QUESTION: Didn’t gold decline from 1980 to 1999 because of all the dumping of gold by central banks?

WV

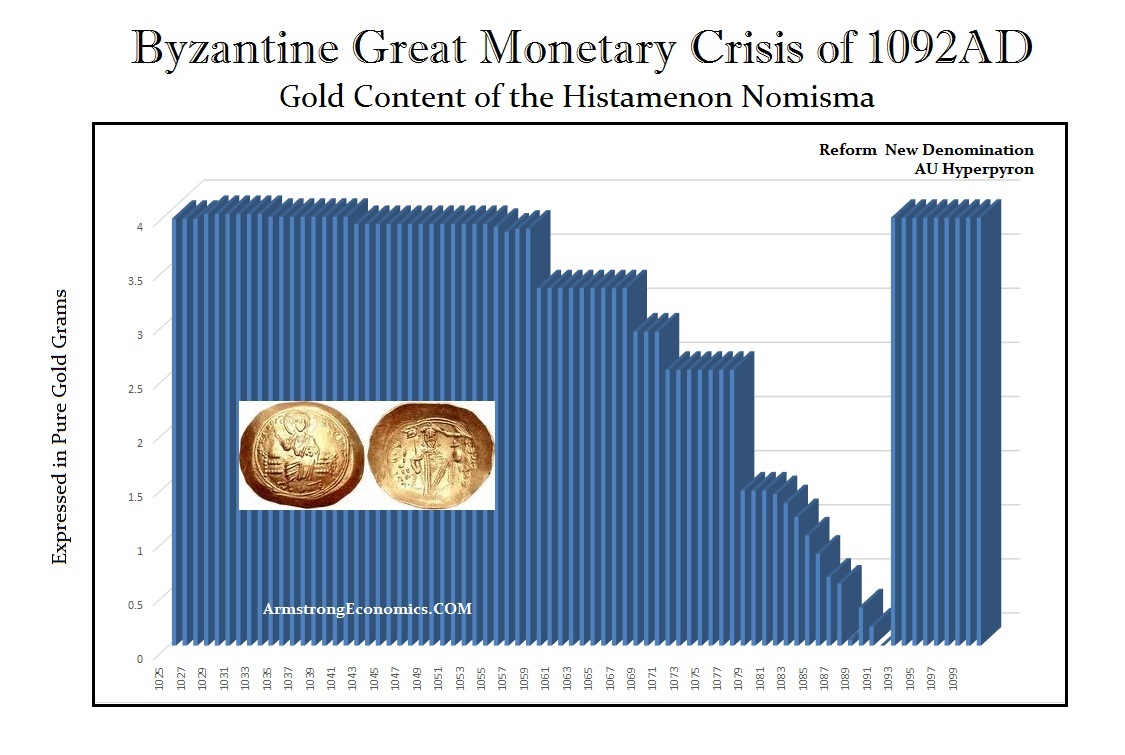

ANSWER: I understand that the quantity rise, in theory, makes sense that the price would decline. But historically, there is no evidence that supports that theory on a consistent basis. There are times when the supply has increased and so has the price. During the Byzantine Empire, confidence in the government began to collapse especially during the monetary crisis of 1092. As people hoarded their gold, the government was forced to debase the coinage even more. When people do not trust the future, they will hoard their wealth. You must understand that all things NEVER remain equal.

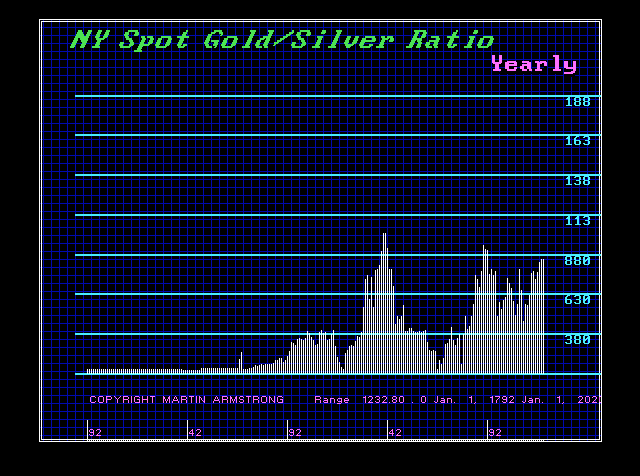

This is also why the silver-to-gold ratio fluctuates. NOTHING is ever permanent. We must remember that because it is when the collapse in government takes place, an increase in supply will never satisfy the demand.

Posted originally on the CTH on January 1, 2023 | Sundance

Abraham Lincoln once said, “No man has a good enough memory to make him a successful liar.” Lincoln somewhat underestimated the Mike Morell types of the world, who have become liars as a profession. {Direct Rumble Link}

Mike Morell was the former acting CIA director in the aftermath of Benghazi when General David Petraeus was removed from the position. Morell is a Clinton crony who not only constructed the infamously fabricated talking points used by Susan Rice to blame the Benghazi attack on a YouTube video, Morell was also the guy moved into position to protect Clinton in the aftermath of the terrorist attack, and then years later in July 2016 the same Mike Morell penned the first Trump-Russia thesis in the New York Times.

After successfully doing his job to protect Clinton in the aftermath of Benghazi, Mike Morell was hired by CBS President David Rhodes. Obama’s Deputy National Security Advisor Ben Rhodes is David’s brother. Mike Morell now continues to work for CBS and today he declared a likelihood that a “U.S. or western interest” is likely to be attacked by an al-Qaeda affiliate in 2023.

Posted originally on the CTH on January 1, 2023 | Sundance

This is an interesting interview in that International Monetary Fund Globalist Director Kristalina Georgieva seems to be laying the landscape for some truthful economic news to surface on the geopolitical level; albeit keeping up the globalist pretenses around western collective energy policy.

One of the more important points Mrs. Georgieva hits on is the reopening of China, from district level COVID bubbles as a containment feature, and the likely impact it will have on global supply chains. Mrs. Georgieva is correct on this issue.

China continued operating their industrial manufacturing base (despite COVID) because they built strict covid isolation bubbles around their industrial sectors geographically. However, with China lifting those isolation bubbles, there is a great potential for the manufacturing sectors to be hit hard by short to medium term virus outbreaks. This could/will have the potential ripple effect of global supply disruptions.

In an ironic twist, ‘deglobalization’ is now a 2023 catchphrase as various nations realize having their supply chains both dependent and interconnected is not good when there are interruptions. A new discussion centering around being dependent on China is the specific issue now being raised. However, the globalists are isolating their viewpoints only to raw material resourcing and development. WATCH:

[Transcript] -MARGARET BRENNAN: I want you to take us around the world and kind of us give us that global view. Let’s start in China. China has been this hub of cheap manufacturing for the world, we are all so dependent on it but right now it looks like COVID cases are exploding as they start pulling back those zero COVID restrictions. What will that mean for the global economy Longterm and short-term?

GEORGIEVA: In the short term, bad news. China has slowed down dramatically in 2022 because of this tight zero COVID policy. For the first time in 40 years China’s growth in 2022 is likely to be at or below global growth. That has never happened before. And looking into next year for three, four, five, six months the relaxation of COVID restrictions will mean bush fire COVID cases throughout China. I was in China last week, in a bubble in the city where there is zero COVID. But that is not going to last once the Chinese people start traveling.

MARGARET BRENNAN: Because they also- they don’t have an effective vaccine right now.

GEORGIEVA: The- the vaccinations fall behind. They have not worked on anti-viral treatments and how that can be offered to people, and so they will go through this tough time. If they stay the course, and this is our advice, stay the course, over time they would be able to catch up with the rest of the world, both in terms of focusing their vaccinations, bringing mRNA vaccines into China, expanding antiviral treatment, and the economy would function. But for the next couple of months, it would be tough for China, and the impact on Chinese growth would be negative. The impact on the region would- would be negative. The impact on global growth would be negative.

MARGARET BRENNAN: Because this is the second-largest economy in the world, and we’ve learned how dependent the world is on the Chinese supply chain. So do you expect then, a domino effect? Will inflation get worse, because all of a sudden there aren’t workers healthy enough to go to factories in China?

GEORGIEVA: We expect that there would be counterweight from the sheer opening of the economy, because up to now, the biggest impact on global value chains came from restrictions due to COVID. When you close down a big city or a big port, the repercussions for the economy is- are significant. Now, we would have the impact of people getting sick, not going to work, but the economy would be open. So the expectations we have for China is to gradually move to a higher level of economic performance, and finish the year better off than it is going to start the year. But you’re absolutely right, the world has relied on China’s growth for a long, long, long time. Before COVID, China would deliver 34, 35, 40% of global growth. It is not doing it anymore. It is actually quite a stressful for the- for the Asian economies. When I talk to Asian leaders, all of them start with this question, what is going to happen with China? Is China going to return to a higher level of growth?

MARGARET BRENNAN: You’ve said that you fear that we are sleepwalking into a world that is poorer and less secure because of a split in the global economy between the US and China. What do you mean by that? Do you see efforts here in Washington to stop it?

GEORGIEVA: It is very easy to reflect on the benefits of the world being more integrated. When we look back over the last three decades, the world economy tripled because of this reliance on an integrated world economy. Who benefited the most? Emerging markets and developing economies, they quadrupled. But rich countries also benefited, they doubled in size of the economy. So we have to be careful not to throw the baby out with the bath water. Yes, the way we have operated created excessive dependency in global chains. We were too focused on costs, how can we make products cheaper. And COVID and then the senseless war Russia started against Ukraine has shown that this is not enough. We cannot just concentrate on what is cheaper. We have to think of the security of supplies and that means diversify the sources of products that make the economy function well, lifting up the level of cost. That economic logic is not only appropriate, it is a must to follow. But we shouldn’t go beyond. We shouldn’t say, okay, we break the world into blocks, one works here, the other one works there because the costs are very, very high. We calculated that just trade, limiting trade into two blocks, would chop $1.5 trillion from the global GDP year after year after year.

MARGARET BRENNAN: If you tried to separate the US and China?

GEORGIEVA: You separate- you separate them, there is an excessive cost. So the logic should be where for security reasons there has to be careful recalibration of supply chains, do it, but don’t go beyond- don’t go into benign areas of products that have no strategic significance but they benefit the US consumer, they benefit the world economy. And this is what we are arguing for, don’t go in a direction in which this separation would make everybody poorer and the world less secure.

MARGARET BRENNAN: So you’re telling Beijing and Washington, figure it out. You can’t be in conflict.

GEORGIEVA: What we have seen in Bali is an indication that this rationale–

MARGARET BRENNAN: You’re talking about the G20 meeting–

GEORGIEVA: The G20 meeting in Bali, when the two presidents, President Biden and President Xi Jinping, met, they spent three and a half hours discussing exactly that. Where is the point of contact that makes both countries better off? And where is that- that there are differences that cannot be bridged and therefore we have to keep them–

MARGARET BRENNAN: The US is trying to block some Chinese technology companies from doing business here. They’re taking measures that are drawing some pretty bright lines between the US and China. Is that tolerable?

GEORGIEVA: We always prefer countries to seek their common interest in economic integration. And when you start breaking the interactions that are based on fair trade, you harm your own people, you not only harm the- the Chinese and therefore it has to be thought through very carefully. Again, I want to be very clear, some diversification of supplies for the security of supply chains is necessary. COVID taught us this lesson, the war taught us this lesson. So the U.S. is right to look into some areas where strategically they need to guarantee the functioning of the U.S. economy without interruptions. But do that keeping in mind the interests of the American people that would like to still have prices moderating, and actually, when we think about prices, one good news we have for 2023 is that towards the end of the year, we do expect inflation to trim down. So don’t take actions that may be contrary to that trend.

MARGARET BRENNAN: But you are predicting inflation to slow to six and a half percent from about 7%. Is that right?

GEORGIEVA: Well, towards the end of the year, we- we project it would go even further down towards the end of 2023, provided central banks stayed the course. Our big worry is that with the economy slowing down globally, we are projecting global growth to go down to 2.7%, maybe even lower next year. Remember, 2021, it was 6%. It dropped to 3.2 this year, 2022. And it will continue to drop down if central banks get the cold foot and say, ‘oh, my god, growth is slowing down, let’s slow down the fight against inflation.’ We risk then inflation to be more persistent. So our message is to central banks, you have to see credible decline in inflation and only then you can think about re-calibrating rate policy.

MARGARET BRENNAN: One of your IMF researchers gave a pretty dire prediction. Overall this year, shocks will reopen economic wounds that were only partially healed post-pandemic. In short, the worst is yet to come and for many people, 2023 will feel like a recession. What do you need to brace for?

GEORGIEVA: The- this is- this is what we see in 2023. For most of the world economy, this is going to be a tough year, tougher than the year we leave behind. Why? Because the three big economies, U.S., E.U., China, are all slowing down simultaneously. The US is most resilient. The U.S. may avoid recession. We see the labor market remaining quite strong. This is, however, mixed blessing because if the labor market is very strong, the Fed may have to keep interest rates tighter for- for longer to bring inflation down. The E.U. very severely hit by the war in Ukraine. Half of the European Union will be in recession next year. China is going to slow down this year further. Next year will be a tough year for China. And that translates into negative trends globally. When we look at the emerging markets in developing economies, there, the picture is even direr. Why? Because on top of everything else, they get hit by high interest rates and by the appreciation of the dollar. For those economies that have high level of that, this is a devastation.

MARGARET BRENNAN: And I want to- I want to come back to you on that. And just to explain that for some of our listeners, a stronger dollar, it’s good for Americans when they go shopping abroad. It’s not good for poor countries who have taken out loans, for example, and borrowed money in dollars. And according to the IMF, 60% of low income countries are in distress because of this- this debt. So what does that look like? Do you- do you see governments collapsing with defaults? Does that bleed into the global financial system? I mean, how much of a contagion does this become?

GEORGIEVA: So far the countries that are in that distress are not systemically significant to trigger a debt crisis. Let’s just look at the map, which are these countries? Chad, Ethiopia, Zambia, Ghana, Lebanon, Surinam, Sri Lanka, very important for their people that we find the resolution to the debt problem, but the risk of contagion is not as high. However, if that list continues to grow, and let’s remember, 25% of emerging markets are trading in distressed territory, then the world economy may be for a bad surprise. And this is why at the IMF, we are working very hard to press for debt resolution for these countries and we have engaged the traditional creditors, the Paris Club, the non-traditional creditors, China, India, Saudi Arabia. I would call this very simple: urgency, we have to act. When I look at the- the debt of the world. Yes, we have to be concerned. During COVID, what did we do? Everywhere governments borrowed, rightly so, to help their people.

MARGARET BRENNAN: Money was cheap.

GEORGIEVA: Money was cheap, and we prevented a collapse of the world economy. That was the right thing to do. But once Russia invaded Ukraine and that added impetus to inflation, money is not- not cheap anymore. So what is the advice we give to governments? Focus on your budgets, make sure that you have sufficient revenues to collect and that you spend very wisely.

MARGARET BRENNAN: That’s good advice, but it’s not always easy politics to follow that advice, as you know–

GEORGIEVA: Of course it is not.

MARGARET BRENNAN: And so that’s why I want to- if- if you can explain for our viewers. You know, we spoke to the CEO of JPMorgan Chase, Jamie Dimon, recently, and he said he sees the global risk as explosive right now. He was saying things like migration, energy, national security, liquidity in the banking system, war, these are all the knock on effects of a government not being able to pay its bills and not being able to deliver for its people. Is that what you are seeing too?

GEORGIEVA: Well, what we’re seeing is the world has changed dramatically. It is a more shock prone world. The lessons we learned from the last couple of years are that no more we operate with relative predictability of what the future would bring. And these shocks COVID, the war, costs of living crisis, they compound their impact. What does that mean for governments? First and foremost, it means that we need to change our mindset towards more resilience, more precautionary actions. And at the IMF, this is what we tell our members. Act early, don’t wait until the problems deepen. And for those who need help, this is why we exist for the developing countries. The fund is a source of resilience and I am- I am very pleased that many of our members are coming to us. Just since the war started we got 16 countries coming for programs to the IMF, $90 billion in support for these countries. And right now we have 36 requests. So that acting early, when you see trouble, look for ways to strengthen your fundamentals, to have buffers to protect you and your people. This is the advice we give to governments. For those who don’t know the IMF, we were created from the ashes of the Second World War to stabilize the world economy. And at a moment like this, we come strong to help our members. My message, don’t think that we are going to go back to pre-COVID predictability. More uncertainty, more overlap of crises wait for us. Rather than crying for the time we had, we have to buckle up and act in that more agile, precautionary manner I described.

MARGARET BRENNAN: I want to make sure I get to Ukraine because I know we’re running out of time. You’ve said- excuse me- you’ve said the single most negative factor in the global economy is the war in Ukraine. And Vladimir Putin says this is going to go on for some time. President Zelensky said they need $55 billion in foreign support next year. He expects $20 billion from the IMF, is he going to get it?

GEORGIEVA: We are working on providing support for Ukraine. So far, out to the international financial institutions, we have provided the largest amount of financing for Ukraine, $2.7 billion in emergency financing, and we are working for 2023 to be a significant part of the support for Ukraine. I expect that sometime early in the year we will go to our board with the request. We have assessed the needs of Ukraine to range somewhere between three and five billion dollars a month. What Putin did with destroying critical infrastructure in Ukraine, this is horrific, and it means that in the next months the country would be more on the high end of this range because it is put in an awful position to have to restore access to electricity, to heat, to water. I have relatives in Ukraine. What I- what I know from them is it is cold, it is dark, and it is scary. Bombardments of civilian areas continue. What I also want to say is that Ukraine has proven to be remarkably resilient. Ukrainian economy is functioning. Pensions are being paid. When there is bombardment, restoration of energy, water, heat is done very quickly and we see revenues collected in Ukraine in a very disciplined manner to support the functioning of the country.

MARGARET BRENNAN: So the government’s not going to collapse?

GEORGIEVA: The government is very well functioning under incredibly difficult circumstances. No, they’re not going to collapse. And then the other thing that is so remarkable is actually the world has proven to be more resilient than we feared, a year in the beginning of the year. We look at the response to the energy shock in Europe, and Europe is moving towards independence from Russia decisively. Yes, there will be a tough winter, maybe the next one would be even tougher, but freedom from dependence on Russia is coming. It is going to be there.

MARGARET BRENNAN: I want to ask you two questions before we go. How do you describe the state of U.S. economics and politics?

GEORGIEVA: The US economy is remarkably resilient. Decision making in the US because of the way the political set is at the moment, it is more difficult. But nonetheless the US has taken some very important steps that are helping to the US economy. Like the child tax-

MARGARET BRENNAN: The tax credit. It expired.

GEORGIEVA: The credit that is it. It is contributing so significantly to reducing poverty in the US, like the infrastructure bill, like the Inflation Reduction Act. These are things that are bringing more dynamism in the US. Good for the US, good for the world. And of course staying on that course is going to be more challenging. But I do hope that the US is not going to slip into recession despite all these risks. We expect one third of the world economy to be in recession. And yes, as you said, even countries that are not in recession, it would feel like recession for hundreds of millions of people. But if that resilience of the labor market in the US holds, the US would help the world to get through a very difficult year.

MARGARET BRENNAN: And as I let you go, my final question is what leaves you hopeful in 2023?

GEORGIEVA: What leaves me hopeful is that I know when we work together, we can overcome the most dramatic challenges. In 2020, the world came together in the face of tremendous threat and was able to overcome this threat. In 2023 we have to do the same. And in this world of ours, of more frequent and devastating shocks, we have to hold hands, we have to work together. And my institution is there to bring together economic policymakers so we can be wise and persistent in the face of truly dramatic challenges we face.

MARGARET BRENNAN: Madam managing Director, thank you for your time this morning.

Posted originally on the CTH on January 1, 2023 | Sundance

The New Year brings a look of forward-looking economic perspectives from major financial institutions. Unfortunately, if the perspective of Bank of America Chief Economist Michael Gapen is reflective of the larger institutional analysis, the financial pretending is anticipated to continue.

[Side Note: Notice how they will all start talking about ‘deglobalization’ in 2023. There’s a reason for that that I will touch on in the IMF interview to follow]

Appearing on Face the Nation Gapen accurately indicates the U.S. housing market is already in a steep economic recession, housing prices falling rapidly with a considerable amount of distance to go (-30% range), and the overall housing market will likely be in this situation for around two years. On a macro level the Bank of America indicators line up with the general housing trajectory. From a lending standpoint, Gapen would have specific insight.

Beyond the housing sector, Mr. Gapen starts to get sketchy. He anticipates inflation taking 24 to 36 months to lower to the norm 2% range. That is generally in line with CTH expectations; however, nowhere in the analysis does Gapen even mention energy costs and the overall impact to the economy from energy policy. You will note this absence will be present in almost all financial punditries. Mentioning “energy policy’ as a cause of economic pain is a third rail amid his peer group; it is simply not permitted.

Astute readers will note the great financial and economic pretending that surrounds the Build Back Better and Green New Deal climate change agenda will not be discussed by anyone, ever. The massive price impacts, the supply side inflation pressures, are baked into the western global economic outlooks. It is strictly verboten to talk about climate change policy being stopped, modified, reversed or even, well, gasp, removed. WATCH:

[TRANSCRIPT] – […] BANK OF AMERICA CHIEF ECONOMIST MICHAEL GAPEN: Happy New Year as well. Thank you for having me on.

MARGARET BRENNAN: You know, a majority of voters polled by The Wall Street Journal say that the economy is going to look and feel worse in 2023. What is your forecast?

GAPEN: So I think that’s probably true. I think we’re in a situation where the risk of recession is high, may not be a deep and prolonged one. But we’re in a situation where the economy has recovered very rapidly from- from COVID, and it’s come with a lot of inflation. And the Federal Reserve is trying to slow down the economy, to bring inflation down. And in the past, more often than not, that’s coincided with some sort of recession in the US economy and the U.S. labor market. It’s not baked in. It’s not for certain. We may be able to avoid it, but I would agree that the outlook by most people who sit in the position that I do think 2023 could be a difficult year for the U.S..

MARGARET BRENNAN: So we may be able to avoid recession?

Gamazda Piano Published originally on Rumble on December 4, 2022

The Sound of Silence is what we will have at the end of World War III as we will all be gone if we can’t find a way to stop the Great Reset and the Build Back Better insanity of Klaus Schwab

There is an onslaught of misinformation about the Federal Reserve from everything that it can go bankrupt, and the Treasury will become a second central bank, and of course, the Fed is really the cause of inflation and its balance sheet. The proposal by Janey Yellen to buy in long-term debt and swap it with short-term is not “creating” money for the Treasury has no such power. It was a proposal for a debt swap to shorten the yield curve. The first proposition that the Fed can go bankrupt only suggests that people do not comprehend that the Fed is different entirely from the European Central Bank.

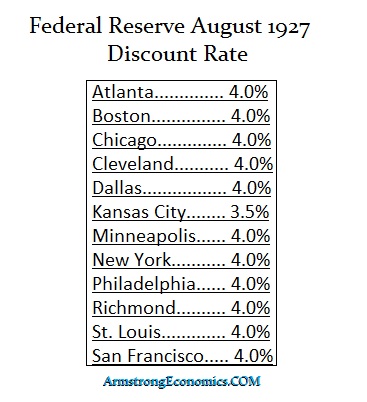

The Fed has the authority to create elastic money for it followed the very idea of J.P. Morgan and how he saved the economy during the Panic of 1907. The Fed can create money when there is a shortage due to economic contractions, and it can then reduce its balance sheet reducing the money supply. When the Fed was created, it was established with branches around the country because the Panic of 1907 exposed that there were regional capital flow problems. The 1906 San Francisco Earthquake drained the cash from the East where all the insurance companies were.

As we can see from this clip of rates in 1927, each branch was independent. There was an excess case in Kansas City so they lowered the interest rates there in hopes that capital would migrate to the other districts to earn more interest. All of that was eliminated by Franklin D. Roosevelt who wanted (1) to stack the Supreme Court to approve his Marxist agenda, which failed, and then he usurped all the power of the Federal Reserve and created the Washington headquarters and the President then was to appoint the head of the Federal Reserve and to illegally lobby him to ensure that his presidential agenda was to be the policy at the Federal Reserve. There was no more independence of the branches.

When Biden was running in 2020, he actually proposed requiring the Federal Reserve to regularly report on what they are doing to close economic gaps that exist along racial lines in the United States. Biden has viewed the Fed as a social tool and he has been making efforts to manipulate the Federal Reserve which will be extremely dangerous if they are carried out. Now, the Biden Administration is talking about closing branches of the Federal Reserve and replacing those board members with his hand-picked political cronies. In January 2022, he was pushing for black economists to be appointed to the Federal Reserve Board. My concern is that academics have ZERO experience and do not really understand the global economy trapped by domestic Keynesian Economics.

It was Paul Volcker who Chaired the Fed into the high in the interest rates back in 1981 who concluded in his Rediscovery of the Business Cycle that “it was not until the events of 1974 and 1975, when a recession sprung on an unsuspecting world with an intensity unmatched in the post-World War II period, that the lessons of the ‘New Economics’ were seriously challenged.” However, former Fed Chair Ben Bernanke has suggested that the Fed’s failure to contain inflation during the 1970s traced back to the political forces that shaped the Fed chairs in charge that he expressed in his book “21st Century Monetary Policy.” He wrote that the inflation of the ’70s puzzled economists relying on the 1958-ventage Phillips Curve, which would have predicted high inflation only in combination with extremely low unemployment rates. Bernanke admitted that the Phillips curve had “broken down” during the 1970s.

The critical problem with the entire way we view inflation rests on the QTM (Quantity Theory of Money) and the assumption that a mere increase in supply must produce inflation. There is absolutely nothing in the economic data that supports these old theories that were based upon (1) fixed exchange rates, and (2) the supply & demand theory dates back to the days of coinage. It was John Law who came up with the supply/demand theory that everyone else plagiarized, including Adam Smith. John Law’s writings influenced many, although they would never admit it. He was clearly the FIRST to use the term DEMAND and he was certainly the FIRST to join it with the word SUPPLY, for only a trader could have seen this connection in the price movements of anything.

The greatest fallacy of Keynesian Economics, Supply v Demand, and the Phillips Curve is that they have ALL failed because the US dollar is the reserve currency of the world and by default, the Federal Reserve has become the central bank of the world. With Biden desperate to get his hands around the neck of the Federal Reserve and force it to yield to his political agenda, threatens more than merely the US economy – but the entire world. Bernanke acknowledges in his book:

“Martin, my boys are dying in Vietnam, and you won’t print the money I need,” President Lyndon B. Johnson reportedly told then-Fed Chair William McChesney Martin Jr. at his Texas ranch after the central bank announced a half-point increase to its key discount rate over inflation fears, Bernanke writes. White House tapes, meanwhile, reveal President Richard Nixon frequently appealing to Fed Chair Arthur Burns’ Republican-party ties to clear the runway for more easy-money policies, with one call going as far as urging the Fed chair not to make any policy decisions that could “hurt us” in the November 1972 election.

I warned the Fed back then that buying in 30-year bonds during the 2007-2009 Financial Crisis, would NOT stimulate the domestic economy for one simple reason and this is why both the goldbugs and central bankers have been wrong. The domestic money supply DID NOT increase to stimulate when China was saying thank you very much and swapping their 30-year holdings for 10-year or less. The assumption that any central bank can control the domestic economy is absurd. The holdings of debt are global. Therefore, buying in 30-year bonds to reduce the supply in hopes of reducing the mortgage rates failed because the money did not stay in the USA. That is why the Fed then began to buy the mortgaged-backed securities because that was a more direct impact domestically.

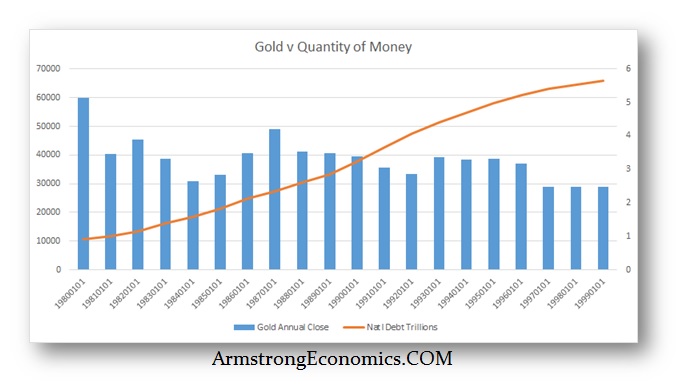

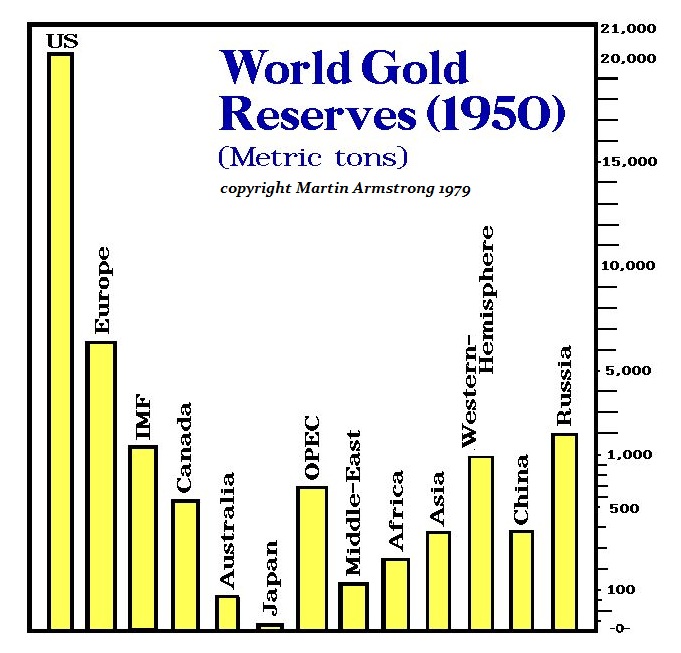

As the money supply increased and the national debt rose consistently, gold declined from 1980 into 1999 for 19 years. All the theories of inflation driving gold higher were simply wrong just as the central bankers relied on the very same theories.

It was World War I and II that drove the gold to flee to the United States so by 1950, there was no choice but to make the dollar the reserve currency. Yet more significant was the realization that the factor which produced that result was ENTIRELY external to the domestic economy. Therefore, all the economic theories were bogus because they were all focused on domestic policy thanks to Karl Marx whose central theory was the government possessed the power to eliminate the business cycle by confiscating all private assets. That altered human nature and created economic stagnation. Nevertheless, Keynes and everyone else have sought to accomplish the very same authority that Marx maintained existed.

This focus on GDP (Gross Domestic Product) has reversed the GNP (Gross National Product), which was more global in its scope. If we attributed world trade to the flag the company flies rather than where it sets up a plant, then you would see that the United States has a trade surplus and not a trade deficit. This is also a backdrop to the reserve status of the dollar. Perhaps the greatest of all the wild proposals is that somehow Bitcoin will rise from the ashes and become the new Reserve Currency of the world. So all governments will issue debt in Bitcoin? Politicians will never be able to run for office and Socialism must collapse.

Rather than betting on the power grid to survive if governments collapse, I think we will see the pre-1965 silver coins return for a medium of exchange and gold for larger transactions. I have said plenty of times, GOLD will NOT rise as a hedge against inflation, it is a hedge against the collapse in confidence of the government.

As I have written before, when the Japanese government lost the confidence of the people, they lost the ability to produce any money for 600 years. The people used the coins of China and bags of rice – no Japanese coins were ever acceptable for 600 years which was the same time interval it took to reestablish gold in Europe following the fall of the Roman Empire.

Everything he says I have confirmed from other sources. French soldiers who volunteered said the same thing, Ukrainians kill Russian prisoners sometimes ruthlessly. It is a total disgrace that we are supporting these Neonazis – the very people still practicing ethnic cleansing.

Posted originally on the CTH on December 28, 2022 | Sundance

In the background of international geopolitics and all things economically attached, the larger climate change agenda, the Build Back Better program, has been unfolding.

Energy driven inflation has destabilized most western economies as the various governments (politicians) and central banks (bureaucrats) work together on behalf of the corporations (World Economic Forum). All of these interests can only advance if they work together. If any individual nation breaks from the group energy agenda, their economy will thrive beyond the limits created by the BBB operation and the association of western nations.

It is with this context at the forefront where we have said to watch Mexico closely. In North America, Mexico has the least to gain from economics behind the climate change agenda. Conversely, if Mexico were to go rogue, they would gain the most. This dynamic puts Mexico in a more powerful position than most realize.

During a July 2022, meeting at the White House, Mexican President Andres Manuel Lopez-Obrador (AMLO) appeared to indicate -for the first time- his understanding of his new position as the ‘Green New Deal’ (climate change) energy agenda was being deployed by the U.S. and Canada. AMLO read from a prepared script in the oval office during a public bilateral meeting with Joe Biden. AMLO’s remarks were quite remarkable in their independence.

“In our country, we shall continue producing oil throughout the energy transition. With the U.S. investors, we are going to be establishing gas-liquefying plants, fertilizer plants, AMLO said, striking a chord that is not in alignment with Joe Biden and Justin Trudeau. AMLO continued, “and we’re going to accomplish this with the support of thermal electric plants and also through transmission lines to produce energy in the domestic market, as well as for exports, to neighboring states in the American union, as for instance, Texas, New Mexico, Arizona, and California.” It’s not just what he said, it’s how AMLO said it.

Keep in mind, the month before that July visit to the White House, AMLO boycotted Joe Biden’s Latin-America Summit. AMLO joined the leaders of Bolivia, Guatemala, Honduras and the tiny Caribbean state of St. Vincent in refusing to attend the Biden summit because Cuba, Venezuela and Nicaragua were blocked from attending by the Biden administration.

Socially and ideologically AMLO is a soft-socialist (immigration). However, he is also a strong economic nationalist who has previously expressed a dislike for the influence of multinational corporations in Mexico. As an outcome of his worldview, AMLO is not in alignment with the World Economic Forum. This is why we have said to watch Mexico in 2023; the dynamic will be very interesting.

Joe Biden and Justin Trudeau are in alignment with a North American approach toward energy, AMLO is the outlier. The people behind Biden and Trudeau also appear to want a North American Union established, essentially a nationless and borderless North America. On that aspect AMLO may be in agreement. However, watch for the key word “equity” in these discussions. Mexico is the poorest house on the block and if Canada and the United States want to create a unified North America, AMLO will want the Mexican people to be the biggest economic beneficiaries.

MEXICO – At today’s morning press conference headed by President Andrés Manuel López Obrador, Foreign Secretary Marcelo Ebrard presented the agenda for the tenth North American Leaders’ Summit (NALS) and its related meetings. The Summit will be held on January 10 in Mexico City.

The Foreign Secretary said that bilateral meetings will be held during the Summit. “The bilateral meeting between Mexico and the United States will include […] a wide range of actions focused on bilateral trade and investment, and on speeding up the border infrastructure projects.”

“Bilateral cooperation issues will be addressed, such as migration […] labor mobility, trade, security, education, culture, combating climate change… Labor mobility has already been added to the dialogue, the narrative, and the concept of the relationship between Mexico and United States. This did not exist [previously]; this is very recent […] Both the agreement we reached with Secretary Kerry, which was announced in Egypt […] on clean energy, […] and the Sonora Plan will be presented. The goal is for this dialogue to strengthen the integration of regional supply chains and the transition towards electromobility and clean energy.”

The Secretary said that, in the National Palace, the Summit tentatively includes “a private segment between the three leaders, that is, a conversation between the three of them, and then we will have an extended meeting with the delegations of each of the three countries.” He mentioned the six main topics that will be addressed at the summit: diversity, equity and inclusion; the environment; competitiveness with the rest of the world; migration and development; health; and shared security. “The three nations will seek to continue the process of regional integration, based on the principles of respect, sovereignty and good faith cooperation for mutual benefit; that is the goal,” he said.

The Foreign Secretary also announced that there will be a bilateral meeting between Mexico and Canada between President López Obrador and Prime Minister Trudeau. “They are going to talk about both governments’ strategy for indigenous peoples and historically marginalized communities. This is a topic that both Minister Trudeau and President López Obrador have promoted. There is a lot of international interest in this, in what has been done with the Yaquis and with other indigenous peoples of Mexico.”

The Foreign Secretary said that, at the Summit, “One of Mexico’s most important priorities relates to the actions that must be taken in 2023-2024 to reduce the poverty and inequality that are growing in the Americas […] this is the most important priority from the Mexican perspective.” “We are going to propose a Partnership for the Prosperity of the Peoples of the Americas […], this is what President López Obrador discussed with former Senator Dodd on his recent visit, and the Canadians have also been consulted,” he said, adding, “The main goal (of the partnership) will be to fight poverty and achieve a more equal distribution of resources in the Americas based on strengthening the trade relations and relations of all kinds on the continent […] so that North America remains a leading economic power at a global level, which would make it possible to establish new ties with the rest of the continent, based on mutual respect,” he concluded. (Read More)

President Lopez-Obrador has all the power in this dynamic right now.

AMLO is using the western energy transition to keep himself in a position of economic strength. In order to pull AMLO into the western climate change energy program, Biden and Trudeau will have to bribe him with major economic incentives; essentially, promises and economic outcomes to close the wealth gap.

If Mexico goes rogue, their economy can skyrocket. However, if Mexico goes rogue, the people behind Biden will destroy AMLO (Brazil exists as a reminder to him).

The U.S. and Canada are going to push every possible political pressure point in order to force Mexico to change energy policy. The stakes are high. It is going to be remarkable to watch what happens as this battle takes place.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America