Posted originally on the CTH on May 4, 2023 | Sundance

According to those who relish the Cloward-Piven strategy, things are proceeding swimmingly.

…”As long as the decisionmakers continue doing the things that are creating the crisis, the crisis will continue.”

Federal Reserve Chairman Jerome Powell said yesterday the “U.S banking system is sound and resilient,” insert uncomfortable snicker here. However, uncertainty is continuing to pummel the banking industry, despite assurances from the Fed, Treasury, FDIC financial regulators and bankers such as Jamie Dimon who are all saying there is no crisis in the banking industry.

If you want to know the big picture source of the uncertainty, it’s the great pretending. The average person can sense something is wrong, and the person who pays attention has the experience of institutional lying over the past several years. The last ten years of lying and pretending has created the biggest collapse in institutional trust in U.S. history.

Russians interfered with the election – trust us. Stick this needle in your arm, it’s safe – trust us. The FBI are the good guys – trust us. Biden won more votes – trust us. This inflation is merely transitory – trust us.

See the problem?

So, when the same voices shout, “the banking industry is sound, trust us,” well,… yeah, that suspicious cat sense that’s on high alert isn’t buying the chorus.

Reasonably intelligent people who accept things as they are, not as they would have us pretend them to be, can see the core connection to the World Economic Forum, Central Banks, and western globalist policy to change the entire dynamic of economics and finance around the “Climate Change” agenda, or Build Back Better, or Green New Deal.

Overlay that commonsense and pragmatic outlook with the logical consequences of the activity, and this banking collapse issue is a self-fulfilling prophecy. As long as the decision makers continue doing the things that are creating the crisis, the crisis will continue.

(Via Wall Street Journal) – Regional-bank stocks tumbled Thursday despite assurances from the Federal Reserve that the banking system is on solid footing.

PacWest Bancorp PACW -47.04%decrease; red down pointing triangle, which has been hit hard since the collapses of several banks, dropped by about 40%. The stock started falling in after-hours trading Wednesday evening, after a report that it was considering selling itself.

PacWest said in a statement after midnight Eastern Time Thursday that its core customer deposits were up since the end of the first quarter, and that it hadn’t experienced any unusual deposit flows since the collapse of First Republic.

[…] Investors have been wondering how much further the problems in regional-banking could spread, and whether they will spill over to the broader economy. Some analysts said the decline in PacWest and others reflected the market’s tendency to view news as categorically good or bad, rather than worries about PacWest specifically. Western Alliance, another bank whose stock has been hit hard, fell by about 35%.

[…] Regional banks, as major lenders to businesses and families across the U.S., also tend to fall when investors are expecting a recession. The 10-year Treasury yield slipped this week, and Brent crude hit a 52-week low on Wednesday.

[…] On Wednesday afternoon, the Fed said the U.S. banking system “is sound and resilient,” echoing language from its March statement. Fed Chair Jerome Powell added then that deposit flows at banks had eased and that this week’s seizure and sale of First Republic should further stabilize the industry.

[…] PacWest shares were recently trading around $3.70, putting them on track for their lowest close on record. The stock has now lost some 85% of its value since March 8, the day that SVB spooked bank investors by announcing a loss and a planned capital raise.

Many of PacWest’s customers are tied to technology startups—a tightknit clientele that pulled from high-balance accounts en masse at Silicon Valley Bank before it failed. (more)

Republicans at the state level are demanding that Biden and the FHFA repeal the asinine new law that punishes Americans with high credit scores by forcing them to subsidize the mortgages of those with low credit scores. The Biden Administration has been attempting to control real estate for some time. In June 2021, Biden forced the Supreme Court to give him the power to fire Mark Calabria as the regulator of Freddie Mac and Fannie Mae. Biden’s team said they were “moving forward today to replace the current director with an appointee who reflects the administration’s values.” This was also when shareholders sued the government for the 2012 decision to pay all proceeds directly to the Treasury.

Trump was in favor of Calabria and fought to separate Freddie and Fannie from the government, but the Democrats repealed everything once Joe took over. Florida Chief Financial Officer Jimmy Patronis and 33 other Republicans at the state level are urging Biden and the FHFA to repeal this “hair-brained” policy. “This new policy … will take money away from the people who played by the rules and did things right – including millions of hardworking, middle-class Americans who built a good credit score and saved enough to make a strong down payment,” the group noted. “Incredibly, those who make down payments of 20 percent or more on their homes will pay the highest fees – one of the most backward incentives imaginable.”

Patronis and others argued that owning a home was once the American dream, and the new law will hurt middle-class families who worked and budgeted for their downpayment and credit score. “[T]he right way to solve that problem is not to use the power of the federal government to penalize hardworking, middle-class American families by confiscating their money and using it as a handout. The right way is to implement policies which will reduce inflation, cut energy costs and bring lower interest rates. Doing so will enable more families to save and improve their credit scores. Increased financial literacy efforts must also be part of the solution,” the letter also states. Lowering energy scores and inflation is not part of the Build Back Better agenda.

Providing people with loans who otherwise would not qualify is part of the plan for the Great Reset. Raising taxes on everything imaginable is also part of the agenda. The government wants to tax the middle class out of homeownership, force the working class to default on their mortgages, and move everyone into government-provided smart cities. The hatred toward government is brewing and will soon bubble over.

Posted originally on the CTH on May 1, 2023 | Sundance

The topline story from the announcement by JPMorgan Chase [SEE HERE] there are no banking rules/laws in the Biden Fed/Treasury system.

The Dodd-Frank laws are still on the books, but the FDIC decision to insure all deposits, regardless of size, now means those laws, rules and regulations are not required to be followed. Additionally, as a result of JPMorgan gaining another $100+/- billion in deposit assets, the law(s) surrounding the 10% U.S. deposit maximum, within too big to fail banks, no longer exists. Noted in the announcement, “JPMorgan Chase is assuming all deposits – insured and uninsured.”

JPMorgan is also assuming assets consisting of $173 billion in loans and approximately $30 billion in securities. The FDIC is going to assume risk (with a risk sharing agreement) for current First Republic Bank mortgage and commercial loans acquired by JPMorgan, guaranteeing JPMorgan a 5-year fed fixed rate on $50 billion in mortgage bonds.

The Federal Deposit Insurance Corporation (FDIC) rule requiring the holding of 1.5% of deposits for all depositors up to $250k in all institutions is now essentially moot. If the FDIC is guaranteeing all deposits, there’s no way for the insurance corporation to capture or hold $1.5% of all banking deposits. The law is in conflict with the outcome action of the Fed/Treasury and ultimately the FDIC, ergo the law is nulled by the ignoring of it.

Mohamed El-Erian gives his take below, but seemingly missed the part of the announcement where JPMorgan states, “no systemic risk exception was required” in the deal. This means the FDIC is completely free-range with the agreement, they are not even trying to justify why they would make a too big to fail bank even bigger. WATCH:

.

The only reason the FDIC violated its own rules and banking regulations, was because the FDIC didn’t, likely -almost certainly- couldn’t, take the financial hit from a full takeover of First Republic Bank against the backdrop of the prior terms for Silicon Valley Bank (SVB).

When the FDIC made the (SVB) decision to guarantee all deposits regardless of size, they put themselves in a position of an insurance declaration they could never fulfill. The FDIC cannot structurally guarantee all of the First Republic Bank (FRB) deposits; they need a structure to avoid the government regulators absorbing the bank. This reality is also why the FDIC violated their own laws, rules and regulations in allowing JPM to exceed the legal U.S. deposits maximum.

In essence, what the FDIC is saying is they cannot maintain the premise of their charter without the big banks helping them. The biggest banks now control all of the leverage, with JPMorgan Chase and Jamie Dimon now controlling more financial power than the government that is supposed to regulate them.

FUBAR… All of it. Everything Biden touches turns to shit.

This is going to be a major hot mess now for Main Street investment and borrowing needs. The economy is going to feel the ramifications of this in less financing available to maintain domestic investment.

Last point. Look at the big picture, there’s no intervention protocol the legislative branch can trigger as a security against the reckless decisions of the FDIC (Fed and Treasury), without creating even bigger issues that could collapse the banking system. If the legislative branch forced the FDIC to follow the laws currently on the books, the domino of banks starts to collapse.

Posted originally on the CTH on April 30, 2023 | Sundance

Gary Cohn is connected to the banking and finance industry, well connected. In this interview with Face The Nation earlier today, Cohn is discussing the current status of First Republic Bank, another big player in the California banking system that is about to collapse. Cohn notes something at the 1:15 mark that just seems obvious yet is undiscussed in most outlines of the FRB discussion.

Six weeks ago, in an effort organized by the FDIC, $30 billion was pushed into FRB by eleven larger banks to stabilize it. However, the only thing that infusion of capital did was allow institutional depositors time and ability to withdraw their funds. A complete racket. Once the at-risk group exits, suddenly the collapse is back on the tee. WATCH:

[Transcript] – MARGARET BRENNAN: We want to turn now to Gary Cohn, who is the vice chairman of IBM, former Goldman Sachs president and a former Trump administration top economic adviser. Good morning to you. Lots of titles, Gary, Lots of experience. That’s why we like having you here. I want to ask you about what’s happening with First Republic. It’s been under pressure. We know they’ve been looking for a buyer, the FDIC, the government is looking to arrange, moving it into government control and then maybe selling it. What are you hearing about how this would roll out?

GARY COHN: Margaret, thanks for having me. I think you’re portraying the situation as we find ourselves again on a weekend. As we closed business of Friday, the FDIC was in a process of looking for acquirers or bidders for the assets over the course of the weekend. I think the FDIC has asked potentially three banks for their final bids for the entire bank. The FDIC would prefer to sell the bank in its entirety than the pieces. What will most likely happen is the FDIC will seize control and then simultaneously resell the asset to the successful bidder. I think that will happen sometime later this afternoon before the markets open in Asia this evening.

MARGARET BRENNAN: And this will be a faster process than what happened with SVB?

COHN: It will be- it will be a much faster process. Now, we’ve been going down this process for the last two weeks or so as first republics continues to be under pressure and continues to lose deposits. Unfortunately, First Republic reported this week that they had a massive outflow of deposits over the last quarter.

MARGARET BRENNAN: So if First Republic is sold, then the acquirer would take on the deposits. So what do you think about the conversation we had earlier with Congressman Khanna about whether Congress needs to do something here? Because it seems like we’re just going into emergency mode now for three banks.

COHN: Yeah.

MARGARET BRENNAN: Does there need to be a broader change to the regulatory system and to the laws?

COHN: Well, it’s an interesting question. So, look, I don’t agree with Congressman Khanna that we want unlimited FDIC insurance. I think that to me is a bit of a race to the bottom.

MARGARET BRENNAN: You had picked like two, 2 million. 5 million, 10 million.

COHN: Yeah. I mean, there’s got to be some limit. It’s- at some point you have to limit because you don’t want to race to the bottom where you know, the weakest bank with the weakest balance sheet in the world can offer you the highest rate of return on your deposits. And therefore, you take your deposits there because guess what? They’re insured by the federal government. That’s not what we want to see. We want to see some type of discipline in the system. When you talk about more and more regulation, I smiled because if you look at the report that came out that you referenced with Ro Khanna as well, you know, one of the findings in the report is that the regulators did not do a very good job enforcing the existing rules. So if you can’t enforce the rules you already have on the books and by- it’s hard to enforce the rules because there are so many rules, do you want to create more and more rules when you can’t enforce the one you already have? Part of me feels like we need to get a simpler, more coherent set of rules so the bank regulators can actually enforce them and they know what the important rules are.

MARGARET BRENNAN: But the bank regulators here are at the Fed. That’s what we’re talking about here.

COHN: They’re at the Fed and at the States. Remember–

MARGARET BRENNAN: That’s true.

COHN: –we have state regulated banks and federally regulated banks.

MARGARET BRENNAN: Well, that’s a big conversation for California since they just had two banks–

COHN: It is.

MARGARET BRENNAN: –have some big problems. But Fed Chairman Powell is going to face questions from the press midweek.

COHN: Yes.

MARGARET BRENNAN: They- he gives a press conference around the decision on interest rates that he is expected to be making. Do you think these banking problems are going to interfere with his plan?

COHN: I don’t think these problems are going to interfere with his plans. I actually think they’re helpful to his plans.

MARGARET BRENNAN: Because they’re slowing the economy?

COHN: Exactly. What the- what the chair has been trying to do is slow the economy down. He’s been trying to tamp down inflation. Inflation is too many goods chasing too few products. And part of the chasing has been the easy availability of credit. Now that we’ve seen deposits lose- the- leave the system and we’ve seen banks in tighter financial position, they are not offering loans as easily as they were before and the loans have become more expensive. So people are borrowing less money, they have less access to credit, so their ability to purchase is going down. Purchasing power is waning in the United States, which is exactly what the chairman’s been trying to do by raising interest rates. So he’s in essence, getting enormous amount of help out of this banking crisis, not what he wanted to see happen in any way, shape or form, but the unintended consequence is very helpful to slowing down the economy and tamping down inflation.

MARGARET BRENNAN: So does it up the odds of a recession being more than mild?

COHN: It probably ups the odds. Yes. I mean, it definitely ups the odds. It takes control out of the Fed. The Fed is no longer in total control of slowing down the economy. They’ve now got the banking industry playing along with them. But as we’ve seen in the economic data recently, the consumer in the United States still is in relatively good shape. They are starting to run out of savings. The money that they got during COVID, we put an enormous amount of stimulus into consumers bank accounts and that administrations, both administrations, every every administration put enormous amount of stimulus in the bank accounts. We see from the savings data that’s starting to to wear down. It’s starting to run off. So is that runs off further and further. The economy would become more credit dependent to keep thriving. So I think we will see a slowdown. And I still think we’re in a relatively decent shape. We may have a recession, but I still. I think we could muddle through the bottom here without a real deep recession.

MARGARET BRENNAN: The chair of the House Financial Services Committee, Congressman McHenry, called the Fed’s report a self-serving justification of Democrats long held priorities. He may be venting. It doesn’t look like Congress is doing anything to change regulation or laws related to banking. There was an FDIC report on the collapse of Signature Bank, which blamed bad management, but it also said regulators just didn’t have enough staff. In New York. I mean, there’s some pretty damaging bits of information in here. If you put aside the politics, the regulators don’t have enough staff. They didn’t act. So who are they being held accountable by unless it’s Chair Powell?

COHN: Well, it is Chair Powell. And I think- I think when the chairman goes to Congress and remember, he testifies in front of both the House and the Senate a couple of times a year. Historically, all of the questions have been on monetary policy. I think we’re going to start seeing a lot more questions on the regulatory and the regulatory policy. How is regulation working? Are they keeping up to what they need to do? Do they have proper staff or there are issues that are going by that are not being covered? This is a huge finding. I mean, this is a bit of a seismic moment because we believe in the United States and I think the US population believes that the banks where they deposit their hard earned money are well regulated. And we have found out this week in the Fed’s own report that these banks are not well regulated, and they admitted it themselves. I ran a regulated bank. I know that if we would have ever told our regulator that we did not have a enough people to regulate ourselves, they would have shut us down. So we cannot be in a position where the regulators themselves say we do not have enough staff to regulate you properly.

MARGARET BRENNAN: You ran one of the biggest banks. Gary, we’ve got to leave it there. We’ll be back in a moment.

Posted originally on the CTH on April 29, 2023 | Sundance

There’s something sketchy afoot in the world of high finance. Following the collapse of Silicon Valley Bank, the most likely first contagion bank would have been First Republic Bank; both California banks carried similar vulnerabilities. However, once the Treasury Dept agreed to cover all deposits, even those unsecured deposits over the $250k FDIC insurance protection, suddenly First Republic Bank survived.

After the FDIC announcement, a group of 11 larger banks lent First Republic a tranche of money ($30 billion) to secure its holdings and help stabilize it. Approximately six weeks passed, suspiciously perhaps the burn rate for the tranche in combination with risk averse exits says I, and suddenly First Republic starts destabilizing again. [Insert Suspicious Cat here]

The First Republic stock value collapsed further last week, and the FDIC is now trying to get a takeover bid secured before government regulators are forced into a position of receivership. I’m not dialed in to the banking industry, but it looks to me like the six-week interim phase was an agreement to give the illusion of stability and afford time for highly exposed, ¹likely well connected, stakeholders to exit.

With the Treasury taking the prior SVB position, thereby securing all deposits regardless of scope, the FDIC is now on the hook if the collapse includes a govt takeover. The FDIC seems to be playing hot potato and looking for a buyer. Additionally, the FDIC is asking JP Morgan-Chase if they are interested. JPMorgan holds more than 10% of all deposit funds in U.S. banking. From a regulatory position, JPM cannot legally take any more institutional deposits. So, what gives? It is all sketchy, all of it.

(Bloomberg) — The Federal Deposit Insurance Corp. has asked banks including JPMorgan Chase & Co., PNC Financial Services Group Inc., US Bancorp and Bank of America Corp. to submit final bids for First Republic Bank by Sunday after gauging initial interest earlier in the week, according to people with knowledge of the matter.

The regulator reached out to some banks late Thursday seeking indications of interest, including a proposed price and an estimated cost to the agency’s deposit insurance fund. Based on submissions received Friday, the regulator invited some of those firms and others to the next step in the bidding process, the people said, asking not to be named discussing the confidential talks.

Spokespeople for JPMorgan, PNC, US Bancorp, Bank of America and the FDIC declined to comment. Bank of America is considering whether to proceed with a formal offer, one of the people said. Citizens Financial Group Inc. is also involved in the bidding, Reuters reported, citing people with knowledge of the matter.

The bidding process kick-started by regulators — after weeks of fruitless talks among banks and their advisers — could pave the way for a tidier sale of First Republic than the drawn-out auctions that followed the failures of Silicon Valley Bank and Signature Bank last month. Authorities are stepping in after a particularly precipitous drop in the company’s stock over the past week, which is now down 97% this year.

Unclear to some involved in the process is whether regulators might use a bid for a so-called open-market solution that avoids formally declaring First Republic a failure and seizing it. The stock’s drop — leaving the company with a $650 million market value — has made such a takeover at least somewhat more feasible.

[…] A group of 11 banks that deposited $30 billion into First Republic last month — giving it time to find a private-sector solution — have proved reluctant to band together on making a joint investment. A few proposals that surfaced in recent days called for a consortium of stronger banks to buy assets from First Republic for more than their market value. But no agreement materialized.

Instead, some stronger firms have been waiting for the government to offer aid or put the bank in receivership, a resolution they view as cleaner — and potentially ending with a sale of the bank or its pieces at attractive prices.

But receivership is an outcome the FDIC would prefer to avoid in part because of the prospect it will inflict a multibillion-dollar hit to its own deposit insurance fund. The agency is already planning to impose a special assessment on the industry to cover the cost of SVB and Signature Bank’s failures last month. (more)

¹This is pure speculation on my part, but if you were a well-connected California big fish and you had exposure in FRB, after the SVB collapse you might ask the govt to construct an exit plan to assist you.

$11 billion flows in, you make your quiet withdrawals, and after exit the delayed outcome proceeds accordingly.

Armstrong Economics Blog/USD $ Re-Posted Apr 24, 2023 by Martin Armstrong

COMMENT: Marty; I was in a board meeting and I just wanted to let you know one guy who is there simply because his family had a stake in the company with zero worldly experience, started ranting about the end of the dollar he probably read on that biased _____________________. I asked this fool, should we then move all our company funds to Russia or China since Brazil is too small of an economy? Should we stop dealing with Americans? He had no response.

Separating a fool from his money seems to be a never-ending fact about humanity.

Cheers

You are the only sane one out there these days

PY

REPLY: I know what you mean. The people promoting this BRICS nonsense have no understanding of the real world. Institutions cannot park billions in Brazil, China, or Russia. Especially in the face of war. The reason the Euro has failed as a serious reserve currency is that there is NO NATIONAL EURO DEBT! Institutions have to still jockey between the various risks of each country and all the Euro did was transfer the foreign exchange risk to the bond market. Sorry, I just do not see where the dollar is in some state of collapse.

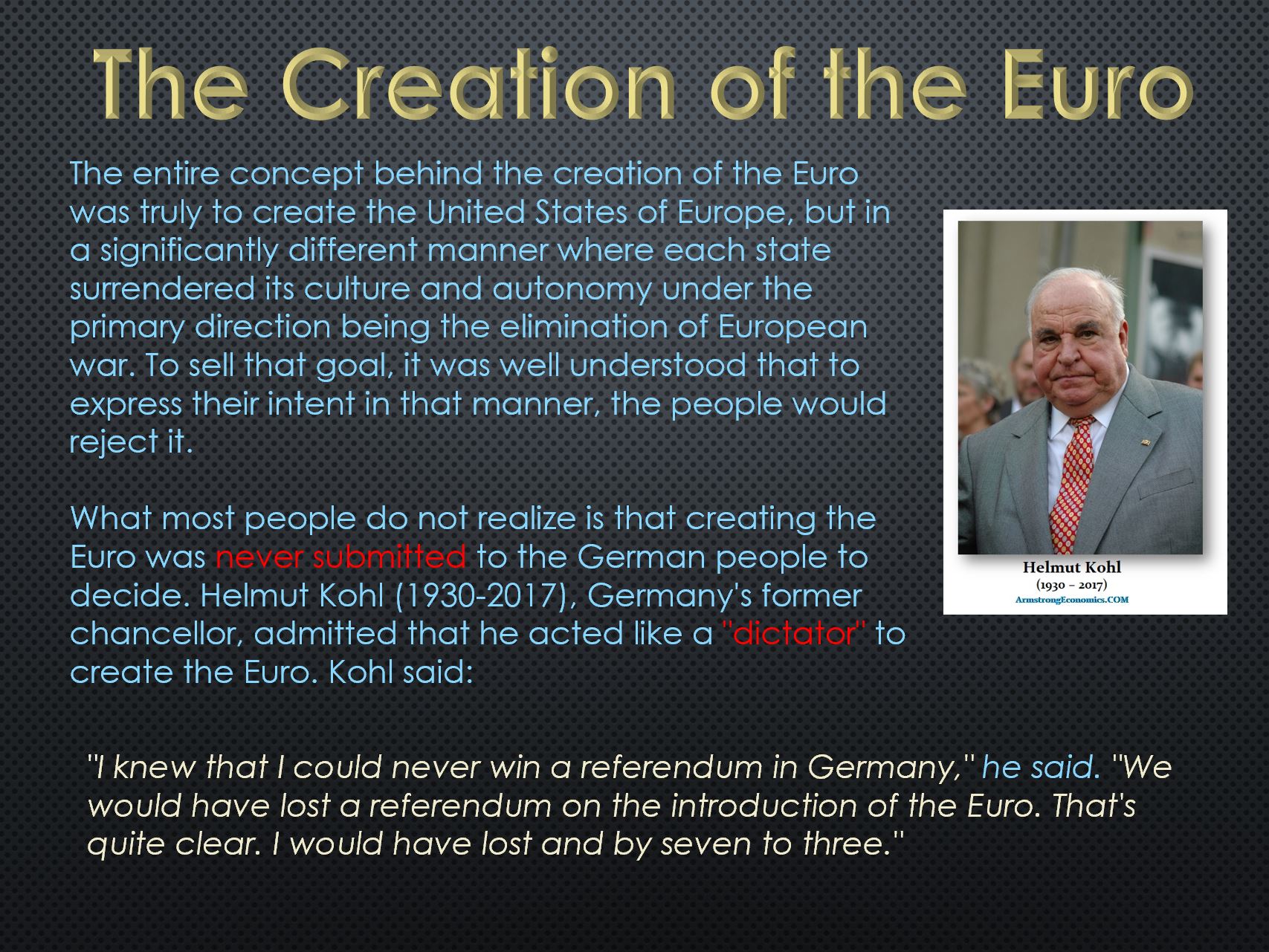

When they came to me to create the Euro, I warned them that there would be no single interest rate without the consolidation of the debt. But Kohl never allowed the German people to vote on joining the Euro, so he would not allow the consolidation of the debt. I was told then that they just had to get the Euro started and they would worry about consolidating the debts later. Of course, that never came. Hence, the volatility in FX simply moved to the debt market. The bottom line – the US dollar is still the ONLY place for major institutions to park money – PERIOD! They are not buying Brazil, China, or Russia.

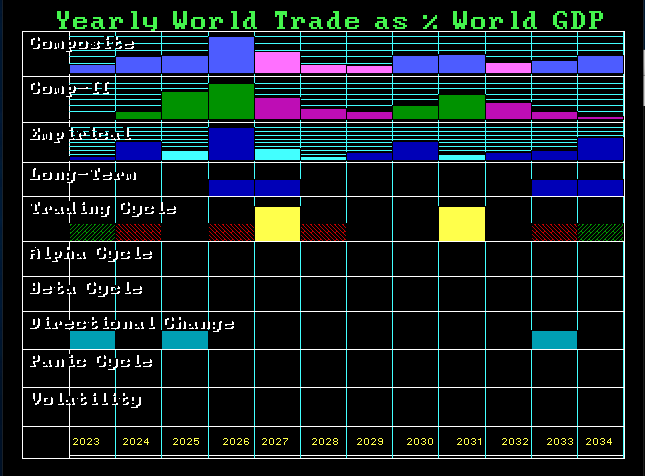

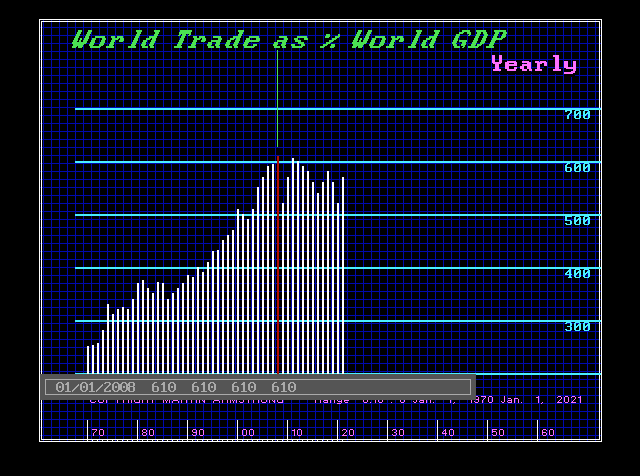

World Trade as a percent of total world GDP PEAKED in 2008 at 61%. It has been in a bear market that will not bottom before 31.4 years taking us into 2040. The sanctions on Russia have divided the world economy and killed SWIFT but it has also ended globalization. To think that the BRICS can replace the dollar with ZERO capacity for international capital to park in such markets is the delusion of absolute fools. China will surpass the USA, but only after 2032.

So here we go again. This nonsense is leading unsuspecting people to follow the piper to divest of dollars and move into what exactly? Most of this is propagated by the gold bugs who will NEVER listen. They hate the dollar because they think gold will rise then. What kind of a world will exist if their doom and gloom were a reality? You might not have any place to spend your wealth. I own gold NOT as an investment, but because of its neutrality.

There is such a major fraud going on with digital currencies with people reporting that the latest scam is using social media to tell people to transfer all their cash to a digital wallet, and BTW – here is the link! If you believe that one, perhaps you would like to buy the Brooklyn Bridge. NYC has a deficit and they will sell it for all the money in your savings. Wake up!

These people remind me of the famous drawing of a fool and his cat.

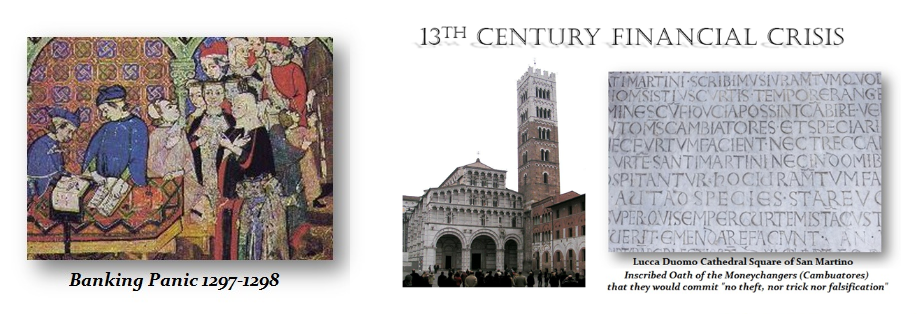

Reposed from Armstrong Economics Blog Posted Apr 25, 2023 by Martin Armstrong

QUESTION: Mr. Armstrong, Your knowledge and database on financial crises is really unprecedented. I googled the first banking crisis and it brought up only the Crisis of 1763, which started in Amsterdam. Yet that list published in the WSJ which showed 1683 as the first panic and the siege of Vienna was most interesting. I know you have written about the sovereign defaults on the ancient central bank in Delos. My question is, was there any major financial banking crisis between antiquity and 1683? I figured if anyone would know, he had to be you.

PF

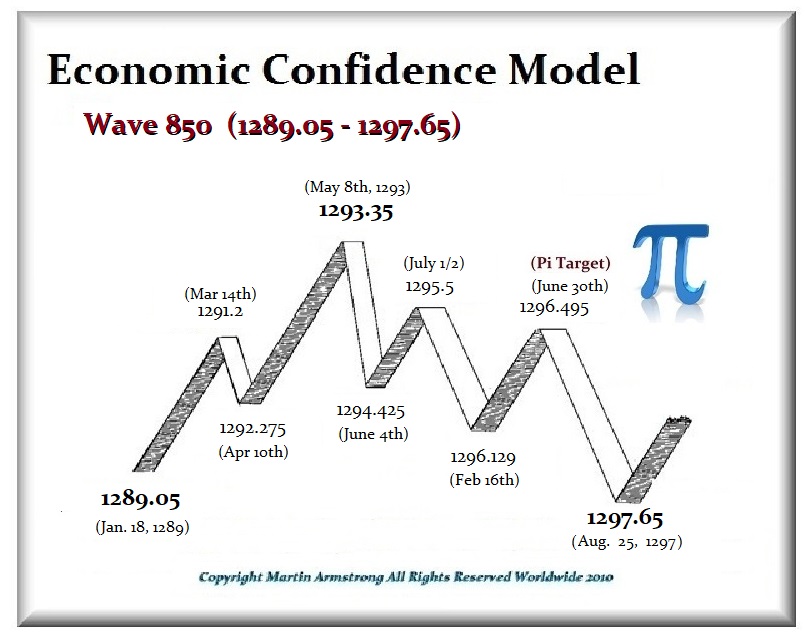

ANSWER: As the 13th century unfolded, the cost of endless Crusades burdened both the crowns of England and France. Throughout the remainder of the 13th century, a variety of Crusades were aimed not so much at toppling Muslim forces in the Holy Land but to combat any and all groups seen as enemies of the Christian faith. Edward began his reign in 1275 with heavy debts incurred from the Crusades.

These endless wars resulted in the time of major sovereign defaults by Edward I of England and Philip IV of France. In 1275, Edward secured a financial monopoly and negotiated a grant of export duties on wool, woolfells, and hides that brought in an average of £10,000 a year. He then used this as collateral to borrow substantially from Italian bankers granting them the security of these customs revenues to fund his endless wars of aggression.

Edward imposed heavy taxes on the value of movable goods. At the beginning of this Wave 850, Edward defaulted on his loans from the English Jewish bankers, and then as 1290 began, to cover that default he expelled all of the Jews from England and confiscate all their property.

Moreover, this was the Edward Langshakes of the movie “Brave Heart” when in 1291 he attacked Scotland. As this 8.6-year Wave 850 peaked, Edward launched his very costly war against Philip IV (1295-1314) of France which lasted until the end of this 8.6-year wave came to an end in 1297.

The Riccardi of Lucca was perhaps one of the major international merchant banking houses to emerge during the 13th century. The Riccardi established branches in Rome, Bordeaux, Paris, Flanders, London, York, and Dublin, Ireland. They engaged in trade with Edward I of England. Prior to 1272, the English kings were customers of the Italian merchant who had exotic imports as they were purchasing luxury goods and would use them to transfer money to Rome. With the outbreak of war against Philip IV in 1294, a major credit crunch and inflation erupted which impacted the entire international money markets throughout Europe at the time. The value of gold rose against silver from 10:1 to virtually 15:1, which was a monumental distortion of the European monetary system as a consequence of these endless wars.

Cash-strapped, Edward sought financial support from the Riccardi establishment but they refused to lend him any funds. In response, Edward seized all of Riccardi’s assets in England, effectively bankrupting them. The Riccardi had derived significant benefits in dealing with the English monarchy. They held contracts with special access to the English wool market. The Riccardi banking establishment was involved in about 50% of all the forward contracts with English wool producers, which were in effect futures contracts in the cash market. When Edward confiscated all the assets of the Riccardi, his action backfired. Nobody else would then deal with England in international money markets. This led Edward I to impose heavy levels of domestic taxation, which led to civil unrest. This led to a constitutional crisis of 1297.

We all may know that Magna Carta established rights that were forced on King John on June 15th, 1215. After John’s death, the regency government of his young son, Henry III, reissued the document in 1216, but it removed some of its more radical content. This led to civil unrest and at the end of the war in 1217, it became part of the peace treaty when it acquired the name “Magna Carta.” Henry III was compelled to reissue the charter again in 1225 in exchange for a grant of new taxes. Edward I was his son who was then once more compelled to reaffirm the Magna Carta in 1297 at the end of the 8.6-year Wave 850. That is when Edward I was forced to confirm that the Magna Carta was England’s statute law. That is when it actually became England’s rule of law.

The Bonsignori bank was known as the Gran Tavola, which had become the most powerful of the Italian merchant banking firms throughout Europe between 1255 and 1298. The Gran Tavola was indeed the greatest bank of the 13th century with branches in Paris, Marseille, Genoa, Bologna, and Pisa in addition to the main office in Siena.

Philip IV of France was also strapped for funds. He chose the debasement of the coinage which was massive. Philip had no other course of action to meet the expenses of the war. He began as a massive debasement of the coinage. Silver began to migrate out of France. This debasement only accelerated after 1298 when Philip IV confiscated all the assets Italian bank known as the Gran Tavola in France on claims that they owed him money, without netting anything with respect to his loans owed to them. This caused a major banking crisis in 1298 with the collapse of the institution which also held funds for the Papacy resulting in their loss of 80,000 gold florins. This was the first Banking Panic post-Dark Age. This confiscation of assets wiped out Siena and the city never again rose to the forefront of European commerce. By 1320, Siena was no longer a significant city in international commerce whatsoever which was a direct attack on the Papacy by Philip IV. This resulted in shifting the banking power to Florence.

A full-blown financial panic unfolded as silver migrated overseas. People hoarded the old currency and by 1301 there was virtually no silver remaining in the open market in France. Currency depreciation let Philip cover the cost of the war but it destroyed the credit of France and that ultimately led to France seizing the Papacy and strip-mining all its assets moving the Church to Avignon where a French Pope was installed. They then seized all the assets of the Knights Templar and burned all resistance alive. The Knights Templar were effectively an international transfer agent. If you were in France and needed to pay someone in Italy, you gave the money to the local office in France and they instructed the brank in Italy to pay. It was a 13th-century version of a wire transfer service. That is why the French crown seized the Knights and strip-mined all their wealth as well.

Obviously, this banking crisis of 1298 was far beyond anything most people would have read about in a financial crisis. This is what I mean when I warn that those in power will do WHATEVER it takes to retain power, and religion never means anything at the end of the day.

People often ask if their money is safe in a regional bank. Yes—if you keep it under $250,000 to guarantee the FDIC insures those funds. Some clueless minds brainwashed into fighting the class warfare thought, “Oh well!” for people who had more than them in the bank and did not care if the Silicon Valley Bank or Signature Bank failed.

My phone did not stop ringing and the bankers wanted to know if they should cover ALL the deposits. I actually lost my voice, screaming, “YES YOU MUST COVER ALL THE DEPOSITS! ALL OF THEM!!!” Aside from the fact that no one deserves to lose their hard-earned money, the primary issue here is that failing to cover the deposits would have completely wiped out small businesses.

Small businesses comprise 70% of GDP and must be protected at all costs. They must park large sums in the bank to cover payroll to pay their employees and operational costs. Small businesses would come to a standstill and banks would fall like dominoes. Unemployment would spike and the entire economy would plummet. We would see a massive banking crisis if all small businesses went under. More banks will go broke, it is only a matter of time, but it is crucial that deposits are covered

QUESTION: Hi. I do not understand why you keep advocating over and over how the depositors should be bailed out over 250k. It makes no sense from a moral hazard perspective. It is fact that should they do that, in spite of depositors signing agreements acknowledging that deposits over 250k would not be guaranteed, the Fed will also need to cancel all outstanding debt instruments, whose borrowers also signed an agreement that if they don’t pay they lose the asset. The moral hazard is so severe as to bloody the eyes. Why do you keep endorsing the bailout which will have to be at least initially funded by taxpayers even if they get the money back? The money to shore up bank reserves in exchange for collateral has to come from somewhere. What is the real fear, that people will move deposits direct to T-bills and in so doing, set up funding for a US CBDC? Please address the moral hazard aspect of your position. So far, I’ve heard nothing to defend the immorality of it.

FO ANSWER: Do not confuse a bank depositor with (1) an investor in a fund, or (2) bank shareholders & Management. A bank depositor is NOT an investor. The $250k is by NO MEANS sufficient for small businesses. They need to keep large amounts on hand for payroll etc. You do business and accept credit cards and they deposit that into your bank account.

Bank depositors are unsophisticated average people. The sophisticated investor moves their, money to a hedge fund or money market fund and fully understands that there is a risk associated with that investment. The bank depositor accepts no risk on any investment the bank makes. It does not give them, a piece of their profits. That goes to shareholders. It is a bailout of the entity and thus the shareholders which presents the moral hazard perspective.

If deposits in excess of $250 are NOT covered, you wipe out small businesses, they cannot pay employees and the ripple effect will be the total destruction of the entire economy. Your house will become worthless for its value will drop to only what someone can pay in cash.

There is a HUGE difference between investing and losing and simply depositing your money in a bank because we are moving to an electronic monetary system that there will be no way for a depositor to even demand money from a bank. Some are restricting wires to $3,000 and limiting the amount of cash one can withdraw. There is also not enough paper currency to facilitate bank withdrawal on a grand scale. Bank robbery will come to an end without cash.

None of that will unfold if a hedge fund fails. We must look deeper into this entire question.

Posted originally on the CTH on March 24, 2023 | Sundance

Almost as soon as German Chancellor Olaf Schulz said, “The banking system is stable in Europe – Generally, I think we are in good shape,” shares of German-based Deutsche Bank began dropping.

After a Friday loss of 14%, the bank came back to close -9.8%, and on the heels of the Credit Suisse collapse and subsequent purchase, concerns are still reverberating.

After a meeting in Brussels, the EU government heads said lenders in Europe are generally in sound health and in a position to weather a combination of rising interest rates and slowing economic growth.

“The banking system is stable in Europe,” German Chancellor Olaf Scholz told reporters after the summit. Dutch Prime Minister Mark Rutte said: “Generally, I think we are in good shape.”

The EU deliberations came in the wake of U.S. regulators’ shutdown of two U.S. banks, including Silicon Valley Bank, and a Swiss-orchestrated takeover of troubled lender Credit Suisse by rival UBS.

The emergency actions on both sides of the Atlantic revived memories of the 2008 global financial meltdown and the ensuing EU sovereign debt crisis, which almost broke apart the euro currency now shared by 20 European countries.

In a sign of market jitters in Europe, shares of Deutsche Bank, Germany’s largest lender, fell as much as 14% in Frankfurt on Friday. The drop, which dragged down the stocks of other European lenders, followed a steep rise in the cost of financial derivatives known as credit default swaps that insure bondholders against the bank defaulting on its debts.

Scholz dismissed the idea of basic weaknesses at Deutsche Bank, saying it has become “very profitable” after modernizing its business. “There is no reason to have any concerns,” he said. (read more)

The German bank has lost about a fifth of its market value this month. Other European banks were also down at closing, including Deutsche Bank German rival Commerzbank, which was down 9%. Credit Suisse and its new parent company, Barclays and Societe Generale were all down over 6% on Friday.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America