It turns out that North Korea-backed hackers stole a record $1.7bn of cryptocurrency in 2022, according to blockchain analysis firm Chainalysis. It also appears that they had a hand in the collapse of the cryptocurrency exchange FTX where the auditors have reported that around $415m of cryptocurrency has been stolen by hackers. This is becoming a very interesting story with several facets from funding North Korea to laundering money for Zelensky to pay off the Democrats for the Midterm elections.

There is no way they will let this case go to trial. They will have to cut a deal or they are going to need to have some pumped-up loser kill him when on bail, or Judge Lewis Kaplan will have to revoke his bail and put him in MCC where they can kill him easily and blame another inmate and the guards fell asleep once again and, of course, the camera didn’t work.

At the end of the day, North Korea has been making a lot of money hacking into cryptocurrencies. Your crypto is going to a good cause – World War III to achieve Bill Gate’s dream – population reduction since the vaccines did not kill enough people off – yet.

Posted originally on the CTH on December 22, 2022 | Sundance

FTX Founder Sam Bankman-Fried waived an extradition fight and U.S. Marshals flew him from the Bahamas to New York late Wednesday night. Appearing in a Manhattan court today, the judge set bail at $250 million and permits SBF to remain under house arrest at his parent’s California home until trial begins.

Additionally, it was revealed that Carolyn Ellison, 28, the former chief executive of Bankman-Fried’s trading firm, Alameda Research, and Gary Wang, 29, who co-founded FTX, pleaded guilty to charges including wire fraud, securities fraud and commodities fraud. Both are cooperating witnesses with the prosecution against the FTX founder.

New York – The cryptocurrency entrepreneur Sam Bankman-Fried can post $250 million bond and live in his parents’ home in California while he awaits trial on charges that he swindled investors and looted customer deposits on his FTX trading platform, a judge said Thursday.

Assistant U.S. Attorney Nicolas Roos said in U.S. District Court in Manhattan that Bankman-Fried, 30, “perpetrated a fraud of epic proportions.” Roos proposed strict bail terms, including a $250 million bond and house arrest at his parents’ home in Palo Alto, California.

An important reason for allowing bail was that Bankman-Fried agreed to waive extradition, Roos said.

Magistrate Judge Gabriel W. Gorenstein agreed to the bond and also approved the house arrest proposal. He also said Bankman-Fried would be required to get an electronic monitoring bracelet before leaving the Manhattan courthouse.

[…] Prosecutors and regulators contend that Bankman-Fried was at the center of several illegal schemes to use customer and investor money for personal gain. He faces the possibility of decades in prison if convicted on all counts.

In a series of interviews before his arrest, Bankman-Fried said he never intended to defraud anyone.

Bankman-Fried is charged with using money, illicitly taken from FTX customers, to enable trades at Alameda, spend lavishly on real estate, and make millions of dollars in campaign contributions to U.S. politicians. (read more)

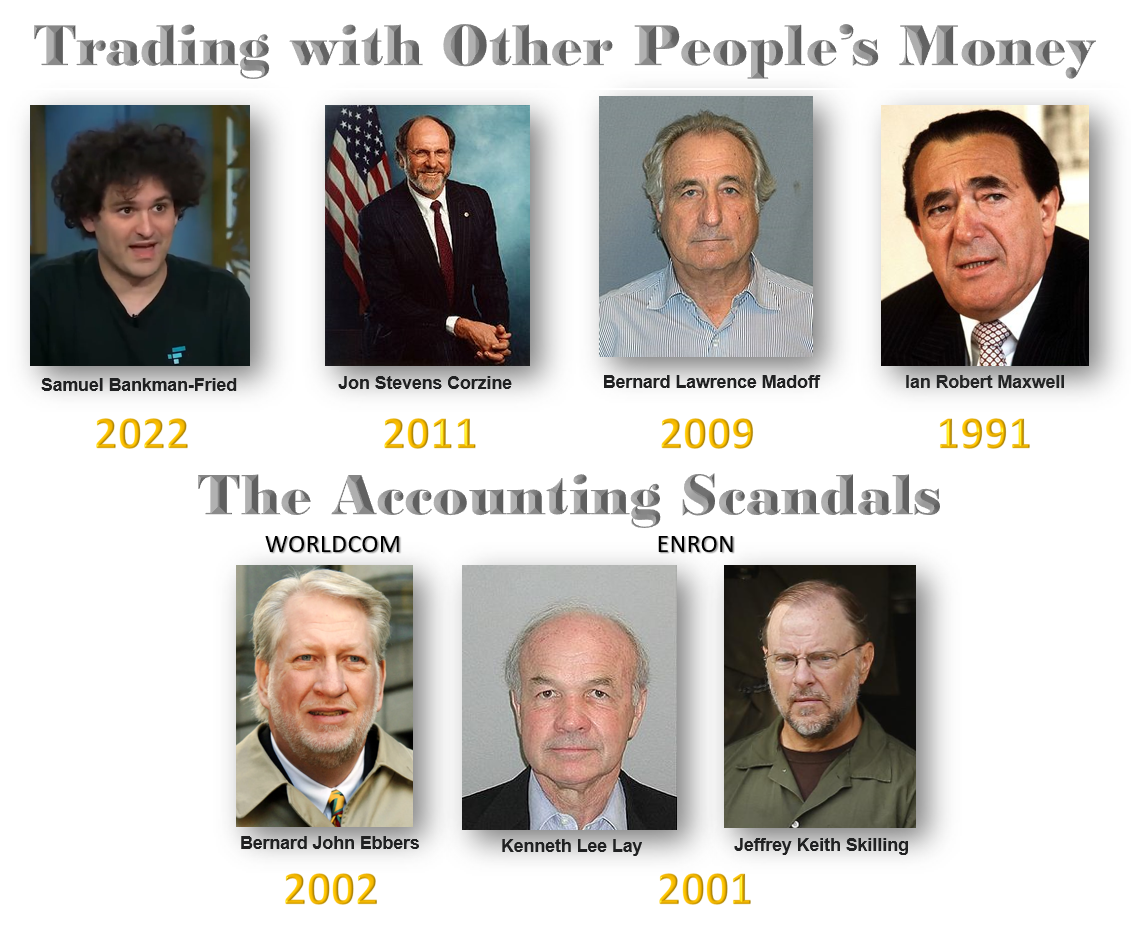

This FTX scandal is the death nil for cryptos. At first, I assumed that perhaps they lost a ton of money because of the implosion of the bond market. But this was not the case. In fact, this is perhaps the worst I have ever seen and it comes from trading losses from kids that had no experience whatsoever with regard to trading. They obviously did not even understand fiduciary responsibility. MF Global was taking client money to trade in London and got the market wrong. Bernie Madoff remains a mystery wrapped up in a political enigma. From 1991 to 2008, Bernie and Ruth Madoff contributed only about $240,000 to federal candidates, parties, and committees. Madoff was not trying to buy influence as was taking place at FTX. Maxwell mysteriously died in 1991 when his trading scandal surfaced, but he was also secretly backing the communist coup against Gorbachev in 1991.

Then there were the accounting scandals of ENRON and Worldcom whereby to hide their losses and failures, they engaged in accounting fraud to cover up the true story. But there were not using other people’s money to trade, they were hiding their bad performance from shareholders hoping to make a comeback.

That is the common denominator. I have been called into many crises. The one thing that always runs through the problem is the refusal to admit a mistake. That seems to lead to losing trades continuing to be held in hope of the infamous COMEBACK. The motive seems to be the same and many of the problems I have been called into to help solve have been in corporations where some strategy went wrong. In these cases of ENRON, Worldcom that were allowed to fester. The trading scandals are perpetuated in the hope that the next trade will win it all back.

Crypto contagion instigated by FTX, has only gotten more interesting since Sam Bankman-Fried sent a series of cryptic tweets spelling out the words “What HAPPENED” after his wealth wipeout. After the collapse of FTX, we are looking at a collapse in confidence in all digital assets.

With this degree of collapse in even Bitcoin, there will be more bankruptcies lining up. Inexperience dominates this young field and facing a stiff recession ahead going into 2023, this meltdown is not over yet. The low in Bitcoin from 2021 high is not likely before 2023. Thus – as they say – it ain’t over until the fat lady sings (a reference to Opera).

The collapse of the FTX Exchange is pretty straightforward insofar as this is the same lesson that constantly repeats in finance time and time again. Basically, FTX lent US$10bn of client funds to their trading arm Alameda, which used it for leveraged their own crypto speculation because the crypto market has been collapsing. Typically, someone like Sam Bankman-Fried had his whole life wrapped up in this venture. Lacking financial controls operating from the Bahamas, moving the money from client funds to his trading arm Alameda was possible. Historically, someone in this position sees his world collapsing but is not prepared to see that unfold for it requires admitting that he was wrong on crypto, to begin with. Consequently, such a person is not trying to actually rob clients’ money, they most likely see it as a temporary loan to save the company and the market will bounce back – or so they believe.

Our computer had picked the high in Bitcoin perfectly and has been projecting the collapse all along the way. But crypto has become a religion and in so doing it clouds the judgment of people who want to believe the story. Alameda blew up in a crypto meltdown because it did not want to accept that the crypto boom was over. The loan he probably thought would be temporary, vanished in the implosion. At first, I would have assumed they had actually invested the money and lost it on the bond market collapse. But that was perhaps too traditional. Here, it appears they were trying to defend their own cryptocurrency and trying to buy the low that kept moving lower. It appears he was allegedly simply using clients’ funds to trade keeping gains for his firm and the clients now suffer the risk.

It appears that they allegedly were trying to defend the crypto market and did not understand that the boom was over. The loans could not then be repaid. As crypto was crashing, some people needed to cash out. The attempt to pull out US$5bn from FTX exposed the fact that the cash was all gone. This is not so unusual. It has happened before. This time, the prosecutors are clamoring to be the one to charge him so they can become famous over his dead body.

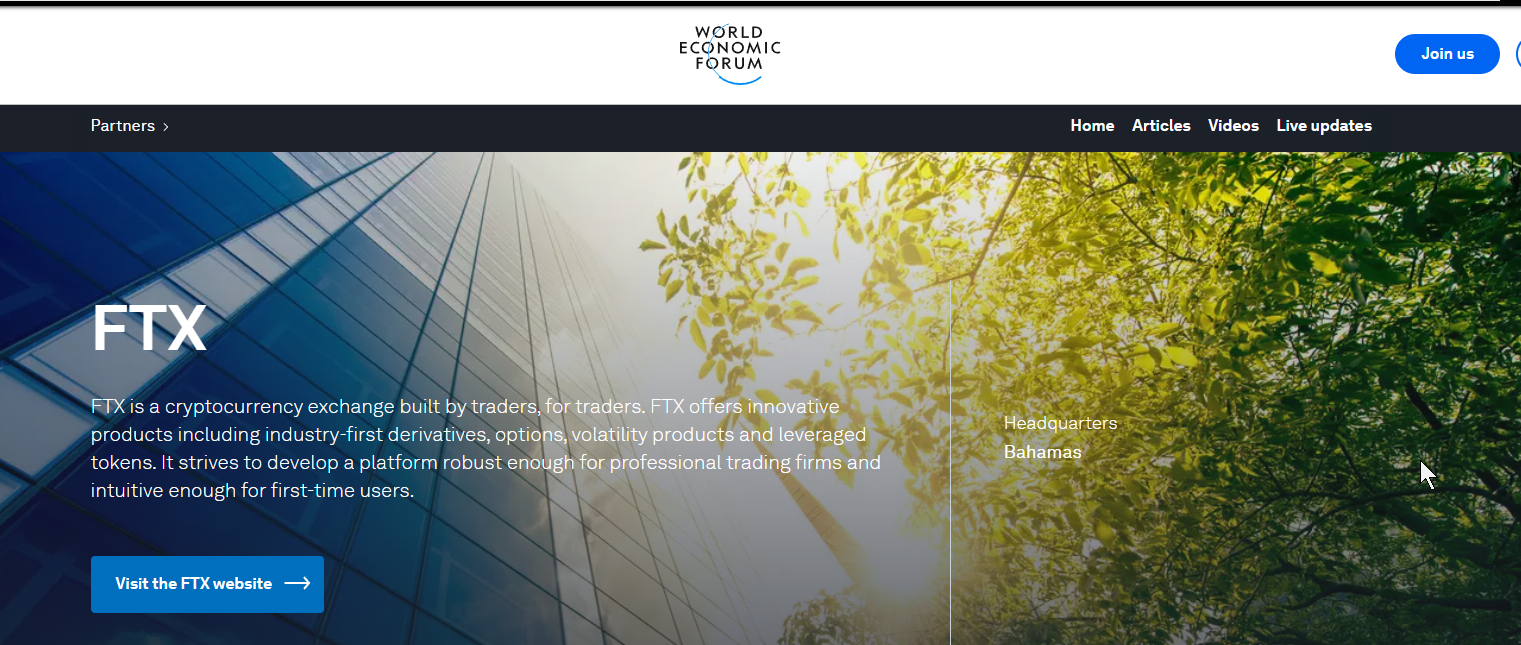

FTX was a partner with Klaus Schwab’s World Economic Forum (WEF). Of course, the WEF has suddenly removed the page and is desperately trying to hide their involvement with FTX and Sam Bankman-Fried. Naturally, eliminating paper currency has been the goal of the WEF because they support the end of not just capitalism, but also democracy. Schwab’s push has been his Great Reset and to control society to impose his economic philosophy inspired by Marx and Lenin.

This is by no means the first violation of fiduciary responsibility that presents a custodial risk. MF Global Holdings Ltd., you might recall, was a firm formerly run by New Jersey ex-Gov. Jon Corzine was accused in 2013 of unlawfully using customer money to meet his firm’s funding needs. When MF Global went bust because of trading by ex-Goldman Sach’s Jon Corzine’s trading using his client’s money in London also outside the regulatory eye of the USA, he was NEVER prosecuted for illegally using $1.6 billion of 26,000 client’s money. That is not going to be the case this time. So what is the difference between Corzine and Bankman-Fried? Corzine was ex-Goldman Sachs.

Indeed, Corzine was well-connected right into the White House with Obama. Nobody went to jail and clients had to wait in bankruptcy to get their money – even cash in the accounts was taken. There are clear risks with the broker and clearer. As long as the SEC is run with former Goldman Sachs staff, there will NEVER be an honest regulator. Even when all the banks pled criminally guilty, the SEC exempted everyone from losing their licenses. They would NEVER do that with anyone outside of New York City. The SEC will never prosecute the banks – EVER!!!!

Indeed, several federal investigations had been launched into MF Global, including probes by the Commodity Futures Trading Commission (its main regulator), the Securities and Exchange Commission, the Federal Bureau of Investigation, and Justice Department prosecutors in both Chicago and New York. The brokerage has also been the focus of several congressional hearings. Not a single one charged Corzine with trading with his client’s money. The losses that eventually drove MF Global into bankruptcy stemmed from high-risk bets on European sovereign bonds that Corzine made as he swung for the fences. Corzine bet big that the bond issuers would not default.

Commodity Futures Trading Commission simply fined Jon Corzine only $5 million over MF Global’s rapid descent into bankruptcy on Oct. 31, 2011, as an estimated $1.6 billion of customer money went missing. Anyone else would have been in prison for a minimum of 20 years.

It was Martin Glenn who was the judge in New York on M.F. Global bankruptcy. He was the first one to engage in FORCED LOANS by abandoning the rule of law to help the bankers by protecting them from losses taking client accounts to cover M.F. Global’s losses. He simply allowed the confiscation of client funds when in fact the rule of law should have been that the bankers were responsible and M.F. Global’s losses should have been reversed as they did even when Robert Maxwell’s companies failed in London from his illegal trading taking employee pension funds.

Yes, that was Ghislaine Maxwell’s father and the guy who was in control of the company that Bill Browder worked for before Edmond Safra. Never should the client’s funds be taken for M.F. Global’s losses to the NY Bankers. It was Judge Martin Glen who placed the entire financial; system at risk by trying to protect the bankers. Martin Glenn pampered these bankers making them the new UNTOUCHABLES. We have to be concerned that there really is no rule of law that will protect you in a crisis.

On Bloomberg TV, Sam Bankman-Fried explained why he even created FTX. He said he was experiencing his own frustration at Alameda Research, which was his crypto-focused proprietary trading firm. He was frustrated with the execution he was receiving at various crypto exchanges so he claimed that inspired FTX’s creation in May 2019. FTX grew rapidly to become the third largest crypto exchange in the world, with approximately $16 billion of customer assets under custody over 43 months.

Bankman-Fried stated that Alameda was making lots of money, but it could have been making more and he did not have access to venture capital. Claims of 100% annualized returns are not uncommon in a boom, but any experienced trader knows what goes up, also comes down. Alameda was relying on “cobbling together lines of credit” to expand its capital base. He then created FTX to solve his funding problem creating his own exchange that even the WEF cheered as a partner. He actually created a platform that was tailored for his own company, Alameda, to facilitate its trading needs. FTX coined the phrase “built by traders, for traders.”

There was an obvious conflict of interest questions regarding the close relationship between FTX and Alameda. Being operated from the Bahamas raised questions among those of us who are seasoned financial market observers whether the two were truly arm’s length from each other. However, people were so pumped up on adrenalin with crypto being the end of the dollar and central banks that this new free-wheeling crypto world believed what they wanted to believe and never looked too closely. FTX operated outside the reach of the US regulatory domain and there was a lack of any fiduciary confirmation. When the founder of Binance, the world’s largest crypto exchange, Changpeng Zhao, openly questioned the soundness of the FTX/Alameda nexus on Twitter saying he would sell over $500 million worth of FTX’s token FTT, that was the kiss of death weather or not he realized he would unleash a crypto panic that would engulf the entire industry in a matter of days.

The collapse of FTX will now become a contagion for the crypto world. This 20-something group of inexperienced traders has signaled the demise of an industry that was getting all the hype with no substance. This crypto world will be seen as the DOT COM Bubble of 2000. With a recession on the horizon, the collapse of sovereign debt, and the monetary system as a whole, people will be looking for more of the safe bets rather than roll the dice on crypto. Nothing ever goes straight down. But by year-end, the volatility should perk up everyone’s view of the world.

Posted originally on the conservative tree house on November 14, 2022 | Sundance

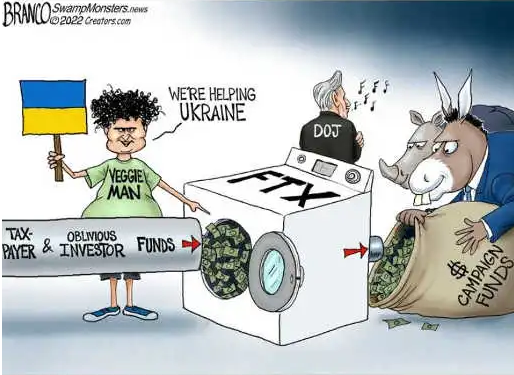

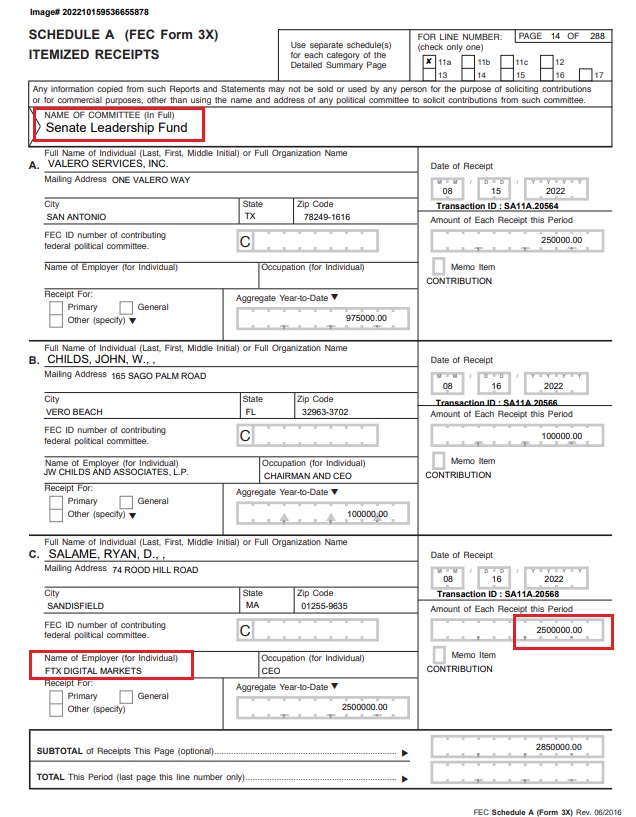

The Senate Leadership Fund is the Political Action Committee (PAC) controlled by Mitch McConnell. Within the quarterly FEC filings of the Senate Leadership Fund, we discover that in addition to funding Joe Biden and Democrats, the ponzi scheme known as the FTX cryptocurrency exchange was also funding Mitch McConnell with $2.5 million. [Document Source]

There is a lot of speculation about U.S. taxpayer funds going to Ukraine, then transferring into the FTX crypto exchange program, then exiting back out with FTX donations to the DC politicians who provided the Ukraine funds. If this ends up being accurate, then the FTX crypto currency operation was being used as a laundry system to funnel money from congress through Ukraine and back into the pockets of politicians.

Do not look for DC politicians to investigate or expose themselves in this potential laundry operation.

Most people think when they vote for a federal politician -a House or Senate representative- they are voting for a person who will go to Washington DC and write or enact legislation. This is the old-fashioned “schoolhouse rock” perspective based on decades past. There is not a single person in congress writing legislation or laws.

In modern politics not a single member of the House of Representatives or Senator writes a law or puts pen to paper to write out a legislative construct. This simply doesn’t happen.

Over the past several decades a system of constructing legislation has taken over Washington DC that more resembles a business operation than a legislative body. Understand this dynamic and you understand how politicians become multi-millionaires on much lesser salaries; and why ‘We The People’ are insignificant and annoying gnats to their business model. Here’s how it works right now.

Outside groups, often called “special interest groups”, are entities that represent their interests in legislative constructs. These groups are often representing foreign governments, Wall Street multinational corporations, banks, financial groups or businesses; or smaller groups of people with a similar connection who come together and form a larger group under an umbrella of interest specific to their affiliation.

Sometimes the groups are social interest groups, activists, climate groups, environmental interests etc. The social interest groups are usually non-profit constructs who depend on the expenditures of government to sustain their cause or need.

The for-profit groups (mostly business) have a purpose in Washington DC to shape policy, legislation and laws favorable to their interests. They have fully staffed offices just like any business would – only their ‘business‘ is getting legislation for their unique interests.

These groups are filled with highly paid lawyers who represent the interests of the entity and actually write laws and legislation briefs.

In the modern era this is actually the origination of the laws that we eventually see passed by congress. Within the walls of these buildings within Washington DC is where the ‘sausage’ is actually made.

Again, no elected official is usually part of this law origination process.

Almost all legislation created is not ‘high profile’, they are obscure changes to current laws, regulations or policies that no-one pays attention to. The passage of the general bills within legislation is not covered in media. Ninety-nine percent of legislative activity happens without anyone outside the system even paying any attention to it.

Once the corporation or representative organizational entity has written the law they want to see passed – they hand it off to the lobbyists.

The lobbyists are people who have deep contacts within the political bodies of the legislative branch, usually former House/Senate staff or former House/Senate politicians themselves.

The lobbyist takes the written brief, the legislative construct, and it’s their job to go to congress and sell it.

“Selling it” means finding politicians who will accept the brief, sponsor their bill and eventually get it to a vote and passage. The lobbyist does this by visiting the politician in their office, or, most currently familiar, by inviting the politician to an event they are hosting. The event is called a junket when it involves travel.

Often the lobbying “event” might be a weekend trip to a ski resort, or a “conference” that takes place at a resort. The actual sales pitch for the bill is usually not too long and the majority of the time is just like a mini vacation etc.

The size of the indulgence within the event, the amount of money the lobbyist is spending, is customarily related to the scale of benefit within the bill the sponsoring business entity is pushing. If the sponsoring business or interest group can gain a lot of financial benefit from the legislation, they spend a lot on the indulgences.

Recap: Corporations (special interest group) write the legislation. Lobbyists take the law and go find politician(s) to support it. Politicians get support from their peers using tenure and status etc. Eventually, if things go according to norm, the legislation gets a vote.

Within every step of the process there are expense account lunches, dinners, trips, venue tickets and a host of other customary financial waypoints to generate/leverage a successful outcome. The amount of money spent is proportional to the benefit derived from the outcome.

The important part to remember is that the origination of the entire process is EXTERNAL to congress.

Congress does not write laws or legislation; special interest groups do. Lobbyists are paid, some very well paid, to get politicians to go along with the need of the legislative group.

When you are voting for a Congressional Rep or a U.S. Senator you are not voting for a person who will write laws. Your rep only votes on legislation to approve or disapprove of constructs that are written by outside groups and sold to them through lobbyists who work for those outside groups.

While all of this is happening the same outside groups who write the laws are providing money for the campaigns of the politicians, they need to pass them. This construct sets up the quid-pro-quo of influence, although much of it is fraught with plausible deniability.

This is the way legislation is created.

If your frame of reference is not established in this basic understanding you can often fall into the trap of viewing a politician, or political vote, through a false prism. The modern origin of all legislative constructs is not within congress.

“we’ll have to pass the bill to, well, find out what is in the bill” etc. ~ Nancy Pelosi 2009

“We rely upon the stupidity of the American voter” ~ Johnathan Gruber 2011, 2012.

Once you understand this process you can understand how politicians get rich.

When a House or Senate member becomes educated on the intent of the legislation, they have attended the sales pitch; and when they find out the likelihood of support for that legislation; they can then position their own (or their families) financial interests to benefit from the consequence of passage. It is a process similar to insider trading on Wall Street, except the trading is based on knowing who will benefit from a legislative passage.

The legislative construct passes from K-Street into the halls of congress through congressional committees. The law originates from the committee to the full House or Senate. Committee seats which vote on these bills are therefore more valuable to the lobbyists. Chairs of these committees are exponentially more valuable.

Now, think about this reality against the backdrop of the 2016 Presidential Election. Legislation is passed based on ideology. In the aftermath of the 2016 election the system within DC was not structurally set-up to receive a Donald Trump presidency.

If Hillary Clinton had won the election, her oval Office desk would be filled with legislation passed by congress which she would have been signing. Heck, she’d have writer’s cramp from all of the special interest legislation, driven by special interest groups that supported her campaign, that would be flowing to her desk.

Why?

Simply because the authors of the legislation, the originating special interest and lobbying groups, were spending millions to fund her campaign. Hillary Clinton would be signing K-Street constructed special interest legislation to repay all of those donors/investors.

Congress would be fast-tracking the passage because the same interest groups also fund the members of congress.

President Donald Trump winning the2016 election threw a monkey wrench into the entire DC system…. In early 2017 the modern legislative machine was frozen in place.

The “America First” policies represented by candidate Donald Trump were not within the legislative constructs coming from the K-Street authors of the legislation. There were no MAGA lobbyists waiting on Trump ideology to advance legislation based on America First objectives.

As a result of an empty feeder system, in early 2017 congress had no bills to advance because all of the myriad of bills and briefs written were not in line with President Trump policy. There was simply no entity within DC writing legislation that was in-line with President Trump’s America-First’ economic and foreign policy agenda.

Exactly the opposite was true. All of the DC legislative briefs and constructs were/are antithetical to Trump policy. There were hundreds of file boxes filled with thousands of legislative constructs that became worthless when Donald Trump won the election.

Those legislative constructs (briefs) representing tens of millions of dollars’ worth of time and influence were just sitting there piled up in boxes under desks and in closets amid K-Street and the congressional offices. Legislation needed to be in-line with an entire new political perspective, and there was no-one, no special interest or lobbying group, currently occupying DC office space with any interest in synergy with Trump policy.

Think about the larger ramifications within that truism. That is also why there was/is so much opposition.

No legislation provided by outside interests means no work for lobbyists who sell it. No work means no money. No money means no expense accounts. No expenses mean politicians paying for their own indulgences etc.

Politicians were not happy without their indulgences, but the issue was actually bigger. No K-Street expenditures also means no personal benefit; and no opportunity to advance financial benefit from the insider trading system.

Without the ability to position personal wealth for benefit, why would a politician stay in office? The income of many long-term politicians on both Republican and Democrat sides of the aisle was completely disrupted by President Trump winning the election. That is one of the key reasons why so many politicians retired immediately thereafter.

When we understand the business of DC, we understand the difference between legislation with a traditional purpose and modern legislation with a financial and political agenda.

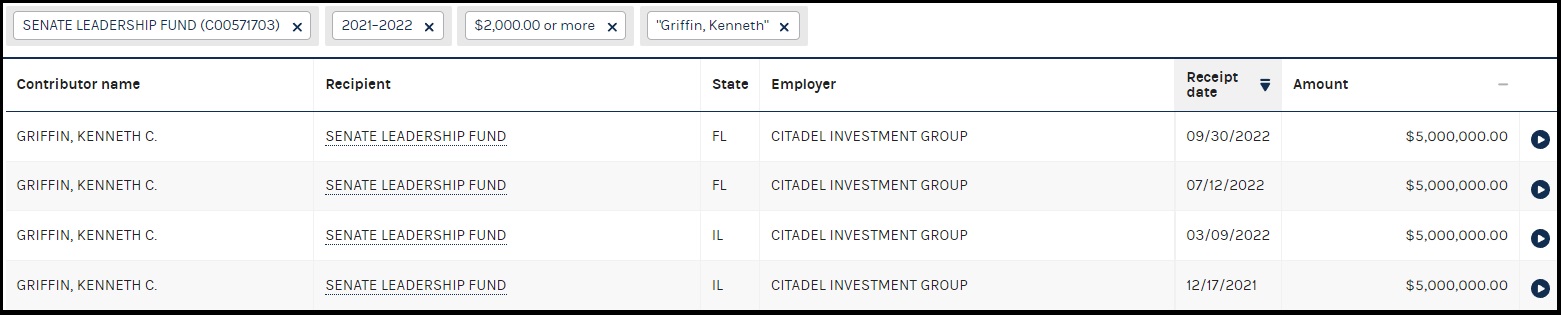

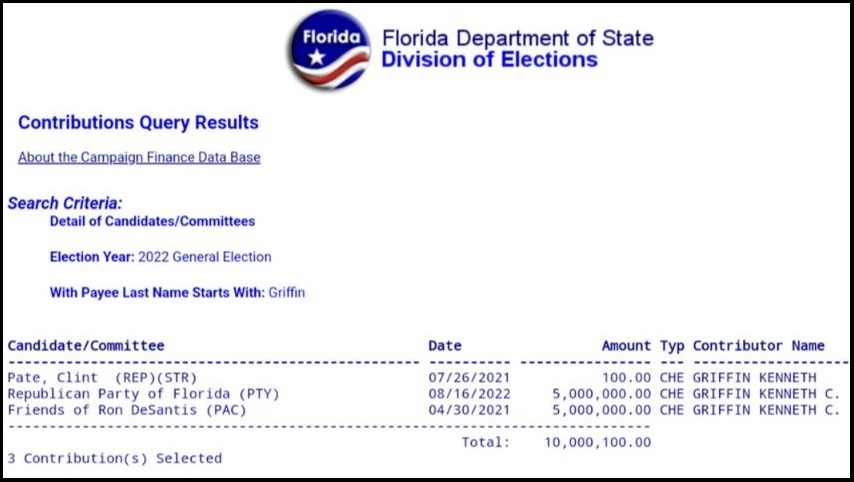

Additionally, while looking for the FTX donations, it’s worth noting that Citadel Investment CEO Ken Griffin also gave Mitch McConnell’s Senate Leadership Fund, $20 million in 2022. This is the same Ken Griffin that is a major donor funding the Ron DeSantis 2024 effort. (SOURCE)

As RedState reported, crypto-exchange FTX collapsed after its much-lauded founder, Sam Bankman-Fried, appeared to make improper transfers of customer money. Somewhere between $1-2 billion of that amount has now gone missing and Bankman-Fried also has disappeared.

What makes this so interesting, though, isn’t just that a lot of really wealthy people got scammed. It’s that Bankman-Fried also happens to be one of the top donors to the Democratic Party. In fact, outside of George Soros, no one has done more to bankroll Democrat efforts since the 2020 election. Joe Biden alone received a whopping $5.2 million.

But here’s where things get even weirder. Apparently, while the United States was bankrolling Ukraine and its war effort, that country’s leaders were investing money into FTX.

It was also revealed that FTX had partnered with Ukraine to process donations to their war efforts within days of Joe Biden pledging billions of American taxpayer dollars to the country. Ukraine invested into FTX as the Biden administration funneled funds to the invaded nation, and FTX then made massive donations to Democrats in the US.

There are so many questions that arise from this. For example, why is Ukraine, which we are all assured is broke and needs US taxpayer money, playing around with a Democrat-linked crypto company? This wasn’t just about accepting donations through the portal. The report specifically says that Ukraine actively invested money in FTX.

While that was happening, FTX’s founder was handing out tens of millions of dollars, from the Bahamas, to help elect Democrats back in the United States. That is one of the shadiest things I’ve ever witnessed in politics.

Yes, the chain of custody regarding the funds involved is tough to know. When and where money was sent is something only an investigation of FTX’s internal operation can ascertain. Still, the appearances here are just horrific. Were Democrats funneling taxpayer money to Ukraine, only for some of it to be sent to FTX so it could be funneled back to Democrat campaigns? That’s a question that must be answered, and any attempt to gloss over it will raise major red flags.

I don’t think I’m going out on a limb by suggesting that if another company had been scamming people while bankrolling the Republican Party, it would be major news. There would be calls for investigations as far as the eye could see to figure out whether Republican politicians were using that company as a passthrough to avoid campaign finance laws. Never mind that simply receiving funds from a Ponzi scheme, even without ill intent, is really bad on its own.

This entire situation stinks to high heaven. It appears that Republicans will end up taking the House of Representatives. When that becomes official, GOP members need to dive headfirst into this and figure out what in the world happened. Because having a Democrat mega-donor get exposed like this while also having Ukraine tied up in the mix is too much to ignore.

Front-page contributor for RedState. Visit my archives for more of my latest articles and help out by following me on Twitter @bonchieredstate.

Posted originally on the conservative tree house on November 12, 2022 | sundance

FTX crypto currency exchange CEO Sam Bankman-Fried is a major donor to multiple progressive causes and politicians. This week as FTX starts to collapse, the financial system underneath the exchange looks more like a Ponzi scheme falling apart.

The CEO had been a major donor to regulators on Capitol Hill, and the tentacles of FTX extend to Ukraine where Sam Bankman-Fried was operating to support the Ukraine government with crypto currency collections and donations. The FTX corporation and CEO Sam Bankman-Fried is now under multiple investigations. Here’s the 90-second recap of the current dynamic. WATCH:

.

(Via Daily Caller) Sam Bankman-Fried, prolific Democratic donor and ex-CEO of now-bankrupt cryptocurrency exchange FTX, funded the campaigns of members of Congress overseeing the Commodity Futures Trading Commission (CFTC), one of the key bodies tasked with regulating the crypto industry and the subject of Bankman-Fried’s aggressive lobbying.

Bankman-Fried’s FTX is currently under investigation by the CFTC and the Securities and Exchange Commission (SEC) after Bankman-Fried allegedly moved $10 billion in client assets from his crypto exchange to his trading firm Alameda Research, and a liquidity crisis at his exchange which prompted the company to file for bankruptcy. However, prior to the agency’s probe, Bankman-Fried aggressively courted the CFTC – and funded several key lawmakers charged with overseeing the agency, pouring cash into their campaign coffers. (read more)

(Via CoinDesk) The past week has seen a dizzying downward spiral for Sam Bankman-Fried’s huge crypto empire. Bankman-Fried’s FTX crypto exchange has paused withdrawals, and a tentative bailout from rival Binance appears to be kaput. That could put depositor funds at risk, and certainly spells a major setback for not only Bankman-Fried but for the cryptocurrency industry as a whole.

These downfalls aren’t rare in crypto, which is subject to extreme boom-bust cycles. But FTX and Bankman-Fried are unique in the stature they achieved before self-immolating. Over the past three years, FTX has come to be widely regarded as a reputable exchange, despite not submitting to U.S. regulation. Bankman-Fried has himself become globally influential, thanks to his thoughts on cryptocurrency regulation and his financial support for U.S. electoral candidates – not necessarily in that order.

These narratives about both FTX and Bankman-Fried are now clearly dead in the water, given recent evidence that everything was not as it seemed at the exchange, or at Bankman-Fried’s other firm, Alameda Research. (read more)

Comment: I use Coinbase to hold some crypto. They sent me an email saying that my account that I had for years would be limited to withdrawals only if I do not give them updated government ID and download the latest version of the application. I use this on my PC and do not have the application. I worry they’ll take what is left of my failing cryptos. Luckily I only put “play money” into these holdings but I imagine others will experience losses and frozen accounts in the near future. The deadline they gave me was October – not sure if that is for all. I messaged out to Coinbase for help updating my account but cannot fully verify it after many tries.

Reply: Government hates cryptocurrency. They have always been concerned about their ability to squeeze out every last penny in taxes from crypto. I am not surprised that Coinbase is emailing users for additional documentation days after the Inflation Reduction Act was passed. With nearly 88,000 new IRS agents, there will certainly be teams of hundreds or thousands of accountants who will analyze all crypto holdings.

The initial idea behind the creation of crypto has been lost. I warned in March on our private blog on Socrates that cryptocurrencies may be suspended altogether one day. Biden could sign an Executive Order to regulate cryptos because countries like Russia can use it to circumvent sanctions. Not only is Biden authorizing the regulation of digital currencies, but he is also instructing to move forward with a central bank cryptocurrency. Once that is done, all other cryptocurrencies will be seized and folded into the government’s crypto. There will be no competition.

I’ve said it before and will say it again – cryptocurrencies are not a safe investment. I know it is not a popular opinion; people have had success with trading. The problems with cryptocurrencies: (1) they depend entirely upon the government; with the stroke of a pen, they can all be seized; (2) they depend upon a power grid; (3) they also become dependent upon others accepting them.

A fourth all too common issue is that crypto trading platforms can prevent people from trading with little or no explanation. Binance recently announced that users are not permitted at this time “due to a stuck transaction causing a backlog.” CEO Changpeng Zhao stated on Twitter that the issue would be fixed in under 30 minutes. Later in the day, he said the issue would “take a bit longer to fix than my initial estimate,” but would only impact the Bitcoin network. Uncoincidentally, this sudden system glitch occurred after bitcoin fell by 10% beneath the $24,000 level.

This happens more than they would like people to believe. A few years back, a friend of mine was blocked out of their Bittrex account as soon as one of their cryptos began crashing. At one point, Bittrex suspended and eliminated numerous accounts in 2017, and it took them days to respond. They claimed the issue was a “compliance review,” as these platforms can seemingly make up any excuse they please. During that instance, they did not even inform users before they were locked out of their accounts. Unpopular opinion but the fact of the matter is that cryptos are seriously flawed.

A Joint Statement, representing 17,000 Physicians and Medical Scientists to End the National Emergency, Restore Scientific Integrity, and Address Crimes Against Humanity

The time is now. As most readers of this substack are now well aware, this is not just about COVID. The constitution hangs in the balance. Please help us to get these messages spread far and wide. The 17,000 Physicians and Medical Scientists in our organization, who are not financially conflicted and remain committed to the Hippocratic Oath, are doing our part. Now we ask that you help us to help you. We need your help.

A Joint Statement, representing 17,000 Physicians and Medical Scientists

To Restore Scientific Integrity

17,000 Physicians and Medical Scientists Declare that the State of Medical Emergency must be lifted, Scientific integrity restored, and crimes against humanity addressed.

17,000 physicians and medical scientists declare that the state of medical emergency must be lifted, scientific integrity restored, and crimes against humanity addressed.

We, the physicians and medical scientists of the world, united through our loyalty to the Hippocratic Oath, recognize that the disastrous COVID-19 public health policies imposed on doctors and our patients are the culmination of a corrupt medical alliance of pharmaceutical, insurance, and healthcare institutions, along with the financial trusts which control them. They have infiltrated our medical system at every level, and are protected and supported by a parallel alliance of big tech, media, academics and government agencies who profited from this orchestrated catastrophe.

This corrupt alliance has compromised the integrity of our most prestigious medical societies to which we belong, generating an illusion of scientific consensus by substituting truth with propaganda. This alliance continues to advance unscientific claims by censoring data, and intimidating and firing doctors and scientists for simply publishing actual clinical results or treating their patients with proven, life-saving medicine. These catastrophic decisions came at the expense of the innocent, who are forced to suffer health damage and death caused by intentionally withholding critical and time-sensitive treatments, or as a result of coerced genetic therapy injections, which are neither safe nor effective.

The medical community has denied patients the fundamental human right to provide true informed consent for the experimental COVID-19 injections. Our patients are also blocked from obtaining the information necessary to understand risks and benefits of vaccines, and their alternatives, due to widespread censorship and propaganda spread by governments, public health officials and media. Patients continue to be subjected to forced lock-downs which harm their health, careers and children’s education, and damage social and family bonds critical to civil society. This is not a coincidence. In the book entitled “COVID-19: The Great Reset”, leadership of this alliance has clearly stated their intention is to leverage COVID-19 as an “opportunity” to reset our entire global society, culture, political structures, and economy.

Our 17,000 Global COVID Summit physicians and medical scientists represent a much larger, enlightened global medical community who refuse to be compromised, and are united and willing to risk the wrath of the corrupt medical alliance to defend the health of their patients.

The mission of theGlobal COVID Summit is to end this orchestrated crisis, which has been illegitimately imposed on the world, and to formally declare that the actions of this corrupt alliance constitute nothing less than crimes against humanity.

We must restore the people’s trust in medicine, which begins with free and open dialogue between physicians and medical scientists. We must restore medical rights and patient autonomy. This includes the foundational principle of the sacred doctor-patient relationship. The social need for this is decades overdue, and therefore, we the physicians of the world are compelled to take action.

After two years of scientific research, millions of patients treated, hundreds of clinical trials performed and scientific data shared, we have demonstrated and documented our success in understanding and combating COVID-19. In considering the risks versus benefits of major policy decisions, our Global COVID Summit of 17,000 physicians and medical scientists from all over the world have reached consensus on the following foundational principles:

We declare and the data confirm that the COVID-19 experimental genetic therapy injections must end.

We declare doctors should not be blocked from providing life-saving medical treatment.

We declare the state of national emergency, which facilitates corruption and extends the pandemic, should be immediately terminated.

We declare medical privacy should never again be violated, and all travel and social restrictions must cease.

We declare masks are not and have never been effective protection against an airborne respiratory virus in the community setting.

We declare funding and research must be established for vaccination damage, death and suffering.

We declare no opportunity should be denied, including education, career, military service or medical treatment, over unwillingness to take an injection.

We declare that first amendment violations and medical censorship by government, technology and media companies should cease, and the Bill of Rights be upheld.

We declare that Pfizer, Moderna, BioNTech, Janssen, Astra Zeneca, and their enablers, withheld and willfully omitted safety and effectiveness information from patients and physicians, and should be immediately indicted for fraud.

We declare government and medical agencies must be held accountable.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America