Armstrong Economics Blog/Banking Crisis Re-Posted Mar 17, 2023 by Martin Armstrong

QUESTION #1: Marty, I think your warning about the collapse of leadership in government and the private sector rings true as Ken Griffin, the founder of hedge fund Citadel, said the rescue of Silicon Valley Bank shows the U.S. economic system is “breaking down before our eyes” because they bailed out the depositors. Yet Carl Icahn seems to agree with your saying that the U.S. economy is at a breaking point because of inflation. He said, “every hegemony has been destroyed by inflation.”

Very few so-called billionaires seem to understand what’s at stake. It makes me think they were just lucky in how they made their money. After Griffin’s comment, I would not be inclined to invest in Citadel. Then a group of banks is talking about depositing $20 to $30 billion to save Republic bank.

Is there any hope for the future when leadership is absent in these times of chaos?

UT

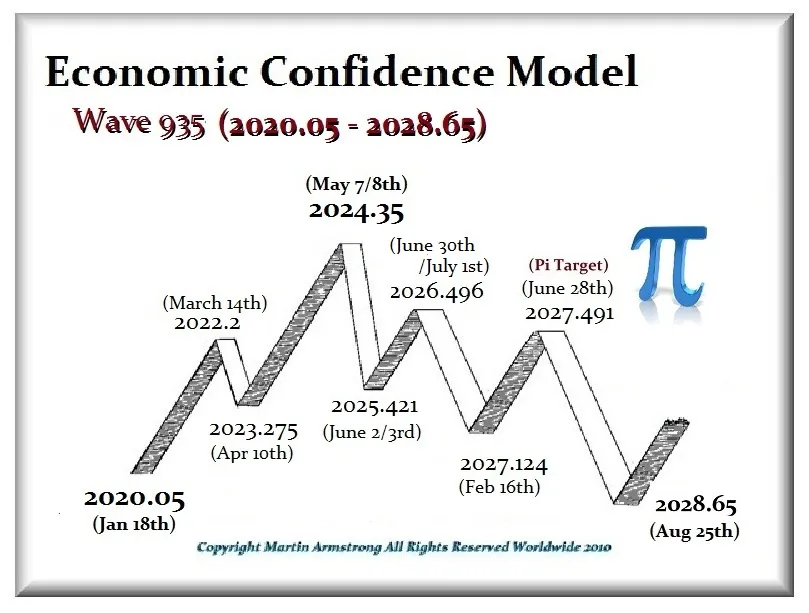

QUESTION #2: Thanks for everything you do. At the WEC, you warned about banks and even the big funds. The turning point was at the end of January here in 2023. Is it possible that this financial crisis will be the major factor even overpowering war when the ECM comes into play by April 10th?

CW

ANSWER: Anyone who does not understand that inflation is a natural occurrence when you get into a war is clearly not a student of history and has no business being the CEO of even the head local dog-catcher. The Roman deity Janus, after whom January is named, was the two face entity who looked at the past and the future. The doors to his temple would be closed when there was peace. That symbolized that nothing was at risk of changing. However, in times of war, they would leave the doors open to symbolize the uncertainty of war that the spirits could flow in and out.

Only today, do we seem to no longer respect that the cost of war is both lives lost and inflation for those who survive. This Ukrainian Proxy War serves no purpose. Winning or losing will have ZERO impact on our national security or the future of the people. This is simply a grudge match instigated by the Neocons who perpetually love war as long as someone else is dying for their personal goals. To them, it is nothing more than watching a war on CNN and cheering as if it were a football game.

I have said that this war will undermine the entire US economy and that is now manifesting in the Financial Crisis of 2023 which will be far worse than any of these people expect. The lack of experience and the stupidity of those who remark that capitalism is collapsing because they are honoring the depositors is absurd. A depositor has NO WAY of understanding the financial status of a bank until it is too late. They receive no warning and yet there are those who say they should suffer the losses because that is capitalism.

Sorry, but that has NOTHING to do with capitalism. It is no different than FRAUD soliciting money with a false pretense. Investing in a hedge fund like Citadel is different from a bank. Depositors in a hedge fund know they are investing their money and they are getting a piece of that return. That is capitalism. Someone who has a bank account where their social security check is automatically deposited took on no such risk. Sorry – that is different that a hedge fund that goes bust.

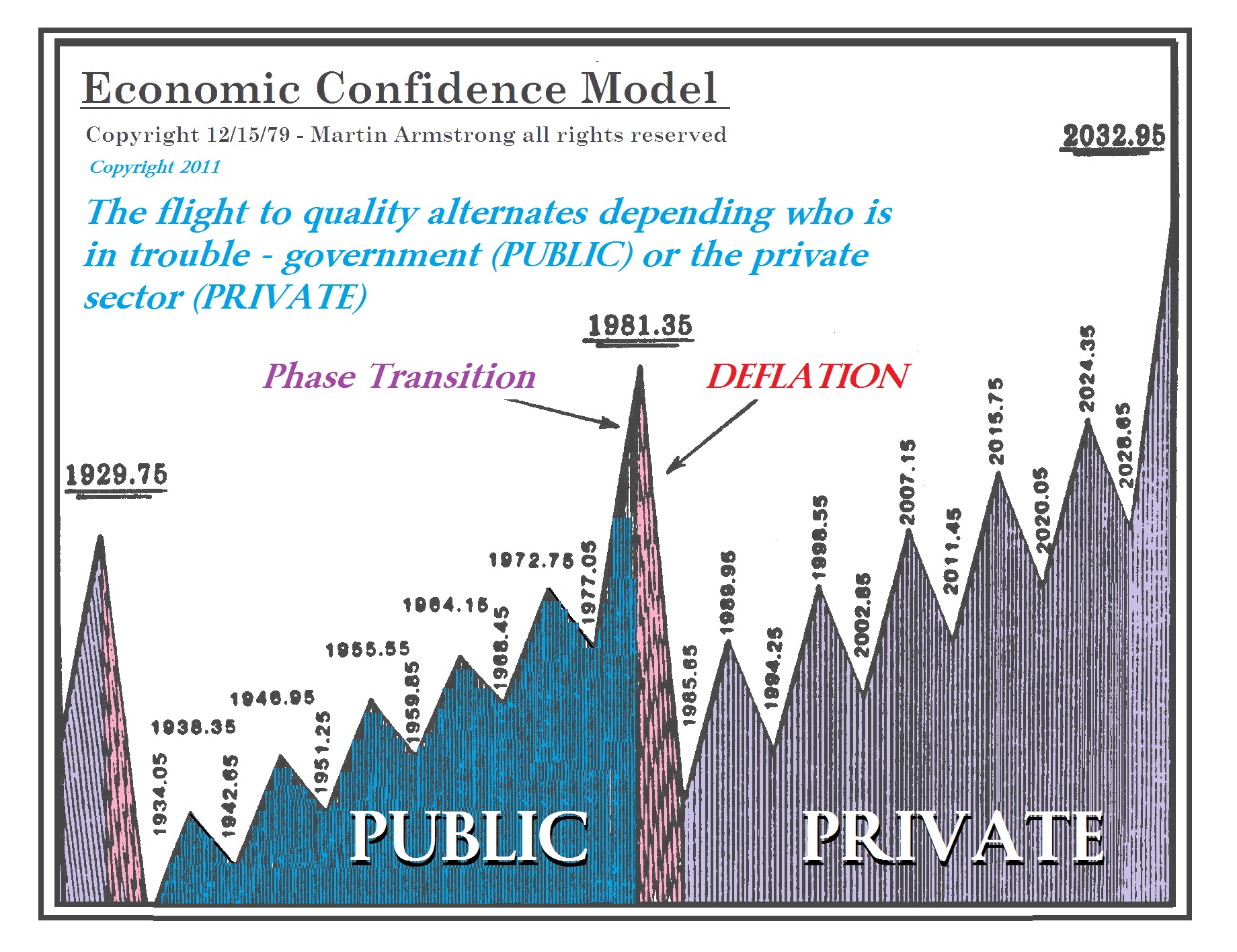

The problem we have is that the ECM turning point is April 10th. Yet it is also the Pi Target from the fall of the USSR and the birth of even Ukraine. We just had Poland losing their mind and sending jets to Ukraine. That makes Poland a viable target for war. Poland is irresponsible given the fact that the Ukrainians slaughtered over 300,000 of them and has refused to ever apologize for their WWII Nazi involvement.

We have a problem here with the Financial Crisis simultaneously with important cyclical targets regarding war. Any personal interpretation I can offer is just a personal opinion. Both trends are colliding into April and this may be a two-prong panic of unprecedented significance.