Posted originally on the conservative tree house on November 21, 2022 | Sundance

The American Farm Bureau price estimation for the Thanksgiving Day basic foodstuffs seems underestimated every year. However, this year with grocery store prices jumping dramatically the basic Thanksgiving Dinner as calculated is up 20% [Data Here]

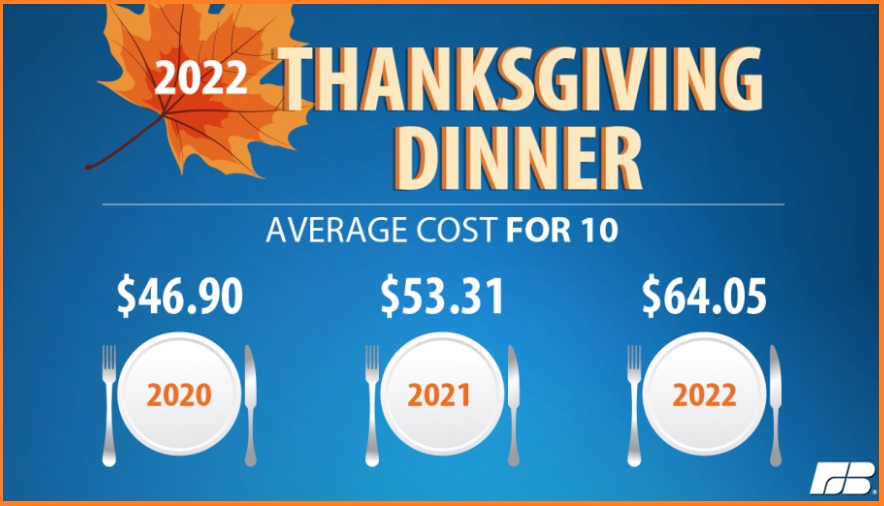

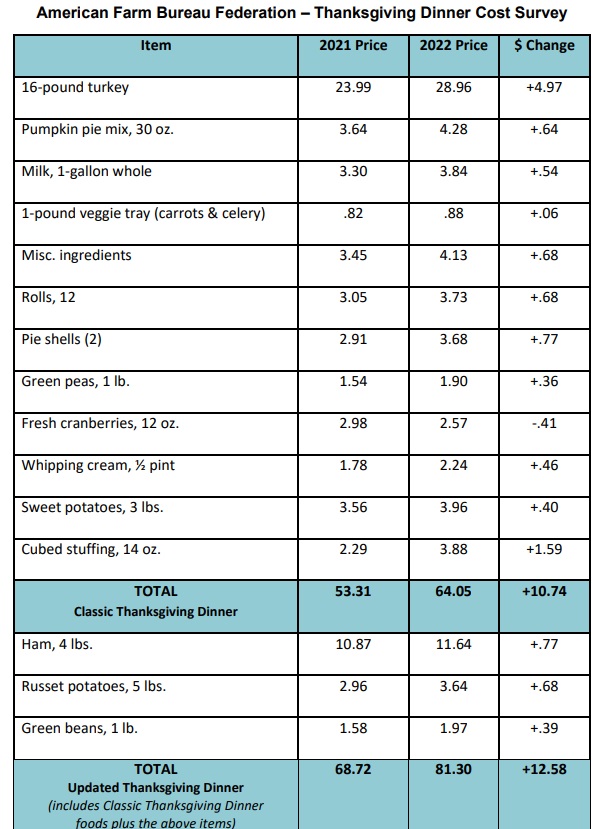

(AFB) – Spending time with family and friends at Thanksgiving remains important for many Americans and this year the cost of the meal is also top of mind. Farm Bureau’s 37th annual survey provides a snapshot of the average cost of this year’s classic Thanksgiving feast for 10, which is $64.05 or less than $6.50 per person. This is a $10.74 or 20% increase from last year’s average of $53.31.

The centerpiece on most Thanksgiving tables – the turkey – costs more than last year, at $28.96 for a 16-pound bird. That’s $1.81 per pound, up 21% from last year, due to several factors beyond general inflation. (read more)

On the positive side of things, we note two points: #1) the third wave of food inflation should crest the beginning of December; and #2) a lot of readers here were proactive and purchased holiday ingredients long before the massive price increases showed up. Great job.

.

Although, as WeeWeed has noticed, this year is making everyone a little spicy…

QUESTION: Marty, It was a fantastic WEC. You tied it all together brilliantly and how the real issue is this liquidity crisis. Suddenly the ECB came out and said that inflation will not subside given a recession. It appears they were watching the WEC. Do you think that the ECB is at least listening now?

NG

ANSWER: For Christine Lagarde to publicly state that a “mild recession” will not reduce inflation is admitting that inflation has been instigated by COVID lockdowns that disrupted the supply chain and unleashed shortages. The Bank of England has come out and stated that we will see the longest recession in 100 years.

The ECB has just forced banks to repay their loans withdrawing $300 billion euros from the banking system in a desperate effort to stop inflation. This will not help for Legarde knows that even an economic recession will not prevent this type of inflation that is more akin to the STAGFLATION of the ’70s where costs rose thanks to the OPEC crisis and where we have the COVID Crisis that created shortages mixed with the climate change zealots determined to end fossil fuels despite the fact there are no alternatives. How do you even make steel without coal?

Everything is now unfolding on schedule. We are facing 2023 which will be known as the year of chaos.

Retail relies on the holiday season for the bulk of its revenue. In fact, a quarter of all retail spending in the US occurs in the last two months of the year. Numerous retailers have already downgraded their forecasts for the holiday season, and therefore, overall revenue estimates will go down. I reported that early indications of Halloween spending amid inflation were cause for concern. People were still willing to spend on the holiday, but everything cost significantly more, and availability was limited.

Two weeks ago, reports were coming in of hiring halts, but now mass layoffs are suddenly appearing in the news. Amazon plans to fire 10,000 employees this week alone. This is a steep mass layoff that represents 3% of corporate employees and 1% of the entire workforce. This is the largest layoff in the company’s history.

Other retailers have announced layoffs as well, and this is not limited to the US. E-commerce giant Alibaba also laid off nearly 10,000 workers this past August due to poor numbers. AliExpress eliminated 40% of its entire workforce and cited supply chain disruptions as the main culprit, as it was one of the most popular shopping apps in Russia.

Gap Inc. will eliminate 500 corporate roles in the US and Asia. Peloton parted ways with 500 people in October in its most recent round of layoffs. Shopify eliminated 10% of its staff in July and plans to make additional cuts. Nordstrom fired 200 employees from a warehouse distribution center. Wayfair eliminated 900 positions after a hiring freeze in May. Mass layoffs are becoming a common occurrence during a time when retailers usually hire additional staff.

The supply chain crisis is to blame. FedEx plans to furlough employees right before the busy Christmas season. Their revenue was up 21% last quarter, but shipments fell 5% in the same time period. Overall inflation and wage losses are a positive sign for the Fed but a complete disaster to individuals and their families. Expect sales as retailers attempt to eliminate outdated inventory to make room for delayed shipments.

Posted originally on the conservative tree house on November 15, 2022 | Sundance

The White House is urging Nancy Pelosi to utilize the lame duck congressional session and construct a massive omnibus spending bill that will wrap Ukraine funding, COVID spending and a federal budget extension via continuous resolution. The request for Ukraine funding is an additional $38 billion.

Federal funds to support FEMA and hurricane recovery efforts will likely be part of the bargaining chips. Essentially, the sausage ingredients are: if congress doesn’t give Zelenskyy more money, then DeSantis will not get federal financial assistance.

If you don’t support Ukraine, you’re a Russian operative.

WASHINGTON DC – The Biden administration sent a letter to Congress on Tuesday outlining nearly a $38 billion request to help Ukraine continue fending off Russian attacks.

The administration is also asking for $10 billion in emergency health funding, with more than $9 billion going toward Covid vaccine access, next-generation Covid vaccines, long Covid research and more. About $750 million would be spent on efforts to control the spread of monkeypox, hepatitis C and HIV.

Congress has so far provided about $66 billion for Ukraine and other war-related needs. The administration argues that about three-quarters of that funding has either been spent or is committed to specific purposes.

An administration official said the White House plans to request additional disaster relief in the coming weeks to help with hurricane and wildfire recovery but didn’t provide any tentative figure.

The administration’s request for emergency money comes as appropriators aim to clinch a year-end government funding deal that would stave off a partial government shutdown on Dec. 16 and increase agency budgets for the current fiscal year. House Speaker Nancy Pelosi has already promised to provide more money for Ukraine in a government funding package, while some conservatives are arguing that the U.S. should cut off financial assistance and assess how funding for the country has been spent to date. (read more)

The collapse of the FTX Exchange is pretty straightforward insofar as this is the same lesson that constantly repeats in finance time and time again. Basically, FTX lent US$10bn of client funds to their trading arm Alameda, which used it for leveraged their own crypto speculation because the crypto market has been collapsing. Typically, someone like Sam Bankman-Fried had his whole life wrapped up in this venture. Lacking financial controls operating from the Bahamas, moving the money from client funds to his trading arm Alameda was possible. Historically, someone in this position sees his world collapsing but is not prepared to see that unfold for it requires admitting that he was wrong on crypto, to begin with. Consequently, such a person is not trying to actually rob clients’ money, they most likely see it as a temporary loan to save the company and the market will bounce back – or so they believe.

Our computer had picked the high in Bitcoin perfectly and has been projecting the collapse all along the way. But crypto has become a religion and in so doing it clouds the judgment of people who want to believe the story. Alameda blew up in a crypto meltdown because it did not want to accept that the crypto boom was over. The loan he probably thought would be temporary, vanished in the implosion. At first, I would have assumed they had actually invested the money and lost it on the bond market collapse. But that was perhaps too traditional. Here, it appears they were trying to defend their own cryptocurrency and trying to buy the low that kept moving lower. It appears he was allegedly simply using clients’ funds to trade keeping gains for his firm and the clients now suffer the risk.

It appears that they allegedly were trying to defend the crypto market and did not understand that the boom was over. The loans could not then be repaid. As crypto was crashing, some people needed to cash out. The attempt to pull out US$5bn from FTX exposed the fact that the cash was all gone. This is not so unusual. It has happened before. This time, the prosecutors are clamoring to be the one to charge him so they can become famous over his dead body.

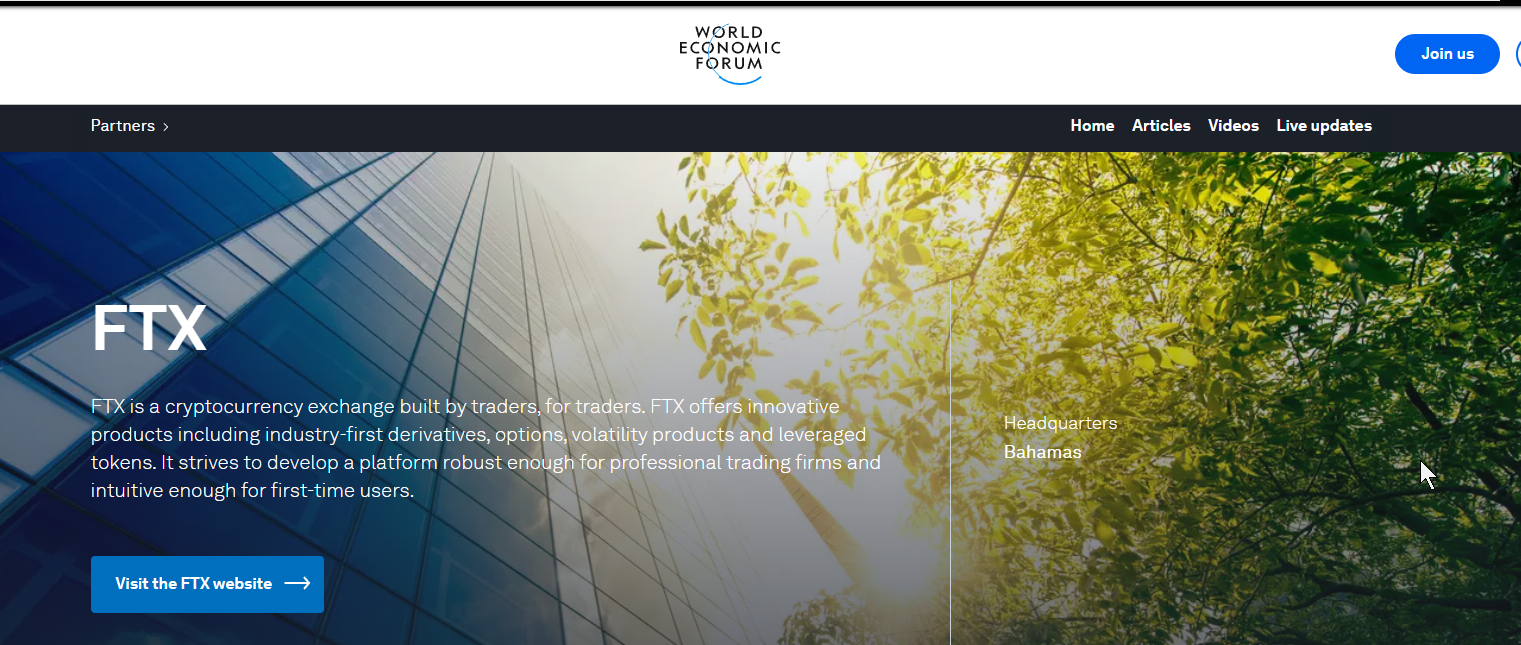

FTX was a partner with Klaus Schwab’s World Economic Forum (WEF). Of course, the WEF has suddenly removed the page and is desperately trying to hide their involvement with FTX and Sam Bankman-Fried. Naturally, eliminating paper currency has been the goal of the WEF because they support the end of not just capitalism, but also democracy. Schwab’s push has been his Great Reset and to control society to impose his economic philosophy inspired by Marx and Lenin.

This is by no means the first violation of fiduciary responsibility that presents a custodial risk. MF Global Holdings Ltd., you might recall, was a firm formerly run by New Jersey ex-Gov. Jon Corzine was accused in 2013 of unlawfully using customer money to meet his firm’s funding needs. When MF Global went bust because of trading by ex-Goldman Sach’s Jon Corzine’s trading using his client’s money in London also outside the regulatory eye of the USA, he was NEVER prosecuted for illegally using $1.6 billion of 26,000 client’s money. That is not going to be the case this time. So what is the difference between Corzine and Bankman-Fried? Corzine was ex-Goldman Sachs.

Indeed, Corzine was well-connected right into the White House with Obama. Nobody went to jail and clients had to wait in bankruptcy to get their money – even cash in the accounts was taken. There are clear risks with the broker and clearer. As long as the SEC is run with former Goldman Sachs staff, there will NEVER be an honest regulator. Even when all the banks pled criminally guilty, the SEC exempted everyone from losing their licenses. They would NEVER do that with anyone outside of New York City. The SEC will never prosecute the banks – EVER!!!!

Indeed, several federal investigations had been launched into MF Global, including probes by the Commodity Futures Trading Commission (its main regulator), the Securities and Exchange Commission, the Federal Bureau of Investigation, and Justice Department prosecutors in both Chicago and New York. The brokerage has also been the focus of several congressional hearings. Not a single one charged Corzine with trading with his client’s money. The losses that eventually drove MF Global into bankruptcy stemmed from high-risk bets on European sovereign bonds that Corzine made as he swung for the fences. Corzine bet big that the bond issuers would not default.

Commodity Futures Trading Commission simply fined Jon Corzine only $5 million over MF Global’s rapid descent into bankruptcy on Oct. 31, 2011, as an estimated $1.6 billion of customer money went missing. Anyone else would have been in prison for a minimum of 20 years.

It was Martin Glenn who was the judge in New York on M.F. Global bankruptcy. He was the first one to engage in FORCED LOANS by abandoning the rule of law to help the bankers by protecting them from losses taking client accounts to cover M.F. Global’s losses. He simply allowed the confiscation of client funds when in fact the rule of law should have been that the bankers were responsible and M.F. Global’s losses should have been reversed as they did even when Robert Maxwell’s companies failed in London from his illegal trading taking employee pension funds.

Yes, that was Ghislaine Maxwell’s father and the guy who was in control of the company that Bill Browder worked for before Edmond Safra. Never should the client’s funds be taken for M.F. Global’s losses to the NY Bankers. It was Judge Martin Glen who placed the entire financial; system at risk by trying to protect the bankers. Martin Glenn pampered these bankers making them the new UNTOUCHABLES. We have to be concerned that there really is no rule of law that will protect you in a crisis.

On Bloomberg TV, Sam Bankman-Fried explained why he even created FTX. He said he was experiencing his own frustration at Alameda Research, which was his crypto-focused proprietary trading firm. He was frustrated with the execution he was receiving at various crypto exchanges so he claimed that inspired FTX’s creation in May 2019. FTX grew rapidly to become the third largest crypto exchange in the world, with approximately $16 billion of customer assets under custody over 43 months.

Bankman-Fried stated that Alameda was making lots of money, but it could have been making more and he did not have access to venture capital. Claims of 100% annualized returns are not uncommon in a boom, but any experienced trader knows what goes up, also comes down. Alameda was relying on “cobbling together lines of credit” to expand its capital base. He then created FTX to solve his funding problem creating his own exchange that even the WEF cheered as a partner. He actually created a platform that was tailored for his own company, Alameda, to facilitate its trading needs. FTX coined the phrase “built by traders, for traders.”

There was an obvious conflict of interest questions regarding the close relationship between FTX and Alameda. Being operated from the Bahamas raised questions among those of us who are seasoned financial market observers whether the two were truly arm’s length from each other. However, people were so pumped up on adrenalin with crypto being the end of the dollar and central banks that this new free-wheeling crypto world believed what they wanted to believe and never looked too closely. FTX operated outside the reach of the US regulatory domain and there was a lack of any fiduciary confirmation. When the founder of Binance, the world’s largest crypto exchange, Changpeng Zhao, openly questioned the soundness of the FTX/Alameda nexus on Twitter saying he would sell over $500 million worth of FTX’s token FTT, that was the kiss of death weather or not he realized he would unleash a crypto panic that would engulf the entire industry in a matter of days.

The collapse of FTX will now become a contagion for the crypto world. This 20-something group of inexperienced traders has signaled the demise of an industry that was getting all the hype with no substance. This crypto world will be seen as the DOT COM Bubble of 2000. With a recession on the horizon, the collapse of sovereign debt, and the monetary system as a whole, people will be looking for more of the safe bets rather than roll the dice on crypto. Nothing ever goes straight down. But by year-end, the volatility should perk up everyone’s view of the world.

It should be clear by this time that popularity has nothing to do with electability. Trump filled rally after rally in state after state with countless, full-house, full-stadium crowds, and such numbers do not lie. There really was a red wave in the midterms, but it was macro-engineered to a trickle, as should have been expected. The scam of “malfunctioning” voting machines, the shortage of paper ballots, the tsunami of mail-in and late ballots, the temporary closing and slow-downs of polling stations, and so on would have been sufficient to determine an electoral result. 2020 was an early run for 2022, which in turn should be regarded as a template for 2024. I am absolutely sure that the Dems are now, even as we speak, preparing favorable ground for the next presidential election. As Stalin is reputed to have said, “It’s not the people who vote that count, it’s the people who count the votes.” To make Trump responsible for Democrat malfeasance is wholly misguided.

DeSantis is now the favorite among many Republican voters and almost all conservative commentators for the Party presidential nomination. Such passionate advocates seem to have missed two essential points:

In a rigged electoral system, no Republican candidate, not even DeSantis, can be expected to win a national election. DeSantis cruised to victory in Florida because, as governor of the state, he had the means and the authority to ensure a clean election. But he would be helpless against a massive crime organization, aka the Democrat Party, which effectively controls the electoral infrastructure, the physical apparatus, the paid loyalty of election workers, and the federal agencies that oversee the process. If the system is not repaired and made answerable to the people, there will never be a Republican president again.

Should DeSantis run in 2024 and lose — which is increasingly likely in the current adulterated circumstances — the sequel would be devastating. Florida would be at the mercy of the next gubernatorial race since DeSantis is a unique political figure and could not be readily replaced. Additionally, DeSantis himself would have become a kind of displaced person, neither an American president nor a state governor. An invaluable political talent would have been sacrificed to the untutored enthusiasm of his supporters. If the American republican experiment is now in dire straits, it would then be expeditiously destroyed. A slim hope will have become an utter disaster.

Trump has obviously made his mistakes. As Alicia Colon writes on American Thinker, “There is no question that Donald Trump is a flawed human being like most successful businessmen.” She goes on: “Whenever I read the complaints from Trump haters, it’s all about his personality, his tweets, his misogynism, his sexist remarks, blah, blah, blah. This is infantile, high school criticism that has no place in political punditry.” Similarly, as J.B. Shurk writes, everything that the establishment class “has fraudulently peddled against Trump—that he’s imperious, mercurial, uncouth, unworthy to hold office, a Russian spy, a warmonger, an insurrectionist, a ‘denier,’ a criminal—is nothing but an endless barrage of psychological warfare directed against MAGA voters.”

Trump’s flaws of character — and who is without them — do not alter the fact that Trump is an indomitable fighter and the most successful president in recent history. His ego is concomitant with his strength; the two cannot be separated. To turn against him now and indulge in gutter journalism, righteous schadenfreude, or in considerations of realpolitik largely because a number of his chosen endorsements succumbed to a corrupt and rigged electoral machine is a sign of conservative defeatism and, in some cases, of self-enamored mobbing. We were quite happy with his major and unprecedented policy successes: making America energy-independent, restoring the manufacturing base, revisiting trade deals to benefit American workers, creating a surge in employment and prosperity, laboring to put a stop to illegal immigration, appointing conservative judges, rebuilding a depleted military, and establishing renewed American pre-eminence on the international stage. Now we are ready to consign him to the golf course. How quickly gratitude turns to recrimination.

Rather, this would be the time to rally the troops and to work indefatigably, as I argued previously, toward cleaning up the Augean Stables that are now the condition of American politics. Trump is still “the Donald.” Republicans need to get their act together instead of unintentionally justifying the betrayal of the RINO Machiavellian elites and foolishly consolidating the Democrat campaign against the very nation they presumably hold dear.

Posted originally on the conservative tree house on November 12, 2022 | sundance

For his weekly monologue Neil Oliver outlines the reality of the British government no longer pretending to represent the people of the United Kingdom, but openly represents corporations and the interests of multinationals.

While the general topic of a disconnected governing body is referenced toward how the U.K. government is disregarding the opinion of the British citizens, the overarching theme outlined by Oliver also applies to the United States. WATCH:

(Transcript) – Does Britain still exist? Or is it being dismantled to make way for something else?

Obviously, there are some square miles of dry land off the coast of mainland Europe still going by the name of Britain. Britain is still on the map.

As a for instance, if you pay a people smuggler some thousands of bucks and say, take me to Britain, he will know where you mean and will transport you to a rendezvous with a British border force vessel or an RNLI lifeboat financed by donations from the British public, and either will cheerfully ferry you to the British coast where you will be collected and taken to a fine hotel and given food, money and access to all the facilities a person might need all of it paid for by taxes from those same British people millions of British people who are themselves painfully short of money and struggling to feed themselves and heat their homes.

Those taxes are predicted to rise, so that more of our money might be flushed out of Britain, away from the British, towards those deemed more deserving.

… but does that name, Britain, still define a sovereign country in any meaningful sense?

The crisis on the south coast is only part of a bigger problem. These islands of ours offer free accommodation, three meals a day and cash – no questions asked – plus more chance of bagging a council house than anyone actually born here. Who wouldn’t jump at the chance? But the setting aside of the border to make way for thousands of new arrivals every day is only a symptom of a homegrown sickness.

Ironically, in the aftermath of all the damage done to the personal immune systems of millions, billions of people worldwide, by the policies and medical practices of the past two years, Britain herself has been similarly weakened, deep down:

Instead of keeping the country safe and well those entities supposed to function like the nation’s immune system parliament, the institutions of state the civil service, the judiciary, the police have turned on the British people instead, and upon the structures that ought to protect us from harm. Like someone suffering from auto-immune disease, our national immune system is now destroying the healthy cells which is to say us, the British people.

Any country is a fiction when you get right down to it. For continued existence, every country depends on enough of the people who happen to occupy that space sharing the same idea about where they live. If enough people believe in the existence of Britain – and are prepared to give their all to maintain Britain – then Britain prevails. If the day comes when too many have forgotten what Britain is, or simply don’t care if she exists or not, then Britain is no more. The dry land will still be there, the roads and buildings, but that is all.

This is the time of remembrance, when we claim … claim to honour the ancestors who gave the last full measure of devotion to protect this country and see it handed on intact to future generations: “When you go home, tell them of us and say … For your tomorrow, we gave our today.”

Those words are graven in stone all over this country.

Today’s leaders have no loyalty to Britain or the British – none that I can see. Maybe a few still FEEL some loyalty – but are just too demoralised or scared to declare it, far less to do anything about it.

Whatever loyalties the rest of them have, on both sides of the aisle … they lie elsewhere, not honestly declared.

For one thing, they are loyal to those entities that DO make all the meaningful decisions, which is to say the markets and the banks. It was the markets that wanted rid of Liz Truss and Kwasi Kwarteng and so they went.

Now we have Rishi Sunak – the prime minister none of us voted for and therefore don’t want. Like Jeremy Hunt – blatantly the markets’ choice of chancellor – his loyalties lie anywhere but with Britain and the British. Imagine how both men drool at the prospect of a CBDC and the surveillance society it will force upon us.

If we are led by figures committed to objectives that are against our interests – are we even obliged to obey their diktats when they are undoing everything Britain has been?

Are the needs and wants of the British people to be set aside in favour of the needs and wants of everyone else, anyone else in the world?

I ask those questions sincerely.

Since we’re talking about the markets and the banks, we might as well focus on what it’s all about, all of this upset and upheaval, which is control … control of the people via control of our money.

At a time when British people are struggling in ways that have been unknown to millions for a very long time, a vast mountain of the money they pay in tax is being shoveled elsewhere. For the crime of having been born in the home of the industrial revolution that changed the world for the better and lifted billions of people out of poverty, this latest generation of British people is to be punished, diminished, made dependent upon a State that openly despises us and treats us with contempt.

Setting aside, for example, the fact that China has pumped out more pollution in the last 8 years than Britain managed in the 220 years since the Industrial Revolution began … more of the taxes paid by British people might be handed to the Developing World … perhaps China included, who knows … as our penance for making it possible for 8 billion people to be alive in the world at the same time … courtesy of cheap, efficient energy, plentiful food and all the benefits born of the modern medicine and technology OUR ancestors’ efforts made possible.

The fire kindled here more than 200 years ago made life better, made life possible, for billions. And in return we are to be mugged in broad daylight, our wallets emptied, and our hard-earned cash handed to anyone around the world that wants it.

A good whack of China’s recent output of CO2 came from burning coal to make our wind turbines and the rest of the vanity projects that let our remotely-controlled leaders spout lies about cutting emissions, but hey-ho … never let the facts get in the way of a good global scam.

Back to the point, British money … earned by hard-working, struggling British people … is being funnelled out of Britain and into the wider world as fast as the leaders can make it flow. Cynic that I am, I conclude that all possible efforts are being made to impoverish and so destroy once and for all that upstart aspirational middling class whose very existence so infuriates today’s rulers.

Natural law is summarised in three words: do not steal. It underpins all lawful behaviour. Do not steal the life of another … do not steal the private property of another … do not steal the product of a worker’s labour, which is to say taxation … do not steal a person’s rights. Do not steal. It’s simple. But that simple foundation of lawful society has been set aside for the benefit and enrichment of the few.

Every day and more and more, those calling themselves our leaders are stealing everything. They look us in the eye and steal from us. During lockdown they stole our rights and liberties … they stole the livelihoods of millions … they stole mental and physical wellbeing. They stole the way things used to be. They are stealing the futures we had planned for our children.

There is a line of Latin that goes:

Quis custodiet ipsos custodes?

It means, who will guard the guards themselves? Those words focus our attention on the situation that arises when people with the power to supervise others are not, themselves, subject to the same scrutiny. It applies also when those who entitle themselves to make the law, also empower themselves to enforce the punishments. That is the definition of tyranny that our constitution was shaped to prevent.

At a time when British people are struggling in ways that have been unknown to millions for a very long time, a vast mountain of the money they pay in tax is being shovelled elsewhere, says Neil Oliver GB News

There’s a Covid enquiry out there. The same people that caused all the harm are now deciding if they did the right thing or not. I think we all know what conclusions they will draw. I ask again, Who will guard the guards themselves?

The UK Border Force – in place to protect and maintain the border – might as well be working in partnership with the people smugglers. The same company involved in border control has the government contract for housing asylum seekers. This is a conflict of interest alongside an inversion of their role.

The police – a citizen police force supposed to protect the British public does next to nothing to keep law-abiding citizens safe from real, violent crime and instead monitors what people say on social media. When they’re not being thought police, they either dance the Macarena with protesters the State likes or take the baton to those it doesn’t.

SO, WHAT SHOULD WE DO NOW?

Philosopher Thomas Hobbes wrote about how, without observance of right and wrong, human life was, “solitary, poor, nasty, brutish and short”. He concluded that such chaos was ended only if individuals agreed, via a social contract, to surrender some liberty to a sovereign on condition that that sovereign would keep them safe.

Who is honouring their part of our social contract now? We, the people, have been doing so … not least because, legally, we have no option.

It is interesting to recall the words of the American declaration of independence:

“Life, Liberty and the pursuit of Happiness … that to secure these rights, governments are instituted among Men, deriving their just powers from the consent of the governed … that whenever any Form of Government becomes destructive of these ends, it is the Right of the People to alter or to abolish it, and to institute new Government, laying its foundation on such principles and organizing its powers in such form, as to them shall seem most likely to affect their Safety and Happiness.”

I say that by their actions over the last many years, our leaders have made the social contract null and void. They are not protecting our freedoms and rights – nor Britain herself.

On the contrary, they are working in league with others to remove those rights and freedoms and to unmake Britain. If they will not honour the social contract, then why should we?

While we were distracted our governments assumed outrageous powers over us. Body and mind we are being crushed and numbed.

The time for accepting all of this has long passed.

Here’s the thing: where should OUR loyalties lie now?

With those who by their actions have made plain they respect us not a jot?

… or with each other, those who have seen through the lies and the transparent grasping for power and control. On this Remembrance weekend I would honour those who gave their lives for a free world and a country called Great Britain.

People are simply not prepared for a sharp economic downturn. The Money and Pensions Serviceconducted a poll in the UK in which it found around 25% of adults have under £100 in savings. The 3,000-person survey found that 17% reported having absolutely nothing set aside. Around 5% reportedly had under £50, while 4% had between £50 and £100.

The drastically increased cost of living has many living paycheck to paycheck. The Building Societies Association (BSA), as reported by the BBC, conducted a separate survey that found that 35% of people in the UK simply stopped saving due to inflation. Around 36% said they are already dipping into their savings accounts to pay the bills.

The Bank of England is anticipating a long recession ahead. The central bank sees economic conditions contracting through the first half of 2024. The central bank’s prediction of five consecutive quarters of contraction would mark the longest recession in UK history. The people have not experienced the full effects of this recession, and most are simply not prepared for what lies ahead.

The Nationwide Retirement Institute conducted a study to determine how Americans are handling rising prices. Nearly one in five respondents (18%) said they had to forego a meal or grocery shopping due to inflation. Gen Z (28%) and Millennials (23%) reported higher rates of skipping meals. Over the past year, two in five households (40%) relied on food banks.

This is having an impact on health. Around 17% said that they no longer can afford healthier food options, which are notoriously more expensive than cheap, calorie-rich junk food. Fourteen percent admitted that they canceled or postponed plans to see a doctor, and 11% skipped out on their annual physical altogether due to the costs involved. An alarming 10% said that they are unable to afford their prescription medication. The younger generations like Gen Z (17%) and Millennials (19%) said that they cannot afford mental health care.

Staying healthy has become a luxury, as 14% of respondents had to downgrade their health insurance plans. Again, Gen Z (23%) and Millennials (20%) have been forced to sacrifice more than other generations. These two generations are also priced out of the housing market and strapped with debt. They are less likely to start families and are worse off than their parent’s generation. This will create a ripple effect as people who are unable to meet their basic needs will struggle to be productive members of society.

Posted originally on the conservative tree house on October 27, 2022 | sundance

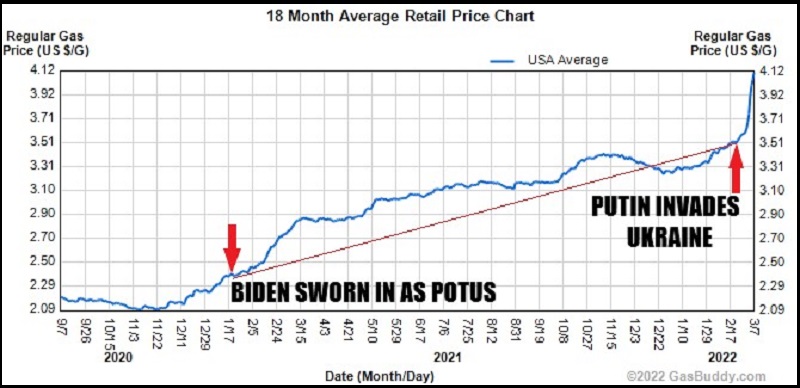

Will big tech and social media remove Joe Biden for violations of misinformation, disinformation and malinformation? Considering his remarks today, they should.

Reading from a teleprompter loaded with lies about the economy, Joe Biden stunningly states that gas prices are lower today than when he took office. Further claiming that gasoline was $5/gal. {Direct Rumble Link} Nothing about any of his economic claims is true. WATCH (1 min):

.

Allowing people to return to work after the pandemic lockdowns is not “creating jobs.” And gasoline was not $5/gal when Joe Biden took office.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America