Posted Originally on Dec 1, 2023 By Martin Armstrong

A recent report by KBW Regional Banking Index (KBW) suggests that Comerica, Zions, and First Horizon are at risk of being acquired by greater competitors. Larger banks with strong returns, such as Huntington, Fifth Third, M&T, and Regions Financial, are positioned to grow by acquiring smaller lenders. Additionally, KBW analysts noted that Western Alliance and Webster Financial could also consider selling themselves. The report highlights that regional banks with assets between $80 billion and $120 billion are facing increasing pressure on returns and profitability, making them potential targets for acquisition by larger rivals.

This analysis underscores the challenges faced by banks in this asset range, as they have the lowest structural returns among banks with at least $10 billion in assets, necessitating growth to help pay for upcoming regulations. The report also mentions that banks with higher returns, such as East West Bank, Popular Bank, and New York Community Bank, could end up as acquirers rather than targets. This analysis reflects the evolving landscape of the banking industry and the potential for consolidation among regional banks.

Three banks have already collapsed in the US this year. New proposed regulations would require banks with over $100 billion in assets to hold onto long-term debt equal to 3.5% of total assets or 6% of risk-weighted assets. Now banks just below the $100 billion mark will potentially face the burden of adhering to these new regulations. Regional bank shares have fallen by over 20% this year. Smaller banks are already struggling to remain profitable, while midsized banks will be forced to join a larger banking organization to stay afloat.

Reposed from Armstrong Economics Blog Posted Apr 25, 2023 by Martin Armstrong

QUESTION: Mr. Armstrong, Your knowledge and database on financial crises is really unprecedented. I googled the first banking crisis and it brought up only the Crisis of 1763, which started in Amsterdam. Yet that list published in the WSJ which showed 1683 as the first panic and the siege of Vienna was most interesting. I know you have written about the sovereign defaults on the ancient central bank in Delos. My question is, was there any major financial banking crisis between antiquity and 1683? I figured if anyone would know, he had to be you.

PF

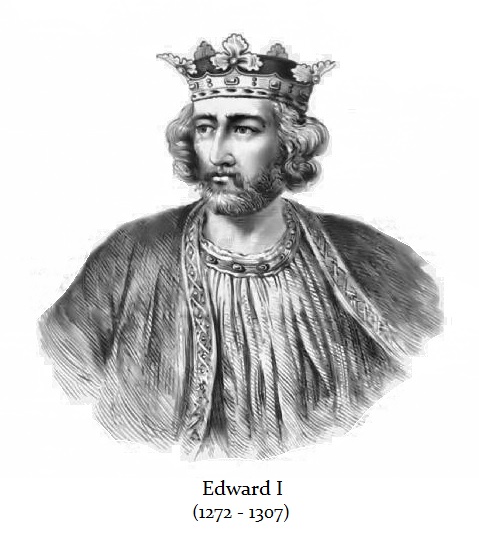

ANSWER: As the 13th century unfolded, the cost of endless Crusades burdened both the crowns of England and France. Throughout the remainder of the 13th century, a variety of Crusades were aimed not so much at toppling Muslim forces in the Holy Land but to combat any and all groups seen as enemies of the Christian faith. Edward began his reign in 1275 with heavy debts incurred from the Crusades.

These endless wars resulted in the time of major sovereign defaults by Edward I of England and Philip IV of France. In 1275, Edward secured a financial monopoly and negotiated a grant of export duties on wool, woolfells, and hides that brought in an average of £10,000 a year. He then used this as collateral to borrow substantially from Italian bankers granting them the security of these customs revenues to fund his endless wars of aggression.

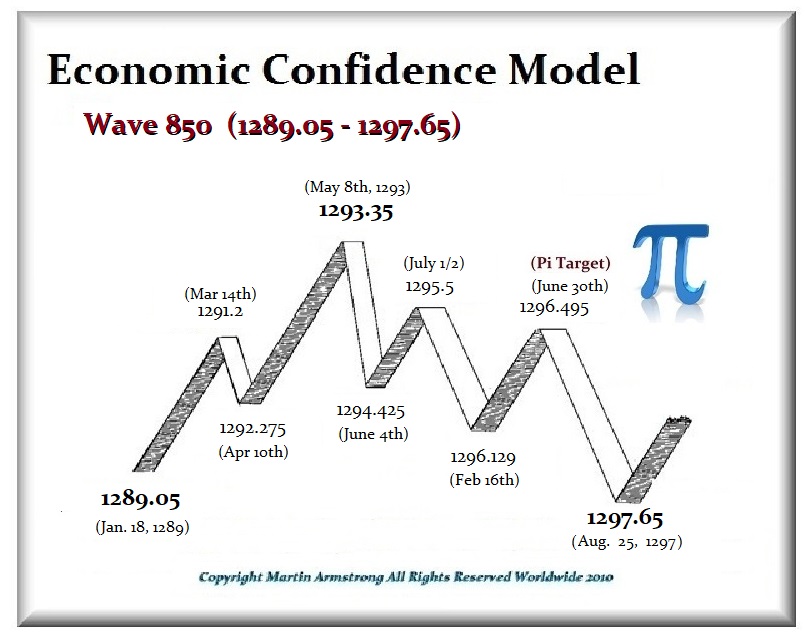

Edward imposed heavy taxes on the value of movable goods. At the beginning of this Wave 850, Edward defaulted on his loans from the English Jewish bankers, and then as 1290 began, to cover that default he expelled all of the Jews from England and confiscate all their property.

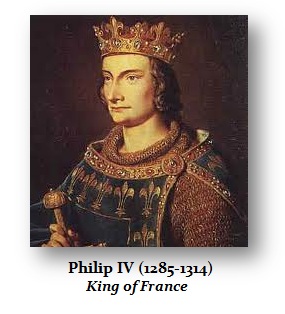

Moreover, this was the Edward Langshakes of the movie “Brave Heart” when in 1291 he attacked Scotland. As this 8.6-year Wave 850 peaked, Edward launched his very costly war against Philip IV (1295-1314) of France which lasted until the end of this 8.6-year wave came to an end in 1297.

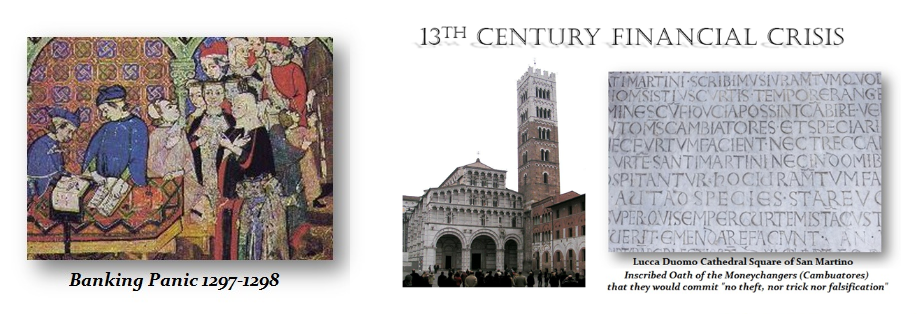

The Riccardi of Lucca was perhaps one of the major international merchant banking houses to emerge during the 13th century. The Riccardi established branches in Rome, Bordeaux, Paris, Flanders, London, York, and Dublin, Ireland. They engaged in trade with Edward I of England. Prior to 1272, the English kings were customers of the Italian merchant who had exotic imports as they were purchasing luxury goods and would use them to transfer money to Rome. With the outbreak of war against Philip IV in 1294, a major credit crunch and inflation erupted which impacted the entire international money markets throughout Europe at the time. The value of gold rose against silver from 10:1 to virtually 15:1, which was a monumental distortion of the European monetary system as a consequence of these endless wars.

Cash-strapped, Edward sought financial support from the Riccardi establishment but they refused to lend him any funds. In response, Edward seized all of Riccardi’s assets in England, effectively bankrupting them. The Riccardi had derived significant benefits in dealing with the English monarchy. They held contracts with special access to the English wool market. The Riccardi banking establishment was involved in about 50% of all the forward contracts with English wool producers, which were in effect futures contracts in the cash market. When Edward confiscated all the assets of the Riccardi, his action backfired. Nobody else would then deal with England in international money markets. This led Edward I to impose heavy levels of domestic taxation, which led to civil unrest. This led to a constitutional crisis of 1297.

We all may know that Magna Carta established rights that were forced on King John on June 15th, 1215. After John’s death, the regency government of his young son, Henry III, reissued the document in 1216, but it removed some of its more radical content. This led to civil unrest and at the end of the war in 1217, it became part of the peace treaty when it acquired the name “Magna Carta.” Henry III was compelled to reissue the charter again in 1225 in exchange for a grant of new taxes. Edward I was his son who was then once more compelled to reaffirm the Magna Carta in 1297 at the end of the 8.6-year Wave 850. That is when Edward I was forced to confirm that the Magna Carta was England’s statute law. That is when it actually became England’s rule of law.

The Bonsignori bank was known as the Gran Tavola, which had become the most powerful of the Italian merchant banking firms throughout Europe between 1255 and 1298. The Gran Tavola was indeed the greatest bank of the 13th century with branches in Paris, Marseille, Genoa, Bologna, and Pisa in addition to the main office in Siena.

Philip IV of France was also strapped for funds. He chose the debasement of the coinage which was massive. Philip had no other course of action to meet the expenses of the war. He began as a massive debasement of the coinage. Silver began to migrate out of France. This debasement only accelerated after 1298 when Philip IV confiscated all the assets Italian bank known as the Gran Tavola in France on claims that they owed him money, without netting anything with respect to his loans owed to them. This caused a major banking crisis in 1298 with the collapse of the institution which also held funds for the Papacy resulting in their loss of 80,000 gold florins. This was the first Banking Panic post-Dark Age. This confiscation of assets wiped out Siena and the city never again rose to the forefront of European commerce. By 1320, Siena was no longer a significant city in international commerce whatsoever which was a direct attack on the Papacy by Philip IV. This resulted in shifting the banking power to Florence.

A full-blown financial panic unfolded as silver migrated overseas. People hoarded the old currency and by 1301 there was virtually no silver remaining in the open market in France. Currency depreciation let Philip cover the cost of the war but it destroyed the credit of France and that ultimately led to France seizing the Papacy and strip-mining all its assets moving the Church to Avignon where a French Pope was installed. They then seized all the assets of the Knights Templar and burned all resistance alive. The Knights Templar were effectively an international transfer agent. If you were in France and needed to pay someone in Italy, you gave the money to the local office in France and they instructed the brank in Italy to pay. It was a 13th-century version of a wire transfer service. That is why the French crown seized the Knights and strip-mined all their wealth as well.

Obviously, this banking crisis of 1298 was far beyond anything most people would have read about in a financial crisis. This is what I mean when I warn that those in power will do WHATEVER it takes to retain power, and religion never means anything at the end of the day.

People often ask if their money is safe in a regional bank. Yes—if you keep it under $250,000 to guarantee the FDIC insures those funds. Some clueless minds brainwashed into fighting the class warfare thought, “Oh well!” for people who had more than them in the bank and did not care if the Silicon Valley Bank or Signature Bank failed.

My phone did not stop ringing and the bankers wanted to know if they should cover ALL the deposits. I actually lost my voice, screaming, “YES YOU MUST COVER ALL THE DEPOSITS! ALL OF THEM!!!” Aside from the fact that no one deserves to lose their hard-earned money, the primary issue here is that failing to cover the deposits would have completely wiped out small businesses.

Small businesses comprise 70% of GDP and must be protected at all costs. They must park large sums in the bank to cover payroll to pay their employees and operational costs. Small businesses would come to a standstill and banks would fall like dominoes. Unemployment would spike and the entire economy would plummet. We would see a massive banking crisis if all small businesses went under. More banks will go broke, it is only a matter of time, but it is crucial that deposits are covered

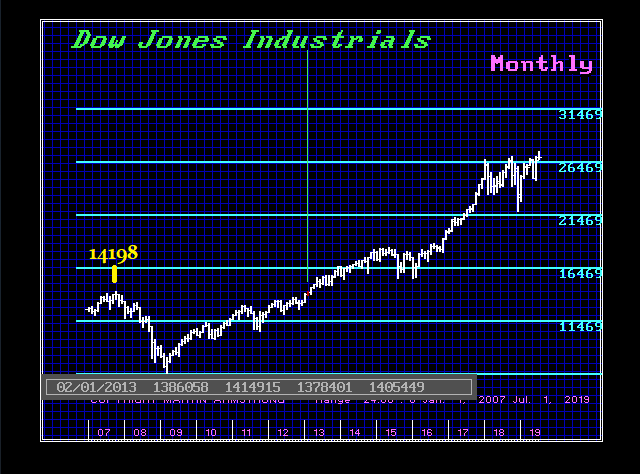

In 2010, Barron’s wrote a piece on me effectively laughing at my forecast that the share market would rally to new highs. What seems to inevitably unfold is this notion that whatever the event might be in motion, the mere thought of a reversal in trend appears impossible. When the press disagrees with Socrates, I know it will be the press who is wrong. And because they end up being wrong, of course, they cannot print a retraction so they will just pretend you do not exist rather than admit – Sorry, we were wrong. The Dow made that new high above 2007 by February 2013. That was 64 months from the October 2007 high.

I have been in the game for many years. With each event, it appears to be like Groundhog Day. They pop their heads out and declare they do not see their shadow, so the entire world will disintegrate and that is always based upon opinion. It is never backed by real analysis. Just the standard human trait of assuming whatever trend is in motion, will remain in motion.

Being an institutional adviser, I have never had that luxury. We have had to deal with some of the biggest portfolios in the world. They want accurate forecasting, and it has to be long-term – not day trading. They are not interested in the typical headlines of doom and gloom that the press love to print with every financial event simply to get readership. That is all they care about. It has been the financial version of the fake news.

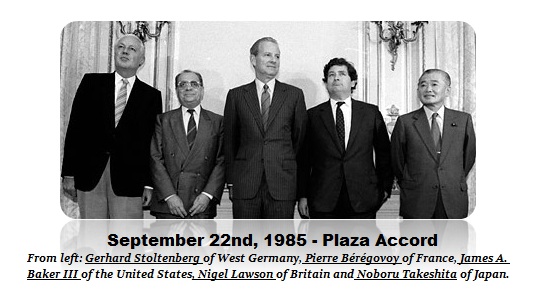

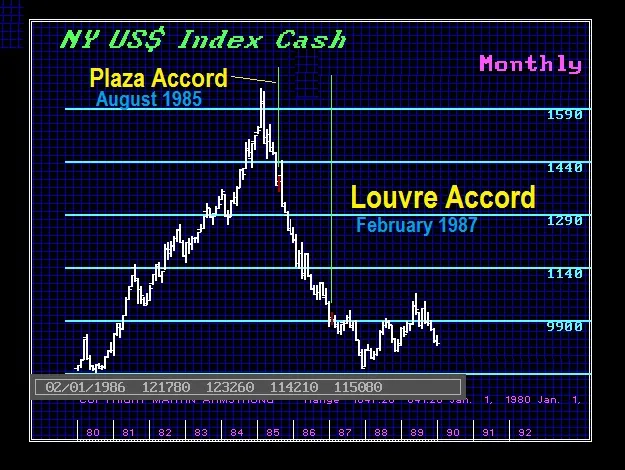

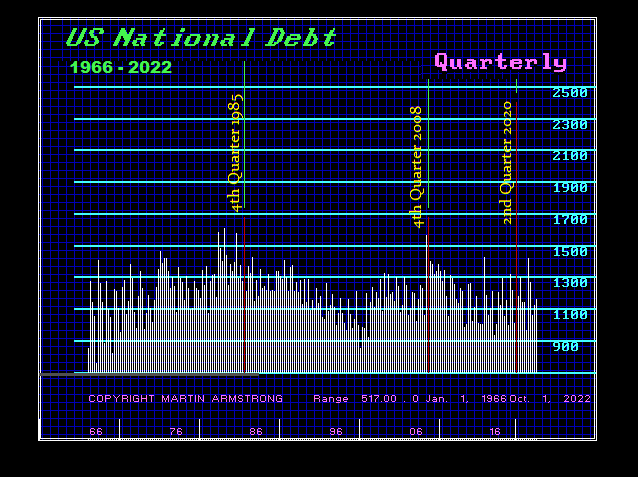

When we step back and look at this favorite fundamental that people beat to death to predict the end of the world, the national debt, and the collapse of the dollar. Little did they know that the increase in National Debt during the 2007-2009 Financial Crisis was supposed to bring down the sky and end the existence of the dollar. We can see the sharp rise in debt simply made a double top with the Financial Crisis of 1985.

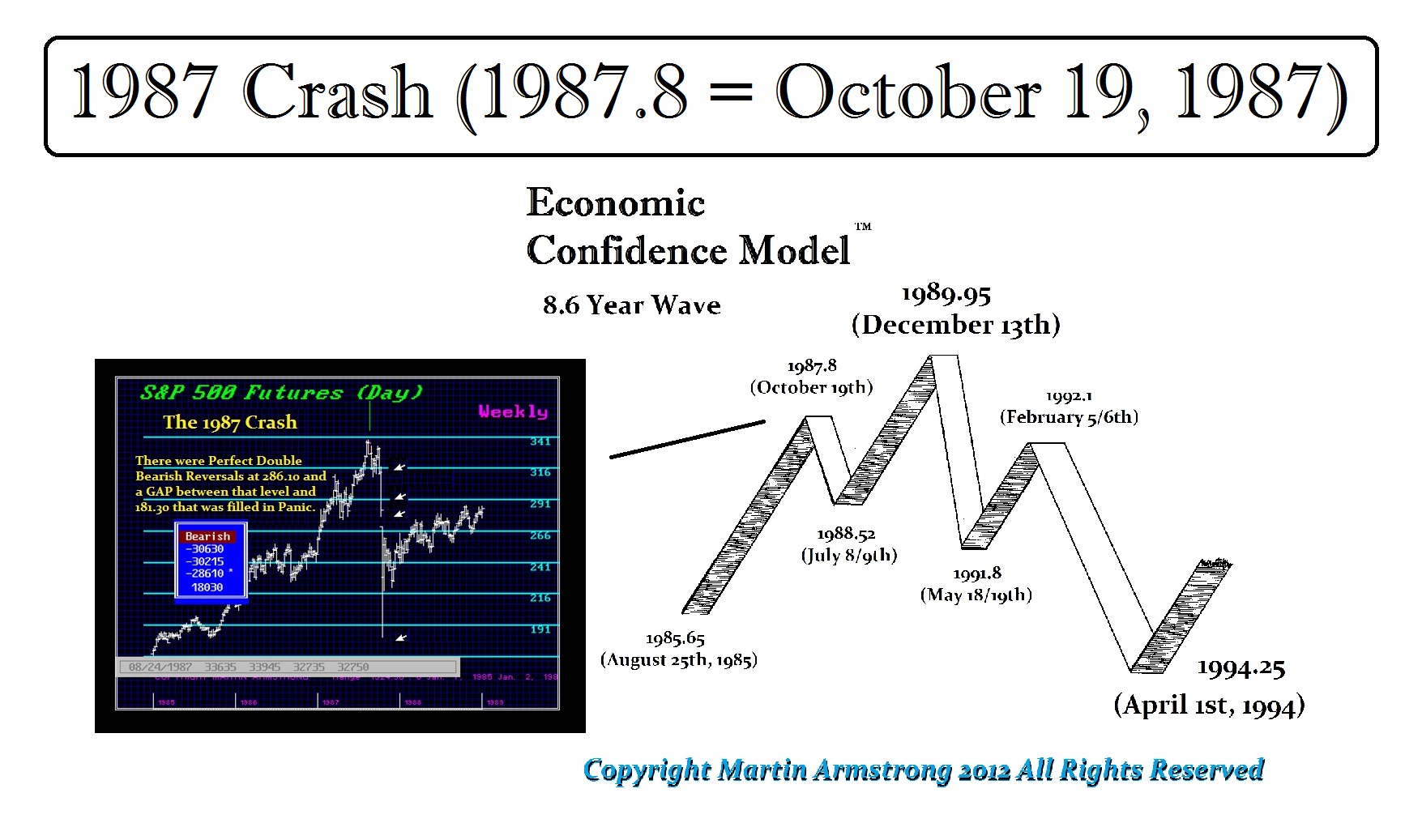

It was that previous 1985 Financial Crisis that set in motion the Plaza Accord which brought together the central banks creating what was then the G5 – now G20. Of course, like every government intervention, the side effect was the 1987 Crash and their attempt to reverse their directive at the Plaza Accord became the Louve Accord. When the traders saw that failed, the collapse in confidence led to the 1987 Crash.

It has always been a CONFIDENCE game as I pointed out with the 1933 Banking Holiday previously. In this case, the failure of the Louvre Accord which came out and said the dollar had fallen enough, once new lows in the dollar unfolded and the central banks could not stop the decline, led to financial panic by 1987 which manifested in the 1987 Crash.

This chart shows the quarterly change in the National Debt since 1966, Here you can see the 1985 and 2008 Financial Crises were on par. Neither one ended the dollar no less the world economy. So when I warned the share market would rally and make new highs and Barron’s laughed in 2010, I said the same thing after the 1987 Crash and people laughed.

In fact, on the very day of the low, I said this was it and that we would rally back to new highs by 1989. That was perfect and the market responded to the Economic Confidence Model (ECM) which has been published back in 1979. This was more than simply forecasting the 1987 Crash and the very day of the low. It clearly established that the ECM had revealed that there was a secret cycle behind the appearance of chaos even in economics.

Larry Edelson was actually a competitor at the time. But Larry respected that the forecast from the model was far beyond what people would ever expect. If we are ever going to advance as a society, we have to stop the bullshit and understand HOW markets trade and WHY. Larry did that. He understood that the model was something larger than just personal opinion.

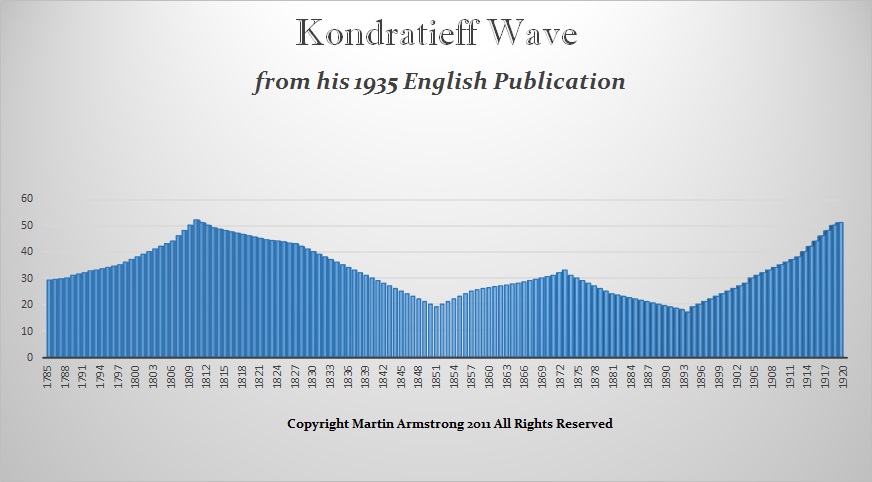

Even those claiming to be using the K-Wave cannot make real forecasts. The basis of Kondratieff’s argument came from his empirical study of the economic performance of the USA, England, France, and Germany between 1790 and 1920. Kondratieff took the wholesale price levels, interest rates, and production and consumption of coal, pig iron, and lead for each economy. He then sought to smooth the data using an averaging mathematical approach of nine years to eliminate the trend as well as shorter waves. Kondratieff thus arrived at his long-wave theory suggesting that the economic process was a process of continuous waves of boom and bust.

Kondratieff’s work was compelling and contributed greatly to the Austrian School of Economics that first began to develop the concept of a Business Cycle. The general central principle of the Austrian Business Cycle Theory is concerned with a period of sustained low-interest rates and excessive credit creation resulting in a volatile and unstable imbalance between saving and investment. Within this context, the theory supposes that the Business Cycle unfolds whereby low rates of interest tend to stimulate borrowing from the banking sector and thus then result in the expansion of the money supply that causes an unsustainable credit source boom which leads to a diminished opportunity for investment by competition.

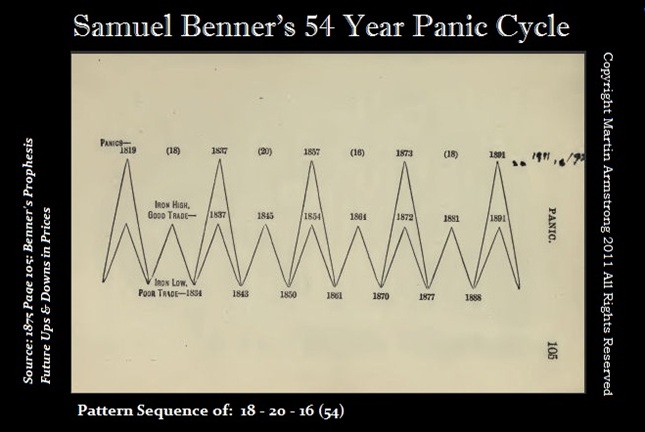

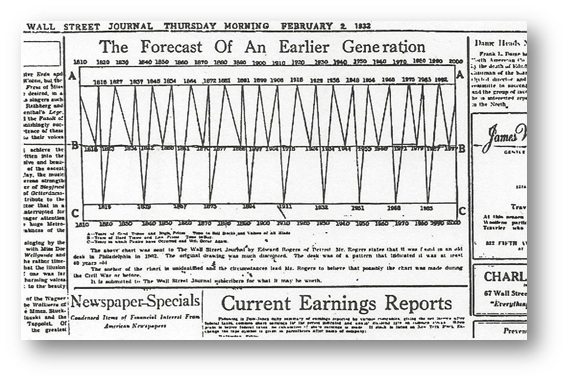

Here is a chart of the business cycle that was created by a farmer named Samuel Benner. Benner based his work on Sunspots, which actually incorporated solar maximum and minimum that today’s Climate Change zealots refuse to consider. Nevertheless, someone manipulated Brenner’s work and created a chart to try to influence society handing it in with a wild story to the Wall Street Journal published this cycle on February 2nd, 1932, when the market bottomed in July 1932. Still, nobody knew who had investigated this phenomenon in 1932.

When I was doing my own research reading all the newspapers to understand how events unfolded, I came across this chart. I found it interesting that during the Great Depression people were reaching out and some began to embrace cyclical ideas. The problem with both Kondratiff and Brenner was that the period they used to develop their cycles was the 19th century because the real Industrial Revolution was unfolding and in the 1850s, 70% of the civil workforce were all in agriculture. Consequently, if you constructed a model based entirely upon one sector, it would work only as long as that sector was the top dog.

Being a historian buff, it quickly hit me that NOTHING remains constant and that the economy will ALWAYS evolve, mature, and then crash and burn. Where agriculture was 70% of the workforce in 18590, it fell to 40% by 1900, and then down to 3% by 1980.

Just look at energy. The earliest lamps, dating to the Upper Paleolithic, were stones with depressions in which animal fats were burned as a source of light. In cultures closer to the sea, they began to use shells as lamps which they would burn at first animal fat. Clay lamps began to appear during the Bronze Age around the 16th century BC and the invention quickly spread throughout the Roman Empire. Initially, they took the form of a saucer with a floating wick.

We even find Roman oil lamps as luxury items crafted out of bronze. There are collectors of terracotta oil lamps for there is a vast variety of motifs. There is everything from dolphins, and various entities, to erotic oil lamps, which may have been used in brothels. The point is, if you constructed a model on oil, you would have surely accomplished similar results to Kondratief and Brenner.

Then of course, just as the energy moved from animal fats to vegetable oils, by the 19th century it returned to whale oil which was extracted from the blubber. Emerging industrial societies used whale oil in oil lamps and to make soap. However, during the 20th century, whale oil was even made into margarine.

Then the discovery of petroleum and the use of whale oils declined considerably from their peak in the 19th century into the 20th century. Ironically, it was fossil fuels that probably saved whales from extinction. Hence, now we are entering a period where they deliberately want to end fossil fuels and move to solar and wind power. Obviously, just a cursory review of energy reveals the problem of basing a model on the current energy source or major economic industry. Things change with time.

The Bank of International Settlements (BIS) has warned in its latest quarterly report that there is $80 trillion dollar in off-balance sheet dollar debt in the form of FX swaps. This has involved pension funds and other ‘non-bank’ financial firms.

What they do not explain is that each “debt” has a counterparty that has an “asset” and in theory, that works out to net zero. But there is counter-party risk that is not discussed. This doesn’t address the liquidity issue either. Still, it is not entirely a black hole as they seem to lead some to proclaim. What is also left unexplained or addressed is the question of if they are netting across all transactions. Many of the players in this market have offsetting positions. It is one thing to scream OMG the size of the stock market is too big, and another to yell fire in a crowded theater.

This $80 trill is effectively the derivatives market. It is what it is. Marking everything to market all the time isn’t a great answer either for there can be imbalances for a day or two in the middle of chaos. What is clear is that the BIS is raising concerns, in which it also said this year’s market upheaval took place without any major issues.

On the other hand, the BIS has been pushing central banks to raise rates to fight inflation which will only accelerate the crisis since it is shortage based. This is no different from the ’70s when there was an external price shock from OPEC,. Raising interest rates did nothing to prevent inflation, instead, it resulted in a strong dollar, the collapse of the pound to $1.03 in 1985, and the US national debt more than doubled on interest expenditures.

Nonetheless, the BIS has been quieter on the inflation front this time around. Just maybe, they are starting to realize that the old theories no longer work. The September UK government bond market turmoil was created by raising interest rates and the losses on holding long-term debt in the face of rising interest rates have been just the tip of the iceberg.

The FX swap markets have become huge. Our clients are well into the trillions these days whereas twenty years ago we had less than 5 clients at the $1 trillion threshold.

Nonetheless, the complexity of the cross-positions is the real risk. One side can blow out because of the chaos these braindead politicians are creating with this war against Russia.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America