Armstrong Economics Blog/Regulation

Re-Posted Jul 16, 2019 by Martin Armstrong

QUESTION: Marty, You are wrong. The US Treasury can create the money as the Constitution says it can. Article I, Section 8, Clause 5. The Congress shall have the Power to coin Money, regulate the Value thereof, and of foreign Coin, and fix the Standard of Weights and Measures.

To coin is used as a verb. At the time the Constitution was written, to coin money meant to create or to make money. Today’s Dictionary defines to coin as a verb meaning to make or to invent.

Why did you fail to mention this in your Blog today?

TD

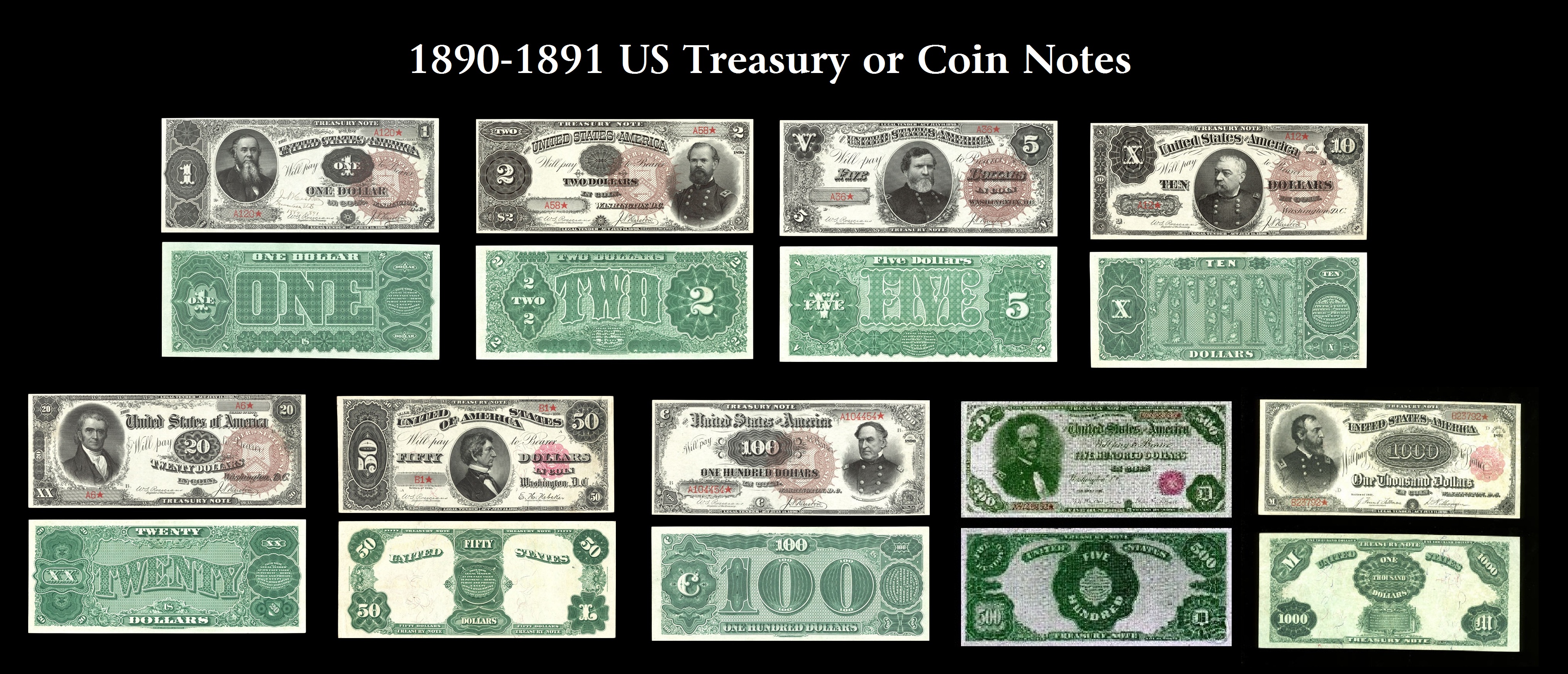

ANSWER: Yes, you are correct. I suppose I was referring to the 99.99% of the money supply rather than the coins put into circulation by the US Treasury. President Nixon only closed the gold window in 1971. He did not demonetize “gold” as money under the Constitution. Yes, technically the US Treasury can coin money, but it coins today’s coins. The Fed does not do that. The coinage it creates is minimal in comparison to the overall scheme of things. Since 1913, the printing of currency has been delegated to the Federal Reserve. Prior to 1913, the Treasury issued the paper currency which was backed by coins.

This was the last issue of paper currency issued by the United States Treasury in 1913, the year that the Federal Reserve Act was passed.

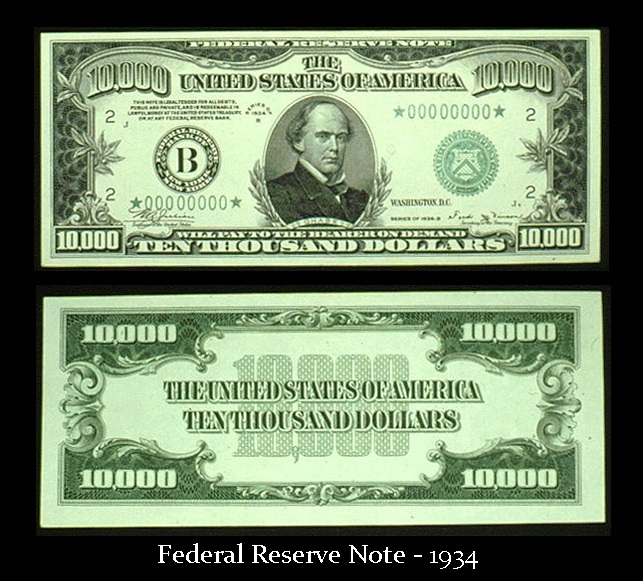

Note that in 1934, the Fed actually issued $10,000 bills

Sweden Implanting Chips in Your Right Hand to Eliminate Cash

Armstrong Economics Blog/The Hunt for Taxes

Re-Posted Jul 15, 2019 by Martin Armstrong

There have been many people who fear the forecasts of the Bible’s Revelations and the sign of the Beast that no one will be able to buy or sell without receiving “a mark on their right hand or on their foreheads, and that no one may buy or sell except one who has the mark or the name of the beast, or the number of his name” (Revelation 13:16-17). Now you would think that someone would be concerned about mimicking that forecast. That does not seem to stop the trend to implant chips in your right hand which is your debt/credit card on a chip about the size of a grain of rice. All you do is wave your hand and you just paid for everything.

Of course, there is a slight problem. The powers that be know who your are, where you are, and you have surrendered all privacy. Perhaps there is no stopping this trend. The governments are is such desperate need of taxation and Quantitative Easing has failed because they argue people withdrew their case from the banks. They have ended bailouts in Europe and the future head of the European Central Bank, Christine Lagarde, is a champion of eliminating money and believes that each country should create their own cryptocurrency and all freedom will come to an end.

This very idea of implanting chips into your hand and eliminating all physical money is a dream come true. I believe it will become one proposal on the table in 2021-2022. Our computer which show major confrontations arising into 2032 which will also involve religion, certainly seems plausible after 4,000 people have accepted chips in Sweden who think this is cool.

How Long Can Artificially Low Interest Rates be Maintained?

Armstrong Economics Blog/Interest Rates

Re-Posted Jul 15, 2019 by Martin Armstrong

QUESTION:

Dear Martin,

First let me thank you for your paradigm shifting blog and the incredible conferences you and your team put together. They really are on a level all their own.

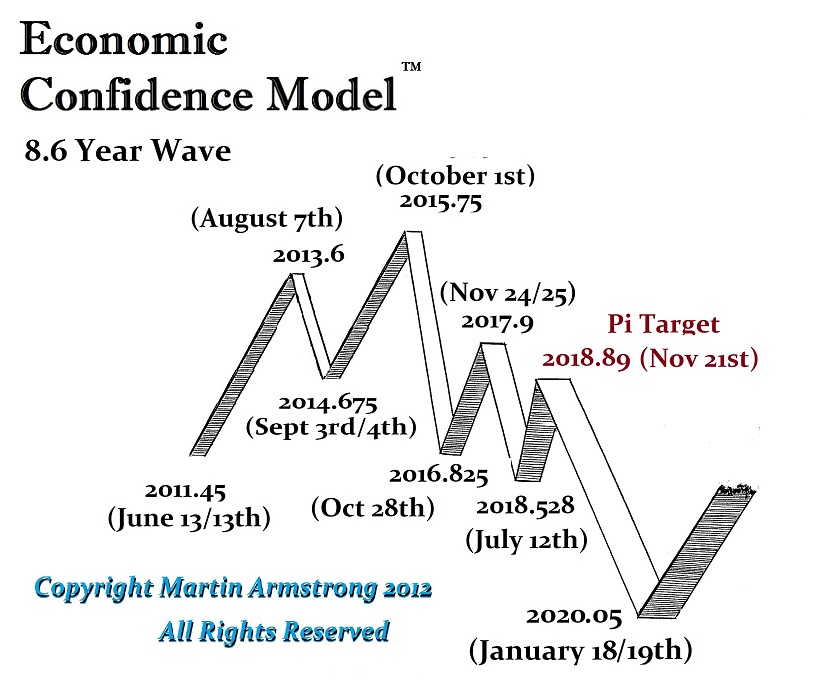

As we approach the next turning points in the ECM it seems that there are tremendous cross currents favoring both inflation and deflation. Given the extremely high debt rates of nearly every country in the world and even a large swath of the corporate world, some degree of moderate to even high inflation coupled with continuing low interest rates seems like the most likely path that central banks and governments will attempt to engineer. This path would avoid the deflation and societal instability that massive defaults would bring while quietly erasing the debt burden. I recognize, this path still leaves the pensions in a crisis, but that is a long slow problem primarily effecting a population group well past their prime years for fomenting revolt.

Of course the historical record shows that inflation is generally, perhaps even always, accompanied by high interest rates in the market.

I was wondering if there has been a historical precedent for moderate inflation (say 8-10% per year) combined with low interest rates on debt (sub 5%). It seems this would be the goldilocks path out of the increasingly ugly position in which the world finds itself. Leaving one to wonder if anyone has ever been able to accomplish such a combination for long? Any ideas how such a strategy would be accomplished, and what the probabilities are that our central bank and government will be able to pull it off?

Sincerely,

JU

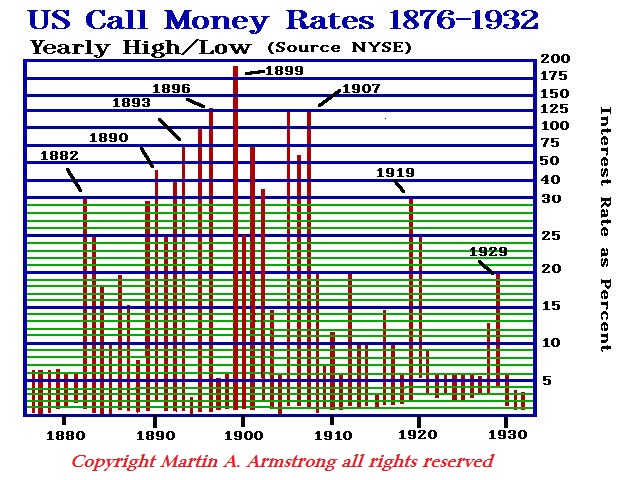

ANSWER: This is why we really, really, really, really, need Socrates. There is no such precedent to which we can refer to in history because this is the first time post-World War II when governments have operated full-blown in this new age of Keynesian-Marxism. By that, I mean that interest rates were always a free market. It is true that there were usury caps to interest rates as far back as the Babylonian days. There was a distinction between lending in commodities and lending money. The former carried a maximum interest rate of 33.33%, whereas the latter the usury rate was 20% (Robert P. Maloney, “Usury and restrictions on interest-taking in the ancient Near East,” Catholic Biblical Quarterly 36.1 (Jan. 1974): 1-20.).

For whatever reason, there are those in the Deep State controlled by the New York banking oligarchy who really want us to shut off this research. They seem to believe that they can maintain everything as long as we keep quiet. That is absurd. What will be, will be. The free markets always win. We are in a very dangerous game here where the entire world is at risk because of a desperate attempt to manipulate the economy by maintaining artificially low interest rates to keep the government budgets in the West under control. This is going to fail!!!!!!

Instead of trying to reform, they are digging in their heels and attempting to keep a failed Quantitative Easing theory in play even after more than 10 years of obvious failure. As the Economic Confidence Model turns, everything they are trying to do will backfire. I have no doubt they will blame me, and once again, claim they would have succeeded but too many people listened to me. That is such a BS line, it is no longer funny. They can kill me and it will not change anything. The monetary system as we have known it will blow up in their face. This is IMPOSSIBLE to maintain.

You cannot keep interest rates at artificial lows and expect this game to continue. What will happen is there will be a great awakening. Once the serious money realizes the emperor has no clothes, they will lose all confidence of the people. The next 8.6-year wave will be inflationary because of a collapse in confidence. I am sure I will be the scapegoat and the fake news will keep that image in motion and support the Deep State as they always do. As they say, Bloomberg News has NEVER exposed the manipulations of the banking oligarchy. I even sent a copy about the SEC controlled by Goldman Sachs to David Glovin who will never report on the issue because their income is paid for by the same oligarchy. That is why we are on our own

Why Are Equities so Disconnected from Economics?

Armstrong Economics Blog/ECM

Re-Posted Jul 12, 2019 by Martin Armstrong

Normally, equity valuations reflect the present value of future cash flows that are primarily a function of current cash flows, growth expectations, and then the discount rate. Most fundamentalists will look at the cash flow generation in both the short and long-term. With equity valuations at their record highs, investors, in theory, are showing confidence in short-term cash flows not declining materially. The interpretation normally would be that they are betting on no recession and on stable long-term growth. However, is this analysis just sophistry?

The probability of a recession is much higher than what global equities are currently reflecting. Then there are people pointing to the yield curve and yelling, “See, a crash is coming!” They argue this is a leading indicator, sending the strongest warning signals to investors. Nevertheless, history begs to differ with that analysis for it has often shown a final bullish move in equities despite clear evidence of an oncoming recession. Is this precisely what we are facing? Others point to the Fed, claiming that the first rate cut is often a reliable signal that a recession is coming, which reduces short-term cash flows and raises return expectations as investors become more risk-averse.

There are those who look at all of these factors and then argue that long-term profit growth expectations are way too high. Others argue that corporate debt is too high and we have also reached debt saturation, especially technology companies.

All things considered, we are facing a slightly different future. Doing simple correlations of equities to interest rates reveals that the share markets have NEVER peaked twice with the same level of interest rates because the real issue is the differential between the cost of money and expectation of inflation or future price gains. We are in a similar pattern where interest rates are so low that even a 3% dividend from shares looks fantastic. When we look at the extremes, we also see that the PE ratio hits its extremes, not at speculative booms, but at the bottom. There comes times like in 2009 where capital no longer trusts the banks, governments, and is just looking to get its money back intact. This is when they will buy blue-chip shares without expectation of future profits and cash flow, but the preservation of capital. So while many see the share markets as totally disconnected, perhaps they need to look at the other side of the equation — who do you trust?

Why Nobody Wants to Forecast the Business Cycle

Armstrong Economics Blog/ECM

Re-Posted Jul 12, 2019 by Martin Armstrong

COMMENT: It is fascinating how your work has been so accurate on forecasting the business cycle, yet you are probably the most ignored by the mainstream media. The only possible reason for this is that they are not interested in someone who can forecast the business cycle when the general belief is that governments can manipulate it.

Keep up the great work

HS

REPLY: You are correct. They are not ready to accept that the business cycle can be forecast. That undermines politics as we know it today.

The OECD’s leading indicators on the global economy are still declining with the latest numbers marking the 19th consecutive monthly decline. The global economy is at its weakest point since July 2008, and the probability of a recession is still elevated and not fully reflected in equity valuations. South Korea, one of the world’s economies most tuned to globalization, is showing significant weakness with its leading indicators declining for 25 straight months to levels not seen since early 2012. The South Korean economy has historically been one of the best indicators for the global economy, so we expect more pain to come in the second half of the year.

The only major economy that has turned positive among the OECD’s leading indicators is China. This is not a big surprise, given the recent major improvement in the credit impulse, although it is still negative. But China’s improved industrial sector is driven by a major national push from the government and is likely driving domestic demand more than global demand. Meanwhile, the country’s car sales (which serve as a proxy for the consumer sector) remain weaker than at the bottom of the financial crisis, highlighting elevated uncertainty among Chinese consumers. In fact, May data shows that sales growth weakened again.

The problem is the entire Keynesian-Marxist agenda whereby governments believe their own propaganda. Nobody is willing to publicly look at our model because it highlights the entire problem with the assumption that governments are in control when they are just aggravating the trend.

Were Banker Ever Prosecuted During the Great Depression?

Armstrong Economics Blog/Rule of Law

Re-Posted Jul 12, 2019 by Martin Armstrong

QUESTION: I was told that none of the big bankers during the Great Depression went to jail either. Doesn’t the government understand that this is the very image of draining the swamp?

DK

ANSWER: The bankers own the reign of government from the courts to the White House. In the years that followed the 2008 financial crisis, the Securities and Exchange Commission brought charges against more than 150 people and institutions and won $2.68 billion in penalties. The SEC loves big fines. Keep in mind if they charge the individual banker, it will never be profitable. Charge the bank and promise no criminal prosecutions and you get the big bucks. So yes, not one of the bankers went to jail from that financial meltdown that they created which left 8.8 million Americans jobless. It also led to a $700 billion government bailout to save the bankers which never stimulated the economy.

Your question was whether it was this way during the Great Depression. Virtually no bankers were jailed in the wake of the Great Depression. However, they were at least charged but beat the criminal charges.

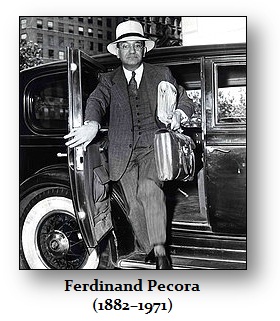

Beginning in 1932, the Senate Committee on Banking and Currency opened a public inquiry into the stock market crash. The Pecora Commission, as the investigation came to be known, led to indictments for several of the era’s finance giants. However, this was all before the SEC and Glass-Steagall, which Goldman Sachs had the Clintons repeal. Since banking laws did not guard against the kind of speculation that fueled the crash, most escaped prosecution for they did not violate any law.

Charles Mitchell was the president of the National City Bank, now Citibank. Mitchell built the bank into the nation’s largest by splitting it into two branches which fed each other. One half became its investment arm, while the other was its banking arm. Hence, this was the reason Glass-Steagall was enacted. The banks sold investments to clients, often financed with money borrowed from the bank. They also knew, as they did in 2007-2009, that the investments were toxic. When the market crashed, clients lost everything after listening to the advice of the bankers and the banks would often collapse. Mitchell resigned and admitted to the Pecora Commission that he knew his bank was pushing bad investments onto its clients, as was the case many alleged with Goldman Sachs in 2007. Mitchell was indicted for tax evasion but was ultimately acquitted. He paid a $1 million civil fine instead.

Then there was the utility magnate Samuel Insull who also appeared before the Pecora Commission. He fled the country in June 1932, which was about eight months before prosecutors brought fraud charges against him. Insull pioneered the concept of a holding company, in which one company holds partial or complete interest in another company. At the height of his success, Insull controlled businesses worth as much as $500 million in assets with just $27 million in equity. When the crash hit, 65 of his businesses failed, ruining 600,000 investors. Insull was eventually returned to the U.S. nearly two years later but he also beat the charges.

The Pecora Commission went after the individuals. The SEC and Justice Department protect those bankers today. The Securities and Exchange Commission is now controlled by the people from Goldman Sachs. The likelihood of the SEC ever prosecuting anyone from the banking industry is ZERO,

BOJ Trapped – How will the Nightmare End?

Armstrong Economics Blog/Japan

Re-Posted Jul 11, 2019 by Martin Armstrong

Bank of Japan (BOJ) Governor Haruhiko Kuroda publicly stated that it may maintain ultra-low rates for a further period of well over a year. However, he also warned against the idea of propping up the economy through unlimited money printing to finance government spending. That may sound nice, but the Bank of Japan is trapped. Its holdings of the national debt have reached nearly 50%. The BOJ modified its forward guidance or pledge on how it will guide future monetary policy. It stated that current very low interest rates will continue at least until the spring of 2020. However, there is ZERO hope without the BOJ buying the government debt that interest rates will rise dramatically and a financial crisis will be in the making.

The BOJ will keep rates low for an extended period of time for they have no choice. There is no way out of this nightmare and the real inflationary cycle comes when the majority wake up and realize that the emperor has no clothes, and that means the central bankers worldwide

EU Refuses to Negotiate Fairly with Britain – Demands of a Customs Union

Armstrong Economics Blog/BRITAIN

Re-Posted Jul 11, 2019 by Martin Armstrong

QUESTION: Mr. Armstrong; could you explain this whole Customs Union issue in BREXIT? Some see it as a great idea, others say it is surrendering sovereignty to Brussels.

SN

ANSWER: A customs union, some claim, would help businesses that send goods back and forth to the European Union. So it would be of interest to Britain’s manufacturers, particularly the automobile industry. They also claim that it might ease complications of the much-hated Irish backstop plan, which is intended to eliminate the need for hard border checks between Northern Ireland and the south.

However, a customs union would allow goods to flow easier, in theory, but it would not allow for frictionless trade. It would keep the tariffs Britain pays on goods that cross the border equal to those that countries in the European Union pay currently but at a huge cost. The goods being traded will still need to meet the same product standards that apply throughout the EU. That is the key.

Turkey is a member of a customs union with the EU, but it is not a member of the EU bloc itself. Therefore, trucks are held up for hours as guards check for permits and make sure the products being transported are in compliance with regulations set in Brussels. They would do the same with a vengeance with Britain. A customs union would not cover trade in services, finance, trading, like legal counsel and information technology, which are by far the largest sector of the British economy – not trucks going back and forth.

The devil is in the detail of a customs union. The EU demands that to be in a customs union they must surrender their sovereignty to Brussels and will be prohibited from making their own trade deals. That means Britain could not enter trade deals with China or the United States simply because it does trade with the EU. This defeats the entire understanding of BREXIT.

France Refuses any Negotiation on BREXIT & Demands to Punish Britain

Armstrong Economics Blog/France

Re-Posted Jul 11, 2019 by Martin Armstrong

Paris is adamant that the EU should not renegotiate the Brexit deal. The French want to punish the British at all costs, and that means at the expense of their own employment and markets. Amélie de Montchalin, France’s minister for European affairs, said, “If the UK wants to leave the EU, and in an orderly way, the withdrawal agreement is the deal on the table, which has been negotiated for over two years. We’ve also said that the political declaration on the future relationship is open to discussion if the prime minister had a majority.”

France’s position is to end trade by blocking trucks from Britain through the ports of Calais and Dover. They are more interested in punishing Britain than anything else. They refuse any negotiation whatsoever. British trucks will not be able to board ships in Dover in a no-deal BREXIT scenario if they do not have the correct customs paperwork, following a deal between the Port of Calais and Channel shipping lines. Any excuse will prevent trucks from delivering anything to Europe.

Goldman Sachs Controls the SEC

Armstrong Economics Blog/Corruption

Re-Posted Jul 10, 2019 by Martin Armstrong

With the departures of Gary Cohn, Steve Bannon, and Dina Powell from the White House, has Goldman Sachs’ initial influence on the Trump Administration dwindled?

The wrote: “Jay Clayton, Goldman Sachs’ past and likely future lawyer, is not alone in the Trump-Goldman axis at the SEC. To better understand how corporations consistently manage to maneuver ostensibly independent agencies in their interest, it is instructive to consider one of Clayon’s “Senior Policy Advisors,” Alan Cohen.

Before Cohen joined the SEC in the summer of 2017, he “served as Goldman’s compliance head for 13 years, after joining the bank in 2004 as a partner from law firm O’Melveny & Myers.” It makes sense that Clayton would reach out to Goldman for senior advisors — not only did Clayton represent Goldman while Cohen was helping run the megabank, Clayton’s wife worked at Goldman Sachs until Clayton’s ascent to the SEC. It’s a small and quite rich circle in which the likes of Clayton and Cohen run.

But while the “how” of Cohen’s rise to SEC prominence is sadly intuitive, the “what the heck” nature of the hiring merits significant explication.

First, what does it mean to have been in charge of “compliance” for Goldman? Per their website, “the global compliance division is dedicated to protecting the reputation of the firm and managing risk across all business areas.” The compliance division is supposed to “ensure compliance with regulatory requirements and determine how the firm can appropriately pursue global market opportunities.”

How did Goldman do under Cohen’s reign? Not well. Not well at all.

Recent weeks have brought an avalanche of news about how Goldman Sachs is at the center of an epically corrupt Malaysian state investment fund called 1MDB. Indeed, just this past Monday (November 12th, 2018), “Goldman Sachs shares slumped the most since November 2011 after Malaysia’s finance minister demanded a full refund of fees it paid the bank tied to a doomed investment fund.”

Why is Malaysia furious at Goldman Sachs? Goldman played a key financial architecture role in the 1MDB fraud. Their engineering assistance to the scheme has already led a senior Goldman banker to plead guilty and has touched Goldman CEO Lloyd Blankfein (Blankfein twice met with the Malaysian fraudster, Jho Low)

It was Cohen’s job to ensure Goldman bankers did not do several of the specific acts that “former senior Goldman Sachs banker Tim Leissner pleaded guilty to,” launder money and violate the Foreign Corrupt Practices Act by paying bribes.

These actions by Goldman under Cohen’s watch are also actions governed in part by the SEC itself. Cohen failed to prevent crimes policed by the SEC, and now he is a senior figure at the SEC.

Given the laxity of current ethics law, so long as Cohen doesn’t specifically meddle in an investigation into Goldman Sachs like 1MDB, he needn’t recuse. That means Cohen can advise on broader enforcement priority issues that implicate SEC policy toward money laundering and the Foreign Corrupt Practices Act, even if he cannot interfere in this specific investigation.

The corruption of Goldman that 1MDB represents is, of course, not the exception but rather the norm for Goldman under Cohen’s watch.

For instance, the SEC is now investigating allegations from a former senior investment banker at Goldman Sachs, James Katzman. Katzman “raised concerns about what he viewed as unethical conduct at the bank” via Goldman’s whistle-blower hotline in 2014. Rather than take Katzman’s concerns seriously, “David M. Solomon, who is now Goldman’s chief executive, urged Mr. Katzman to move past his complaints, and he left the firm in 2015.”

Indeed, Katzman initially felt silenced by a confidentiality agreement with Goldman. A serious compliance director would seek to act on the concerns of a whistle-blower, rather than stifle their complaints.

There are other issues. For instance, one can hardly avoid laughing at the dark comedy of the Forbes headline, “A Bad Omen When Goldman Sachs’ Compliance Staff Is Charged With Insider Trading,” noting that “Perhaps Goldman Sachs needs to hire compliance staff to monitor its compliance staff.”

However, the biggest issues at Goldman under Cohen’s watch cut to the core of the Great Recession.

Consider the take of the Justice Department on Cohen’s handiwork. “The Justice Department, along with federal and state partners, announced today a $5.06 billion settlement with Goldman Sachs related to Goldman’s conduct in the packaging, securitization, marketing, sale and issuance of residential mortgage-backed securities (RMBS) between 2005 and 2007.”

If you watched The Big Short and came away unimpressed by the ethics of Goldman Sachs, or if you agree with Matt Taibbi’s colorful claim that the “world’s most powerful investment bank is a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money,” then you think Alan Cohen failed at Goldman Sachs.

But enough about the past; what is the SEC currently doing that would make Clayton and Cohen especially valuable to Goldman Sachs?

Per Bloomberg, one big priority for Wall Street is to make sure that European investor protections “don’t spread to America.” Bloomberg notes that the “dustup is playing out behind closed doors in Washington at the Securities and Exchange Commission, where brokers want the agency to make clear they can continue combining the cost of financial research and trading in one bill for U.S. customers — the practice that is being banned in the European Union.”

And who is at the center of this closed door effort by the SEC to ensure Goldman and comparable firms can reap profits European regulators have determined are unfair? Alan Cohen, whose hiring was announced by a press release stating that Cohen was hired in part to advise Clayton on issues including “new European Union regulations (e.g. MiFID II).”

Pro-investor groups and large state pension systems that manage money for government employees object to this set up.

Typically, Goldman Sachs is the favorite in a dispute against “investor groups” and “state pension systems” because Goldman is richer, more powerful, and savvier about the inner workings of the government than its opponents.

Hopefully, that is not always going to be true.

The Revolving Door Project has announced an Independent Federal Agencies Leadership Tracker because agencies like the SEC are obscure to nearly everyone who doesn’t have business before them. In other words, banks like Goldman Sachs wield influence over the SEC because it matters enormously and directly to their bottom line. Figures like Alan Cohen are not exceptions but the norm.

That should change.

The Revolving Door Project is committed to educating the broader public about issues previously rendered obscure by entrenched banks operating exclusively in their self-interest.”