William Alfred “Bill” Whittle (born April 7, 1959) is an American conservative blogger, political commentator, director, screenwriter, editor, pilot, and author.

Tag Archives: BREXIT

Bill Whittle: 5 STEPS to Take the Country Back from the Left

William Alfred “Bill” Whittle (born April 7, 1959) is an American conservative blogger, political commentator, director, screenwriter, editor, pilot, and author.

Bill Whittle: How the Critical Theory Ruined a Generation

William Alfred “Bill” Whittle (born April 7, 1959) is an American conservative blogger, political commentator, director, screenwriter, editor, pilot, and author.

Pension Crisis

Armstrong Economics Blog/Uncategorized

Re-Posted Oct 12, 2014 by Martin Armstrong

After 2015.75, we will begin to observe the Pension Crisis manifest before our eyes. There are few governmental exceptions within Western Society without this serious trouble. While they keep everyone occupied between soccer and football, governments have done an incredible job of committing massive fraud upon the public. Public unions are simply demanding that governments raise taxes and extort money from other sectors to hand to them.

After 2015.75, we will begin to observe the Pension Crisis manifest before our eyes. There are few governmental exceptions within Western Society without this serious trouble. While they keep everyone occupied between soccer and football, governments have done an incredible job of committing massive fraud upon the public. Public unions are simply demanding that governments raise taxes and extort money from other sectors to hand to them.

Government pension funds are a joke. Even in Britain, pensions will run out of cash next year: Amount handed out to future generations will be disastrous. Those under 35 should not expect anything for their taxes. (see also the Mail). This will be part of the ever increasing civil unrest that we see coming after 2015.75 moving into January 2020.

European Banking Crisis

Armstrong Economics Blog/Banking Crisis

Re-Posted Nov 13, 2017 by Martin Armstrong

There is intense resistance building against the stricter new rules on bad loans among the European banks. This will hit Italy hard and may push off the edge more than one Italian bank. With the elections coming next year in Italy, the banking rules may be the straw that breaks the back.

There is intense resistance building against the stricter new rules on bad loans among the European banks. This will hit Italy hard and may push off the edge more than one Italian bank. With the elections coming next year in Italy, the banking rules may be the straw that breaks the back.

The background to the dispute is the demand of the ECB’s banking supervisor that banks must withhold higher reserves for the default-prone loans in their portfolios. The crisis stems from the fact that as taxes have increased, the economy has declined. The total bad loans in the Eurozone add up to about €844 billion euros. About 25% of this figure is concentrated in Italian banks.

A good stiff wind may blow over the European banking system

Draghi Knew About Hiding Losses by Italian Banks

Armstrong Economics Blog/Banking Crisis

Re-Posted Nov 13, 2017 by Martin Armstrong

The Bank of Italy, when it was headed at the time by Mario Draghi, knew Banca Monte dei Paschi di Siena SpA hid the loss of almost half a billion dollars using derivatives two years before prosecutors were alerted to the complex transactions, according to documents revealed in a Milan court.

Mario Draghi, now president of the European Central Bank, was fully aware of how derivatives were being used to hide losses. Goldman Sachs did that for Greece, which blew up in 2010. It is now showing that Draghi was aware of the problems stemming from a 2008 trade entered into with Deutsche Bank AG which was the mirror image of an earlier deal Monte Paschi had with the same bank. The Italian bank was losing about €370 million euros on the earlier transaction, internally they called “Santorini” named after the island that blew up in a volcano. The new trade posted a gain of roughly the same amount and allowed losses to be spread out over a longer period. We use to call these tax straddles.

Mario Draghi, now president of the European Central Bank, was fully aware of how derivatives were being used to hide losses. Goldman Sachs did that for Greece, which blew up in 2010. It is now showing that Draghi was aware of the problems stemming from a 2008 trade entered into with Deutsche Bank AG which was the mirror image of an earlier deal Monte Paschi had with the same bank. The Italian bank was losing about €370 million euros on the earlier transaction, internally they called “Santorini” named after the island that blew up in a volcano. The new trade posted a gain of roughly the same amount and allowed losses to be spread out over a longer period. We use to call these tax straddles.

The report was dated September 17th, 2010, and marked “private” demonstrating that the Bank of Italy was aware that by choosing not to book the trade at fair value Monte Paschi avoided showing a loss at the time. If the bank had used a mark-to-market valuation in the fourth quarter of 2008, it would have been included in its year-end report as the credit crisis was cresting.

This is the real picture behind the curtain. Draghi has known all about using derivatives to mask-over losses and pretend they are not there. The entire Greece Crisis was caused by Goldman Sachs constructing derivatives to pretend Greece made the criteria for the Eurozone.

Greece joined the Euro in 2001 under Costas Simitis. At the time, Greece owed about €3.4 billion euros it had borrowed. Goldman engineered a currency swap whereby the Greek debt, issued in dollars and yen, was exchanged for euros that were priced at a “historical” or entirely fictitious currency rate. Of course, swapping dollar and yen debt at nearly the low of 2000 when the euro was only 82 cents to the dollar became a nightmare. Greece’s debt doubled in real terms as the euro then rose to $1.60 by 2008. Obviously, Goldman offered no advice but structured a deal that only benefited itself by directing Greece to sell the dollar at the low. Goldman also set up an off-market interest-rate swap to repay the loan off the books, which was a currency position and therefore not technically a “loan” outside any reporting requirement as debt. The trade kept this part of the Greek debt off the books and cleverly hidden from scrutiny. This falsely created the idea that the Greek debt was moving in the right direction to meet the Maastricht rules eventually. Goldman overpriced the deal to such an extent that 12% of their $6.35 billion in trading and investment revenue for 2001 came from restructuring Greece. In total, they pocketed a premium fee of $300 million. Goldman also warned, as they typically do, Goldman would cancel the offer that if Greece shopped the deal around for a better price. Goldman further demanded that Greece pledge landing fees from Greek airports and revenue from the national lottery as part of the transaction to secure their own profits strip-mining Greece.

Within just three months of signing the deal, the bond markets took a major swing following the September 11 attack in New York during 2001. Furthermore, the dollar declined and the Euro soared. Greek officials began to realize that the deal was not going well in the least. The Greek national debt nearly doubled in size, and in real terms (currency adjusted), the debt would double by 2008 just in Euro terms nominally. Greece faced another financial crisis in 2005, which few understood. Goldman Sachs “restructured” the deal once again, but this time they were selling the interest rate swap to the National Bank of Greece under the new government that came to power in 2004 under Karamanlis. This increased the debt even further stretching-out the payments beyond 2032. Goldman managed to extract $500 million from the Greeks, according to numerous press stories (Independent Friday 10 July 2015; Greek debt crisis: Goldman Sachs could be sued for helping hide debts when it joined euro).

Goldman didn’t even blink and went to Athens to try to sell another deal. Goldman Sachs’ president Gary Cohn personally traveled there and offered to finance the country’s health care system debt, pushing that debt even further into the future. Goldman did not merely make huge fees, it even allegedly placed a bet on the economy of Greece that it would fail based upon its inside information. Goldman is known as Government Sachs and has been apparently beyond the reach of any law anywhere. Papandreou wisely declined Goldman’s 2009 deal and this is when he blew the lid off of what Goldman had done to his country.

Goldman didn’t even blink and went to Athens to try to sell another deal. Goldman Sachs’ president Gary Cohn personally traveled there and offered to finance the country’s health care system debt, pushing that debt even further into the future. Goldman did not merely make huge fees, it even allegedly placed a bet on the economy of Greece that it would fail based upon its inside information. Goldman is known as Government Sachs and has been apparently beyond the reach of any law anywhere. Papandreou wisely declined Goldman’s 2009 deal and this is when he blew the lid off of what Goldman had done to his country.

Now Gary Cohen is in the White House orchestrating the resurrection of Glass Steagall to knock all the commercial banks out of the investment bank business leaving Goldman Sachs (Government Sachs) with just one competitor – Morgan Stanley.

Meanwhile, because the ECB will cut its bond purchases by 50% next year, Draghi will be unable to help the Italian government and rules against bailing out the banks may just explode in everyone’s face next year.

They Now Want to Criminally Charge Le Pen to Remove Her from Politics

Armstrong Economics Blog/Corruption

Re-Posted Nov 12, 2017 by Martin Armstrong

To assist the European Parliament, the French National Assembly has lifted the immunity of the head of the National Front, Marine Le Pen. The Paris parliamentary administration claims it is simply responding to a request of the judiciary, which under French law, prosecutes crimes. The trumped-up charges against Le Pen stem for publishing on Twitter the atrocities of victims of the jihadist militia Islamic State (IS). Le Pen faces several years in prison and this is obviously a political prosecution.

Le Pen responded to the press (AFP): “The freedom of opinion and the prosecution of grievances that are fundamental to a deputy is dead with this politically motivated decision.”

We seriously MUST take away the power to prosecute from the government. Any crime should be limited to VIOLENCE that results in prison and ALL prosecutions MUST be at the signed request of a citizen. If the citizen files a false charge, then they should suffer the same fate that they sought against the individual. We simply have to end political-prosecutions. That power MUST be stripped from governments when we get to reset the entire system once they crash and burn as a result of their own corruption.

Iraq & Hunt for Taxes from American Contractors

Armstrong Economics Blog/The Hunt for Taxes

Re-Posted Nov 11, 2017 by Martin Armstrong

Iraq has been accused of employing strong-arm tactics to make American military contractors operating in Iraq to pay exorbitant income taxes. They are running to Trump complaining that this is hampering the fight against Islamic State extremists – of course.

The Iraq government is demanding millions of dollars in taxes that these contractors earn providing services in Iraq. Iraqi government officials have refused to issue, or have delayed, the delivery of work visas to employees of companies that refuse to pay income taxes. They are running to Trump crying that the Iraqi authorities have held up delivery of essential supplies, such as food, fuel, and water according to The Associated Press.

Interesting how the hunt for taxes is impacting everything. Of course, any foreign company doing business in the USA has to pay taxes to the USA on what they earn. Why should this be any different?

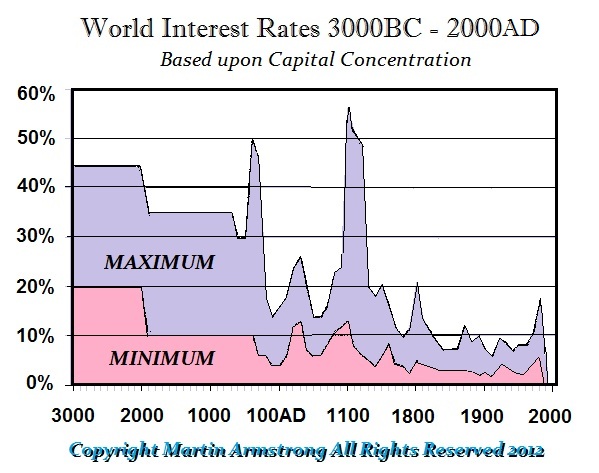

Interest Rates will Double

QUESTION: Mr. Armstrong; Thank you for an excellent conference. I have been attending since 2011. Each time you deliver a different conference and they are always better than the last. I could not help to notice on Zero Hedge they ran a piece about a Harvard University’s visiting scholar at the Bank of England who claims:

“We trace the use of the dominant risk-free asset over time, starting with sovereign rates in the Italian city states in the 14th and 15th centuries, later switching to long-term rates in Spain, followed by the Province of Holland, since 1703 the UK, subsequently Germany, and finally the US.”

Besides claiming to calculate the 700-year average real rate at 4.78% suggesting that rates will rise sharply when your models are 5,000 years, the two ridiculous statements are a 700-year average as if this really means something in the near-term when rates have been below that for nearly 10 years, and second the statement that he traces “the dominant risk-free asset over time.” You have demonstrated that moving averages are not valid in forecasting and that government routinely defaults.

You forecast at the conference that rates would rise very rapidly as we move into the Monetary Crisis Cycle. When I returned home to Greece, the latest news here is that so many people do not even have the money left to pay taxes. Is this part of the first stone in the water that sets off the waves of the Monetary Crisis Cycle?

ANSWER: It is very nice to trace 700 years and come up with the average of 4.78% by switching to the dominant economy as the financial capital of the world moved. However, starting the study in the 14th century skips the crazy part. There was the Great Financial Crisis of 1092 in Byzantium. This was really a watermark event that set in motion the decline thereafter. This study of moving from Spain to Holland, UK, Germany, and then the USA, is interesting, but regionally biased.

The fall of Byzantium resulting in the financial capital of the world moving to India – not Spain. That is why Columbus set sail trying to get to India, which was the financial capital of the world after Byzantium.

We hit a 5,000 year low. The Reversals we provided at the conference show we are looking at a near doubling in rates when we cross that number.

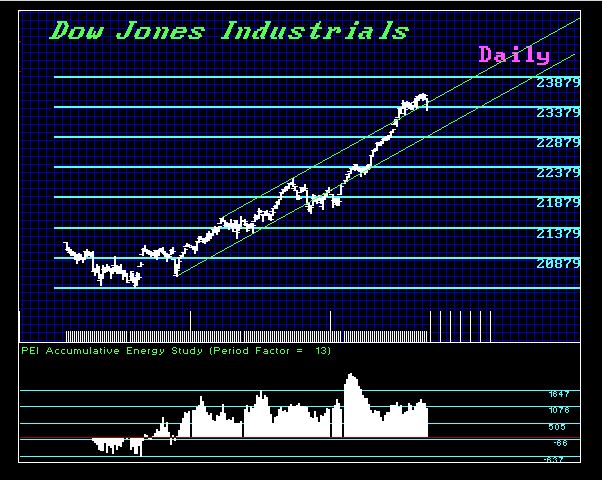

Tax Reform & the Dow

Armstrong Economics Blog/Dow Jones

Re-Posted Nov 10, 2017 by Martin Armstrong

Trump’s tax reform to cut the corporate income tax rate from 35% to 20% will be a huge boost for the economy and place tremendous pressure on the rest of the world. But already we have Republicans playing games for personal careers. They want to postpone the cut for corporations until 2019 AFTER, of course, the 2018 mid-term elections. As always, they are afraid that the Democrats will point to the rich and regain seats.

The longer they delay, the greater the economic decline. This may be the fundamental behind our model which targeted November for a temporary high. Nonetheless, our Energy Models have peaked on the Daily level suggesting that we are still not really in a serious overbought position. That implies a correction is possible, but not a major crash and change in long-term trend.