Armstrong Economics Blog/Armstrong in the Media Re-Posted Mar 25, 2023 by Martin Armstrong

Watch the video above or click here to watch my latest interview with Maria Zeee: “The Financial Collapse is GUARANTEED – What Now?”

Watch the video above or click here to watch my latest interview with Maria Zeee: “The Financial Collapse is GUARANTEED – What Now?”

It is refreshing when you actually find a journalist who is honest and is not being included by the Neocons to put out their propaganda. Her review of Credit Suisse is a worthwhile read. Especially when this is not over yet and the winds of finance are now turning toward questioning Deutsche Bank.

Izabella Kaminska is senior finance editor at POLITICO Europe.

Over the span of 10 days, the global financial system was once again shaken.

The time frame between the collapse of Californian lender Silicon Valley Bank, America’s 16th largest bank, and that of the 167-year-old lender Credit Suisse was approximately just that — 10 days.

And as we witness the fallout, so far it appears contained. Stock markets are up, bank stocks seem stabilized and government bonds are in high demand. Officials reassure ad nauseam that the financial system remains strong and stable.

But the truth is, even if so, what happened in this period of time has changed the financial system forever — and worryingly, most people haven’t even noticed.

Governments and central banks would have you believe that in both cases, private sector solutions were found to resolve the failures. No taxpayer funds were used.

But that is likely not true.

In the United States, growing calls from the country’s top billionaires and hedge fund bosses to guarantee the full extent of customer deposits would, if acted on, deliver a backstop that must be underwritten by public funds. That’s the case even if costs are distributed among whatever healthy banks remain later. The sums involved are eye-watering — by some measures up to $17 trillion of unfunded liabilities.

If the rule is passed — and all indications are that it will be — this would finally make the implicit explicit: that the financial system was never really rescued following the 2008 financial crisis but merely put on life-support. And that has now failed, which means socialization of the losses beckons.

Over in Europe, things are potentially worse. This time, it wasn’t the storming of the Winter Palace Hotel in Gstadt that seized the means of financing but something far more mundane: an untidy bank resolution for Credit Suisse, which relies far too heavily for comfort on Swiss National Bank (SNB) guarantees.

As one former top British central banker told POLITICO, “They could have used bail-in; it would have worked; and banking would become part of a capitalist market economy” — a reference to the loss-absorbing processes regulators came up with after 2008 to ensure bank failures didn’t have to draw on public resources ever again. “The only stable equilibrium is one where bank resolution works, or socialism,” he added.

But the resolution didn’t work. And investors are belatedly realizing this.

Key to this reality is that Credit Suisse was a bank considered to be in good condition and solvent by all regulatory measures. As one bank analyst told POLITICO, going by the assets, you would never have seen the problem coming. Even the SNB and financial markets regulator FINMA said so as recently as last week.

So were the regulators lying? Or is the accounting somehow fundamentally broken?

What we know for sure is that markets questioned the numbers, and this was evidenced by a run on the bank’s deposits, equity and bonds. And the discrepancy poses a big problem going forward, as it knocks trust in the accounting of all similarly assessed banks, which, thanks to international accounting standards, means pretty much all of them.

Credit Suisse’s sale to domestic rival UBS at cents on the dollar of what regulators claim the underlying assets are worth presents another problem too. If similar assets are lurking in UBS’ own balance sheet — and chances are that is the case, as the assets in question are probably government bonds — they might have to be written down to a similar degree. This is probably why UBS needed the guarantee from the SNB to be doubled to 100 billion Swiss francs to do the deal.

In light of this, Switzerland now faces an even larger issue: If UBS were to become stressed — and it very well could due to this discrepancy — there’s no private sector pathway for resolution left. The country now only has one major bank and, thus, only two possible pathways to deal with a failure — nationalization or acquisition by a foreign buyer with enough cash to keep the valuation of all the consolidated assets at a price that brings everything back to par. And there are few of those in the Western hemisphere.

With a full foreign acquisition off the table due to global discord, this leaves only an unthinkable solution for the home of Swiss private banking — the dawn of a type of finance more commonly seen in communist countries, where banks are directed by the state to allocate funds to activities they prioritize. Combined with a central bank digital currency, this would reduce banks to mere proxies of the state, with uncertain consequences for efficient capital allocation and inflation.

How things would unfold from then on is unclear. The only thing we can be sure of is that nothing in banking, or capitalism, may ever be the same again.

Almost as soon as German Chancellor Olaf Schulz said, “The banking system is stable in Europe – Generally, I think we are in good shape,” shares of German-based Deutsche Bank began dropping.

After a Friday loss of 14%, the bank came back to close -9.8%, and on the heels of the Credit Suisse collapse and subsequent purchase, concerns are still reverberating.

BRUSSELS (AP) — European Union leaders Friday played down the risk of a banking crisis developing from recent global financial turbulence and hitting the economy even harder than the energy crunch tied to Russia’s war in Ukraine.

After a meeting in Brussels, the EU government heads said lenders in Europe are generally in sound health and in a position to weather a combination of rising interest rates and slowing economic growth.

“The banking system is stable in Europe,” German Chancellor Olaf Scholz told reporters after the summit. Dutch Prime Minister Mark Rutte said: “Generally, I think we are in good shape.”

The EU deliberations came in the wake of U.S. regulators’ shutdown of two U.S. banks, including Silicon Valley Bank, and a Swiss-orchestrated takeover of troubled lender Credit Suisse by rival UBS.

The emergency actions on both sides of the Atlantic revived memories of the 2008 global financial meltdown and the ensuing EU sovereign debt crisis, which almost broke apart the euro currency now shared by 20 European countries.

In a sign of market jitters in Europe, shares of Deutsche Bank, Germany’s largest lender, fell as much as 14% in Frankfurt on Friday. The drop, which dragged down the stocks of other European lenders, followed a steep rise in the cost of financial derivatives known as credit default swaps that insure bondholders against the bank defaulting on its debts.

Scholz dismissed the idea of basic weaknesses at Deutsche Bank, saying it has become “very profitable” after modernizing its business. “There is no reason to have any concerns,” he said. (read more)

The German bank has lost about a fifth of its market value this month. Other European banks were also down at closing, including Deutsche Bank German rival Commerzbank, which was down 9%. Credit Suisse and its new parent company, Barclays and Societe Generale were all down over 6% on Friday.

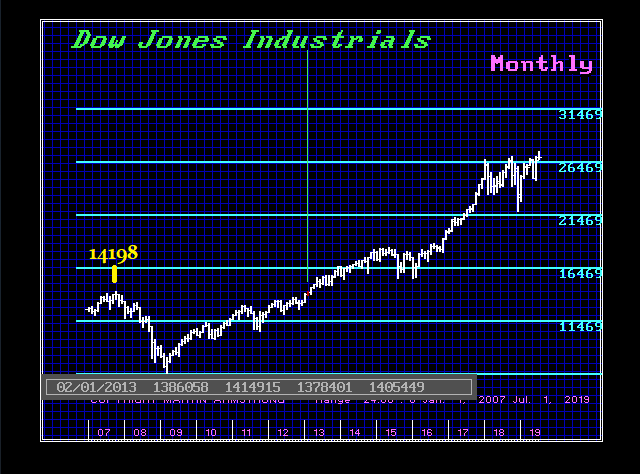

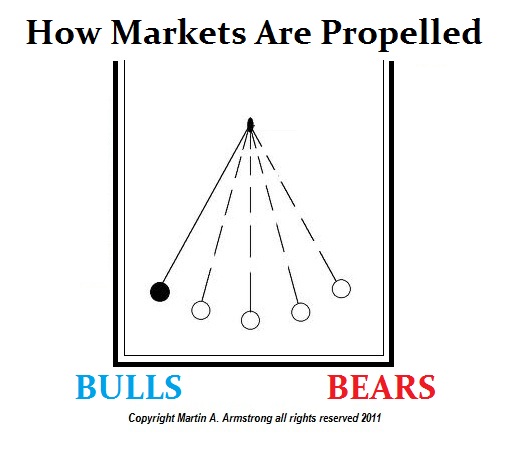

In 2010, Barron’s wrote a piece on me effectively laughing at my forecast that the share market would rally to new highs. What seems to inevitably unfold is this notion that whatever the event might be in motion, the mere thought of a reversal in trend appears impossible. When the press disagrees with Socrates, I know it will be the press who is wrong. And because they end up being wrong, of course, they cannot print a retraction so they will just pretend you do not exist rather than admit – Sorry, we were wrong. The Dow made that new high above 2007 by February 2013. That was 64 months from the October 2007 high.

I have been in the game for many years. With each event, it appears to be like Groundhog Day. They pop their heads out and declare they do not see their shadow, so the entire world will disintegrate and that is always based upon opinion. It is never backed by real analysis. Just the standard human trait of assuming whatever trend is in motion, will remain in motion.

Being an institutional adviser, I have never had that luxury. We have had to deal with some of the biggest portfolios in the world. They want accurate forecasting, and it has to be long-term – not day trading. They are not interested in the typical headlines of doom and gloom that the press love to print with every financial event simply to get readership. That is all they care about. It has been the financial version of the fake news.

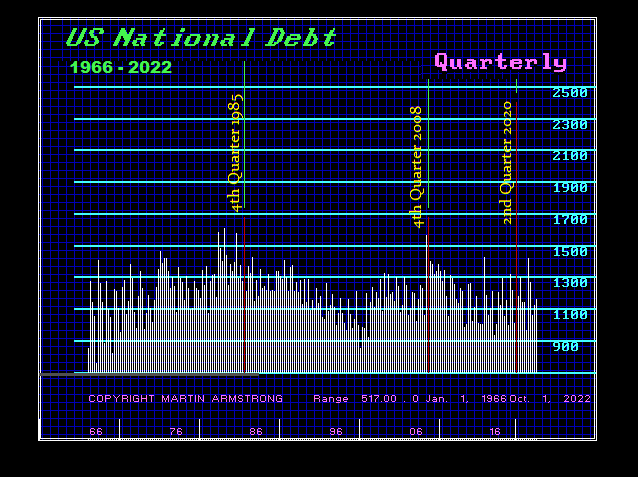

When we step back and look at this favorite fundamental that people beat to death to predict the end of the world, the national debt, and the collapse of the dollar. Little did they know that the increase in National Debt during the 2007-2009 Financial Crisis was supposed to bring down the sky and end the existence of the dollar. We can see the sharp rise in debt simply made a double top with the Financial Crisis of 1985.

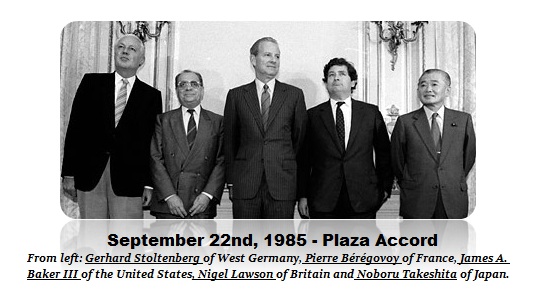

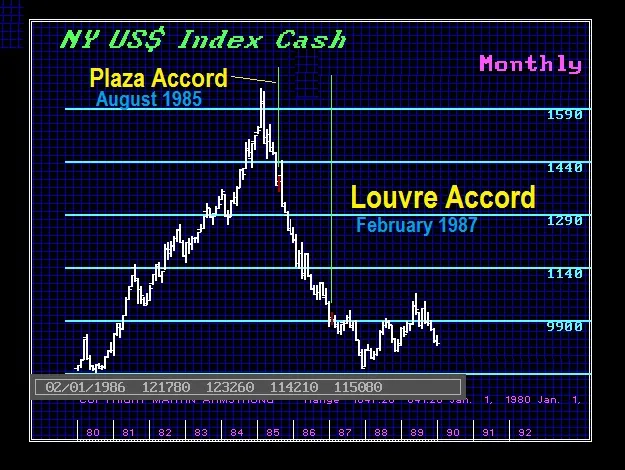

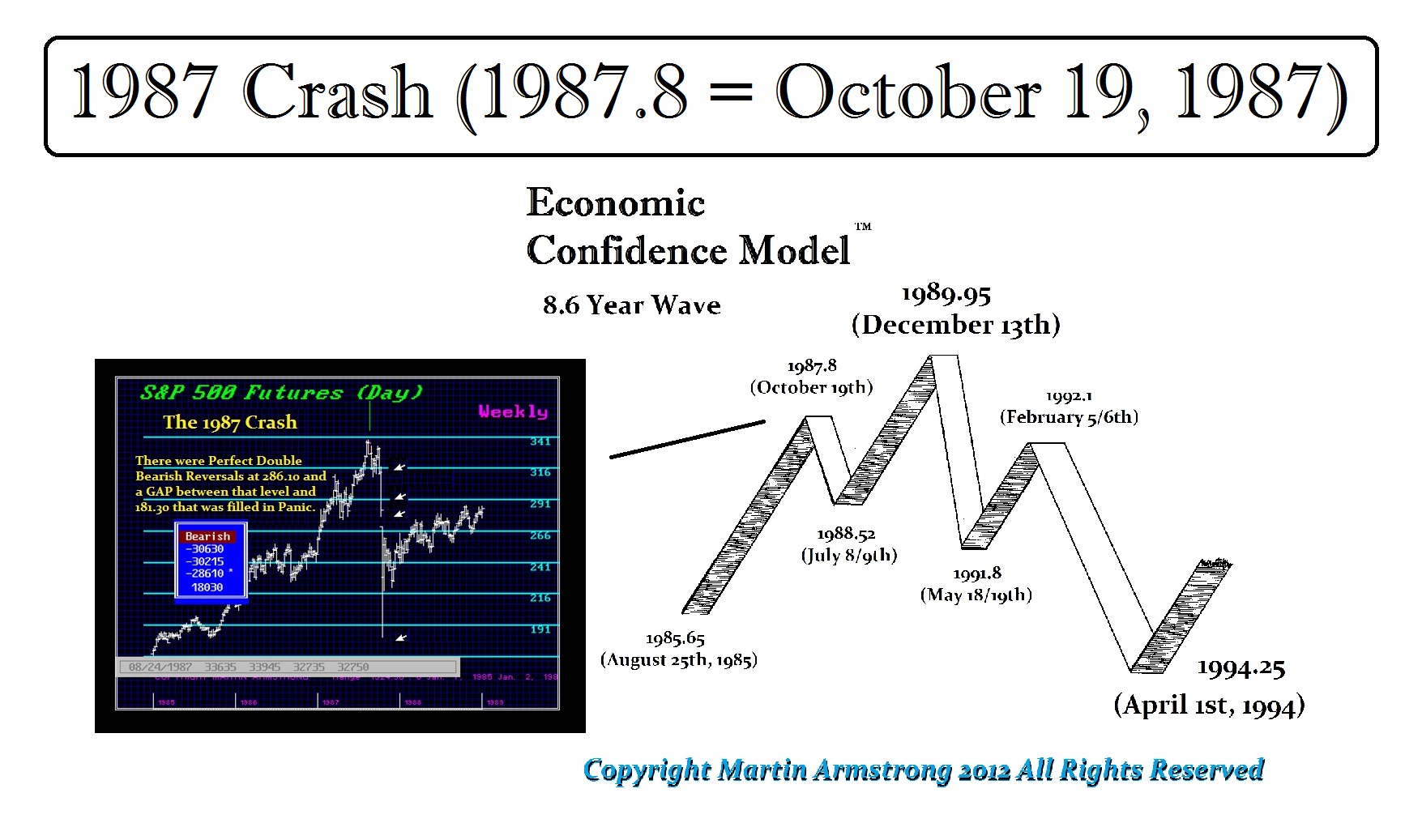

It was that previous 1985 Financial Crisis that set in motion the Plaza Accord which brought together the central banks creating what was then the G5 – now G20. Of course, like every government intervention, the side effect was the 1987 Crash and their attempt to reverse their directive at the Plaza Accord became the Louve Accord. When the traders saw that failed, the collapse in confidence led to the 1987 Crash.

It has always been a CONFIDENCE game as I pointed out with the 1933 Banking Holiday previously. In this case, the failure of the Louvre Accord which came out and said the dollar had fallen enough, once new lows in the dollar unfolded and the central banks could not stop the decline, led to financial panic by 1987 which manifested in the 1987 Crash.

This chart shows the quarterly change in the National Debt since 1966, Here you can see the 1985 and 2008 Financial Crises were on par. Neither one ended the dollar no less the world economy. So when I warned the share market would rally and make new highs and Barron’s laughed in 2010, I said the same thing after the 1987 Crash and people laughed.

In fact, on the very day of the low, I said this was it and that we would rally back to new highs by 1989. That was perfect and the market responded to the Economic Confidence Model (ECM) which has been published back in 1979. This was more than simply forecasting the 1987 Crash and the very day of the low. It clearly established that the ECM had revealed that there was a secret cycle behind the appearance of chaos even in economics.

Larry Edelson was actually a competitor at the time. But Larry respected that the forecast from the model was far beyond what people would ever expect. If we are ever going to advance as a society, we have to stop the bullshit and understand HOW markets trade and WHY. Larry did that. He understood that the model was something larger than just personal opinion.

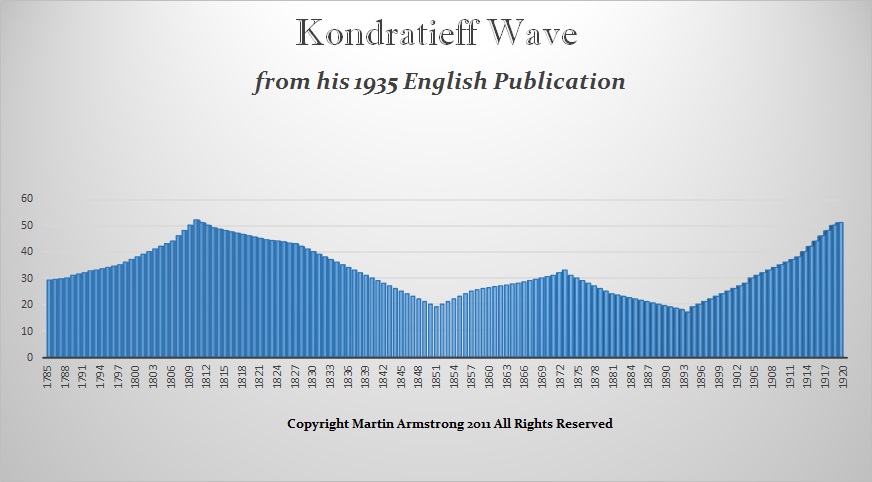

Even those claiming to be using the K-Wave cannot make real forecasts. The basis of Kondratieff’s argument came from his empirical study of the economic performance of the USA, England, France, and Germany between 1790 and 1920. Kondratieff took the wholesale price levels, interest rates, and production and consumption of coal, pig iron, and lead for each economy. He then sought to smooth the data using an averaging mathematical approach of nine years to eliminate the trend as well as shorter waves. Kondratieff thus arrived at his long-wave theory suggesting that the economic process was a process of continuous waves of boom and bust.

Kondratieff’s work was compelling and contributed greatly to the Austrian School of Economics that first began to develop the concept of a Business Cycle. The general central principle of the Austrian Business Cycle Theory is concerned with a period of sustained low-interest rates and excessive credit creation resulting in a volatile and unstable imbalance between saving and investment. Within this context, the theory supposes that the Business Cycle unfolds whereby low rates of interest tend to stimulate borrowing from the banking sector and thus then result in the expansion of the money supply that causes an unsustainable credit source boom which leads to a diminished opportunity for investment by competition.

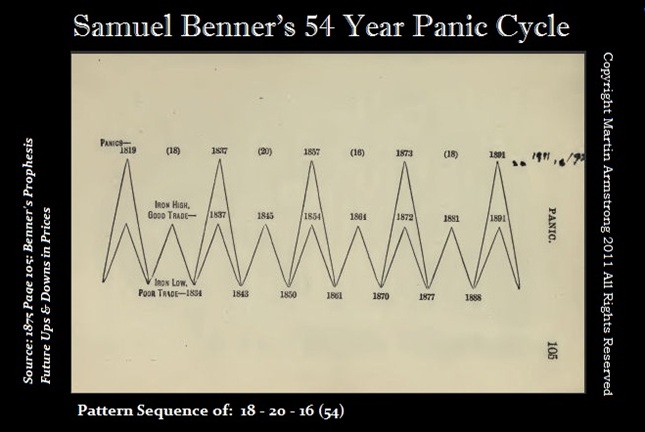

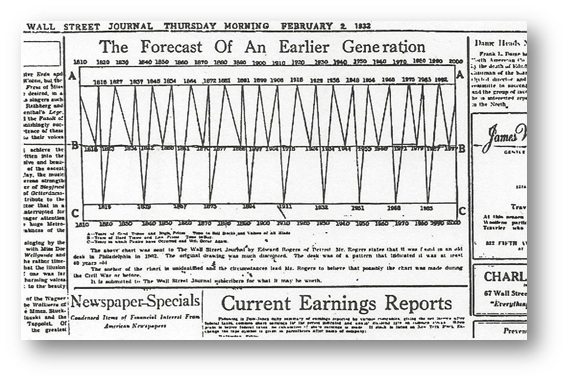

Here is a chart of the business cycle that was created by a farmer named Samuel Benner. Benner based his work on Sunspots, which actually incorporated solar maximum and minimum that today’s Climate Change zealots refuse to consider. Nevertheless, someone manipulated Brenner’s work and created a chart to try to influence society handing it in with a wild story to the Wall Street Journal published this cycle on February 2nd, 1932, when the market bottomed in July 1932. Still, nobody knew who had investigated this phenomenon in 1932.

When I was doing my own research reading all the newspapers to understand how events unfolded, I came across this chart. I found it interesting that during the Great Depression people were reaching out and some began to embrace cyclical ideas. The problem with both Kondratiff and Brenner was that the period they used to develop their cycles was the 19th century because the real Industrial Revolution was unfolding and in the 1850s, 70% of the civil workforce were all in agriculture. Consequently, if you constructed a model based entirely upon one sector, it would work only as long as that sector was the top dog.

Being a historian buff, it quickly hit me that NOTHING remains constant and that the economy will ALWAYS evolve, mature, and then crash and burn. Where agriculture was 70% of the workforce in 18590, it fell to 40% by 1900, and then down to 3% by 1980.

Just look at energy. The earliest lamps, dating to the Upper Paleolithic, were stones with depressions in which animal fats were burned as a source of light. In cultures closer to the sea, they began to use shells as lamps which they would burn at first animal fat. Clay lamps began to appear during the Bronze Age around the 16th century BC and the invention quickly spread throughout the Roman Empire. Initially, they took the form of a saucer with a floating wick.

We even find Roman oil lamps as luxury items crafted out of bronze. There are collectors of terracotta oil lamps for there is a vast variety of motifs. There is everything from dolphins, and various entities, to erotic oil lamps, which may have been used in brothels. The point is, if you constructed a model on oil, you would have surely accomplished similar results to Kondratief and Brenner.

Then of course, just as the energy moved from animal fats to vegetable oils, by the 19th century it returned to whale oil which was extracted from the blubber. Emerging industrial societies used whale oil in oil lamps and to make soap. However, during the 20th century, whale oil was even made into margarine.

Then the discovery of petroleum and the use of whale oils declined considerably from their peak in the 19th century into the 20th century. Ironically, it was fossil fuels that probably saved whales from extinction. Hence, now we are entering a period where they deliberately want to end fossil fuels and move to solar and wind power. Obviously, just a cursory review of energy reveals the problem of basing a model on the current energy source or major economic industry. Things change with time.

Honest journalism has become a crime. I have appeared numerous times on Maria Zaric’s program, Zeee Media. Maria is a professional journalist who asks thought-provoking questions to the experts that appear on her show. Her content goes against the grain and traditional narrative. The Australian-based journalist has been questioning COVID, the Great Reset, governments, globalists, the war in Ukraine, and many other topics that are completely taboo in the mainstream media. They attempted to shut down her channel in the past. Now, she has been de-banked with no explanation.

“Do you shut down peoples accounts due to their political views by any chance?” Maria asked the bank representative, only to be met with silence. Maria had been banking with ING Bank for numerous years without issues. Her account was suddenly shut down shortly after releasing a story on domestic terrorism in Australia. ING Bank has been unable to explain why her account was canceled.

Interestingly, ING is a partner of the World Economic Forum. Maria has extensively covered the WEF’s agenda to “enslave humanity.” Is Australia secretly keeping track of journalists’ “social credit scores” to silence skepticism?

The idea of eliminating someone’s ability to bank is essentially eliminating them from society. We saw Canada do the same thing to those protesting the Trucker Convoy. Trudeau took things a step further by also de-banking people who simply donated to the cause. The Canadian government used the premise of money laundering as a way to coerce the banks into reporting any activity that could have been intended to help the protestors. I know of numerous people who were frantically attempting to remove their funds from the bank during this time.

As if the public needed more reasons to lose trust in the banking system. This is not limited to one bank or country. I discussed how banks have the ability to “cancel” someone after JPMorgan Chase de-banked the rapper Kanye West for antisemitic remarks. The bank acts as the jury and judge. Epstein was permitted to hold funds at JPMorgan Chase despite an ongoing pedophile ring trial. Bernie Madoff banked with JPMorgan Chase. The bank has secret ties to the Third Reich and helped the group funnel money through South America during World War II. Again, the bank acts as the jury and judge; anyone can be de-banked anytime for any reason.

Most countries may not openly have social credit scores, but they’re keeping tabs on us. They are keenly aware that resistance to this New World Order is building. So they are now using professional journalists as examples hoping that people will stop asking questions to learn the truth. That is one of the reasons why this blog is free of charge – you deserve to know the truth.

The banking crisis continues and it is impacting funds that have been buying bonds. Allianz, a subsidiary of Pimco, is writing off countless millions with Credit Suisse bonds. The banking crisis has been the result of artificially low-interest rates for far too long and banks were used to free money and buy long-term bonds all because they were making their money on the spread. Now that rates are rising, their risk management was effectively nonexistent, and thus the losses and widespread.

The Allianz subsidiary Pimco is one of the largest asset managers in the world. They have to now write off a loss in Credit Suisse bonds and it’s ain’t over yet as we head into April 10th.

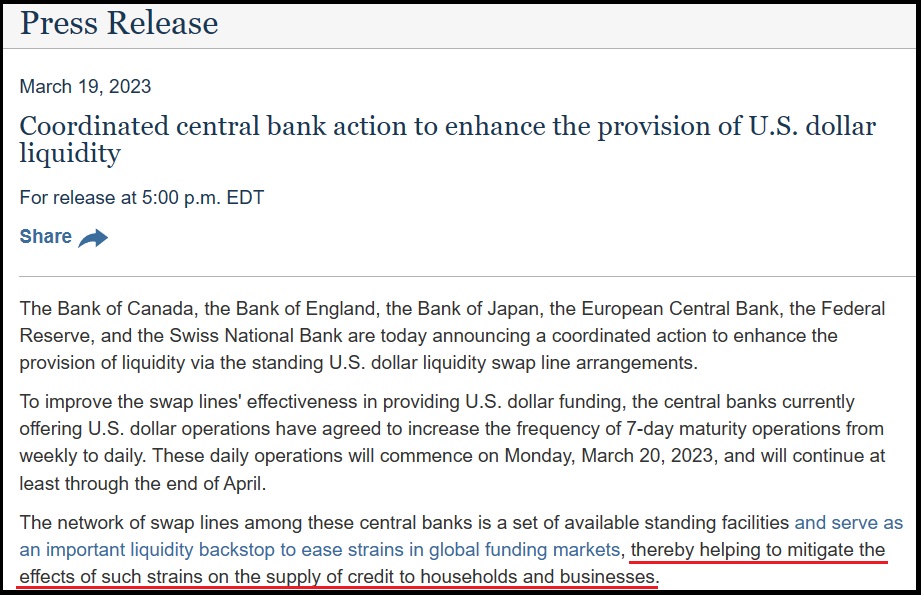

This is rather remarkable and tells us something about the current status of the “western” financial system. The last sentence in today’s announcement from the FED is particularly laughable. Check this out [Source]:

That last sentence is nonsense. When was the last time the ‘central banks’ worried about the supply of credit to households and businesses? Total and complete nonsense. What they are worried about is the need to have readily available dollars, faster, to backstop banks that are supposed to be holding deposits.

Nothing quite inspires ‘global banking confidence’ like the need to swap dollars rapidly, from country to country on a daily basis, because the amount of currency in bank, within any western nation, at any given time, might disappear.

Yesterday’s monologue from Neil Oliver, and the recent personal banking story that structures his comments, is standing as eerily prescient right now. SEE BELOW:

.

“This just in. Everything is fine… the liquidity of the Western banking system has never been stronger”… “Look over there folks, Trump indictment, nothing to see here folks… move along now”…

COMMENT: Marty, I hate to tell you but the reason you saw this coming was that you are old – like me. LOL. Do you realize that the 2007-2008 crisis was 16 years ago! Time flies, my friend. Most traders at these banks are under 35. That means that they have never seen anything like this and could not smell, taste, or see it coming. When we were youngsters, the old guy in the corner of the room would always say this is like 1929. Remember him? We are that guy today. I will buy you a Dewars when I get to Florida. The good news is we won’t have to endure this insanity much longer.

Cheers

ND

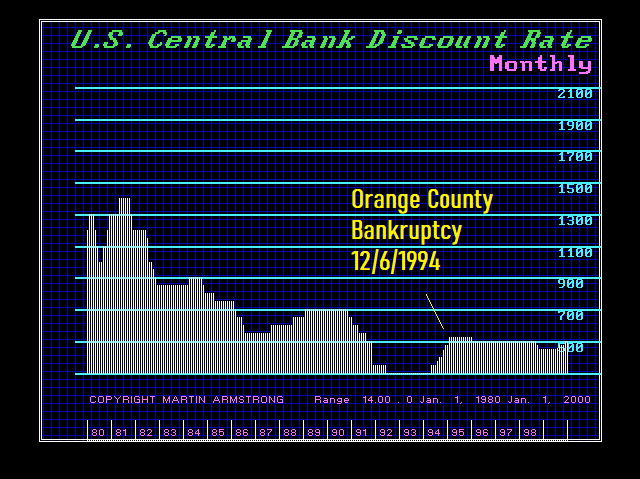

REPLY: I guess you are right. There has been a cycle of events like this for centuries. Perhaps it requires a new generation of traders every 16 years or so who think they know everything. When I was advising Temple University’s portfolio and Merrill was trying to sell them the “new way” to make money by buying the long-term, selling the short-term, leveraging that to the moon and the spread would enhance your yield, the way to increase the yield on your portfolio. The chairman of Temple told them if I approved it the University would consider the proposal. I told them interest rates would rise and they would blow up. These two young kids selling this leverage deal told the University I was “too old” back in the 90s because I did not know the “new way” to make money. The chairman was older than me. The University told them to take a hike. On December 6th, 1994, Orange County California became the largest municipality in U.S. history ever to file for bankruptcy for they tried the “new way” to make money and blew up. That was in the courts for some time.

These people NEVER seem to ever understand when the trend will change especially in interest rates. They also position themselves based upon opinion and consensus but the consensus MUST be wrong for that is what flips the trend back and forth. Only fools invest money based on opinion and the consensus view and are quickly separated from their money. Without that loss, they never learn how how markets work and those that blame others are hopeless perpetual losers for they never learn anything.

Even Ben Franklin said during the Financial Crisis: “In this world nothing can be certain, except death and taxes.” He uttered those words because of the financial panics. in his day. There was the Panic of 1791 which was followed by a massive real estate bubble that then burst during the next Panic of 1792.

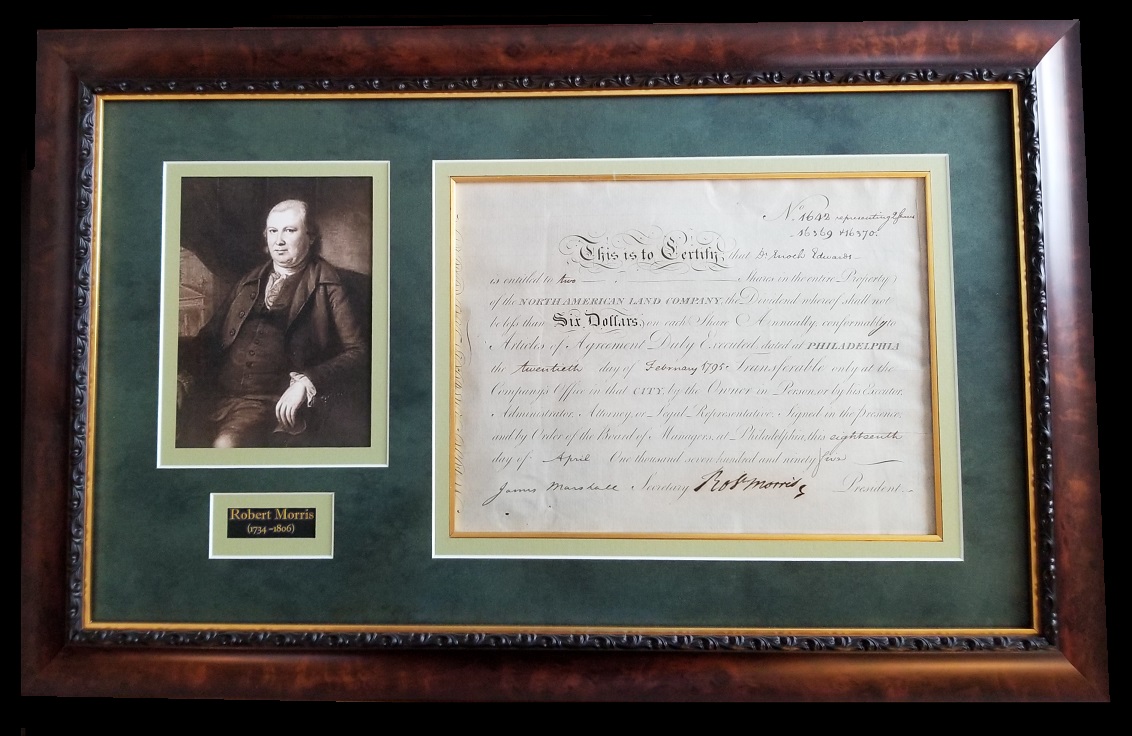

The Bank of North America had been the creation of Robert Morris (1734-1806) who got caught up in the whole real estate bubble. Morris had financed the American Revolution. He was a major patriot. Nevertheless, his bank went bust in the first Financial Panic over interest rates back then and he ended up in debtor’s prison thanks to the Panic of 1792. This is one of my favorite relics of the era.

So banks have been failing over interest rate swings for hundreds of years. They don’t teach this risk management in university and the current risk models do little but snooze over the real risks for they ignore cycles. We NEVER learn from the past because people find history irrelevant or boring. You are right, we are the old guys in the corner of the room compelled to watch others repeat history over and over again.

QUESTION #1: Marty, I think your warning about the collapse of leadership in government and the private sector rings true as Ken Griffin, the founder of hedge fund Citadel, said the rescue of Silicon Valley Bank shows the U.S. economic system is “breaking down before our eyes” because they bailed out the depositors. Yet Carl Icahn seems to agree with your saying that the U.S. economy is at a breaking point because of inflation. He said, “every hegemony has been destroyed by inflation.”

Very few so-called billionaires seem to understand what’s at stake. It makes me think they were just lucky in how they made their money. After Griffin’s comment, I would not be inclined to invest in Citadel. Then a group of banks is talking about depositing $20 to $30 billion to save Republic bank.

Is there any hope for the future when leadership is absent in these times of chaos?

UT

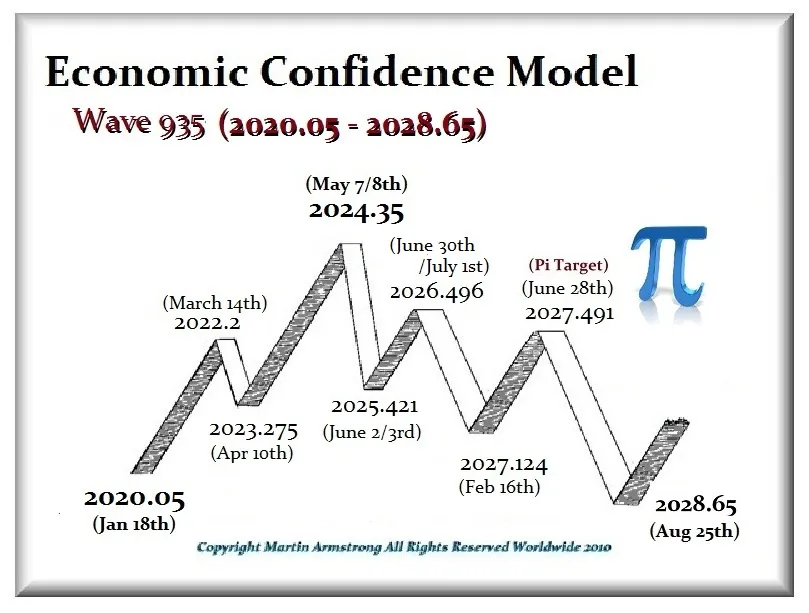

QUESTION #2: Thanks for everything you do. At the WEC, you warned about banks and even the big funds. The turning point was at the end of January here in 2023. Is it possible that this financial crisis will be the major factor even overpowering war when the ECM comes into play by April 10th?

CW

ANSWER: Anyone who does not understand that inflation is a natural occurrence when you get into a war is clearly not a student of history and has no business being the CEO of even the head local dog-catcher. The Roman deity Janus, after whom January is named, was the two face entity who looked at the past and the future. The doors to his temple would be closed when there was peace. That symbolized that nothing was at risk of changing. However, in times of war, they would leave the doors open to symbolize the uncertainty of war that the spirits could flow in and out.

Only today, do we seem to no longer respect that the cost of war is both lives lost and inflation for those who survive. This Ukrainian Proxy War serves no purpose. Winning or losing will have ZERO impact on our national security or the future of the people. This is simply a grudge match instigated by the Neocons who perpetually love war as long as someone else is dying for their personal goals. To them, it is nothing more than watching a war on CNN and cheering as if it were a football game.

I have said that this war will undermine the entire US economy and that is now manifesting in the Financial Crisis of 2023 which will be far worse than any of these people expect. The lack of experience and the stupidity of those who remark that capitalism is collapsing because they are honoring the depositors is absurd. A depositor has NO WAY of understanding the financial status of a bank until it is too late. They receive no warning and yet there are those who say they should suffer the losses because that is capitalism.

Sorry, but that has NOTHING to do with capitalism. It is no different than FRAUD soliciting money with a false pretense. Investing in a hedge fund like Citadel is different from a bank. Depositors in a hedge fund know they are investing their money and they are getting a piece of that return. That is capitalism. Someone who has a bank account where their social security check is automatically deposited took on no such risk. Sorry – that is different that a hedge fund that goes bust.

The problem we have is that the ECM turning point is April 10th. Yet it is also the Pi Target from the fall of the USSR and the birth of even Ukraine. We just had Poland losing their mind and sending jets to Ukraine. That makes Poland a viable target for war. Poland is irresponsible given the fact that the Ukrainians slaughtered over 300,000 of them and has refused to ever apologize for their WWII Nazi involvement.

We have a problem here with the Financial Crisis simultaneously with important cyclical targets regarding war. Any personal interpretation I can offer is just a personal opinion. Both trends are colliding into April and this may be a two-prong panic of unprecedented significance.

Small to medium sized banks along with credit unions are the best vehicle for Main Street USA small businesses. Somehow in all the conversations about banking customers, this little factoid is seemingly, perhaps purposefully, overlooked. WATCH:

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

De Oppresso Liber

A group of Americans united by our commitment to Freedom, Constitutional Governance, and Civic Duty.

Share the truth at whatever cost.

De Oppresso Liber

Uncensored updates on world events, economics, the environment and medicine

De Oppresso Liber

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America

Australia's Front Line | Since 2011

See what War is like and how it affects our Warriors

Nwo News, End Time, Deep State, World News, No Fake News

De Oppresso Liber

Politics | Talk | Opinion - Contact Info: stellasplace@wowway.com

Exposition and Encouragement

The Physician Wellness Movement and Illegitimate Authority: The Need for Revolt and Reconstruction

Real Estate Lending