armstrong Economics Blog/Corruption Re-Posted Apr 30, 2022 by Martin Armstrong

Spread the love

The first principle in battling against the Alinsky crew is to not to accept their terminology. Controlling language is a specific tactic of the professional political left. We used to call it labeling, but modern leftists moved beyond labels into the creation of new definitions. Modern leftists now use two different strategies depending on their target: (1) create new words, the traditional labeling; and (2) redefine existing words.

In this interview Naomi Wolf is one of the few people I have seen who correctly starts her discussion by dispatching the linguistics and framing her own baseline argument. All politicians and candidates for office should watch how Wolf responds to the first question from Tucker Carlson, and then makes the better argument.

Wolf doesn’t waste time debating “misinformation”, “disinformation”, or “malinformation”, instead she accurately just says those things do not exist. Information stands undefined. From that position there are truth and lies. Her approach is exactly correct. Do not accept the insanity of the Alinsky language effort. A refreshing and really good interview, WATCH:

.

On January 13, 2022, the fraudulent and managed autocrat, the installed occupant of the White House, gave instructions to his fellow travelers in Big Tech, and I quote:

It was crystal clear what Joe Biden was telling his allies in social media to do. There is information the Government wants us to hear, and everything else is disinformation or misinformation the U.S. Govt disapproves of.

Immediately CTH encountered criticism for our position on information. However, Wolf understands exactly what we have discussed:

Ultimately, the government is not trying to control words, they are trying to control thoughts.

Comrades, the deep, long and sullen violins were playing tearfully today as the World War Reddit theatrical performance came heavily to the Pentagon. Leading narrative engineer John Kirby was captivating in his role as profoundly sullen squire overwhelmed with the magnitude of the moment and the emotion of the struggle in Ukraine.

The Biden production company is attempting to raise another $33 billion for enhanced theater operations in the besieged European country. Pentagon chournalists are collecting canned goods, including soundbites, to support the war effort; and the Defense Dept is broadcasting the theme to Chariots of Fire across NATO signals.

Meanwhile, emotions throughout Europe are running high as valiant Prince Volodymyr of Donbas assembles his polished armor and directs his trusted steed into the wind.

Yes, today the clouds loomed heavy as Director Kirby narrated his audience while fighting bravely to keep the spirit of Edward R Murrow alive. The wide-eyed maidens held their collective breath waiting in the mournful stillness of the moment… You could hear a pin drop. WATCH:

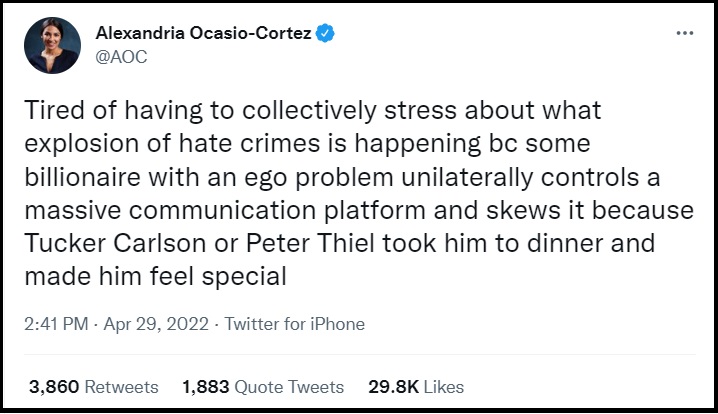

An emotionally unstable moonbat from the House of Representatives is “collectively stressed” because apparently Twitter ownership is directly connected to hate crimes on the streets. (Source)

Being worried about Twitter creating hate crimes, is one fear higher than being chased by a turtle.

Comrades, earlier today dissident Governor Ron DeSantis spoke out against the latest effort of the Biden administration to create an official disinformation bureau with a dedicated mission to assist Big Tech and social media platforms in their control of speech. {Direct Rumble Link}

There is no dis-, mis-, or mal-information There is only information the Government wants you to hear, and the information the U.S. Govt disapproves of. The DHS disinformation board is dedicated to dealing with the latter.

Governor DeSantis made his remarks during an announcement to expand Florida infrastructure. WATCH:

Posted originally on the conservative tree house on April 29, 2022 | Sundance

The Bureau of Economic Analysis (BEA) released March and first quarter (Q1) data today on personal income and outlays [DATA HERE]. The results show an increase in Q1 wages of 4.5%. However, inflation is running 6.6% on the items workers need to purchase. The net result on Main Street is unsustainable inside the economy. The U.S. stock market is responding negatively to this release.

It’s easy to get caught up in the esoteric weeds, so my effort here is to show just what is happening by putting an overlay of checkbook economics into the BEA release. If we take out the noise it is very easy to see the problem. I have modified TABLE-4 to put the results into simple understandable terms.

By looking at the far-right column (Q1 2022) you can see the problem. Wage growth at $268.00, minus taxes paid $51.40, leaves disposable income or take-home pay at $216.60. However, our expenses for living (shelter, food, utilities, energy, etc) cost $398.50, leaving a deficit for our income of $181.90. We either dip into our savings to cover our expenses, or we go into debt. This is not sustainable.

If you look at Q1 last year, you can clearly see where all of the inflation is coming from. That massive increase in income came from the federal COVID bailout and stimulus funds. $4 trillion directly pumped into the economy at a time when Biden justified massive bailout spending by saying they needed to offset the economic cost of prior COVID intervention (businesses and workers shut down). That is the primary source of current inflation.

If you take out that Q1 spend from the economic activity, the U.S. economy was already contracting. This is why CTH has continued to say our economy was in a state of contraction since June/July of 2021. Everything after that massive dump of money was false economic activity; the GDP growth was artificial. That bailout spending dried up in the fall and winter of last year and now we see the 2022 GDP going negative.

In essence the GDP contraction that we should have seen in 2021 was delayed by the massive infusion of cash in April of 2021. However, that massive infusion of cash created inflation. That inflation has been a crisis that grew from the summer of 2021 to its apex in the last month.

♦ So, what does all of this mean?

Let’s cut to the chase. As CTH accurately predicted previously, inflation comes in waves because supplier purchases are done in contract terms of 30, 60 and 90 days. As each contract for purchased goods expires, the new prices for future goods are changed. We see waves of inflation in roughly three-month increments, and while prices were rising faster on a daily and weekly basis, those wave cycles started in October of 2021.

Wave 1, came Oct/Nov/Dec 2021.

Wave 2, came Jan/Feb/March 2022.

We talked about each wave as it was coming and as it arrived. Ultimately, Wave-2 was bigger than Wave-1 as the cumulative increases the total supply chain and manufacturing flowed into the products we purchase.

♦ Where are we now? There are two sub-sets:

• Inflation on durable goods is now at the apex. The durable goods price flatlines right now as all production costs are embedded in the cost of the product. The prices of finished goods are now set; inflation has caught up to production; the prices of on-shelf and inbound deliveries are higher, but stable.

Now, we enter the phase where consumer demand becomes the dominant factor in price. Simultaneously, demand is contracting because the higher rate of inflation in highly consumable goods (energy, utility costs, housing, gasoline, food) is now a spending priority for consumers and eating a larger portion of wages. As a result, the price of durable goods is now dependent on the ability of the consumer to pay for them.

Sellers of durable goods are going to be chasing a smaller customer base who can afford them. Durable goods prices will remain static, and now durable goods prices will likely become part of the competitive equation. The businesses within the durable goods sector are going to have to find customers in order to stay in business. Incentives will show up this spring/summer as businesses need customers. If you are a wise, careful and smart shopper for durable goods you will find deals

• Inflation on consumable goods is not yet at the apex. It’s likely close to production parity, but prices pressures are still volatile in the upward direction. The price of gasoline and transportation overall will be a big factor in current prices of highly consumable goods. We should see oil, gas and energy prices stabilize first.

Rents will likely increase for another three to six months, then stabilize (and, in my opinion start to fall late summer).

Housing overall is far more challenging as mortgage rates are climbing. Refinancing as a method to bridge the income gap between wages and expenses is a big problem now in this phase. There is going to be a period of massive fluctuations and instability in the housing market depending on region and employment stability as the recession phase of the total economy is going to bite hard.

For most regions with mixed blend underlying economies (products and services) macro housing prices have peaked in the last 15 days. For ordinary housing purchases, not institutional investments, we should start to see price decreases again as the customer base for high prices shrinks. Obviously, this is driven by inventory and regional specifics; however, I am talking in the aggregate within the macro housing situation.

Food prices still have some upward pressures through Memorial day. Then a period of stability will settle, before the third wave of food inflation hits later in the summer/fall of this year; that’s when the increases in farming costs will reach the fork.

Late summer and fall food prices will likely be 15 to 20 percent higher than current prices at the supermarket. The fresh foods will be on the upper side of the future price wave, and the processed foods on the lower end; however, both will increase.

The last factors in the food price are far more challenging to predict…. Supply? Any problems within the food production cycle that impacts supply will drive prices, beyond what we already expect. If there are major shortages, the prices will go even higher.

This food environment is unfortunately the best time for Big Agriculture, the Wall Street multinationals, to make the most profit. The Big Ag multinationals will exploit every possible angle within inventory, supply and harvest controls to maximize their profit equation. There are a great deal of unknown global variables right now that could impact U.S. food prices later this year. The only certainty is that prices will further increase.

Joe Biden sucks.

.

Footnote, pray for good weather and stability this summer. If it is an active hurricane season, gasoline, oil exploration and refinery issues will make matters worse. The southern coastal areas, especially Florida, Louisiana and Texas need a non-dramatic summer.

QUESTION #1: Now that Canadian banks have proven themselves completely compromised by Trudeau and his bootlickers, is there a “safer” haven for $CAD? US$ accounts held by Canadian banks are available but are they really any better?

D

QUESTION #2: Dear Mr. Armstrong, Thanks to your Blog I learned a long time ago that Europeans should get their money out of Europe while they still can (into USA). I did that, but now the Wells Fargo bank asked me to close the account. Apparently because since Biden’s new government came to power a new Federal law requires now all banks (including in Florida) to get proof of a residence in the USA. I can not even enter the USA anymore because I’m not vaccinated. Could you please help? What can we do now? Thank you.

FV

ANSWER: I believe a European/Non-American can open an investment account such as a money market in the United States. I know that Merrill’s money market is done through a specific group at Merrill that only works with international clients. They then report back to your home country where you have an account. The hunt for money is really global now.

The US is already starting to cooperate with Europe given the capital flows to the US in the wake of the stupidity over Ukraine. As long as the West continues to fill the pockets of Zelensky, who is now believed to have $850 million stashed offshore, then there is no resolution. Zelensky has no incentive to negotiate an end to this as long as arms and money pour into Ukraine. Let Donbas go with Crimea, which is Russian anyhow, and stop pushing for World War III. The West simply wants war with Russia, or they would not be sending arms to Ukraine and pushing Zelensky to settle.

For now, the capital flows are pointing to the dollar as the safe haven given the prospects of war in Europe. This trend appears to be in motion into 2024. Thereafter, we have the risk of a global war on a grand scale.

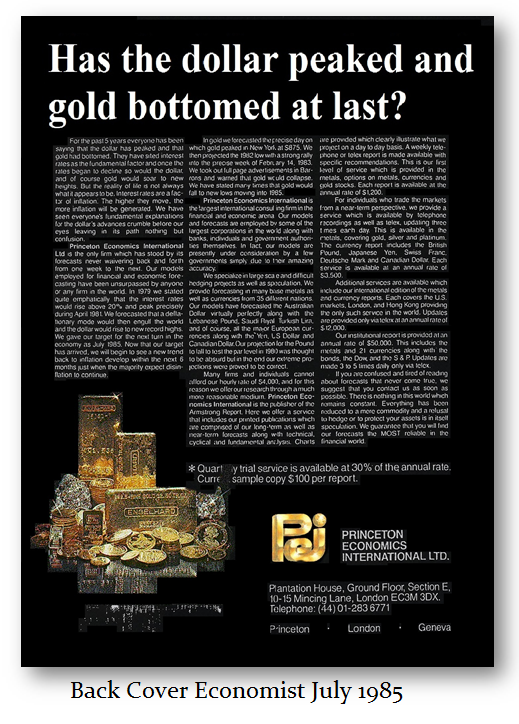

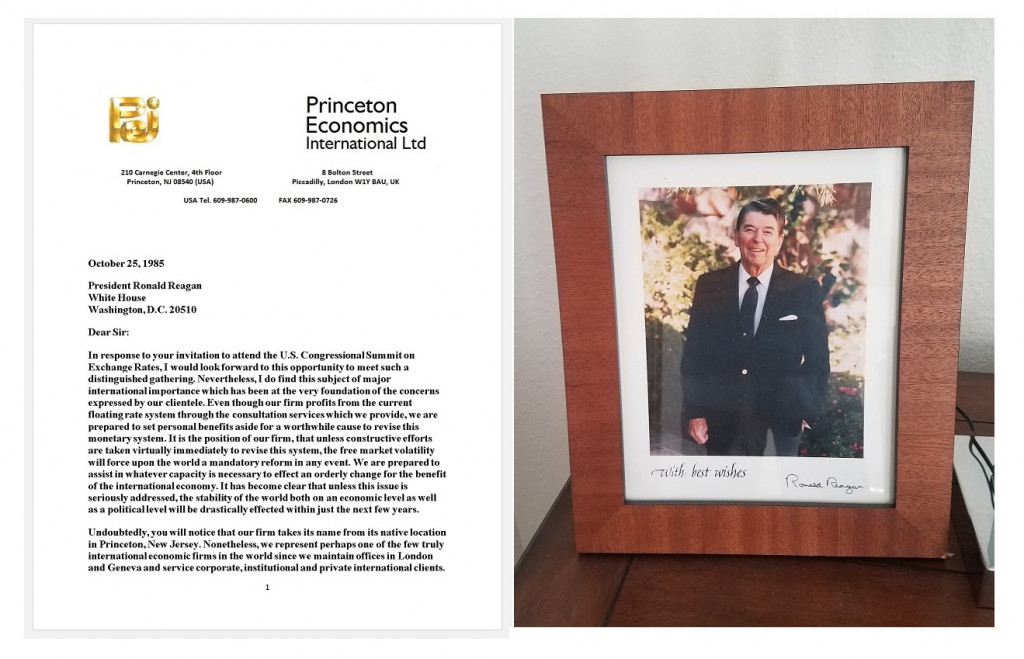

Once upon a time, I use to respect The Economist. I even took the back cover in July 1985 to announce that the Economic Confidence Model was beginning a new 51.6-year Cycle that was a Private Wave that would ultimately peak in 2032. I boldly announced the bottom in gold and the peak in the dollar taking the back cover every week in July 1985.

The Economist just released its cover article sadly demonstrating that the publication remains in the Dark Age of economics. They began:

“Central Banks are supposed to inspire confidence in the economy by keeping inflation low and stable. America’s Federal Reserve has suffered a hair-raising loss of control. In March consumer prices were 8.5% higher than a year earlier, the fastest annual rise since 1981. … It is the Fed, however, that had the tools to stop inflation and failed to use them in time.”

To say I am shocked at their reporting that is no better than a first-semester student in Economics 101. It reflects a complete lack of comprehension of how the economy even functions and adopts the politician view that they are NEVER responsible for inflation – it is always the central bank.

Clearly, they have not bothered to take notice that something major took place with the fall of Bretton Woods in 1971. Previously, the theory was if you borrowed, that was less inflationary rather than printing more money. Of course, that was a throwback to the days of Gresham’s Law when currencies traded in Amsterdam were based not on political-military power, but on the pure metal content. The debasement of the coinage by Henry VIII led to (1) the higher-based coinage being hoarded and (2) the decline in the value of English coinage trading in Amsterdam.

That theory became the Quantity of Money Theory which today is totally obsolete yet that is what we hear all the time when the Fed increased its balance sheet and therefore it should have been inflationary following 2008 but the Fed and other central banks could not create 2% inflation. That even led to some claiming MMT (Modern Monetary Theory) proves that the creation of money is NOT inflationary.

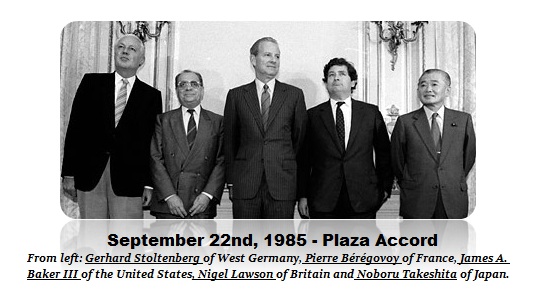

It was barely two months after we announced the beginning of a Private Wave in the Economist in July 1985 that in September 1985, the central banks were all called together and formed the G5 and then proclaimed that they wanted the dollar lower by 40%. This was James Baker’s brainchild that manipulating the dollar lower would reduce the US trade deficit and create jobs.

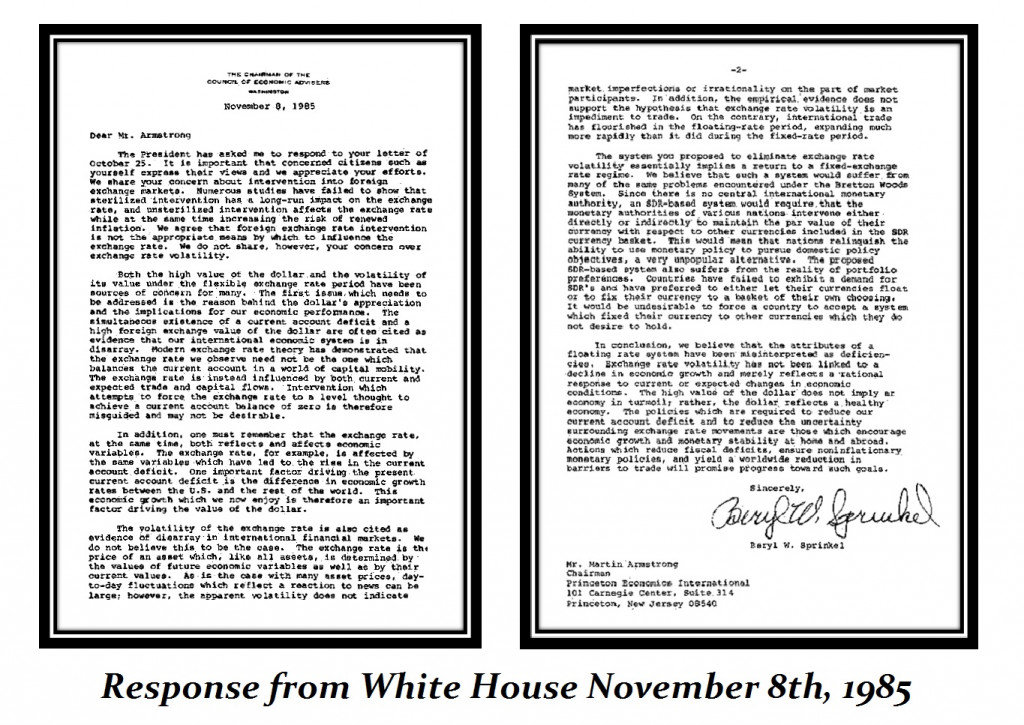

I was summoned to be among the global experts who solicit advice but never listen. It is always a dog & pony show so they can pretend they summoned the top experts in the world and then announce what they intended to do anyhow. Of course, it is always pretended to be based on independent advice. However, that is just not how Washington or any government functions. So I wrote to President Reagan and warned that devaluing the dollar to reverse the trade deficit would lead to a crash.

The present ordered Beryl Sprinkel who was the 14th Chariman of the Economic Advisers to the President (1985-1989) to respond. It had been the rise in interest rates to 14% under Paul Volcker to reduce inflation that led to the Deflation. Capital poured into the dollar for the high-interest rates which peaked precisely with the previous ECM wave in March 1981. Thereafter, the dollar soared driving the British pound down to $1.03 in 1985.

Clearly, the entire theory that the Economist is still clinging to currently is unsupported by the historical evidence. The raising of interest rates to stop inflation led to the explosion of the national debt thanks to the servicing costs. In 1980, the national debt stood at $907.7 billion. By 1989, the debt reached $2.857 trillion. The raising of interest rates created deflation near-term but expanded the inflation longer-term.

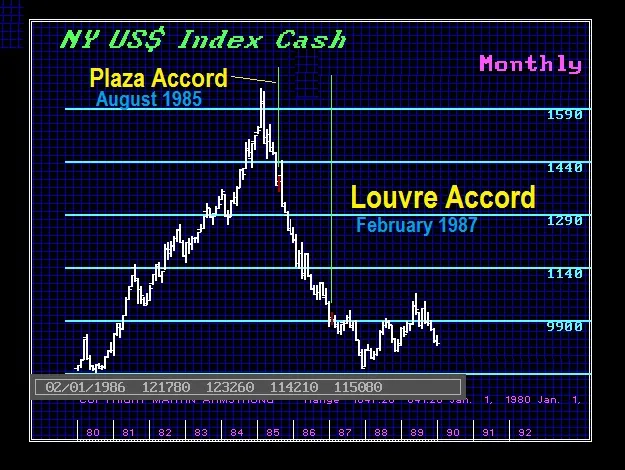

The Plaza Accord set in motion the 1987 Crash. They failed to understand that lowering the value of the dollar may have made US goods appear cheaper overseas to reduce the trade deficit, but at the same time, it also devalues all the US assets in the eyes of foreign investors. After selling more than one-third of the US national debt to the Japanese, the lowering of the dollar by 40% would mean a 40% loss on their holding of US debt.

As the dollar began a free-fall, the central banks began to realize this was a mistake. The Louvre Accord was an agreement, signed on February 22, 1987, in Paris, that aimed to stabilize the international currency markets and halt the continued decline of the US Dollar caused by the Plaza Accord. The agreement was signed by France, West Germany, Japan, Canada, the United States, and the United Kingdom. Italy declined to sign the agreement. The Group of 5 became the Group of 7 – G7 (now G20).

The G7 meeting of central bankers and finance ministers in Paris announced that the dollar was now “consistent with economic fundamentals.” They announced that they would only intervene when required to ensure foreign exchange stability. The objective was then to manage the floating currency system.

Democrats gained control of Congress in 1986 and immediately called for protectionist measures. The dollar depreciation agreed to in 1985 at the Plaza Accord, failed to really improve the trade perspective. In 1986, the trade deficit actually rose to approximately $166 billion with exports at about $370 billion and imports at about $520 billion. The object of manipulating currency to try to create jobs and alter trade flows proved to be completely false.

My concerns warning the White House that volatility would increase made back in 1985 were materializing. What they did not understand was that lowering the dollar in value also led to a shift in capital flows and the selling of US assets. Foreigners were suffering losses by financing U.S. trade by purchasing United States Treasury bonds in an attempt to ease the trade deficit criticism. We were advising the Japanese to buy gold on the New York COMEX, export it, and then resell which would also make it appear that the US exports were increasing. However, the lower dollar was then resulting in the importation of inflation into their own nations.

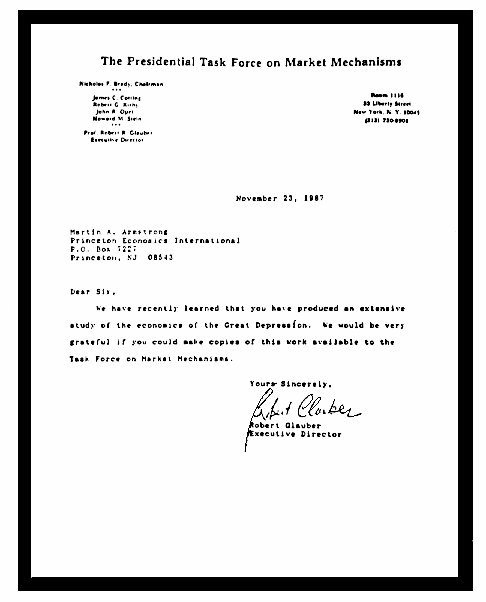

The press back then never understood the crash. I was called in by the Brady Commission charged with investigating the causes of the Crash. Of course, they would not blame the government. The best I could do was to prevent a witch-hunt on Wall Street and the final report casually mentioned that they believed foreign exchange had something to do with it.

There is probably nobody else who has dealt with more central banks than me from China to Switzerland and into the Middle East. To read this cover story by the Economist was indeed shocking. They are obviously still under the impression that inflation is the result of the rise and fall of the money supply that dates back to the days of Henry VIII. I dare say, things have changed slightly.

Today, governments have borrowed relentlessly. But the debt is acceptable now as collateral so national debts are simply money that pays interest. That is completely out of the scope of the central bank so it DOES NOT have the tools to prevent or create inflation. The politicians always want to spend whatever it takes to win the next election and then blame the central bank if it resulted in inflation. It is a sad day that the Economist is so out of touch its rambling and that of someone serious out of touch with reality.

The lockdown in Shanghai has caused immeasurable damage to the people and battered an already stunted global supply chain. The wealthy are now fleeing the city, as numerous agencies have reported a large uptick in immigration requests. The Financial Times reported a 7-fold increase in the search term “immigration” among residents.

The media has downplayed this story as they do not want the people to remember governments’ capabilities. As with the fall of many great cities, the wealthy are the first to leave. Shanghai may be one of the richest cities in China, but it is not immune to government tyranny.

Only 25 deaths in Shanghai were attributed to the coronavirus, but over 25 million people directly suffered from this lockdown. The lockdown was not about safety. Warehouses are beginning to open, but the world’s largest port ceased operations. Again, no world leaders commented heavily on these major issues.

Pets of the “infected” were eliminated by the government. There were reports of people jumping from high rises and others begging the police to take them to jail with the hope of having a meal. No world leaders have commented on these human rights abuses as they were done in the name of COVID.

Fannie Mae forecasts a “modest recession in the latter half of 2023” and believes the house-buying frenzy will begin to cool in the US. The Federal Reserve’s hawkish direction to curb inflation has led the agency to believe that a “soft landing” for the US economy is unlikely.

“With the most recent inflation readings at levels not seen since the early 1980s and wage growth exceeding that which is consistent with a 2-percent inflation objective, we believe the odds of a soft landing are even lower. Returning to the Fed’s policy target, therefore, likely necessitates economic growth slowing sufficiently to lead to a rise in the unemployment rate, which would cool wage and price pressures.”

Naturally, they see mortgage rates rising. Home sales for 2022 are now predicted to decline 7.4% compared to their initial forecast of 4.1%, while sales in 2023 are expected to decrease by 9.7% (initial projection: 2.7% decline). Adjusted for inflation, Fannie Mae sees house price growth approaching 0% by the end of next year.

Mortgage credit is not a factor as it was during the Great Recession and the checks and balances are in place after the 2008 scare. New construction is also expected to help with the “eventual recovery” as there is a lower inventory relative to demographic demand. Mortgage rates are now hovering around 5% after rising 1.95 percentage points since the December low. A similar spike in mortgage rates occurred in 2013 and 2018 and led to a downturn in home sales.

Interestingly, Fannie Mae has specified that the coming “modest recession” is “COVID-driven” and even admitted that the business cycle is at play:

“We have previously posited that the current business cycle would likely be shorter than those of the past few decades. GDP growth surged in 2021 after the relaxation of many COVID restrictions – also supported by historic income transfers and monetary policy easing – which led to a swift recovery but also planted the seeds of inflation. Therefore, despite only two years having passed since the COVID-driven recession of 2020, the economy has already moved into what could be described as the mature stage of the business cycle. Specifically, the unemployment rate is below the “full employment” level, inflation is accelerating as growth slows, and the Federal Reserve is beginning to tighten policy. These conditions typically mark the beginning of the end of an economic expansion.”

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending