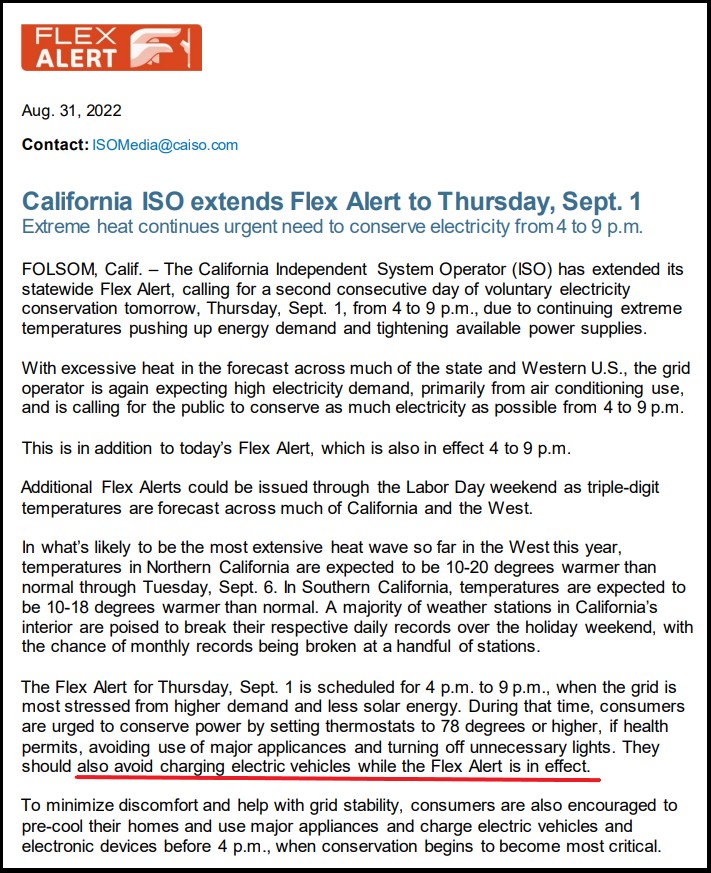

However, just a week later, the California Independent System Operator (ISO) issues a flex alert for the Labor Day holiday weekend asking people not to charge electric vehicles because the power grid cannot handle the demand. [Alert Notice]

The Flex Alert for Thursday, Sept. 1 is scheduled for 4 p.m. to 9 p.m., when the grid is most stressed from higher demand and less solar energy. During that time, consumers are urged to conserve power by setting thermostats to 78 degrees or higher, if health permits, avoiding use of major appliances and turning off unnecessary lights. They should also avoid charging electric vehicles while the Flex Alert is in effect.

To minimize discomfort and help with grid stability, consumers are also encouraged to pre-cool their homes and use major appliances and charge electric vehicles and electronic devices before 4 p.m., when conservation begins to become most critical. (LINK)

Posted originally on the conservative tree house on August 30, 2022 | Sundance

Let’s say you are an average household with an income around $100,000/yr who has an increase in electricity rates from $300 to $500 due to Joe Biden’s new national energy policy known as the Green New Deal. That’s $200 more per month for this initial economic/energy “transition” moment.

That extra $200/month equates to $2,400 per year.

That $2,400 per year is static economic activity. Meaning nothing additional was created, and nothing additional was generated. The captured $2,400 is simply an increase in the price of a preexisting expense.

Take that expense and expand it to your community of 100 friends and family households. The $2,400 now becomes $240,000 in cost that doesn’t generate anything. $240,000 is removed from the community economy. $240,000 is no longer available for purchasing other goods or services within this community of 100 households.

The economic purchasing power of the 100-household community is reduced by $240,000 per year.

Take that expense and expand it to your county of 10,000 households. Now you are reducing the county economic activity by $24 million. In this county of 10,000 households, $24 million in economic transactions have been wiped out. Meals at restaurants, purchases of goods and services, or any other spending of the $24 million within the county of 10,000 households (approximately 25,000 residents) has been lost.

Now expand that expense to a larger county, quantified as a mid-size county, of 50,000 households. The mid-sized county has lost $120 million in household economic activity, simply to sustain the status quo on electricity rates. Nothing extra has been generated. $120 million is lost. The activity within the county of 50,000 households shrinks by $120 million.

Expand that expense to a large county of 100,000 households, and the lost economic activity is $240 million.

Expand that expense to a small state of 1 million households (2.5 million residents), and the lost economic activity is $2.4 billion.

Expand that expense to a state with 5 million households (approximately 12 million residents) and the economic cost is $12 billion in lost economic activity unrelated to the expense of maintaining the status-quo on electricity use. This state loses $12 billion in purchases of goods and services, just to retain current energy use.

These examples only touch on household expenses. The community, county and state business expenses for offices, supermarkets, stores, etc. are in addition to the households quoted.

Meanwhile the Gross Domestic Product (GDP) of the community, county and state, remains static because the GDP is calculated on the total value of goods and services generated in dollar terms. The appearance of a static GDP is artificial. In real Main Street terms, $12 billion in economic activity is lost, but the price or increased value of electricity hides the drop created by the absence of goods and services purchased.

Fewer goods and services are purchased and consumed. However, statistically the inflated price of electricity gives the illusion of a status quo economy.

Now expand that perspective to a national level and you can see our current economic condition.

China does not want a war with the US. The US, however, is continually provoking China by using Taiwan as its scapegoat. The US Navy announced that two warships will be traveling through the Taiwan Strait. The reasoning? The military aims to demonstrate freedom of movement through international waters. In other words, they deliberately want to anger China.

Nancy Pelosi began the subtle attack on China when she visited Taiwan and disregarded warnings from every intelligence agency. China repeatedly warned America not to interfere in its One China policy. Yet, Pelosi said she wants Taiwan to liberate Taiwan.

China flexed its military power as soon as Pelosi left by performing almost a mock invasion through the skies and sea. As of this week, Taiwan reported 23 Chinese aircrafts and eight ships around Taiwan. Russia was provoked by NATO and backed into a corner before invading Ukraine. Beijing is increasingly feeling the pressure as the US is not actively abiding by its One China policy. Between the current recession, proxy war in Ukraine, and surmounting debt, the US is simply stretched too thin to enter a war with China.

Our models warn that geopolitical tensions will rise going into 2023. China is selling off US debt, which is another sign of coming geopolitical problems.

Reports are circulating that Greenpeace may soon ditch their poster child for climate change, Greta Thunberg. The Swedish activist was pushed to fame as a child and became notorious for passionate speeches that she was likely forced to read and believe. Klaus Schwab even featured the young girl in his film, “The Forum,” to promote Agenda 2030.

Greta is now 19 years old and no longer the perfect child-like puppet with braids and innocence. I warned that her parents manipulated this girl for their own benefit. She suffers from autism and depression, and her parents publicly stated that parading her around the globe was “medicine” for her ailments.

As an adult, she is diverting from the script. Last year, she said that democracy should be prioritized over climate change in a move that angered her handlers. She accidentally shared an image of “suggested posts” that her handlers asked her to share across social media platforms. Greta even came under fire by the Indian government after being spotted with pop star Rihanna who began promoting the Indian farmer’s protest.

There are now talks that the climate change crowd plans to discard the teen. Other activists have begun publicly criticizing her, which would have never happened when she was surrounded by the likes of Al Gore and Jennifer Morgan. “Since the beginning, we have said that we want to be hierarchy-free – and yet many saw Greta as the leader,” Swiss Jann Kessler stated. Others have whined that she was not the first to protest the weather cycle.

To the adults who abused this innocent girl – how dare you!

“The Texas miracle died in Uvalde,” the billboards states. It is in bad taste to use a school shooting to promote an agenda. The gunman was apprehended by a Texas resident with a gun. The police failed those children. None of this has anything to do with California’s policies; crime is not as prominent in Texas.

Between 2020 and 2021, over 25,000 fled California to Texas, according to the US Census data. Overall, over 360,000 people left California in 2021. Most cite that California has become completely unaffordable, with the median home price at about $797,470. Companies have fled California since the beginning of the pandemic to tax-friendly states. They lost huge job creators and revenue makers such as Facebook, Twitter, Dropbox, SpaceX, and Tesla, to name a few. Another less discussed reason is the intense woke rhetoric spewed by Newsom and others. Theft has basically become legal. Despite the beautiful scenery and weather, people simply do not want to live in the Golden State for a plethora of reasons.

Posted originally on the conservative tree house on August 29, 2022 | Sundance

During his opening monologue tonight, Tucker Carlson becomes the first mainstream pundit to point out the lies in the central bank argument.

The federal reserve and EU central banks claim they are raising interest rates to stop inflation by slowing demand. A demand side approach. However, it isn’t demand driving inflation; it’s the cost of energy driving inflation. That’s a supply side issue.

The central banks cannot admit what they are doing, or people would catch on. They are intentionally reducing economic activity in order to support having scarce energy production. WATCH:

Posted originally on the conservative tree house on August 29, 2022 | Sundance

The financial pundits are slowly starting to drop the pretending and discuss the bigger economic picture. However, as they tread very carefully, they are being very cautious about admitting too much.

A Reuters discussion of the comments by Federal Reserve Chairman Jerome Powell, starts to dip the media toe in the painful pool; yet they will not admit the Biden energy program is the source of the inflation Powell is targeting with his policy moves to shrink energy demand. Thus, the pretending continues.

If you take the written words and extract the parseltongue, you can see a more fulsome picture of what is being outlined.

JACKSON HOLE, Wyo., Aug 29 (Reuters) – The message from the world’s top finance chiefs is loud and clear: rampant inflation is here to stay and taming it will take an extraordinary effort, most likely a recession with job losses and shockwaves through emerging markets.

That price is still worth paying, however. Central banks spent decades building their credibility on inflation fighting skills and losing this battle could shake the foundations of modern monetary policy.

In other words, the U.S. economy is based on core U.S. energy systems and moving that construct to alternative energy, windmills, electric vehicles and solar panels; along with getting Americans to accept a lowered standard of living; is an “extraordinary effort.”

Yes, they are ‘all-in’ and if they lose “this battle,” the core foundations of modern monetary policy will “shake” along with the economic collapse that follows. The economic energy “transition” is the Biden policy, the federal reserve is trying to support that policy by lowering economic demand.

Yes, they also now admit that people will lose their jobs, their livelihoods and the foundation of their economic stability in the process.

[…] “Regaining and preserving trust requires us to bring inflation back to target quickly,” European Central Bank board member Isabel Schnabel said. “The longer inflation stays high, the greater the risk that the public will lose confidence in our determination and ability to preserve purchasing power.”

Banks should also keep going even if growth suffers and people start to lose their jobs. “Even if we enter a recession, we have basically little choice but to continue our policy path,” Schnabel said. “If there were a deanchoring of inflation expectations, the effect on the economy would be even worse.”

[Energy inflation, the root of all supply side inflation] “is near double-digit territory in many of the world’s biggest economies, a level not seen in close to a half century.”

[…] Deglobalisation, the realignment of alliances due to Russia’s war, demographic changes and more expensive production in emerging markets could all make supply constraints more permanent. (read more)

Yes, the “realignment global of alliances,” as an outcome of the western world policy to fracture global markets based on energy use. Notice they are now starting to admit what we have discussed here for over a year?

“The global economy seems to be on the cusp of a historic change as many of the aggregate supply tailwinds that have kept a lid on inflation look set to turn into headwinds,” Agustín Carstens, the head of the Bank of International Settlements, said.

“If so, the recent pickup in inflationary pressures may prove to be more persistent,” said Carstens, who heads a group often called the central bank of the world’s central banks.

All this points to rapid interest rates hikes, led by the Fed with the ECB now trying to catch up, and elevated rates for years to come. (read more)

Indeed, we are only now on the front side “cusp” of the transition which will force the continued lowering of economic activity within the aligned nations for more than a generation or two. All economic activity, essentially all human activity, will have to be stalled and reduced until the levels of sustainable energy production can catch up to the levels of energy needed for the now smaller economy.

With current estimations of 50+ years before sustainable energy can generate 25 to 50 percent of the need, this is going to take a long time, and the bankers & financial control agents are going to have to simultaneously make the economies of the allied nations much smaller.

The planned energy oven is small, the size of the economic pizza must be shrunk in order to fit within it.

My last and important point is this…. The multinational corporations, banks and global finance folks, do not enter into these situations without a carefully planned way to retain their own wealth. The job of a “hedge fund manager” is described in the title, to find a “hedge” against risk to continue increasing wealth.

The billionaire elites that have assembled their wealth on the old economic system will not trust anything to chance as this global cleaving of the world economy takes place. Being reactionary is not how they operate. These groups pre-stage their wealth and assets outside the zone of collateral damage. They are proactive, not reactive to these global financial events.

With the foundation of the western economic system now being changed, look carefully at the political landscape to see what Wall Street risk mitigation maneuvers are taking place. My very strong hunch on this wealth preservation facet leads me back to domestic politics, and suddenlythings make sense. I’m not wrong. I am open to being wrong, but I’m not wrong.

Posted originally on the conservative tree house on August 29, 2022 | Sundance

As the global cleaving begins taking shape based on the new western energy system, the Build Back Better agenda, Russian energy exports are worth a lot more money. As a result, the Russian economy has gained more wealth than before the western sanctions regime was triggered. As noted by the Wall Street Journal:

(Via WSJ) – […] Demand from some of the world’s largest economies has given Russian President Vladimir Putin the upper hand in the energy battle that shadows the war in Ukraine, and has confounded the West’s bid to cripple Russia’s economy with sanctions.

Sales are booming in Russia’s export market, the world’s largest in crude and refined fuels. And new trade arrangements have given Mr. Putin cover to use natural gas exports as an economic weapon against Ukraine’s European allies. Before the war, Russia supplied Europe with 40% of its gas. It has since throttled flows through the Nord Stream pipeline to Germany and other conduits, driving prices higher and putting pressure on European households and businesses.

Oil revenue more than makes up the difference. “Russia is swimming in cash,” said Elina Ribakova, deputy chief economist at the Institute of International Finance. Moscow earned $97 billion from oil and gas sales through July this year, about $74 billion of that from oil, she said.

[…] Russian energy sales have flourished by finding new buyers, new means of payment, new traders and new ways of financing exports, according to oil traders, former Russian industry executives and shipping officials.

“There came a realization that the world needs oil, and nobody’s brave enough to embargo 7.5 million barrels a day of Russian oil and oil products,” said Sergey Vakulenko, an analyst and former Russian energy executive.

After buyers in the U.S., the European Union and their Pacific allies cut back their Russian oil imports, much of it went to nations in Asia that have declined to take sides in the conflict.

An unexpected market has been the Middle East. Exports of Russian fuel oil, a lightly refined version of crude, now go to Saudi Arabia and the United Arab Emirates, often stopping in Egypt en route.

The Russian oil is either burned in Saudi power stations or exported from Fujairah, a U.A.E. port and hot spot for blending Russian and Iranian oils to conceal their provenance. This is oil that before the war was shipped to U.S. refiners.

The Russian imports, purchased at a discount, free state giant Saudi Arabian Oil Co. to export its crude at market prices. “The Saudis are happy to take their oil and sell it rather than burning it,” said Carole Nakhle, chief executive at consulting firm Crystol Energy.

The arrangement adds supply to the global oil market, helping put a lid on prices. “This is a win-win situation for the Russians and even, I would say, for the Europeans and the U.S.,” Ms. Nakhle said. (read more)

Posted originally on the conservative tree house on August 26, 2022 | Sundance

Buried inside Section 5114(b)(4) of the National Defense Authorization Act for Fiscal Year 2022 was a repeal of 1994 law that required the U.S. State Department to publish an annual list of arms sales to foreign countries. The “World Military Expenditures and Arms Transfers” report (WMEAT) put sunlight every year on what weapons the U.S. was selling to foreign countries.

Conveniently timed with the $60+ billion aid package to Ukraine, the U.S. State Dept, now says the WMEAT report will not be published any longer. If a person was to believe the Ukraine arms deals were essentially money laundering operations, well, this announcement by the State Dept. might be interpreted as a way to hide it. [LINK]

State Dept – WMEAT 2021, which the Department of State published in December 2021, is the final edition of World Military Expenditures and Arms Transfers (WMEAT). Section 5114(b)(4) of the National Defense Authorization Act for Fiscal Year 2022 repealed the 1994 statutory provision that required the Department of State to publish an edition of WMEAT every year. Consistent with this repeal, the Department of State will cease to produce and publish WMEAT.

Copies of all editions of WMEAT dating from 1974 to 2021 remain publicly accessible as Adobe PDF or Excel spreadsheet documents (LINK)

Posted originally on the conservative tree house on August 26, 2022 | Sundance

When Chairman Powell says things are really, really going to suck as monetary policy tries to support Biden’s goals to reduce energy supplies, will people believe him?

The agenda of the federal reserve was clearly outlined today in the remarks from Chairman Powell in Jackson Hole, Wyoming. The Fed chair is trying to manage the economic policy transition by reducing economic activity to match intentionally diminished energy supplies. Lowering economic activity drops demand for energy. Unfortunately, as admitted by Powell today, this means a period of “some pain” for Americans as the central banks join together in an effort to lower consumption. WATCH:

What does “some pain” mean? It means lower incomes, higher prices, lowered standards of living and more scarce resources. During this transition to owning nothing and being happy about it, the pain is your wealth being stripped as the economy is intentionally diminished.

We will not be able to afford much; we won’t be able to afford the foods we want; we will not be able to purchase anything except the essentials, and those essentials will cost much more; we won’t be able to vacation, travel, or enjoy recreational activities; we won’t be able to afford any indulgences; but at the end of the process, we will learn to live more meager existences based on lowered expectations needed for sustaining the planet. Pay no attention to the elites who don’t have those concerns, comrade.

[Transcript] – POWELL: “At past Jackson Hole conferences, I have discussed broad topics such as the ever-changing structure of the economy and the challenges of conducting monetary policy under high uncertainty. Today, my remarks will be shorter, my focus narrower, and my message more direct.”

“The Federal Open Market Committee’s (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal. Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy. Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all. The burdens of high inflation fall heaviest on those who are least able to bear them.

Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.

The U.S. economy is clearly slowing from the historically high growth rates of 2021, which reflected the reopening of the economy following the pandemic recession. While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum. The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers. Inflation is running well above 2 percent, and high inflation has continued to spread through the economy. While the lower inflation readings for July are welcome, a single month’s improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.

We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent. At our most recent meeting in July, the FOMC raised the target range for the federal funds rate to 2.25 to 2.5 percent, which is in the Summary of Economic Projection’s (SEP) range of estimates of where the federal funds rate is projected to settle in the longer run. In current circumstances, with inflation running far above 2 percent and the labor market extremely tight, estimates of longer-run neutral are not a place to stop or pause.

July’s increase in the target range was the second 75 basis point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting. We are now about halfway through the intermeeting period. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook. At some point, as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases.

Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy. Committee participants’ most recent individual projections from the June SEP showed the median federal funds rate running slightly below 4 percent through the end of 2023. Participants will update their projections at the September meeting.

Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century. In particular, we are drawing on three important lessons.

The first lesson is that central banks can and should take responsibility for delivering low and stable inflation. It may seem strange now that central bankers and others once needed convincing on these two fronts, but as former Chairman Ben Bernanke has shown, both propositions were widely questioned during the Great Inflation period.1 Today, we regard these questions as settled. Our responsibility to deliver price stability is unconditional. It is true that the current high inflation is a global phenomenon, and that many economies around the world face inflation as high or higher than seen here in the United States.

It is also true, in my view, that the current high inflation in the United States is the product of strong demand and constrained supply, and that the Fed’s tools work principally on aggregate demand. None of this diminishes the Federal Reserve’s responsibility to carry out our assigned task of achieving price stability. There is clearly a job to do in moderating demand to better align with supply. We are committed to doing that job.

The second lesson is that the public’s expectations about future inflation can play an important role in setting the path of inflation over time. Today, by many measures, longer-term inflation expectations appear to remain well anchored. That is broadly true of surveys of households, businesses, and forecasters, and of market-based measures as well. But that is not grounds for complacency, with inflation having run well above our goal for some time.

If the public expects that inflation will remain low and stable over time, then, absent major shocks, it likely will. Unfortunately, the same is true of expectations of high and volatile inflation. During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decisionmaking of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions. As former Chairman Paul Volcker put it at the height of the Great Inflation in 1979, “Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations.”2

One useful insight into how actual inflation may affect expectations about its future path is based in the concept of “rational inattention.”3 When inflation is persistently high, households and businesses must pay close attention and incorporate inflation into their economic decisions. When inflation is low and stable, they are freer to focus their attention elsewhere. Former Chairman Alan Greenspan put it this way: “For all practical purposes, price stability means that expected changes in the average price level are small enough and gradual enough that they do not materially enter business and household financial decisions.”4

Of course, inflation has just about everyone’s attention right now, which highlights a particular risk today: The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.

That brings me to the third lesson, which is that we must keep at it until the job is done. History shows that the employment costs of bringing down inflation are likely to increase with delay, as high inflation becomes more entrenched in wage and price setting. The successful Volcker disinflation in the early 1980s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem the high inflation and start the process of getting inflation down to the low and stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.

These lessons are guiding us as we use our tools to bring inflation down. We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.” [Transcript End]

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America