Armstrong Economics Blog/Economics Re-Posted Apr 7, 2021 by Martin Armstrong

QUESTION: Hello Martin, can you explain to me how a currency would sustain value for international trade if a country, like Canada (where I live), did what you suggested and stopped issuing debt and just printed money to level that was 5% – 10% of national GDP? would it depend on the attractiveness of what a country exports eg: Canada exports oil, lumber, crops like wheat/soy/canola, minerals – both precious and functional? What would happen to a country that didn’t have exports as a significant portion of it’s GDP? I am curious about how currencies would react to your restructuring plan that eliminated the need for a country to issue debt. Thanks for all your insights and theories. Very helpful.

Trapped in Canada with an egoistic misguided Prime Minister who doesn’t appear to like Canada (he keeps telling us how awful we are) or Canadians, he prefers spending time with global elites and is following their plan even though it damages Canada pretty significantly.

MB

ANSWER: Right now, every country spends more than it takes in. The deficits are funded by selling debt, which then competes against the private sector. The interest rates rise and fall on sovereign debt based upon the confidence from one week to the next. If they stopped borrowing, then the capital investment would turn to the private sector, creating more economic growth. If income taxes were eliminated, the economy would grow based upon innovation which is what it should be driven by.

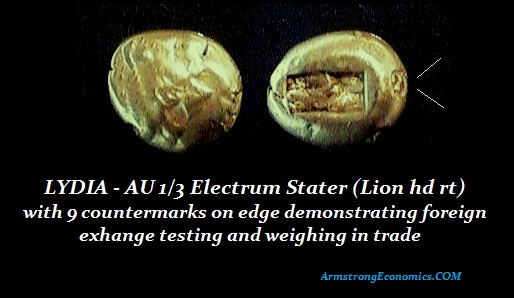

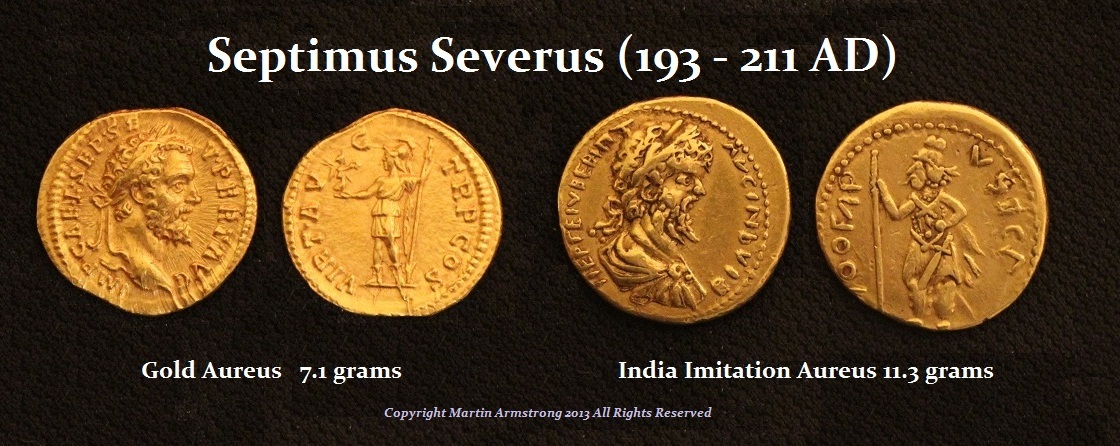

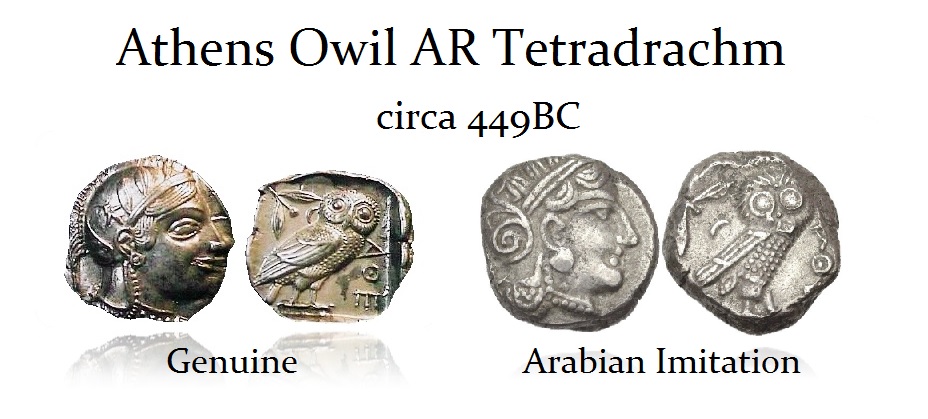

The confidence in the currency would simply depend upon the strength of the economy, as was the case for Athens and Rome in ancient times. Their coinage was imitated because they were the dominant economies of their time. The value of a currency is the strength of its economy. It has NEVER been about its backing, which is purely a theory that arrived with paper money. Rome had no national debt. The value of the currency was more than its metal content. Here we have a gold aureus of Septimus Severus (193-211 AD) and the imitation in gold made in India. The imitation weighed more than the original. Imitations were made in the same quality of metal, so it proves that it was not a counterfeit but that a coin from the core economy possessed a greater value than the raw metal.

Just compare Russia, which has tremendous resources, against China, Japan, and Germany that had really no gold reserves. Russia did not expand its economy while the others boomed because of its people. The value of a currency is the TOTAL productive capacity of its economy — the work ethic of its people. Russia has not been able to rise substantially because it never fully embraced the idea of capitalism. They moved from communism to an oligarchy.