Armstrong Economics Blog/Sovereign Debt Crisis

Re-Posted Jun 12, 2020 by Martin Armstrong

Illinois became the first entity to borrow from the Fed’s new facility known as the “Municipal Liquidity Facility” for state and local governments. The Fed’s legal authority lies in section 13(3) of the Federal Reserve Act. This authorizes the Fed to directly lend to “individuals, partnerships and corporations” in “unusual and exigent circumstances.” Section 13(3) is titled “Discounts for individuals, partnerships, and corporations,” raising questions whether the Municipal Liquidity Facility is actually authorized under Section 13(3). This has been capped at $500 billion.

To qualify they need a credit rating which is always up for sale to the highest bidder as we saw in 2007. Illinois is already insolvent and its debt is trading at junk bond status. However, as long as they pay the fee, one of the credit agencies can certify a rating which is arbitrary so they get the funds for a kick-back. Welcome to the wonderful world of corrupt credit ratings. This proves that Illinois cannot hope to raise money to borrow. Someone should just turn out the lights.

British Pound Down & Dirty?

Armstrong Economics Blog/BRITAIN

Re-Posted Jun 10, 2020 by Martin Armstrong

I have received a lot of emails from Britain asking if Boris is the new reason for the collapse of the pound. Fundamentals always emerge to support the projected trend. Boris is approving contract tracing which will undermine the economy dramatically. This is a plot by the socialists to realize their Marxist dreams. The press is so intensely keen on keeping COVID as a national security threat that it is really hopeless.

The British pound appears to be still destined to break the 1985 low. However, we first need the false move with the dollar down to trap everyone into short-dollars and then this will flip around. Contact tracing and certificates to prove you do not have COVID will end tourism for Europe. No Americans will be traveling there if they have their way. The stupidity of Boris and other European world leaders is beyond description. I think I have seen London for the last time already.

We are in a battle with the socialists on an unprecedented scale. They are deliberately destroying businesses under the pretense of the New Green Deal.

Global Unemployment

Armstrong Economics Blog/Economics

Re-Posted Jun 9, 2020 by Martin Armstrong

COMMENT: Dear Mr. Armstrong,

According to a survey done by an online HR/recruitment firm (link attached above), 1 in 5 of Malaysians lost their job due to MCO aka lockdown arising from the COVID.

This is a stark contrast from what mainstream media reports or official numbers. It looks like things are getting ugly when reality sets in.

Stay safe and stay healthy. God bless America!

S

REPLY: It appears that on average, the global unemployment rate is around 20% thanks to COVID-19. Certain places where they rely on tourism has reached 50%+. This is so profound. Governments in Europe are telling people to stay home for vacations and not travel to southern Europe. Americans have been terrorized by the media not to take cruises or travel by plane. This summer will only heighten the sovereign debt crisis as we head into August.

What is Different This Time Between 1987 & 2020 – 33 years Later?

Armstrong Economics Blog/ECM

Re-Posted Jun 9, 2020 by Martin Armstrong

Your loyal follower on this quest for knowledge.

PGD

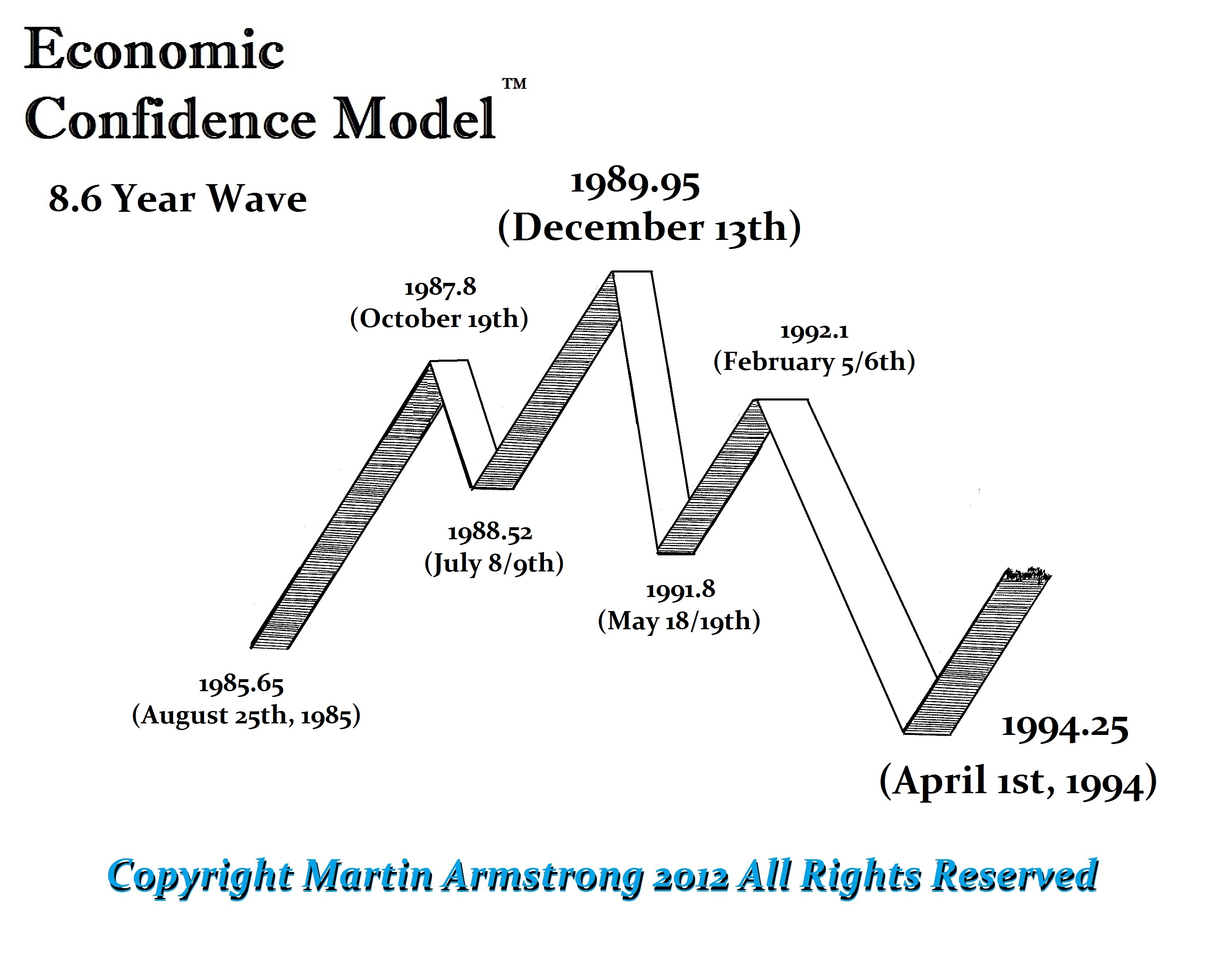

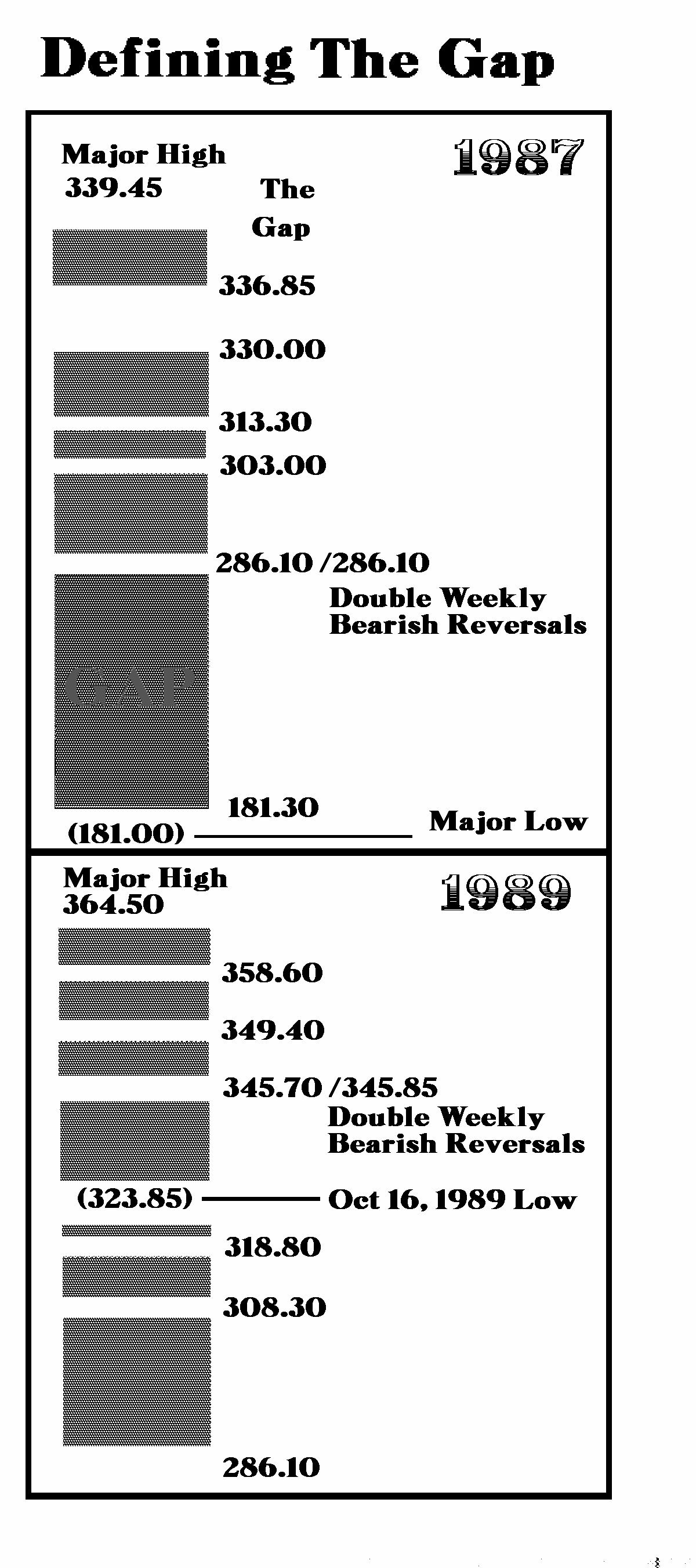

ANSWER: The 1987 Crash took place on the day of the ECM on October 19, 1987. So we have the low on the turning point, which confirmed that we should make new highs by the next turning point 1989.95.

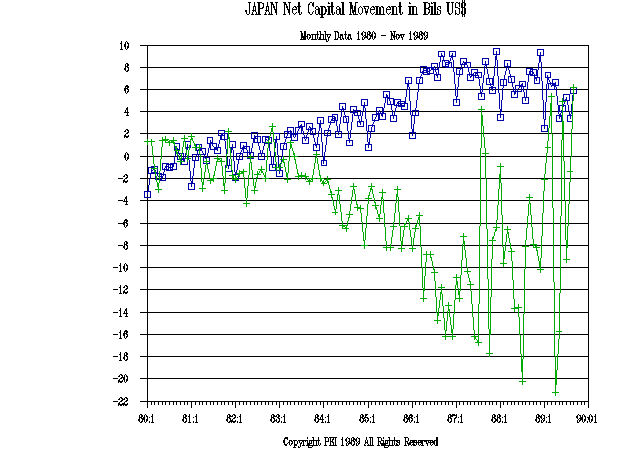

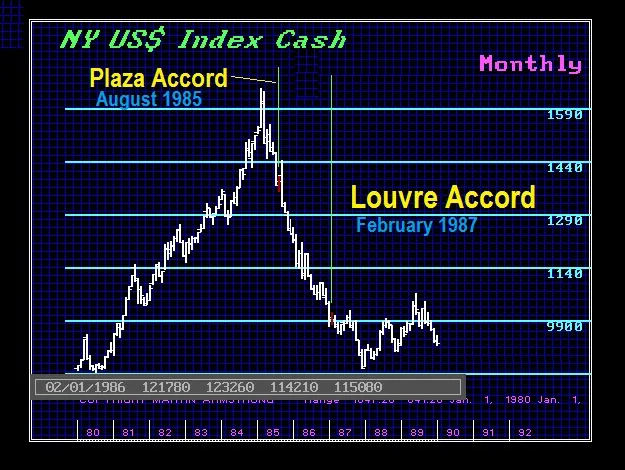

The cause was termination from the foreign exchange markets set in motion by the stupidity of the G5 in trying to manipulate the dollar lower for trade AFTER they sold 1/3 of the US national debt to the Japanese.

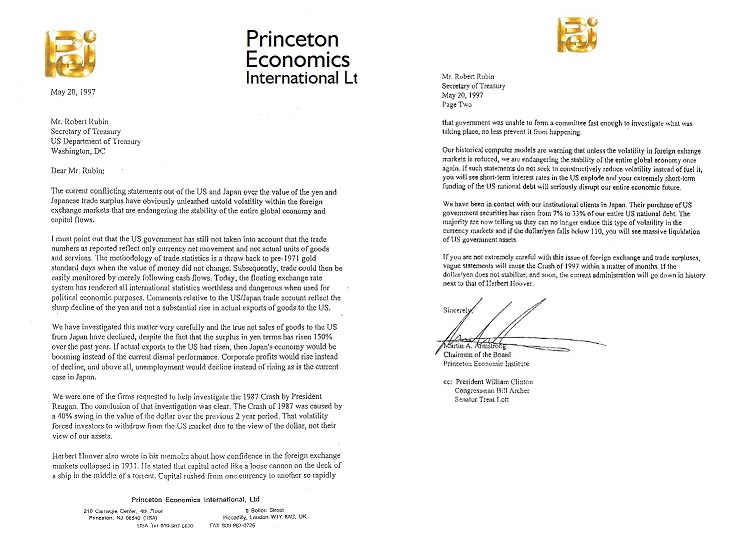

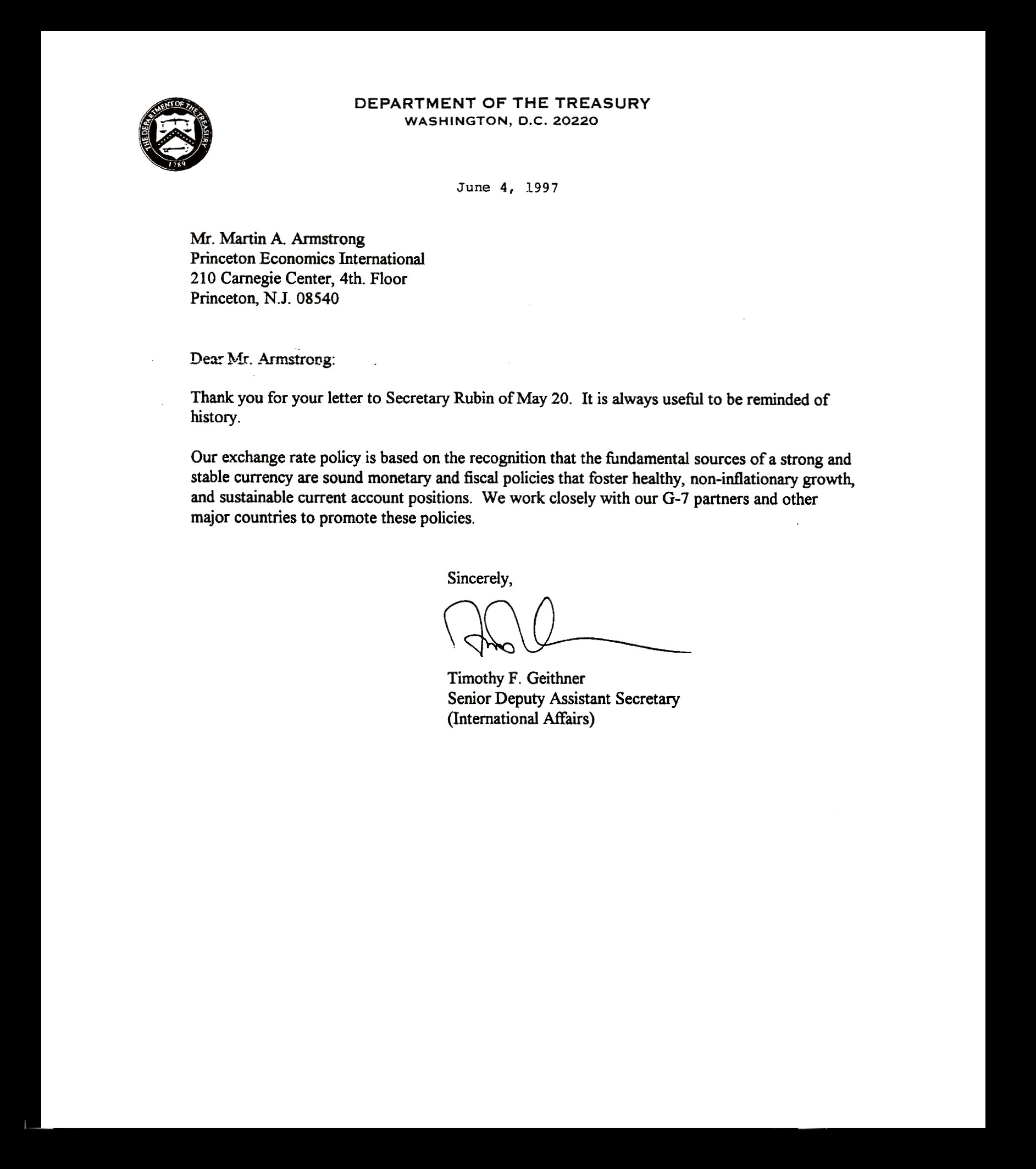

By attempting to manipulate the dollar lower to gain trade benefits, they fail to understand that foreign investment in the US would also be repelled. You cannot lower the value of a currency by 40% to help trade without causing losses to foreign investors. So the 1987 Crash was currency driven and not economic. When Rubin was trying the same stupid nonsense in 1997, 10 years later, that is when I warned them this was a stupid idea that created the 1987 Crash. They responded, but more importantly, they backed off.

This time we have brain-dead epidemiologists who are as corrupt as a $3 bill and should be thrown in prison for the global damage they have done deliberately without regard to the people. They have sold their souls to the Bill & Melinda Gates Foundation, which should be investigated for covert activities. The economic patterns are distinctly different and reflect the actions of a terrorist organization. This was not the mere stupidity of unqualified people in government. We have billionaires acting like usurpers, seizing power to force their vision of the future upon the rest of society.

This has been a direct assault to destroy and redesign the economy from the ground up. The patterns are completely different and display a frontal attack upon the economy. This is not a result of an unintended consequence of manipulating one market without comprehending the interconnectivity throughout the entire system. This has been a deliberate attempt to destroy the economy and our way of life as we have known it. Therefore, the stark difference has been the collapse of many sectors that have been set in motion deliberately. We then see European politicians gleefully looking at this as an opportunity to rebuild the economy from a green perspective. You have Spain introducing basic income which is all designed to move Europe into a full-blown Marxist state by eliminating paper currency. Soon, they will default on all debt by transforming all government debt to perpetual bonds when they realize they cannot sell debt anymore.

When we look at the 1987 Crash, the entire event was 8.6 weeks. It bottomed with the ECM, which was not the case this time. Moreover, there was a set of Double Weekly Bearish Reversals at 286.10. Once they were elected, there was nothing on our system models, including technical, that would reflect any support until we reached the Monthly Bearish Reversal. Hence, the forecast we would drop 10,000 points and then bottom wit the ECM.

The Monthly Bearish Reversal was 180.30 and the low was 180.00. That met all our criteria perfectly. But look at the pattern for the recovery. We do not see the strong immediate bounce as we have seen this time. In fact, it took 41 weeks to elect the first Weekly Bullish Reversal. There was a slow but steady advance which was reflecting the underlying strength within the economy. There was no Paradigm Shift, but a disruption to the foreign exchange markets which is the foundation of international capital investment.

The G5 was created at the Plaza Accord in 1985, calling for the dollar to decline by 40% to reduce the US trade deficit. As the dollar fell too far, other members complained and this led to the Louvre Accord in February 1987, when they declared the dollar had declined far enough. The dollar kept falling, the sentiment shifted, and everyone began to question if the central banks were capable of doing anything. Hence, by October 1987, there was a massive panic selling in the dollar which led to selling dollar assets.

Energy & the Stock Market

Armstrong Economics Blog/Stock Indicies

Re-Posted Jun 8, 2020 by Martin Armstrong

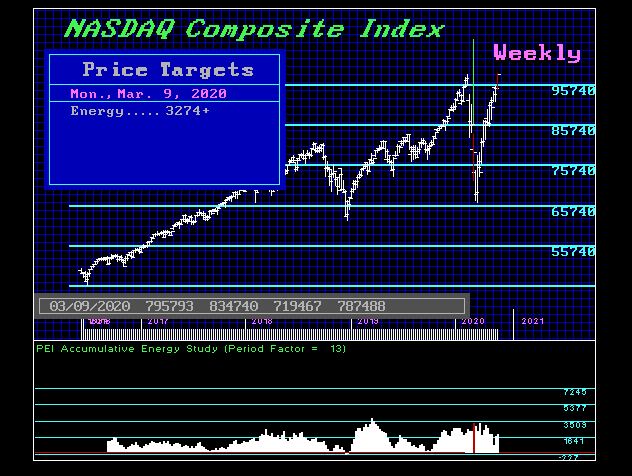

QUESTION: Marty; Your energy model seems to be warning that the bounce is not going to last. I have followed the reversals and they have been great for the bounce. What I have noticed is your energy model peaked two weeks before the low but as the market has rallied, energy has been declining. The 2018 December low your energy bottomed with the low and that was a good rally. This seems to be the opposite. Is my interpretation correct?

DF

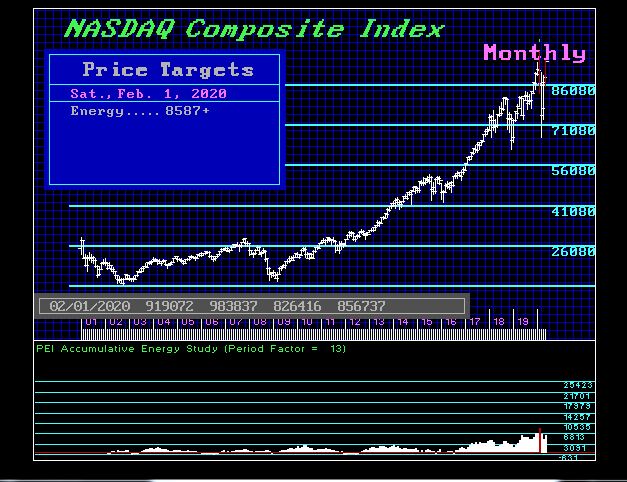

ANSWER: Yes. We have a divergence on the weekly level with the typical novice rushing in to buy based upon the fact the market has simply rallied. They will always judge the next 5 years by a few weeks of price action. When we look at the monthly level, the peak in price was very high in energy which has been declining ever since. This also warns of caution. Keep in mind that we had a nice 11-year rally in the Dow & S&P500 from the 2009 low. That is a traditional bull market. But the NASDAQ bottomed in 2002, not 2009, so that was an 18-year rally, which is significantly different.

German Companies Plan to Reduce Investments

Armstrong Economics Blog/Germany

Re-Posted Jun 7, 2020 by Martin Armstrong

According to a recent survey conducted by the Institute for Economic Research (Ifo), German companies plan to reduce investments by 50% this year due to the lingering effects of the coronavirus. In fact, 28% of companies reportedly already canceled investments. The manufacturing sector, the heart of the German economy and therefore the entire Eurozone, purportedly plans to cut back projects and future investments by 64%, and 32% reported that they have already canceled business ventures entirely.

The coronavirus cannot account for the toll on German manufacturing, as 2019 was the worst year for that sector in a decade. In February of this year, the Financial Times reported that ECB President Christine Lagarde said low rates and inflation “significantly reduced the scope for the ECB and other central banks worldwide to ease monetary policy.” This was in February when the main concern was the US-China trade war, as Germany imports 9.4% of intermediate goods from China.

Chancellor Angela Merkel wants to pump $146 billion USD ($130 billion euros) into a stimulus package, while of course designating $56 billion USD of those funds to further the climate change agenda. The German economy already shrank by 2.2% in the first quarter. Merkel recently announced that she will “absolutely not” run for a fifth term, meaning she will leave her mess for the next person to clean up.

Sovereign Defaults Unfolding

Armstrong Economics Blog/Emerging Markets

Re-Posted Jun 3, 2020 by Martin Armstrong

In the Gulf, states are facing bankruptcy. Oman can hardly even pay his electricity bill. The IMF has been now lobbying to defer emerging-market debt for one year. We have been able to confirm from behind the curtain that more than 100 nations have asked the IMF for help. The sheer stupidity of this coronavirus lockdown is beyond belief. It seems no politician bothered to ask advice from anyone other than epidemiologists. Neil Ferguson may have resigned for bad judgment, but the politicians who failed to consult other fields including economics should resign. The lack of common sense amounts to the said fact that politicians have set off a Monetary Crisis cycle over the next two years, for they have seriously disrupted the entire world economy. These emerging markets will not be able to pay their debts any time soon, especially when European politicians are trying to convert the economy to a New Green Order.

Thatcher on the Redistribution of Wealth Rather than Creating Wealth

Armstrong Economics Blog/Economics

Re-Posted May 31, 2020 by Martin Armstrong

Trump Could Launch the Receivables Liquidity Corporation

The RLC backed by the government is in a better position to wait out the economic recovery and collect at the best time and have an organized collection program

Re-posted from the Canada Free Press By Jonathon Moseley —— Bio and Archives—May 24, 2020

We are fortunate that President Donald Trump is a businessman who knows how to bounce back from difficulties. However, the United States really is already in a depression. We don’t yet have technical indicators stretching over several quarters. Yet: “Total nonfarm payroll employment fell by 20.5 million in April, and the unemployment rate rose to 14.7 percent, the U.S. Bureau of Labor Statistics” reported on May 8.

We can fix this. But it will take swift and decisive action. We’ve seen it in movies: The giant airplane is in a power dive heading down into the side of a mountain. The hero manages to restart the engines and turns the nose up just in time to clear the mountainside and head back upward.

This is a proposal based on my years as a debt-collection attorney in Virginia

President Trump could create a Receivables Liquidity Corporation. (You heard that name and idea here first.) After the Savings & Loan crisis, the government created a private corporation backed by the U.S. Treasury, called the Resolution Trust Corp. The RTC took over failing banksand slowly liquidated their assets at opportune times. During the 2008 mortgage crisis bailouts, allegedly the U.S. Treasury turned a profit eventually. The government sold the stock it acquired in the bail outs at a time of panic (low prices) and then sold them after the economy had grown healthy (high stock prices).

This is a proposal based on my years as a debt-collection attorney in Virginia. This could work for Canada, the European Union, now independent England, even the Bahamas or almost any country – not just the United States. It can even work combining several nations together. However, it does require a nation with sufficient financial credit to carry debts for a long time until the ideal time to collect on them. And it requires a mindset to think outside the box with a more business-oriented public private partnership.

The engine has seized up. When we try to start the engine again, it is going to be bad. If everyone pulls back and values plummet just because people are frightened, the damage will be far greater than if the new RLC takes payment much later, after things have rebounded.

As soon as the economy re-opens, it will end the freeze on evictions of renters behind on their rent and foreclosures on mortgages. Within two months of re-opening, many of those 20.5 million unemployed could be homeless. Those unemployed won’t be able to suddenly repay 2 to 4 months of overdue rent or mortgage payments.

President Trump hoped early on that there would be pent-up demand and the economy would snap back. But he acknowledged back then that the longer the economy stays closed the harder it would get. Now, there may be a lot of desire to buy. But will people have the money to spend?

Consider the situation for many small businesses: As a solo attorney, I am a small business. Before the pandemic, clients typically had no money to pay me. Now, no one is paying them. They have on-going expenses for food and what rent they can cover, with no income in most cases. The people who should be paying them have no money because they are not getting paid. So I’m not getting paid for past work or hired for new work. So my vendors aren’t getting paid. Etc. A negative cascade.

The stimulus checks in the United States were small and late. For many businesses, the $10,000 small business advance loan never arrived. And the Paycheck Protection Program Loan—for the very small businesses who can get one—is only 2 ½ months of a business’ payroll after cutting any salaries above $100,000. The size of the economy is enormous.

However, those programs do not have to be repaid. The only way that the U.S. Government can afford to spend a lot more is if the money is repaid—eventually.

How? The time horizon for small business is short. They can’t survive for long without getting paid by clients. By contrast, the Treasury can carry those invoices for years until the economy has rebounded and the debtor can afford to pay.

So let’s say a landlord is owed 4 months’ rent for a business or a residence. Once the economy restarts, and the ban on evictions is over, he’s got to collect that unpaid rent from people who don’t have any money after 4 months of house arrest. Or businesses have shipped products that they haven’t been paid for. Or utility companies have overdue utilities for 3 to 5 months. What are they going to do? If they try to collect, they will leave businesses in the dark without electricity or homes without water. How is the economy going to rebound like that?

Instead, the landlord or utility company sells the invoice to the Receivables Liquidity Corporation and gets paid in full. Hopefully, the invoice eventually gets paid to the RLC with interest when the economy has recovered. The debtor must agree to:

- waive rights to discharge that particular debt in any bankruptcy,

- provide the owner’s personal guarantee for a business,

- waive the statute of limitations,

- consent to deduction from tax refunds,

- certify that they do not dispute the debt or to what extent, and

- add interest if the invoice did not provide for it.

In return the debtor gets a grace period of one year or more before having to start repaying the invoice(s) (with a possible hardship extension if circumstances warrant on application). The debtor would get an installment plan to pay back over time. If the debtor does not agree they are subject to immediate collection action. So they have motivation to agree to the terms. If they cooperate, they get a breather of at least a year before they have to pay.

The RLC backed by the government is in a better position to wait out the economic recovery and collect at the best time and have an organized collection program. While some invoices will not get paid, hopefully enough will be paid with interest and collection fees – eventually—to come close to breaking even.

One small problem: Who would run this program? Wink. Call me….

Is this Unfolding Faster than Expected?

Armstrong Economics Blog/Understanding Cycles

Re-Posted May 25, 2020 by Martin Armstrong

QUESTION: Mr. Armstrong, you have been targeting 2021 into 2022 as a critical time. Do you think this is unfolding faster than expected, or is this yet another sucker rally to get people all trapped in again on a bounce and then slaughter them? I find it curious how people get so bullish at every high and it smells that way now. What do you see in the near-term? I saw Socrates traded the rally in gold very good, but the ratio just shifted and it did not make a new high. It looks like weakness is coming back. All these people clamoring that they missed the NASDAQ rally look like they will be separated from their money really soon. What do you think?

FP

ANSWER: You have to subscribe to Socrates for each particular market. I do not have the time to comment on every single market and you cannot make a comment of the Dow and apply to another index any more than gold applies to silver or platinum. They are all different. Socrates is there for a reason. It is objective without bias and is not written by any person – it is totally computer generated which is a good thing in times like this. We all have our prejudices that can get in the way of objectivity. That is why people sell the low and buy highs.

We definitely have to be careful here for it is true that only fools rush in where wise men dare not tread. With all the chaos in the world, these people who think they missed everything with the NASDAQ rally merely illustrates how naive they are to even think the market can rally from here with no problems because some states are opening up. They will simply become the fuel for the moves ahead.

Those are the people who inevitably buy the high because they get so caught up always at the top. The pattern which seems to get the emotions flowing the most is always the Knee-Jerk Reaction before the high. This is often the strongest type of move just before the high which sucks them all in at the top thinking this is it and here we go. They want to pretend to be investors, but then they want to really trade every move.

When we look at the German DAX, there we have elected ALL FOUR Monthly Bearish Reversals from the February high but we also elected a Quarterly Bearish Reversal at the end of March. This is a clear warning that we have a very serious shift in the trend moving forward into 2022. We have not elected any Quarterly Bearish Reversal in the Dow, there is obviously a major shift in trend within the US v externally even with the lockdown.

We are NOT ahead of schedule. June remains a Directional Change and July is the next key target. We then have the 2020 elections coming and that will have a major impact upon the confidence behind the dollar into 2022.

Nobody is capable of forecasting this type of market from a gut perspective. This is the entire reason you need to look at Socrates per market and not assume anything. This is something that cannot be judged even fundamentally because there are so many things changing only a fool will assume they can see the future reducing everything to a single cause and effect.

So far, there is nothing that suggests the trend has accelerated. The swings are still within historical movements. The NASDAQ is different for its low was 2002 not 2009. Obviously, you cannot apply the same outlook to the NASDAQ as you see in the S&P500 or the Dow. To each its own, as they say.

We are creating a new index with 30 stocks to reflect the Paradigm Equity Shift. We are working on a special report to cover this event since it is the first time it has taken place since the 1930s.