Russia has come out and denied that their missiles entered Poland. It is time the West calls out Zelensky for what he is – a ruthless liar who should be removed from power to save humanity – forget the planet. I warned from the outset, this would be the man who will create World War III. He is a total disgrace. He has done nothing but lies to the world EVERY SINGLE TIME. Any Western Media who supports Zelensky are puppets of the deep state and are NOT independent journalists. If they did their job. they would report the truth.

The Ukrainians shot down the Malaysian flight MH17 and tried to blame the Russians in the Donbas. They used an old Russian missile that was no longer in use. The Ukrainians killed their own people to create a false flag before at Bucha. They massacred Russian civilians in Odessa in May and the West was silent. Those who went to Ukraine believing they were fighting for democracy have returned accusing Ukraine of carrying out war crimes.

Besides Zelensky outlawing the Russian language when the people of Eastern Ukraine are ethnic Russians who have lived there for centuries and Ukraine NEVER existed before the USSR, he has also carried out a Holy War outlawing Russian churches and demanding they are not subservient to Kyiv. They is no different from the French seizure of the Vatican and moving it to Avinion – the period of the anti-popes. He has done the same thing and outlawed the equivalent of the pope to Russian Orthodox. He has not just denied democracy by rejecting the Belgrade and Minsk Agreements where the Donbas was to vote for their own independence, but he has even denied them the Freedom of Religion.

This is the man who is destroying the world and the West cheers this character? Every newspaper that cheers the death of people on the battlefield and civilians all to support this ruthless greedy character, has washed their hands in blood. They should put on their high heels to join him on the world stage. Claiming they cannot “independently” confirm is not good enough They are COVERING UP the Truth.

Information is surfacing that we may be dealing with another Ukrainian desperate attempt to create World War III and that the missiles fired were from Ukraine. This is not yet verified but the US is now saying the missile attack is not yet confirmed to be from Russia. It would be nice if the West acknowledged that Ukraine is ruthless and NOT to be trusted. The Ukrainians killed their own people to create a false flag before at Bucha. There are reports that NATO has proof that the people were killed by Ukrainians. There are also confirmations that the claimed people shooting Ukrainians from the rood tops during Maidan were Ukrainians – not Yanukovich.

Russia fired a number of missiles at Ukraine taking down power grids and hitting Lviv which is just 50 miles from Poland. It appears that two of those missiles fell short and landed in Poland. Latvia’s deputy prime minister, Artis Pabriks, said Moscow had fired missiles that landed in Poland and Putin sent Warsaw his condolences. Meanwhile, the US Pentagon has said it could not confirm that Russian missiles had crossed into Poland.

The question is will NATO use this as the excuse they have been waiting for to launch a war against Russia next week or come January, or do they want Ukraine to run out of soldiers to wear down Russia first? The strategy has been to use Ukraine as they did in Afghanistan to fund locals to wage a war to defeat Russia by attrition. We created the Taliban and all the arms we provided in that proxy war then led to them turning against Americans and also the attack on 9/11 – the unintended consequences of proxy wars.

Despite the fact that McCain was a Republican, he conspired with Hillary against Trump and handed the fake dossier to the FBI because Trump would not fund his dream proxy war to have Ukrainians start the civil war against the Russians in the Donbas he started back in 2014. McCain and Hillary were both Neocons. Despite being in opposite parties, they both always wanted to destroy Russia. No doubt, Hillary is calling everyone urging World War III now using these two missiles that hit Poland proclaiming this is a war on NATO. US Intelligence now confirms that Russian missiles hit Poland. Now Poland has called an emergency meeting about the incident.

These people are desperate for war. They want to create world war III all to hide the collapse of our monetary system and the central banks cannot prop up the bond markets where nobody in their right mind would buy any long-term debt from any of these countries. The game is over! If they cannot keep the funding going for socialism, then it is time for war. As Maggie use to say – we have run out of other people’s money – just like FTX.

Posted originally on the conservative tree house on November 15, 2022 | Sundance

The White House is urging Nancy Pelosi to utilize the lame duck congressional session and construct a massive omnibus spending bill that will wrap Ukraine funding, COVID spending and a federal budget extension via continuous resolution. The request for Ukraine funding is an additional $38 billion.

Federal funds to support FEMA and hurricane recovery efforts will likely be part of the bargaining chips. Essentially, the sausage ingredients are: if congress doesn’t give Zelenskyy more money, then DeSantis will not get federal financial assistance.

If you don’t support Ukraine, you’re a Russian operative.

WASHINGTON DC – The Biden administration sent a letter to Congress on Tuesday outlining nearly a $38 billion request to help Ukraine continue fending off Russian attacks.

The administration is also asking for $10 billion in emergency health funding, with more than $9 billion going toward Covid vaccine access, next-generation Covid vaccines, long Covid research and more. About $750 million would be spent on efforts to control the spread of monkeypox, hepatitis C and HIV.

Congress has so far provided about $66 billion for Ukraine and other war-related needs. The administration argues that about three-quarters of that funding has either been spent or is committed to specific purposes.

An administration official said the White House plans to request additional disaster relief in the coming weeks to help with hurricane and wildfire recovery but didn’t provide any tentative figure.

The administration’s request for emergency money comes as appropriators aim to clinch a year-end government funding deal that would stave off a partial government shutdown on Dec. 16 and increase agency budgets for the current fiscal year. House Speaker Nancy Pelosi has already promised to provide more money for Ukraine in a government funding package, while some conservatives are arguing that the U.S. should cut off financial assistance and assess how funding for the country has been spent to date. (read more)

I reported in September that the Heritage Foundation estimated that the average American lost $4,200 since Biden became president. Within only a month, their analysis for October revealed that the average family had lost an average of $7,400. Around $6,100 of the loss came from annual income, while interest rates cost the average American $1,300 annually. For the analysis to nearly double in the course of a month is alarming, and it is reasonable to suspect that losses will become steeper due to current policies.

The Heritage Foundation said this estimate, obviously, does not “fully reflect the pain experienced by families.” They did not factor in losses from retirement accounts or investments. They certainly did not count the number who lost their careers due to pandemic mandates. Nor did they factor in the increased cost of borrowing money, mortgages, or the doomed bond market. They also did not factor in that he caused the public to lose all confidence in the government.

All gains under the Trump era were erased in less than two years. The changes that a new administration can implement are astronomical. The spending packages pushed forth acted as a temporary band-aid over a wound that will never heal. At least the generally uninformed public believed those packages would help, but that tide is turning as they can no longer offer unlimited free handouts. The economy was brought to a screeching halt in 2020, and absolutely nothing has been done by Washington to improve conditions since then. The spending packages lack all common sense and seem to be a deliberate attempt to hurt the country.

Anyone who wants to pay more for everything – go ahead. Those of us who voted for sensible politicians with real plans will send you the bill.

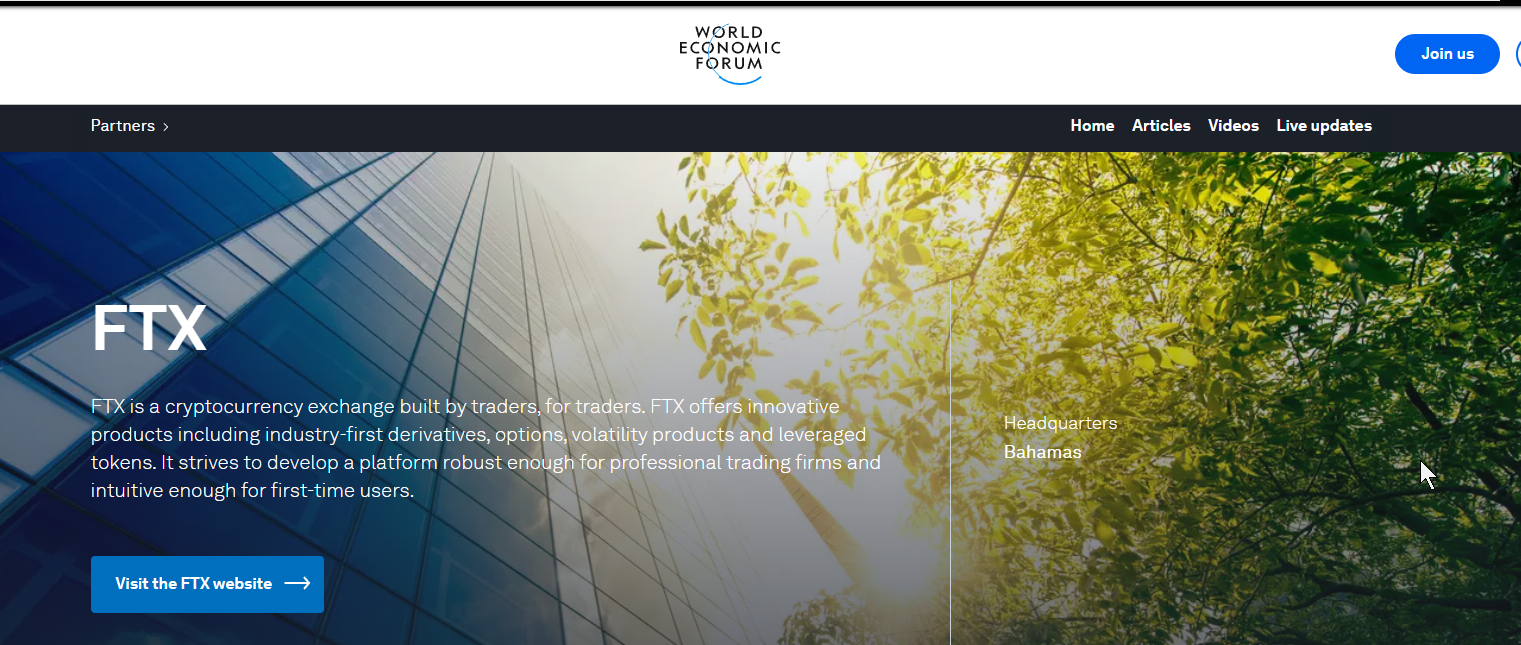

The collapse of the FTX Exchange is pretty straightforward insofar as this is the same lesson that constantly repeats in finance time and time again. Basically, FTX lent US$10bn of client funds to their trading arm Alameda, which used it for leveraged their own crypto speculation because the crypto market has been collapsing. Typically, someone like Sam Bankman-Fried had his whole life wrapped up in this venture. Lacking financial controls operating from the Bahamas, moving the money from client funds to his trading arm Alameda was possible. Historically, someone in this position sees his world collapsing but is not prepared to see that unfold for it requires admitting that he was wrong on crypto, to begin with. Consequently, such a person is not trying to actually rob clients’ money, they most likely see it as a temporary loan to save the company and the market will bounce back – or so they believe.

Our computer had picked the high in Bitcoin perfectly and has been projecting the collapse all along the way. But crypto has become a religion and in so doing it clouds the judgment of people who want to believe the story. Alameda blew up in a crypto meltdown because it did not want to accept that the crypto boom was over. The loan he probably thought would be temporary, vanished in the implosion. At first, I would have assumed they had actually invested the money and lost it on the bond market collapse. But that was perhaps too traditional. Here, it appears they were trying to defend their own cryptocurrency and trying to buy the low that kept moving lower. It appears he was allegedly simply using clients’ funds to trade keeping gains for his firm and the clients now suffer the risk.

It appears that they allegedly were trying to defend the crypto market and did not understand that the boom was over. The loans could not then be repaid. As crypto was crashing, some people needed to cash out. The attempt to pull out US$5bn from FTX exposed the fact that the cash was all gone. This is not so unusual. It has happened before. This time, the prosecutors are clamoring to be the one to charge him so they can become famous over his dead body.

FTX was a partner with Klaus Schwab’s World Economic Forum (WEF). Of course, the WEF has suddenly removed the page and is desperately trying to hide their involvement with FTX and Sam Bankman-Fried. Naturally, eliminating paper currency has been the goal of the WEF because they support the end of not just capitalism, but also democracy. Schwab’s push has been his Great Reset and to control society to impose his economic philosophy inspired by Marx and Lenin.

This is by no means the first violation of fiduciary responsibility that presents a custodial risk. MF Global Holdings Ltd., you might recall, was a firm formerly run by New Jersey ex-Gov. Jon Corzine was accused in 2013 of unlawfully using customer money to meet his firm’s funding needs. When MF Global went bust because of trading by ex-Goldman Sach’s Jon Corzine’s trading using his client’s money in London also outside the regulatory eye of the USA, he was NEVER prosecuted for illegally using $1.6 billion of 26,000 client’s money. That is not going to be the case this time. So what is the difference between Corzine and Bankman-Fried? Corzine was ex-Goldman Sachs.

Indeed, Corzine was well-connected right into the White House with Obama. Nobody went to jail and clients had to wait in bankruptcy to get their money – even cash in the accounts was taken. There are clear risks with the broker and clearer. As long as the SEC is run with former Goldman Sachs staff, there will NEVER be an honest regulator. Even when all the banks pled criminally guilty, the SEC exempted everyone from losing their licenses. They would NEVER do that with anyone outside of New York City. The SEC will never prosecute the banks – EVER!!!!

Indeed, several federal investigations had been launched into MF Global, including probes by the Commodity Futures Trading Commission (its main regulator), the Securities and Exchange Commission, the Federal Bureau of Investigation, and Justice Department prosecutors in both Chicago and New York. The brokerage has also been the focus of several congressional hearings. Not a single one charged Corzine with trading with his client’s money. The losses that eventually drove MF Global into bankruptcy stemmed from high-risk bets on European sovereign bonds that Corzine made as he swung for the fences. Corzine bet big that the bond issuers would not default.

Commodity Futures Trading Commission simply fined Jon Corzine only $5 million over MF Global’s rapid descent into bankruptcy on Oct. 31, 2011, as an estimated $1.6 billion of customer money went missing. Anyone else would have been in prison for a minimum of 20 years.

It was Martin Glenn who was the judge in New York on M.F. Global bankruptcy. He was the first one to engage in FORCED LOANS by abandoning the rule of law to help the bankers by protecting them from losses taking client accounts to cover M.F. Global’s losses. He simply allowed the confiscation of client funds when in fact the rule of law should have been that the bankers were responsible and M.F. Global’s losses should have been reversed as they did even when Robert Maxwell’s companies failed in London from his illegal trading taking employee pension funds.

Yes, that was Ghislaine Maxwell’s father and the guy who was in control of the company that Bill Browder worked for before Edmond Safra. Never should the client’s funds be taken for M.F. Global’s losses to the NY Bankers. It was Judge Martin Glen who placed the entire financial; system at risk by trying to protect the bankers. Martin Glenn pampered these bankers making them the new UNTOUCHABLES. We have to be concerned that there really is no rule of law that will protect you in a crisis.

On Bloomberg TV, Sam Bankman-Fried explained why he even created FTX. He said he was experiencing his own frustration at Alameda Research, which was his crypto-focused proprietary trading firm. He was frustrated with the execution he was receiving at various crypto exchanges so he claimed that inspired FTX’s creation in May 2019. FTX grew rapidly to become the third largest crypto exchange in the world, with approximately $16 billion of customer assets under custody over 43 months.

Bankman-Fried stated that Alameda was making lots of money, but it could have been making more and he did not have access to venture capital. Claims of 100% annualized returns are not uncommon in a boom, but any experienced trader knows what goes up, also comes down. Alameda was relying on “cobbling together lines of credit” to expand its capital base. He then created FTX to solve his funding problem creating his own exchange that even the WEF cheered as a partner. He actually created a platform that was tailored for his own company, Alameda, to facilitate its trading needs. FTX coined the phrase “built by traders, for traders.”

There was an obvious conflict of interest questions regarding the close relationship between FTX and Alameda. Being operated from the Bahamas raised questions among those of us who are seasoned financial market observers whether the two were truly arm’s length from each other. However, people were so pumped up on adrenalin with crypto being the end of the dollar and central banks that this new free-wheeling crypto world believed what they wanted to believe and never looked too closely. FTX operated outside the reach of the US regulatory domain and there was a lack of any fiduciary confirmation. When the founder of Binance, the world’s largest crypto exchange, Changpeng Zhao, openly questioned the soundness of the FTX/Alameda nexus on Twitter saying he would sell over $500 million worth of FTX’s token FTT, that was the kiss of death weather or not he realized he would unleash a crypto panic that would engulf the entire industry in a matter of days.

The collapse of FTX will now become a contagion for the crypto world. This 20-something group of inexperienced traders has signaled the demise of an industry that was getting all the hype with no substance. This crypto world will be seen as the DOT COM Bubble of 2000. With a recession on the horizon, the collapse of sovereign debt, and the monetary system as a whole, people will be looking for more of the safe bets rather than roll the dice on crypto. Nothing ever goes straight down. But by year-end, the volatility should perk up everyone’s view of the world.

Posted originally on the conservative tree house on November 14, 2022 | Sundance

At a time when/if the economy was functioning as most economic pundits have previously proclaimed, Amazon and other retail giants would normally be beefing up workers in anticipation of the holiday shopping season. However, with the midterm election in the rearview mirror, exactly the opposite is happening. {Backstory on prior employment announcements}

According to multiple media reports, Amazon is expected to announce layoffs for approximately 10,000 U.S. workers this week. Yet another indication the economic pretending is coming to an end right after the midterm election is concluded.

(CNBC) – Amazon is planning to lay off approximately 10,000 employees in corporate and technology roles beginning this week, according to a report from The New York Times. Separately, The Wall Street Journal also cited a source saying the company plans to lay off thousands of employees.

Shares of Amazon closed down about 2% on Monday.

The cuts would be the largest in the company’s history and would primarily impact Amazon’s devices organization, retail division and human resources, according to the report. The reported layoffs would represent less than 1% of Amazon’s global workforce and 3% of its corporate employees. (read more)

“Bye”

As previously noted by Yahoo News, a “wave of layoffs” has begun that encompasses dozens of medium and large corporations [SEE HERE].

The layoffs, outlined in Yahoo, cover real estate, tech companies, banking, finance, automakers, EV startups, and brick and mortar stores like 7-11 and GAP. It should not come as a surprise, but it is sad to see, nonetheless.

Within the economy, a great pretending can only last so long… then reality hits.

The skilled trades should likely end up in the best employment situation, with the tech sector the worst. Service industries are also one of the first sectors hit when employment becomes an issue.

With rising interest rates, high inflation, excessive inventories, a shrinking production economy, extreme energy costs and diminished disposable income as a result of inflation and gas prices, there was going to come a time when it all starts to congregate.

2023 looks to be the year when economic pretenses collapse under the weight of having to admit a recession exists.

This is shaping up to be a painful holiday season….

Now that politicians have secured their positions in the elections prepare for the promises to fade. These people will say anything for our vote with no intention of following through. Biden has already announced that they will no longer accept student loan forgiveness applications. A Texas court barred future applications a day after the election – coincidence?

In fact, there is a website tracking Biden’s political promises, albeit not the most accurate. So far, he has kept only 22% of promises made during his campaign – at most. Many of these promises benefit absolutely no one, such as nominating the first black woman to the US Supreme Court, new fuel standards, increasing COVID testing, and rejoining the World Health Organization (WHO). That’s where his administration has placed their energy as if the entire world isn’t crumbling under their rule.

The website downplayed his broken promises after listing them at only 1%. He certainly broke his promise to “Build Back Better” – well… actually, he is following that plan accordingly. He has handed over America to the World Economic Forum on a silver platter. International objectives far outweigh domestic policies. The domestic policies in place and asinine spending packages have only made America less competitive and have hurt the pockets of not only the American people but the global economy.

Conservatives did not experience the red wave that they were hoping to see. Voting trends historically show the youth voting in favor of Democrats. As the quote often attributed to John Adams goes, “If You Are Not a Liberal at 25, You Have No Heart. If You Are Not a Conservative at 35, You Have No Brain.”

Pretending to champion one-voter issues with the backing of celebrities adds to this trend. A new NBC poll examined the exit polling data from voters between 18 and 29 (12% of the electorate) and 63% voted Democrat, while only 35% in this age range voted Republican.

People turn to the Republican Party as time goes on. Those 30 to 44 (21% of the electorate) voted 51% in favor of Democrats and 47% in favor of Republicans. The next age bracket, 45 to 64 (39% of the electorate), voted 44% in favor of Democrats and 54% in favor of Republicans. Those 65 and older (28% of the electorate) voted 43% Democrat and 55% Republican.

As we can see, support for conservative leadership grows with age and wisdom.

Posted originally on the conservative tree house on November 13, 2022 | Sundance

It’s just coincidental happenstance they say. Both George W Bush and Barack H Obama have scheduled conferences to highlight concerns over disinformation in the wake of the U.S. midterm election. Democracy is at stake if people do not blindly trust the constructs of the election systems that are now in place.

With a demand to accept the new normal….Former Presidents George W. Bush and Barack Obama are hosting back-to-back conferences about disinformation in the days following Donald Trump’s ‘big announcement.’

Bush, 76, will host his The Struggle for Freedom conference in Dallas on November 16, while Obama’s democracy conference will be held in New York City on the 17th.

Trump’s big announcement – largely rumored to be his 2024 presidential campaign announcement – is set for Tuesday.

Organizers said the conferences were not planned together, but will focus on the rising threats from authoritarianism and disinformation.

David J. Kramer, of the Bush Institute, said it was ‘terrific’ the two presidents would be focusing on similar topics, saying: ‘We’re very mindful of what’s happening in the United States, and we have to make sure we stay on a democratic path. (read more)

All just a coincidence…. nothing to see here, move along… move along.

Ignore any remembering that George Bush created the U.S. surveillance state (Patriot Act) and that Barack Obama weaponized it. However, also remember, the most dangerous time for a victim is that moment when the abuser realizes their battered victim has become numb to the continued psychological effort.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America