September 6, 2019

White House Economic Council Chairman Larry Kudlow discusses the August jobs report and the latest on China trade negotiations. Main Street USA is thriving, and the U.S. economy is very strong.

White House Economic Council Chairman Larry Kudlow discusses the August jobs report and the latest on China trade negotiations. Main Street USA is thriving, and the U.S. economy is very strong.

The Bureau of Labor Statistics released the August Jobs Report showing 130,000 jobs added during the month. Year-over-year wage growth remains 3.2%, with a very strong three month wage growth showing gains of 4.2%.

Overall the top line growth of 130k jobs sounds modest; but jumpin’ ju-ju bones, the data underneath the top line is extremely strong and highlights exactly why wage rates have been rapidly increasing over the past three months. [Table A – BLS Report]

With a tight labor market we are seeing the natural upward pressure on wages. In the past four months wage rates have increased 4.2% [Table B-3], and from the employment data it appears those large wage incentives are bringing people back into the workforce.

Year-over-year the number of employed Americans has grown by 2,274,000 people.

Trump War Room

Trump War Room✔@TrumpWarRoom

CNN’s Christine Romans: “More than 500,000 people entered the labor market…that is an important sign of success in the labor market right now.”

Published on Sep 4, 2019

Published on Sep 4, 2019

This is another one of the rare interviews where an American CEO calls out the specifics of how Wall Street greed created the China problem that pummeled Main Street.

Cambria CEO Marty Davis discusses the root of the trade issues with China and President Trump’s efforts to address the problem. He accurately calls attention to the origin of the issue; and then brilliantly explains the current consequences of decisions made by an alignment of Wall Street interests and powerful U.S. politicians.

CTH readers will notice a significant amount of similarity in the words and phrases Mr. Davis uses to describe the issues. This guy gets it.

This is well worth nine minutes of your time. Mr. Davis really gets it, and is not afraid to call the baby ugly. His criticisms are so spot-on accurate they made Maria Bartiromo uncomfortable in broadcast. These things are usually not said. Must Watch:

Boy howdy if ever there was an article that showed the layers and ramifications of President Trump’s global trade reset, this is a good one. The multinational media do not want American voters to understand the dynamic, because if we did people would catch-on to how the global economy was structured upon removal of U.S. wealth…

Reuters is reporting on a significant drop in German industrial orders, and they specifically point to diminished orders from the U.K (small part) and China (big part) as the cause. However, the analysis stops at the part where China’s lack of industrial orders is the leading contribution to retraction in the German export sector.

What the financial analysis does not approach (ie. the third rail of multinational corporate admission that must never be outlined), is the reason why Chinese orders for German industrial goods have dropped.

The problem for China, and ultimately for Germany, is that Trump’s trade reset has stopped a big amount of U.S. wealth from arriving in Beijing. Simultaneously, Beijing is countering Trump’s tariffs by devaluing their currency. The rebound economic impact is doubled. China has: (1) less income; and (2) less value within their own currency.

Where does this dynamic show up?…. Anytime China is going to buy something.

China’s currency devaluation makes their exports cheaper; however, at the same time it makes any of their imports more expensive. As a consequence China buys less… and that now exhibits in lower purchases of German stuff. See how that happens?

So yeah, the ramifications for Merkel’s German economy -twice as bad as originally forecast- are based on China fighting Trump. The fact that China is bleeding cash, and has simultaneously dropped the value of their currency, means China can’t buy stuff.

All of those nations who were counting on Chinese purchases are now going bananas. This is why the multinationals blame Donald Trump… and to make matters even worse – the U.S. economy is thriving, while they watch from the sidelines. It’s a delicious dynamic.

For more than three decades global economies have grown by removing wealth from the United States. The U.S. multinationals have countered the economic arguments by claiming those global economies have purchased U.S. treasuries; but that means we trade our current wealth for future debt.

President Trump has reversed this dynamic. We are repatriating our national wealth through new trade policies, and will pay for any incurred foreign debt by expanding our own economy and controlling our own destiny.

Here’s Reuters article (emphasis mine):

BERLIN (Reuters) – Weaker demand from abroad drove a bigger-than-expected drop in German industrial orders in July, suggesting that struggling manufacturers could tip Europe’s biggest economy into a recession in the third quarter.

Germany’s export-reliant economy is suffering from slower global growth and business uncertainty caused by U.S. President Donald Trump’s ‘America First’ trade policies and Britain’s planned, but delayed, exit from the European Union.

Contracts for ‘Made in Germany’ goods fell 2.7% from the previous month in July, data showed on Thursday, driven by a big drop in bookings from non-euro zone countries, the economy ministry said. That undershot a Reuters consensus forecast for a 1.5% drop.

“The misery in manufacturing continues. The decline in new orders significantly increases the risk of a recession for the German economy,” VP Bank analyst Thomas Gitzel said.

Germany’s gross domestic product contracted by 0.1% quarter-on-quarter in the second quarter on weaker exports, with the decrease in foreign sales mainly driven by Britain and below average demand from China.

“The danger is great that negative growth will also be recorded in the third quarter,” Gitzel added. (read more)

CTH readers are well versed in the dynamics of the Panda mask -vs- Dragon motives of China. Therefore we are able to discuss events without the MSM financial filter; which is narrated specifically to the benefit of multinational interests. Always keep that in mind.

Everything needed to understand the latest panda narrative from Beijing is identified in this simple paragraph:

(Beijing) […] The talks were supposed to have resumed this month but China’s commerce ministry said Vice Premier Liu He, Beijing’s pointman on trade, agreed to October in a phone call with US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin on Thursday. (more)

First, anything from Vice Premier Liu He is panda-speak; he is a tool in the process of Chinese narrative engineering. All former trade negotiation authority held by Liu He was stripped by Chairman Xi Jinping. Commerce Minister Zhong Shan is the real voice of Xi and the Beijing authority.

Second, what exactly is Beijing selling? An “October phone call”…. and that manipulates markets for the multinationals on Wall Street. A friggin’ announcement of a phone call?

Beijing is attempting to stop the financial bleed; the organization and planning of exits from the Chinese manufacturing system. Notice the U.S. media ran to the typeset pushing quoted reports from Beijing, not quoting reports from the USTR office or U.S. trade team. Again, the quote from the Associated Foreign Press (AFP):

…”China and the United States will resume trade talks in Washington in early October, Beijing said on Thursday”…

President Trump will not block, refute or diminish, this specifically sold Beijing narrative because it increases the U.S. stock market valuation. However, no-one who really pays attention to the dance should put any weight behind the announcement. It’s pure panda.

The U.S. position is the same. U.S. interests doing business in China should ‘get out’. Those who choose to remain in China; and/or those who choose to join with Beijing in selling false-hope in a temporary effort to prop up their multinational stock values; will eventually run into the brick wall of reality.

We can discuss this here, because the dance has been so visible for so long we know the music before it plays…. ie. ‘conduct your affairs accordingly’.

Today’s jump in the stock market; the part centered around this announcement from Beijing; is based on a false premise.

Beijing is bleeding cash. Beijing is attempting to get to 2020 and will deploy all resources to eliminate President Trump. Beijing is trying to save their economic model and stop the exodus from their manufacturing base.

There will be no U.S-China trade deal.

Any U.S. corporation who makes a decision based on the false-hope implied in the Chinese messaging is going to hit a world of hurt when it all comes crashing down.

Don’t expect any sympathies from these pages.

ADP Payroll analysis for August reflects continued strong gains in the jobs market beating all expectations from the financial pundits. The official government stats will be released tomorrow (private and public sector); in the interim the ADP payroll of private sector job creation shows that Main Street continues to be very strong.

(Reuters) U.S. private employers added 195,000 jobs in August, above economists’ expectations, a report by a payrolls processor showed on Wednesday.

Economists surveyed by Reuters had forecast the ADP National Employment Report would show a gain of 149,000 jobs, with estimates ranging from 110,000 to 175,000.

Private payroll gains in July were revised down to 142,000 from an originally reported 156,000 increase. The report is jointly developed with Moody’s Analytics.

The ADP figures come ahead of the U.S. Labor Department’s more comprehensive non-farm payrolls report on Friday, which includes both public and private-sector employment. (more)

CTH would advise not to place too much emphasis on negative ISM manufacturing order index statistics now that a complete U.S-Global trade reset is underway.

Right now global supply chains are in a state of flux as manufacturers are moving production based on tariffs and geopolitical issues.

As the component manufacturing is moving from one place to another; and as manufacturers evaluate their supply chain stability; there are going to be swings in purchase orders based on shifts in production facilities. This is an expected dynamic that is necessary if President Trump is to succeed in pressuring product manufacturers to move operations.

The multinational Wall Street media will hype any downward component manufacturing fluctuation during this process, but the fluctuation itself doesn’t speak to any lessening of demand; merely shifted operations and shifting contracts (ie. purchase orders).

The internal U.S. economy is very strong. It’s the U.S. companies, multinationals, that rely on external operations for their end-product production income that are tentatively positioned.

Main Street is thriving; Wall Street is in flux. This is the exact opposite of two prior decades where Wall Street was thriving and Main Street was in flux. Why?…

Because Trump!

Prime Minister Borris Johnson had wanted an election on October 15, but Labour and other opposition MPs would not back the move while the option of a no-deal Brexit on October 31 remained open to the PM. The House of Lords said it would pass the legislation by Friday.

The British pound rallied on the defeat of the PM clinging to the notion that leaving the EU is somehow bad for Britain. It remains the same old dire predictions they used back in the nineties when Britain was not going to surrender the pound and adopt the euro.

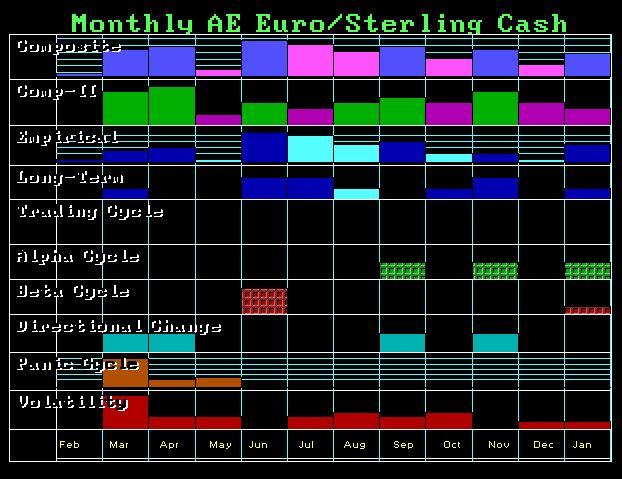

While our models indeed pinpointed a Directional Change with rising volatility into the week of 9/16, the pound has held the October 2016 for now, but a close for September below 12350 keeps the pound in check.

This idea of trade being so important is really quite insane. Nevertheless, Trump has not helped by trying to create jobs with his trade negotiations. China will listen to the US news which will show Trump losing 2020 even if you put a monkey up as the Democratic candidate. The press is so against Trump that they will turn this trade issue into real insanity. Likewise, this aids those in Britain desperate to keep their perks and pensions in place so they are selling out Britain for personal gain using the same issue as trade.

So far the Euro/Sterling Cross has been following the forecast array perfectly. The low was March followed by the breakout May/June with a Directional Change due in September. The next target is November followed by January.

What is very clear is that the financial markets are far more afraid of Labour taking power than BREXIT. We do not see any reversal of fortune for the pound and its long-term decline before 2021. Labour has become extreme. They will most certainly destroy the capital formation in Britain perhaps once and for all.

QUESTION: Do you think that Cambridge Analytica actually had any influence in creating BREXIT given the controversy that they were hired but then not? Can such influence actually change elections?

DK

ANSWER: As Nigel Farage noted at our Rome WEC in early 2019, our computer forecast BREXIT when nobody else did. Our computer does not even look at polls nor does it have any way of influencing the masses. Its sole input is economic trends globally which includes all the various trading free markets. That said, the real question is are we deluding ourselves that the media or firms such as Cambridge Analytica can even influence people to start with?

I have told the story how at the very day of the top in interest rates back in 1981, my mother and her sister went to the bank and bought 10 year CDs paying 20%. They never asked me. There was never a discussion between me and them regarding interest rates. All on their own they went to the bank and locked in money for 10 years. I then asked them why they made that decision? They said at 20%, they didn’t think they would see that high of a rate again.

The average person is driven more by what they see and feel on the street than in the news. All the stats show that less than 60% of adults even bother to watch the news. It has been declining with about 50% of U.S. adults now get news regularly from television, which is down from 57% a year prior in early 2016.

Our computer forecasts the start of what we called Big Bang that began 2015.75. That was more than just the beginning of crazy negative interest rates and the start of the Sovereign Debt Crisis, which is becoming painfully obvious at the state and local levels. The crisis will expand into the federal levels probably around 2021-2022 in Europe and then Japan. Back in 1985, we also warned that the 2016 election would be the first time a third party could possibly win the presidency. Well, that was clearly the Trump Revolution. How was this forecast even possible? The start of this Economic Confidence Model wave was 1985.65. Add Pi, 31.4 years, and we come to 2017.o5 to the day that Trump was sworn in.

Our computer forecasts the start of what we called Big Bang that began 2015.75. That was more than just the beginning of crazy negative interest rates and the start of the Sovereign Debt Crisis, which is becoming painfully obvious at the state and local levels. The crisis will expand into the federal levels probably around 2021-2022 in Europe and then Japan. Back in 1985, we also warned that the 2016 election would be the first time a third party could possibly win the presidency. Well, that was clearly the Trump Revolution. How was this forecast even possible? The start of this Economic Confidence Model wave was 1985.65. Add Pi, 31.4 years, and we come to 2017.o5 to the day that Trump was sworn in.

This pi interval is where political change often takes place. In the wave which peaked in 1929, the start was 1882.45; add pi and we arrive on November 6, 1913. That was the precise day that Mohandas Karamchand Gandhi (1869-1948) began the decline of the British Empire.

This pi interval is where political change often takes place. In the wave which peaked in 1929, the start was 1882.45; add pi and we arrive on November 6, 1913. That was the precise day that Mohandas Karamchand Gandhi (1869-1948) began the decline of the British Empire.

By the end of World War I which began the next year, the United States had displaced Britain as the financial capital of the Western world.

The next wave began 1934.05 (January 17/18). It was precisely the 17th when the German salute of raising the right hand was introduced by the Prussian Economic and Labour Ministry. Then on the 24th of January, Alfred Rosenberg became the ideological supervisor of the Nazi Party. It was Rosenberg who pushed the anti-Semitic and racial ideologies using what Hitler had written in ‘Mein Kampf’ as the basis for his ideas.

While Hitler expounded his own ideas, there is little doubt that he was influenced by some of Rosenberg’s beliefs. Hitler would not achieve full dictatorial power until after the death of Hindenburg in August 1934. It took just 17 days thereafter when Hitler combined the office of President and Chancellor while the army swore a pledge to Hitler personally rather than to the nation.

These Pi intervals mark the beginning of a political change. Manipulating the people does not create these changes. It is the economics behind the events. The harsh reparation payments on Germany and punishing the people for their leaders in World War I only set the stage for Hitler. It is ALWAYSeconomics which create political change. It was 1933 which not only brought Hitler up in Germany but FDR in the USA and the New Deal as well as Mao in China.

The computer in its forecasts would never be able to accomplish these results if it relied upon opinion polls which are often wrong. The way to influence people is economics. CNN and its fake news are preaching to those who would never vote for any Republican. The pools were all manipulated for both BREXIT and the 2016 election. Our computer is the ONLY forecast that got both correct without human opinion – just economics. Why do you think the press will NEVER report our forecasts? They want opinions not a computer.

What I have learned is straight forward. Given a specific time interval, humans will simply respond in the same manner consistently. Government abuses their power and over-tax and over-regulate in a quest to maintain control. In that process, they inevitably seal their own fate and thus governments die by their own hand. There is simply no exception. Undermine the economy and everything else will change accordingly.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending