We had to wait a few weeks to see how the Beijing communists and Xi Jinping hardliners were positioned for new trade talks; and now things make sense.

Initially it seemed at odds with Beijing’s prior position to restart U.S-China trade negotiations with Vice-Premier Liu He. The prior three months of negotiation came to a collapse when Beijing resoundingly rejected the trade terms organized by Liu He. If the Red Dragon was so opposed to conciliatory terms, why would team Xi restart with the same negotiator? Now it makes sense, they didn’t.

China’s Commerce Minister Zhong Shan has been assigned the role to harden the position of the communist regime and override any panda presentations by Liu He. Vice-Premier Liu retains the panda mask, but Zhong is the ultimate control agent. The message within Zhong’s placement tells the true nature of the Chinese position: Trade War !

Beijing attempts to downplay the position of their hard-line commerce addition, but the reality of the re-started trade discussions tells a more fulsome story. Chairman Xi took the strategically presented bait and is going to engage in full confrontational trade war with President Trump and the U.S. team.

SCMP – The participation of China’s Commerce Minister in the latest trade discussion with the United States was “normal”, China’s Ministry of Commerce said on Thursday, playing down the eye-catching change in Beijing’s negotiating team.

Zhong, 64, joined Vice-Premier Liu He’s phone conversation with US Trade Representative Robert Lighthizer and US Treasury Secretary Steven Mnuchin on Tuesday – the first phone call between top negotiators since President Xi Jinping and US counterpart Donald Trump agreed to resume discussions during their summit in Osaka

on June 29.

While Zhong had previously accompanied Xi at meetings with Trump in both Buenos Aires and Osaka, this was the first time that he had joined in direct conversations with US trade negotiators, a move that put him front and centre in the talks.

At a press conference in Beijing, asked why Zhong was on board, Gao Feng, the ministry’s spokesman, said it was “quite normal” as “the [Commerce] Ministry is in charge of trade negotiations”. Gao did not explain why Zhong had not directly taken part in the previous 11 rounds of meetings between US and Chinese trade negotiators.

[…] Zhong, who previously worked under Xi when the president was at the helm of Zhejiang province, is viewed as a hardliner who has strictly toed the party line during his public speeches. (read more)

Ultimately an openly hostile and aggressive position by China is exactly what President Trump would prefer. Pretense is a painstakingly annoying negotiation strategy and President Trump is pre-disposed to be a notoriously ‘get-to-the-nub-of-it’ type of negotiator. Down South the term would be: ‘he doesn’t suffer fools’.

The current status-quo, where international investment is paused to wait and see what happens (while corporations make alternate plans), is buckets more favorable to President Trump than Chairman Xi. Essentially, the current stalemate has nimble companies departing China, the Belt-and-Road initiatives shrinking and Beijing is burning through cash to subsidize their current manufacturing base. [The currency devaluation is ongoing]

Existing tariffs remain a financial drain on China, not U.S. consumers. In actuality U.S. inflation continues to decline. Meanwhile President Trump is hitting Xi with public questions about Beijing purchasing U.S. agricultural products; a previous promise.

In actuality President Trump knows the purchase promises were the typical false-promises of Beijing; but, well, the lies have a value in calling out Panda’s duplicity.

The potential tariffs (25 percent on $300+ billion in goods) sit on the table as a weapon President Trump would love to start using. However, in the dance with the dragon Lighthizer and Ross have to wait to allow the panda mask to fully drop. Currently Chairman Xi Jinping is trying to keep the financial/investment class from noticing the panda mask is slipping. However, that ruse can’t last too much longer. Thus the dance continues.

At the 30,000/ft level China appears to have accepted that President Trump isn’t going to concede an inch. Therefore their position in the trade stand-off is timed to exhaust around the 2020 presidential election. Despite what the U.S. media are claiming, Beijing is making very visible moves to withstand more than a year of status quo strain.

SCMP – China is reinforcing its state-directed economic model despite demands for change from the United States as a condition to end the trade war, and is in fact increasing the influence of state-owned enterprises and the Communist Party’s intrusion into the boardrooms of private companies, as highlighted by a string of recent events.

On Monday, the State-owned Assets Supervision and Administration Commission (SASAC), which directly supervises more than 50 trillion yuan (US$7.3 trillion) of state assets, announced that China Poly Group, one of the industrial giants under its scope of influence, would absorb China Silk Corporation as part of a government restructuring plan.

The consolidation of state-owned enterprises has also touched local government-owned firms, especially those in resources, port and overcapacity industries. In the first half of this year, controlling stakes in at least four listed firms, including Hainan Strait Shipping and Maanshan Iron & Steel, have been shifted from local governments to the SASAC. (more)

Generally speaking President Trump has followed a 90-day process within most of the trade negotiations and discussions (KORUS, USMCA etc.), meaning when a loggerhead position is reached, he waits around 90-days as the U.S. team works to negotiate a particular point; and then if nothing, he makes a larger move to cut the Gordian knot.

If this pattern holds, we will likely see President Trump do something significant to target the Chinese stalemate around late September(ish). In the interim, USTR Lighthizer will be dancing with Liu He, while Commerce Secretary Wilbur Ross and China’s Commerce Minister Zhong Shan have a stare-off.

As much as we love him, we wouldn’t want to stare at ice-veined Wilbur Ross for three months while he smiles. When it comes to negotiation, his face is a perpetual mask.

While this is happening President Trump will take non-tariff action to make his good friend Chairman Xi feel the heat. Warm public displays toward Hong Kong, Taiwan and North Korea will make Beijing fume, but hey – that’s not a trade issue right?….

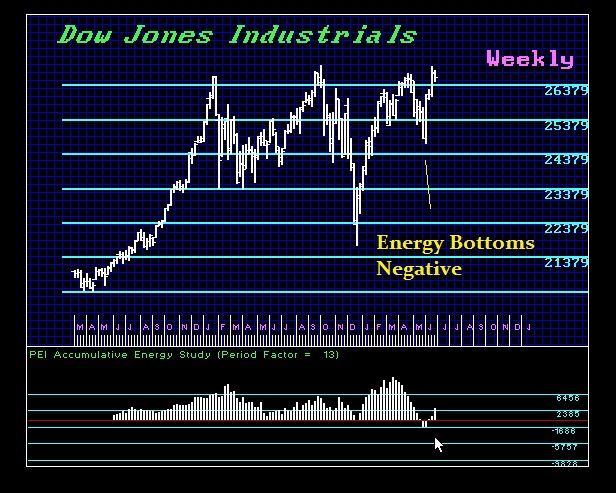

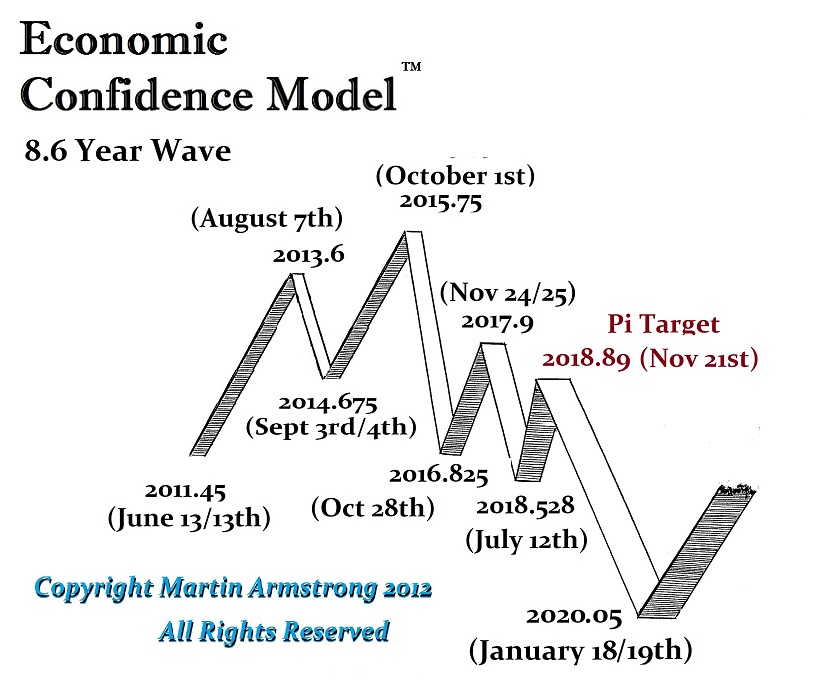

This Year’s WEC is extremely important as we now approach the turn in the Economic Confidence Model come January 2020. There were two critical patterns which were possible – 2020 low and rally thereafter, or a 2020 high with respect to the share markets. Meanwhile, we face the biggest Bond Bubble in the history of civilization and the last time something like that took place, it did not end very nicely for civilization.

This Year’s WEC is extremely important as we now approach the turn in the Economic Confidence Model come January 2020. There were two critical patterns which were possible – 2020 low and rally thereafter, or a 2020 high with respect to the share markets. Meanwhile, we face the biggest Bond Bubble in the history of civilization and the last time something like that took place, it did not end very nicely for civilization.

The Pi target on the ECM 11/21/2018 was the start of a slingshot where we had to drop sharply, scare the longs, and then rally to new highs. The problem with this pattern is that such moves are more often not sustainable on a broader sense and can warn of trouble ahead depending on who gets sucked into the mix.

The Pi target on the ECM 11/21/2018 was the start of a slingshot where we had to drop sharply, scare the longs, and then rally to new highs. The problem with this pattern is that such moves are more often not sustainable on a broader sense and can warn of trouble ahead depending on who gets sucked into the mix.