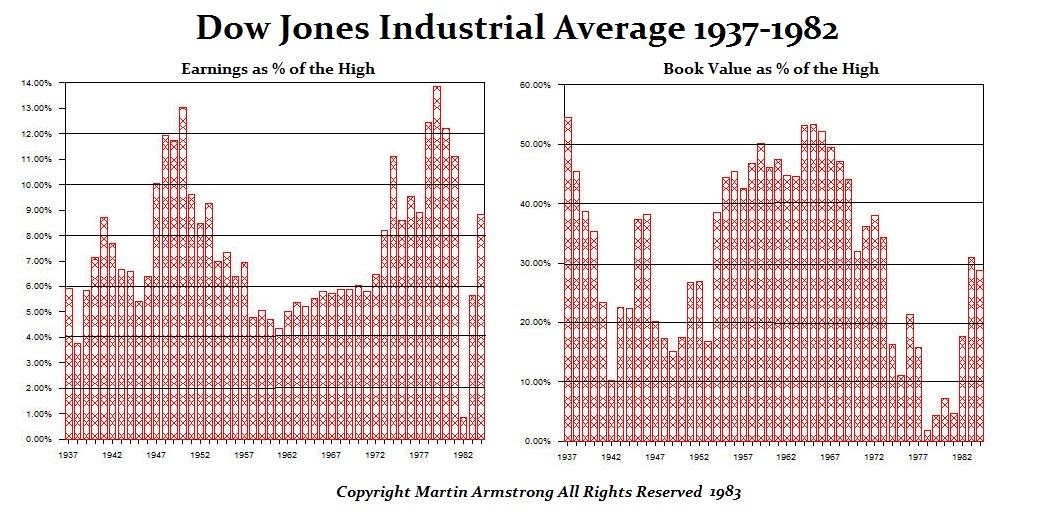

First, I was showing these charts and how in terms of book value, the Dow Jones bottomed in 1977. It was obvious that if you could buy a company, sell its assets, and double or triple your money, then the market was obviously not overpriced. We had forecast that the Dow was undervalued and that it would rise from the 1982 low of 769.98 and test the 2500 level in two years in 1985. Indeed, it reached 2695.47 by September 1987. We also projected that by the next decade, the Dow would test 6,000 on its next rally.

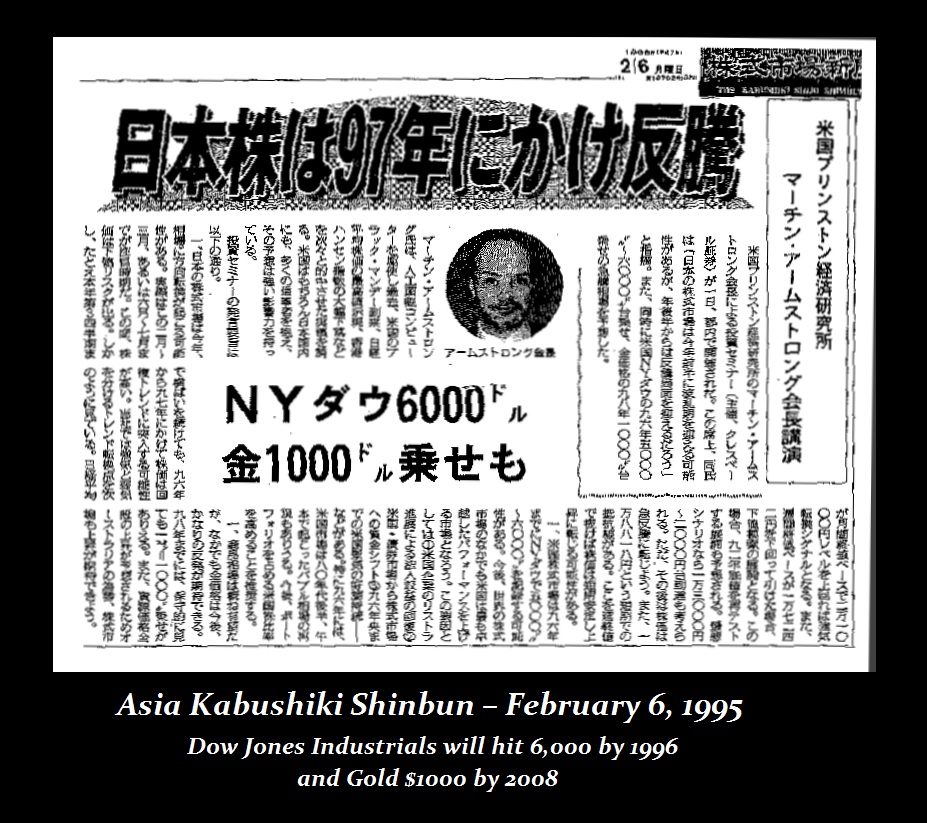

Even the press in Japan was shocked. We were also projected that Crude would fall below $10 in 1998. Indeed, that forecast was covered by Mark Pitman at Bloomberg News. It bottomed at $10.65 in 1998. In gold would forecast that it would drop to test $250 by 1999 completing a 19-year cycle low. Then gold would rally to test 1,000. Gold reached the $1,000 level by 2008. The Japanese press thought those forecasts were wild, to say the least.

The SECOND aspect of our advice to the takeover boys of the ’80s was something the press NEVER understood. We would advise borrowing in one currency for an asset in another. We were able to turn debt into a performing asset. We would make 20-40% profit on the currency alone. Often, the press would just look at the debt and not understand what we were even doing.

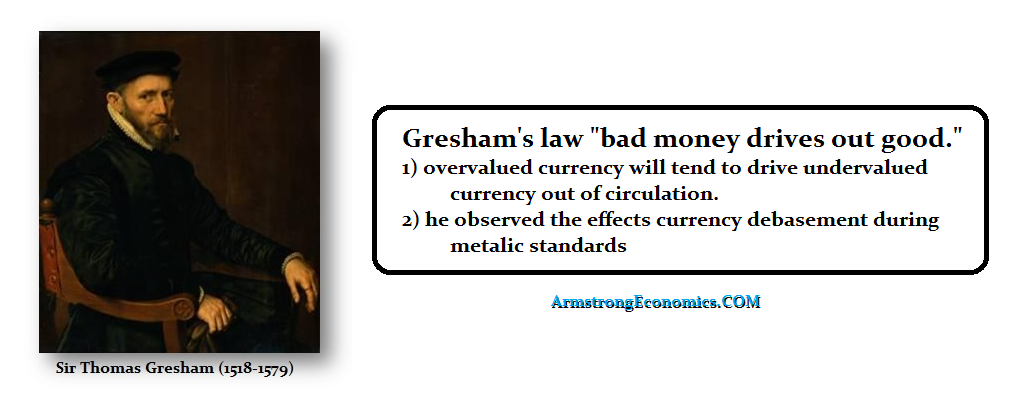

Most of this reasoning stems from Sir Tomas Gresham’s observations when he represented England at the Amsterdam exchange during the reign of Henry VI’s reign and debasement. As Henry debased the silver coinage as was taking place in Spain, the more they debased the coinage, the higher the inflation took place. His observation that bad money drives out the good has been grossly misunderstood. When I was growing up, they took the silver out of the coinage in 1965. People were culling out the silver showing that the debased new coinage of 1965 drove out of circulation the old silver coinage. The same thing has taken place with the copper pennings.

Because people hoard old coinage, the money supply shrinks. That then forces the government to issue far more debased coinage to compensate for the coinage that has been withdrawn from hoarding. Consequently, inflation unfolds for all tangible assets to rise in value as expressed in the newly debased coinage.

What these people always try to sell is the same old scenario that they cannot point to a single instance in history where everything collapses to dust but only gold survives. Such periods will typically result in revolution. When Caesar crossed the Rubicon, that was also all bout a debt crisis.

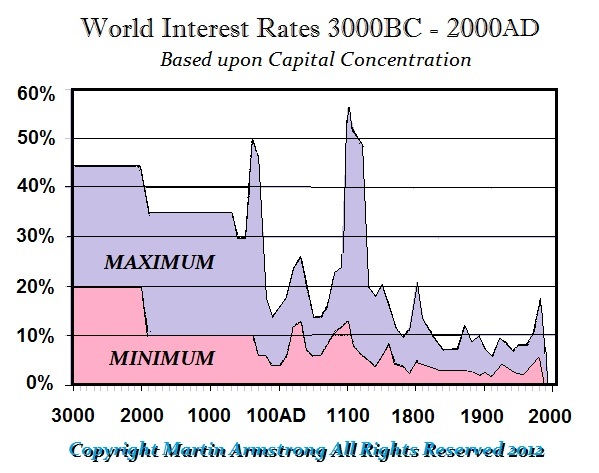

You must also understand that interest rates will be at their LOWEST internationally in the core economy of the Financial Capital of the World – which is the USA right now. The further you move from the center, the higher the interest rate will be. Hence, I have warned that the United States will be the LAST to fall – never the first. This is not based upon my opinion, this is simply historical fact.

The Bottom Line is very simple. There is just no such period as people describe where everything turns to dust and only gold survives. Even if that were true, they what good would the gold do if everything else is worth ZERO? Gold would have also ZERO value since nothing would have value.

The real issue is that as government defaults unfold, tangible assets will rise in value for the amount of money in debt always dwarfs that in even the stock market. We are in a Sovereign Debt Crisis and that is very different from a private debt crisis.

COMMENT: Marty, you are 100% spot on about governments only ever being capable of lying and mismanaging money and raising taxes. The Australian Labor party that ran on a mandate to not change superannuation are now proposing to change superannuation. Their plan is the abolish tax benefits for accounts with balances above $3M, using the usual argument of targeting only the rich. That is always the selling pitch isn’t it? Only the rich and of course the majority take the bait. I have desperately tried to inform people that it is NEVER just the rich that re impacted. I have can not for the. life of me get people to understand that the so called rich, will be required to sell assets to meet tax commitments and have less money to buy assets into the future, and that, that in turn will impact asset prices and thus affect everyone. Rich and poor. And then there is the obvious. Thresholds never remain where they begin and are always lowered. Government is on the hunt for money in every country. Cheers

AQ

REPLY: That is the problem. Most people do not want to believe that the government only looks out for its own power. It is so critical to prohibit career politicians no matter which direction they lean. For in the end, they will always lean in their own favor.

Perhaps you might remind them of the “Luxury Tax” that the sales pitch was they were going to tax their Ferarries, Fur Coats, & their French Wines. I was there in Australia back then. Maybe I saw two Ferraries because they were already 100% taxed to import. Some perhaps wore a fur coat down in Melbin, and nobody ever served me French wine – its was always Australian. People cheered then too – get those evil rich people. Then they woke up and ALL electrical products were suddenly a luxury.

The bulk of all taxes is always from the common people simply because we outnumber the billionaires. There are less than 500 such people in the USA. Confiscate all their wealth and you will not balance the budget even for one year.

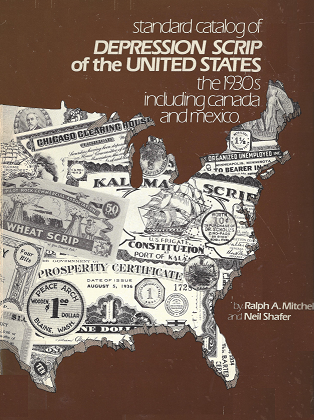

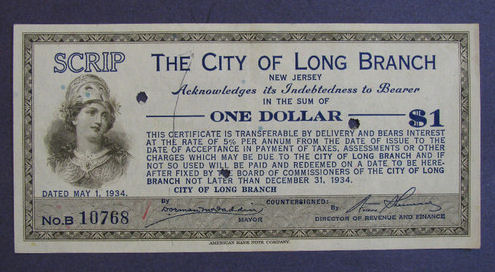

QUESTION: At the WEC, you said as the nation breaks apart, the most likely course of action will be the creation of local currencies. You also said you would post a catalog of Depression Scrip. I have not seen that. Can you post that, please?

Thank you for a great WEC. Always learning something new.

GJ

ANSWER: Sorry. I may have forgotten to publish that because I searched Amazon and could not find it. It was published back in 1984. Because Depression Scrip is not a huge field of collectors largely because most have never heard of the existence of private currency during the Great Depression, this book is quite rare. You may find some used copies that go for $125 or more.

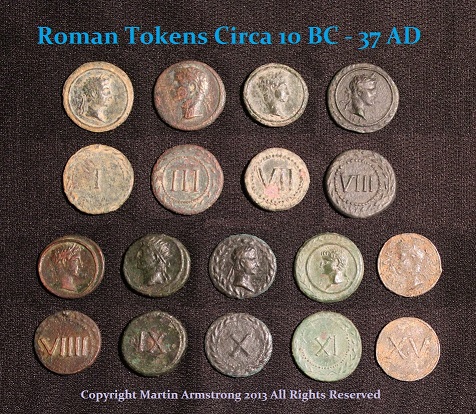

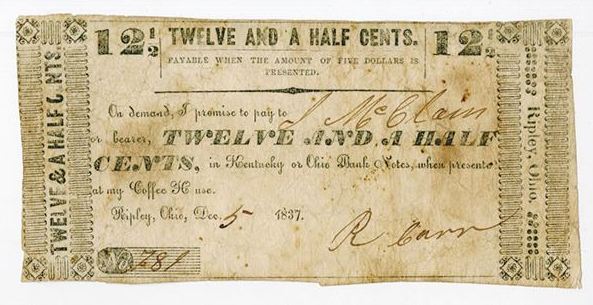

I have studied the subject from the standpoint of economics. During the reign of Tiberius (14-37AD), he was very frugal and as such there was a shortage of money which led to a Financial Panic in 33AD. During such periods, private money surfaces as a necessity. This is why history repeats because human nature never changes. It will always respond the same way.

Here is private money from the Panic of 1837. The denomination reads 12 1/2 cents. This was issued by a Coffee House. Here is a half-penny issued by the New York store of Macy’s in 1876 following the Panic of 1873.

Throughout history, we see the very same reaction each and every time. I have collected a large number of private currencies covering the various financial waves of panic since Roman times. It has been a critical part of being able to forecast what takes place during these events. The common denominator is always humanity since we never change for thousands of years. We only progress in terms of technology – not our human emotions.

Here is private scrip issued by the San Francisco Clearing House where transactions were settled in the bond and stock markets. The backing was the private shares in companies. This was the Panic of 1907.

Here is another issued in 1908 in Augusta, Georgia. It was the Panic of 1907 that really we began to see widespread stock exchanges issuing money that began because if there was a shortage of cash, you could not conduct any business whatsoever since it was impossible to pay.

Here is the Chicago Clearing House which issued private money during the Great Depression in 1933. We find various stock exchanges issuing private currency in times when there was a shortage of money because people were hoarding their cash in times of uncertainty.

This was the very first Depression Scrip I ever saw and immediately purchased it. This opened the door in economics for me to understand how things function during a great crash. What took place during the Great Depression was that there was such a shortage of cash, over 200 cities began to issue their own currencies just to enable transactions to take place. Businesses could not hire people because there was no available cash to pay them

There are catalogs available in German concerning the NotGeld, private issues of currency, during the Hyperinflation of the 1920s. Once again, it does not matter what nation or culture. The same human response will unfold every time.

As the United States breaks up, as is the case in Europe, we will see currencies appears on a regional basis. This is how it will always work. I spent more than two decades investigating these trends and collecting scrip from all financial crises going back to ancient times. Without access to these examples, there is just no economic historical account that has ever tied all of this together. I had to explore this all on my own.

QUESTION: Marty, Ever since the debacle in London with the long-term debt, there have been whispers in NYC about how the demand for long-term is drying up. When this becomes critical, is that when the whole thing comes crashing down?

KW

ANSWER: That was the real gist of Yellen’s speech back in October of 2022. Of course, the US press will never elaborate on this problem until it smacks them in the face. Yellen publicly admitted that the Treasury asked the primary dealers of US government debt for their views on the merits and limitations of a buyback program. The Treasury Borrowing Advisory Committee, made up of market participants, highly recommended considering the move because the demand for long-term was declining.

Yellen herself publicly acknowledged the decline in trading volume in 20-year bonds, which they reintroduced in 2020 thanks to COVID. Quoting from her direct comments:

“The 20-year Treasury is an area, an issue where there’s been less liquidity — but we haven”t made any decisions about it.”

Even the Securities Industry and Financial Markets Association came out and publicly also stated last October that there had been episodes of illiquidity. This was the same problem that created the Crisis in the Long-term British gilt market.

Institutions do not want to buy the long-term in the face of (1) rising interest rates to fight inflation, and (2) unlimited handing of money to Ukraine that will NEVER come back for Ukraine is a black hole and reliable sources are deeply concerned that Ukraine will lose and exist no more.

The escalation in debt on the horizon with World War III is beyond the capacity of the Primary Dealers to buy. They are strained now with the debt expansion for socialism, then Ukraine, and add War, this system is cracking NOW! The Primary Dealers cannot buy more debt than their balance sheets allow. The “whispers” running around have been on the street. The press has not articulated this for (1) it’s above their pay grade to comprehend, and (2) they cannot dare report the truth.

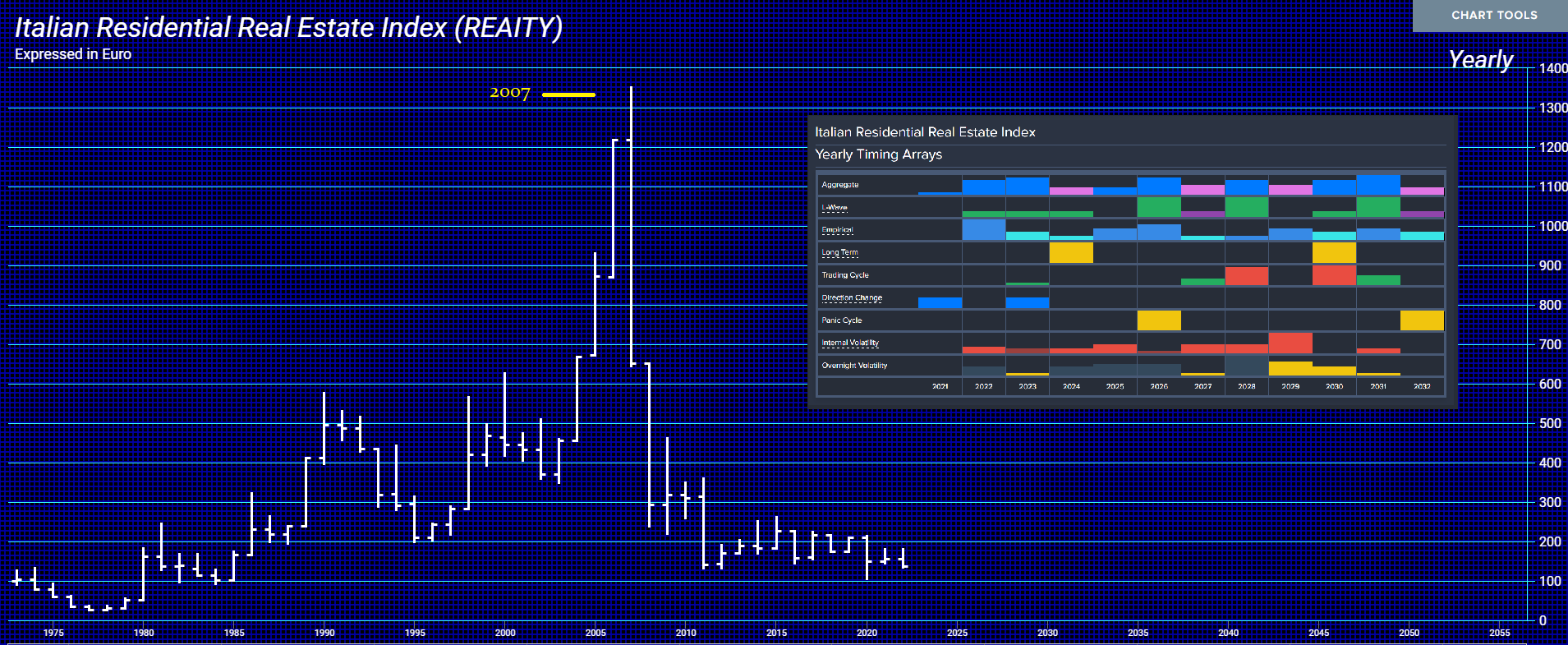

QUESTION: Dear Sir, Hello from Europe and a hopeful new year. In WW2 in Athens, people were exchanging their apartments for a few liters of olive oil, hence real estate went really down. The short question that you can answer even with a yes or no: If this year’s aggressivity in terms of war actions will rise, what happens? Will real estate fall on the first stage and then – due to governmental actions – will rise again? It is a bit confusing while I am trying to understand the mechanism… economy is not simple at all. Thank you. SM

ANSWER: The real truth about real estate and war, declines the closer you get to the action. When we look at our models for European real estate, it clearly shows 2023 as a directional change and it appears to be heading into a Panic Cycle for 2027. Our leaders project like we should all go charge into Russia and defeat it in a matter of weeks or just days. Besides the fact that they never discuss that civilian deaths are twice as high as military, they also never talk about how the net worth of everyone in Europe will decline. Your house will decline in value for (1) people are not interested in buying a new home in times of uncertainty, and (2) interest rates will rise sharply due to inflation which is also part of the war cycle.

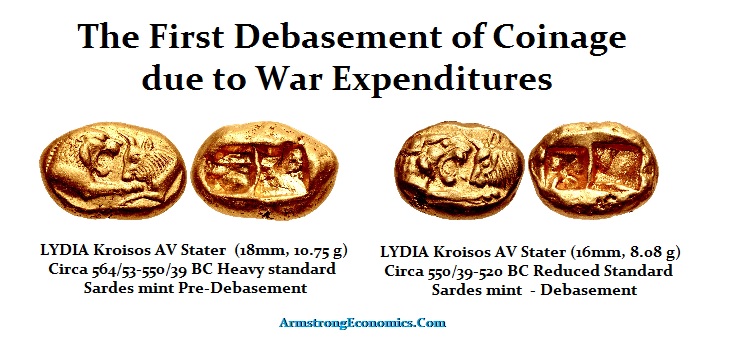

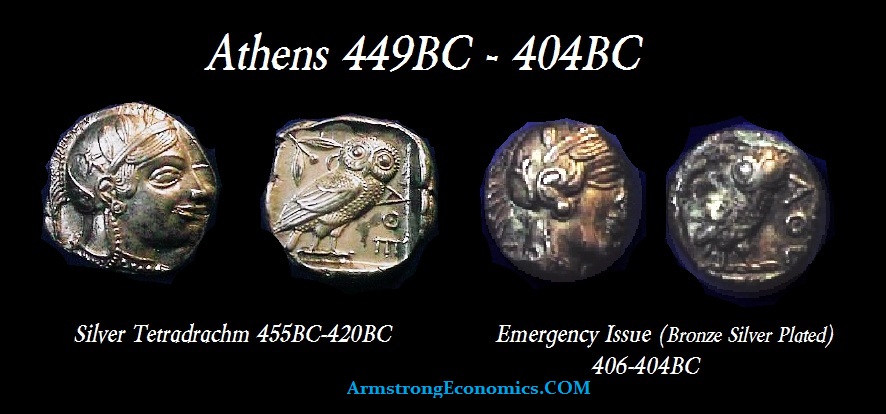

Lydia, in modern Turkey where coins were invented, shows the impact of war. It was Lydia v Person (Cyrus the Great) and we see the very first debasement in recorded history which accompanies war. The coinage was debased showing roughly a 25% devaluation in the purchasing power during the 6th century BC.

The Peloponnesian War in Greece saw the Athenian Owl reduced from silver to bronze and just silver plated. We find the same trend in Rome. There is NEVER any exception to this rule.

Beware, as the West insists upon expanding this war, you are sacrificing all your life savings in real estate for the political nonsense of our leaders in Europe as a whole. They are true war criminals. They could settle this in a day. Just honor the Minsk Agreement.

The Federal Reserve raised the benchmark by 25 bps, as expected. The Fed fully understands that the manipulation of the CPI is a necessary aspect both for containing government benefits and understating inflation also results in high tax revenues. The market loves hope, and as a result, they focused on the warning that we’ll be in restrictive territory for just a bit longer. Most still believe that there will be a slowdown in inflation just ahead.

The Fed’s cautionary commentary saying that the “disinflation process” has started triggered shares to jump ending up 1%. This shows how insane the analysis had become that they cheer a recession and think that lower interest rates are bullish for the stock market. Obviously, they just listen to the talking heads on TV and have never bothered to look at reality. When interest rates decline, so has the stock market. Interest rates rose for the entire Trump Rally, and they crashed during the Great Recession of 2007-2009. For the life of me, I just shake my head when the talking heads cheer lower rates and spread doom and gloom with higher rates.

Posted originally on the CTH on January 18, 2023 | Sundance

There is something predictable about Main Street economics, eventually what you see around you overwhelms the great pretending. CTH has been outlining the state of the consumer economy in great detail for quite a while, and though it is difficult to note when the outcomes will surface, eventually they do surface. [Reminder Here]

CONTEXT. CTH outlined the moment when the purchasing power of the U.S. middle class actually began contracting. It was March and April of 2021 when that Rubicon was crossed. We saw it in the second and third quarter data from 2021, but few were willing to admit.

What changed in those two months back in ’21 was a dramatic drop in the “unit sales” of stuff within the consumer economy. The drop in unit sales was hidden because it happened simultaneously with the first wave of massive spike in prices. Prices rose so fast the sales data was giving an artificial impression of sales growth, but in the background the actual unit sales dropped. Those analysts correcting and adjusting historic data to ‘inflation adjusted terms’ are now noticing.

Additionally, and not coincidentally – because the metrics are connected, you will note this line from the Wall Street Journal review of the producer price index. “The producer-price index, which generally reflects supply conditions in the economy, rose 6.2% in December from a year earlier, the Labor Department said Wednesday, the slowest annual pace since March 2021.” In essence, the current rate of wholesale price increase on materials is now returning to the rate of price increase that happened in the period when prices spiked. Again, this is predictable.

Inflation is the measure of the ‘rate’ of price increase over time. March and April of 2021 were the beginning of the first inflationary spike.

Driven almost entirely by the supply side shock from Biden energy policy, in the subsequent 20 months the rate of price increase skyrocketed, peaked August 2022, and now the rate of increase starts returning. This does not mean price declines; this means the rate of growth in the price increase is lessening.

This is a cyclical outcome.

After 20 months of dropping unit sales, a result of massive price increases; and as the rate of inflation now starts to moderate created by the cyclical nature of it; what we now see is the inability of the price increases to continue hiding the drop in unit sales. [Background pdf Data] Total retail sales data is now exposed and that’s why we will see this increasing story about negative sales data as the inflation cycle plateaus.

(Via Wall Street Journal) – Retail spending fell in December at the sharpest pace of 2022, marking a dismal end to the holiday shopping season as rising interest rates, still-high inflation and concerns about a slowing economy pinched American consumers.

Purchases at stores, restaurants and online, declined a seasonally adjusted 1.1% in December from the prior month, the Commerce Department said Wednesday. Sales were also revised lower in November and have fallen three of the past four months.

The decline in retail spending late last year adds to signs that the U.S. economy is slowing. Hiring and wage growth eased in December, U.S. commerce with the rest of the world declined significantly in November, and existing-home sales have fallen for 10 straight months. The Federal Reserve said Wednesday that industrial production slumped in December, led by weakness in the manufacturing industry.

S&P Global downgraded its estimate for fourth-quarter economic growth by a half percentage point to a 2.3% annual rate after Wednesday’s data releases. Economists surveyed by The Wall Street Journal this month expect higher interest rates to tip the U.S. economy into a recession in the coming year.

“The lag impact of elevated inflation weighs heavily on U.S. households, it’s very clear that the median American consumer is still reeling from the loss of wages in inflation-adjusted terms,” said Joseph Brusuelas, chief economist at RSM US LLP. “We’re moving towards what I would expect to be a mild recession in 2023,” he added. (read more)

When the Baghdad Bob economic pretenders say, “mild recession,” anticipate something more akin to a mild nuclear meltdown, something with breadlines and soup kitchens.

Now, you must keep in mind that almost every financial media outlet used the same Retail Federation talking point about anticipating an 8% increase in holiday sales last year. [Reminder] Apparently, collective pretenses must be maintained. Meanwhile, news crews and camera crews were having a desperate time finding any holiday shopping to use as background footage for the claims that sales were strong. Here we are in January and the pretending has hit reality.

Negative retail sales in November and December when prices are roughly +10% over the prior year, means the unit sales collapse was far more dramatic…. Far more.

Trying to survive policy driven price increases in housing costs, energy costs, electricity costs, home heating, food and fuel costs has forced consumers to reevaluate purchasing decisions. Consumer demand for non-essential items has collapsed, and Americans are dig deep into their savings just to sustain unavoidable expenses. Eventually, pretending this is not happening is going to run into the wall of reality.

On one hand the leaders of large multinationals must pretend everything is splendid; after all, the only acceptable position they can articulate is to support interest rates being raised because demand is just too darned high…. pretending. But on the other hand – those same suppliers and multinationals are furiously trying to calculate how to avoid being stuck with billions worth of unsold inventory and idle industrial equipment.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America