President Recep Tayyip Erdogan of Turkey is finding his dreams of an all-powerful resurrection of the Ottoman Empire are falling apart. Qatar has come to the aid of Turkey offering $15 billion in a loan, but keep in mind that the entire issue with Syria began with Qatar proposing a pipeline through Syria to compete with natural gas with Russia. Therefore, it is in Qatar’s best interest to keep Turkey trying to invade Syria. The price will be the pipeline, which we seriously doubt will ever take place.

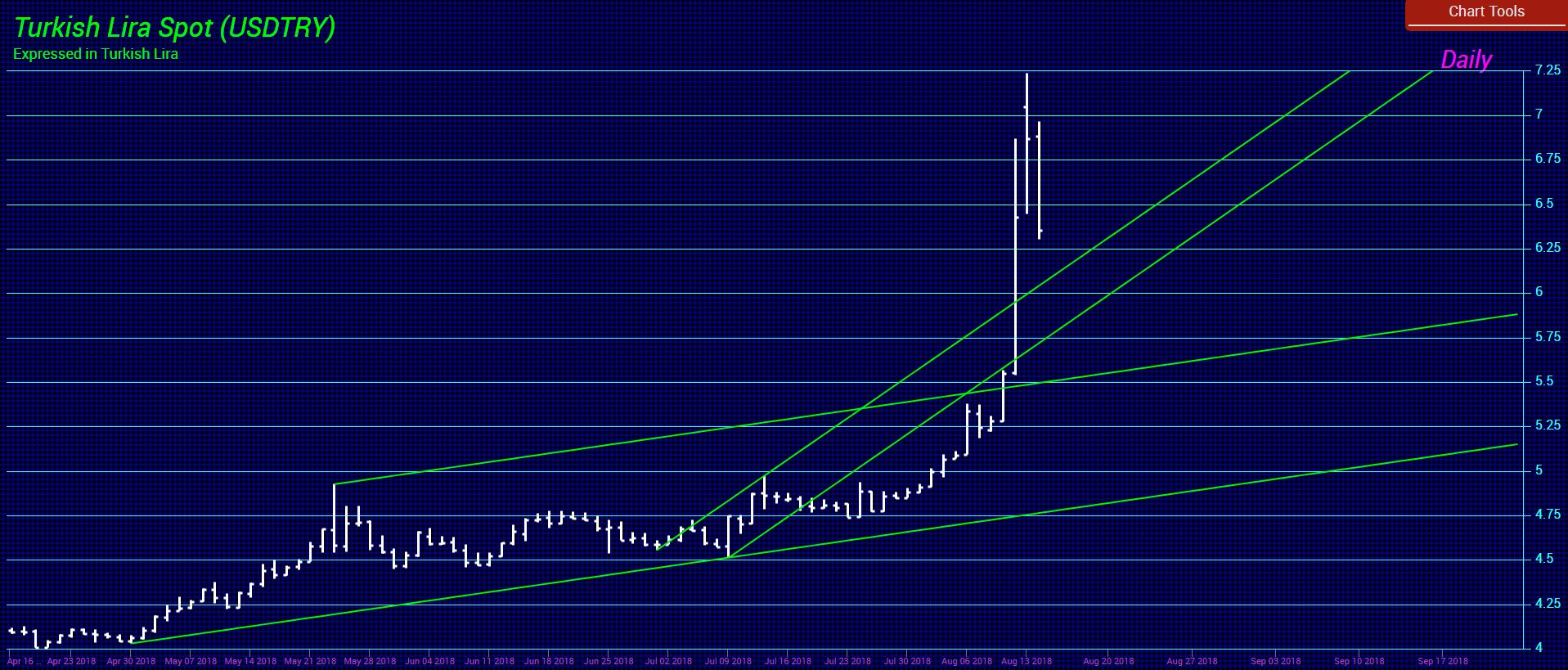

Erdogan has sent the Turkish economy into a downward spiral for some time. Its soaring inflation has exceeded 100% and rising debt-to-GDP of about 70% under President Recep Erdogan’s regime has been a growing problem. As central banks pumped money into the system over the past decade, nations like Turkey and other emerging market economies used the opportunity to raise more and more “cheap” debt to boost their productivity. Turkey has attracted capital from Europe seeking higher yields because of the negative interest rates policy of the ECB. Now we have a crisis in Turkey that is also the result of Draghi’s Quantitative Easing that drove capital to Turkey and FAILED to revived the European economy.

Erdogan’s dream of restoring the Ottoman Empire is no joke. It has been European money seeking higher yield that kept him in power. It is curious how those who seek dictatorial power are the ones who dream of restoring the power of empires long since dead. Erdogan has wanted to recreate the Ottoman Empire just as the dream of the reestablishment of the old Roman Empire as was the desire behind Napoleon and Hitler. The days of Empire Building are long gone and Erdogan has been living in the past. His goal was to expand his country’s military operations in Syria and this, he hoped, would be the first step as with Hitler’s invasion of Poland.

Nevertheless, the Turkish lira collapse and the expensive dollar have been conspiring against him reflecting his disastrous management of the economy and the collapse in confidence among the Turkish people. There remain serious questions about elections in Turkey being rigged to keep him in power. Therefore, on the one hand, Erdogan is attracted to dealing with Russia who is on the opposite side of the game board with Qatar. Erdogan has the free markets moving against him and he is more likely to turn to Russia than the West to retain personal power and the free markets show what most likely the real sentiment of the Turkish people was for the fake elections. Consequently, Erdogan turned to Qatar because he was desperate for money to retain personal power. If he loses the support of his military, then they will side with the people and Erdogan’s head may end up on a spike. Qatar will discover they are dealing with someone who will not be loyal to them either. Yet, the financial markets are working against Erdogan and as the crisis continues to evolve in the months ahead as $15 billion will not reverse the crisis, Turkey can hardly afford military adventures. Erdogan will be more likely to turn to Russia when he cannot retain power otherwise. He can blame the USA all he wants publicly, but the free markets are conspiring against him and that includes his own people.

Many European institutions rushed into Turkey and bought their bonds at 20%. Many Spanish banks had capital was invested in Turkish bonds to get the higher yield to the tune of on average 20%+. Based on the phone calls, there are way too many institutions who invested into Turkey. They simply assumed that NO government defaults because the powers that be will always bail out the bondholders. This time the IMF is really powerless. They can make some noise and others will say the crisis is subsiding. However, this is just talking. There is nobody who can save Turkey at this point as long as Erdogan remains in power. Qatar will discover that Turkey is a bottomless pit. They will try to now ease the crisis with words because of the extensive foolishness of banks and pension funds who bought Turkey bonds to try to get yield.

The fall in the Turkish lira has also benefited the Syrian Army, which launched an offensive on the last large mercenary fortress in Idlib. Turkey was actually against the offensive because it feared that it would fall to Syria and that is against Erdogan’s dreams of taking more territory. What is not really looked at internationally is the plain fact that Turkey does not have its own arms industry. Erdogan needs arms to be imported and as the lira crisis materialized, his Turkish operation Olive branch and shield of the Euphrates in Syria become rapidly too expensive. Back in January 2018, the Siyasi Haber newspaper reported that an estimated $400 million was being spent on Operation Olive Branch alone. Erdogan has spent over $1 billion so far in his attempt to conquer that region of Syria.

Instead of building his economy and benefiting the people of Turkey, Erdogan has been more interested in resurrecting the Ottoman Empire. It has been his mismanagement of the economy and his hostile attitude even to Greece that is behind the Turkish Lira Crisis. He has lost the confidence of his own people! August has been our target for the crisis and so far the computer has been correct on that score. However, volatility will remain high going into October and then we see it will return as the new year begins. Qatar coming to the rescue should help support the lira for now. Those who are wise had better sell their Turkish bonds and step oy of this trade. August should prove to be only a temporary low for the lira