I reported how BlackRock is now the largest landlord in the US. Institutions have purchased hundreds of billions in real estate across the nation and have no plans to sell because rentals are a lucrative venture. Inventory is at a historic low and people simply cannot find a place to live if they need to relocate. Rental price gouging has reached astronomical levels and demand far outweighs supply.

There are eight prospective renters for each available apartment in the US, and the average occupancy rate is 94.2%. Of those occupied leases, 60.7% chose to renew. New housing grew by a measly 0.43% as building costs have increased substantially. The high-density state of New Jersey has become the most competitive real estate market in the US. This is particularly true for the northern part of the state, which is no surprise as the average cost for rent in NYC is $5,186 monthly. That price tag makes places like Los Angeles look cheap, with an average rental price of $2,600. Miami, the new Wall Street of the south, has become the second most competitive market in the US. Apartments in Miami-Dade County last an average of 33 days on the market if a unit even becomes available.

Housing is completely unaffordable and people with good-paying jobs are struggling to find a place to live if they do not already own. Purchasing property was once the smart financial choice, but that is out of reach for the average person. In fact, over three million Americans earning over $150,000 annually still choose to rent as there is simply no alternative at this time.

Rentals across America are almost at total capacity. The typical person locks in a 12-month lease, but the landlord (in most states) can raise the price at the end of that term and there are little protections for residents. In fairness to the landlords, their costs have increased substantially as well in terms of taxes, insurance, and maintenance. The price of a renewal increase is typically lower than what it would cost to relocate, aiding in the decision for the majority to renew their leases.

Where I live, we also face seasonal rental price gauging. Off-season one-bedrooms in the Tampa Bay area are over $2,000 monthly and rising. But once the “snow birds” return during the winter months, prices increase substantially. There is a 13% tax here on short-term rentals as well, but finding a full 12-month lease is increasingly difficult.

Adding to this crisis is the mass influx of migrants as cities across the nation develop ways to house tens of thousands of people at the expense of taxpaying citizens. Landlords typically require renters to earn 3X the monthly rental price as well, forcing many to leave the cities and more desirable areas even if they earn a good living.

Shelter costs are unsustainably high for both buyers and renters. People cannot find a place to live. Those who rent often become stuck in a cycle of renting perpetually, unable to save as all their income goes toward shelter.

Anyone familiar with the housing market conditions post-pandemic knows that cash buyers and institutions consistently outbid the average buyer. I know a realtor who has spoken primarily to consultants working on behalf of companies, and they’re willing to purchase properties over-market on a consistent basis. They know they can buy these properties and rent them out for a fraction of what they paid because they have the liquidity to do so. Currently, BlackRock is the largest landlord in America, with over $120 billion in residential real estate.

BlackRock has invested significantly in mortgage securities since the pandemic. The company insists that they are not purchasing single-family homes, meaning they’re not flipping homes to resell. “Our focus is on building single-family rental housing that can be managed and operated similar to multifamily properties with dedicated property management, leasing and amenities,” the company’s website states. “Additionally, BlackRock invests in multifamily properties, apartment complexes, and other residential real estate.”

The goal is to own as much land as possible so that the people can become perpetual renters. BlackRock also is part of the World Economic Forum and promises “sustainability” and “ESG integration,” and is a member of GRESB (formerly the Global Real Estate Sustainability Benchmark). GRESB is the global standard for providing and acquiring real estate and infrastructure in a sustainable way.

BlackRock noted that “displacement” from the pandemic and other economic downturns will provide a great investment opportunity. “In the near-term, we expect dislocation and opportunity, yet there is greater dispersion between markets and sectors with logistics of storage, high-quality residential, and data centers having emerged as clear winners, while hotel, retail, and student housing will likely face a longer road to recovery.” They’ve been on top of the downturn in real estate since the beginning. This is not limited to the US as they have investments and branches worldwide.

BlackRock is one of many institutions purchasing land and real estate at a rapid pace. Invitation Homes, a BlackRock investor, owns over 80,000 single-family rentals in the US alone. Again, the goal is to profit off of rental income. This is another reason inventory is at a historic low and will remain tight since most institutions do not plan to sell the real estate they have acquired.

There is no climate emergency. As I have been saying for years, the climate change agenda to end fossil fuels is merely a fraudulent cause intended to gain power. The Global Climate Intelligence Group (CLINTEL) is an independent foundation founded in 2019 by emeritus professor of geophysics Guus Berkhout and science journalist Marcel Crok. “The climate view of CLINTEL can be easily summarized as: There is no climate emergency.”Over 1540 experts respected in their independent fields have joined CLINTEL to spread the message that there is no scientific data to indicate that climate change is political propaganda.

“Climate science should be less political, while climate policies should be more scientific. In particular, scientists should emphasize that their modeling output is not the result of magic: computer models are human-made. What comes out is fully dependent on what theoreticians and programmers have put in: hypotheses, assumptions, relationships, parameterizations, stability constraints, etc. Unfortunately, in mainstream climate science most of this input is undeclared.

To believe the outcome of a climate model is to believe what the model makers have put in. This is precisely the problem of today’s climate discussion to which climate models are central. Climate science has degenerated into a discussion based on beliefs, not on sound self-critical science. We should free ourselves from the naïve belief in immature climate models. In future, climate research must give significantly more emphasis to empirical science.”

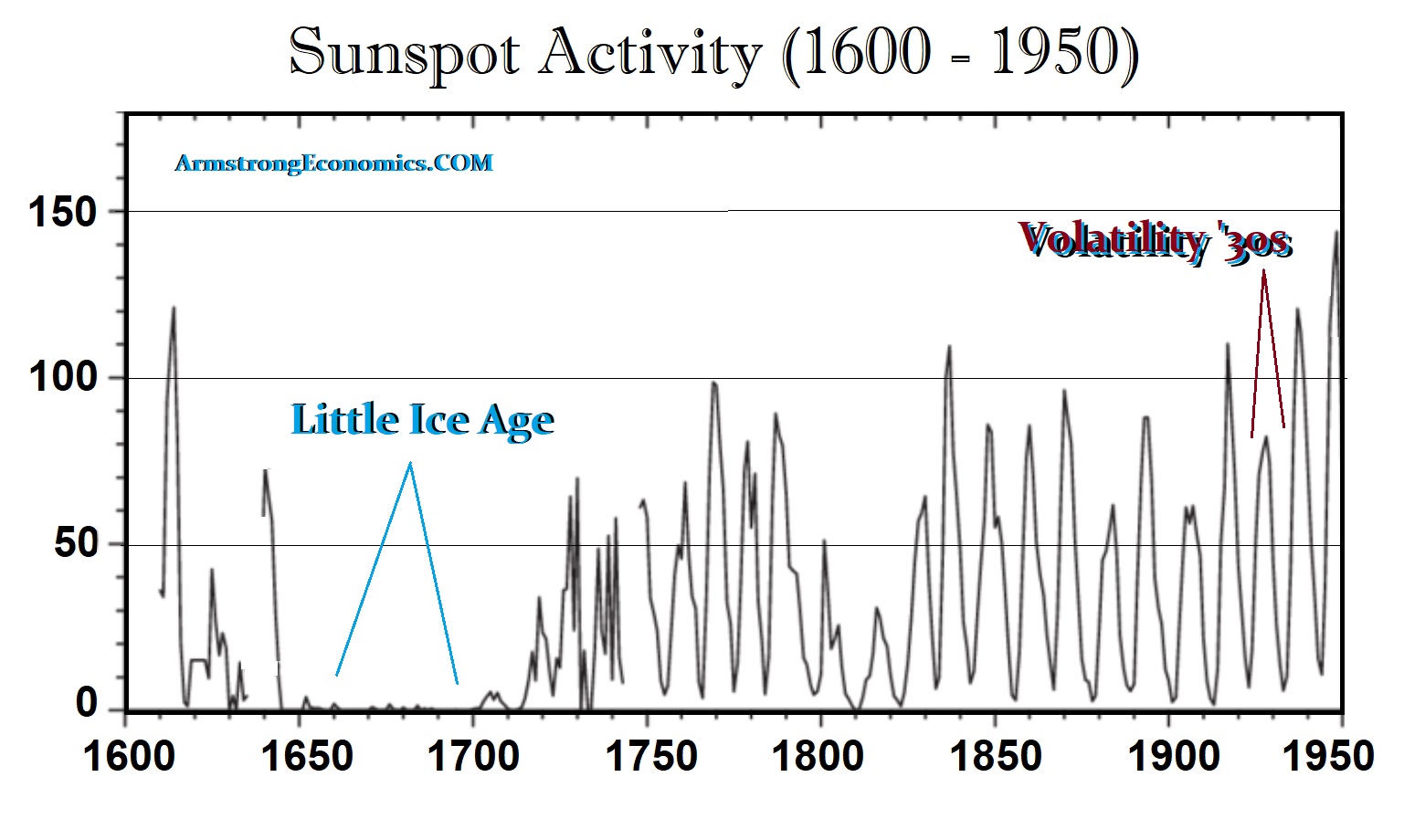

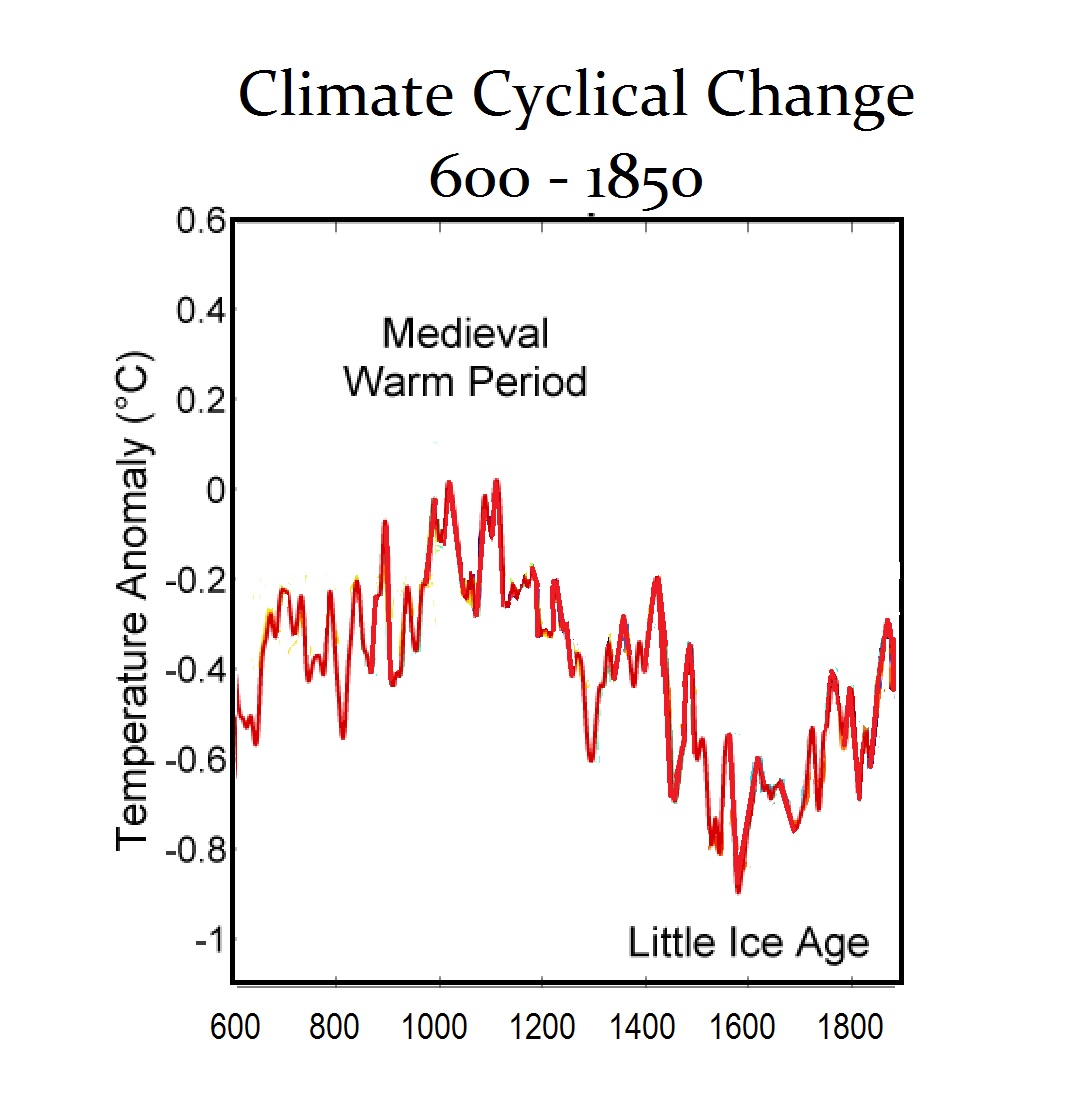

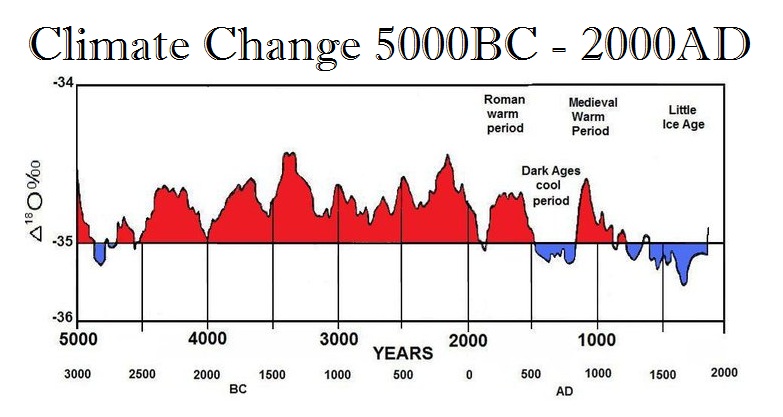

Climate science currently starts with a preconceived notion that leads to biased, untrustworthy studies, which are often funded by those with special interests. Climate experts have convinced the world that CO2 is a pollutant when it is essential to all life. They have also lied to us and claimed that natural disasters are somehow created by man when there is zero supporting evidence. Climate has varied on a cyclical basis, with the most recent Little Ice Age ending in 1850. We are experiencing nature’s cyclical pattern of warming and there is no case for alarm.”

We MUST question why governments across the world are fighting tooth and nail to eliminate fossil fuels and our way of life as we know it. Why are we following the World Economic Forum’s 2030 agenda to save a planet that does not need saving? Why are we allowing our elected officials to spend endless funds on an imaginary cause? Everything has a cycle, including the weather. So while the climate may be changing, there is absolutely nothing humans can do to alter the course of nature, and those stating otherwise are lying.

Posted originally on the CTH on April 14, 2023 | Sundance

Always keep in mind that retails sales from the Dept of Commerce [DATA HERE pdf] are always calculated in dollars. Inflation can artificially skewer retail sales if prices increase, and yet consumer purchases decline at a rate lower than the increase in price. Fewer units sold at higher prices can give the false impression of increased sales.

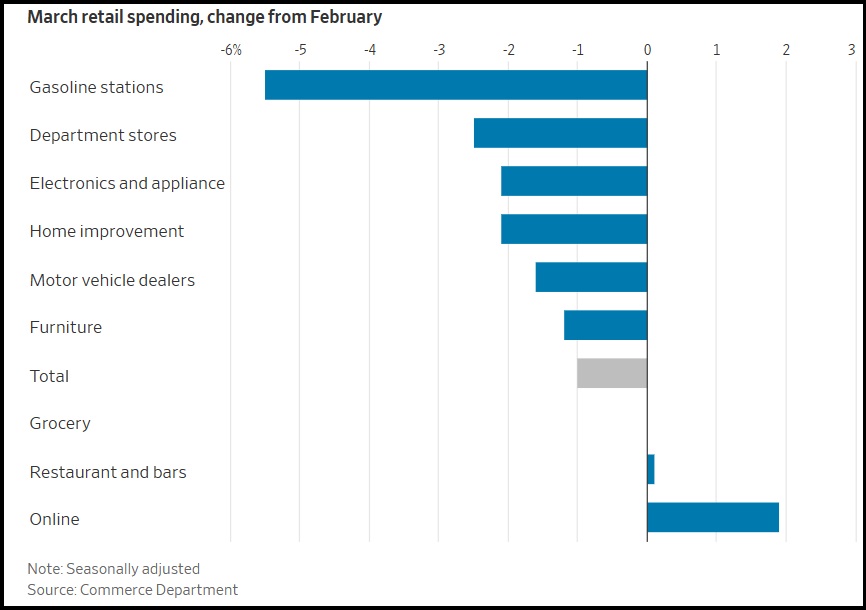

During an inflationary environment, when prices increase yet retail sales drop, there are substantially fewer units being purchased. Overall purchases at stores, restaurants and online declined a seasonally adjusted 1% in March from the prior month.

During the time measured gasoline was less expensive, so that led the drop in fuel sales; however, drops in dept stores (-2.5%), General Merchandise (-3.0%), electronics (-2.1%), and building supplies (-2.1%), shows another broad-based pullback of Main Street consumer spending. (pdf here)

These outcomes are in general alignment with what many people have shared via regional ground reports. Grocery store sales are flat despite major increases in grocery store prices (+10 to +20%). People are buying fewer grocery store units and making their food budget stretch as far as possible.

Durable goods are not considered essential, and sales of cars, electronics and department store products are much lower.

I am actually a little (pleasantly) surprised to see restaurant sales holding (+0.1%), despite the massive increase in fresh food costs. I thought people would eat out less, but the total decline in restaurant foot traffic seems to be in the single digits. I guess people can afford it more than I anticipated.

(Via Wall Street Journal) – […] The retail-sales report mainly captures spending on goods rather than most services such as travel, rent and utilities, offering only a partial picture of spending. The Commerce Department will release more complete figures later this month.

Spending on air travel was robust in March but outlays on other services like hotels declined, transaction data from Bank of America credit and debit cards showed. And the cost of shelter has increased faster than the overall rate of inflation, federal data show.

Some Americans have had to make adjustments to allow them to keep spending.

Recent data suggest many consumers are more cautious about purchases of goods they often have to borrow money to buy. In March, spending declined in big-ticket categories including vehicle sales, electronics, furniture, and at home-improvement and department stores.

“The current challenges in the used auto industry are well documented,” CarMax Inc. Chief Executive Bill Nash said on a call with analysts this week, “with affordability pressured by broad inflation, climbing interest rates, tightening lending standards and prolonged low consumer confidence.” (more)

The talking heads have been warning of a housing crash, but that is not what Socrates indicated. The 30-year fixed rate is around 6.89% at the time of this writing. Housing costs continue to rise, causing the costs of servicing mortgage debt to rise. Housing inventory is limited, and a recent report explains why we saw mass layoffs in the banking sector. The demand is still there and it is a sellers’ market. Cash is king when it comes to real estate for those who can afford it. Mortgage lenders are in trouble. In fact, only 32% of mortgage companies were profitable in 2022 compared to 98% in 2020.

The Mortgage Bankers Association (MBA) recently announced that independent mortgage banks and subsidiaries of chartered banks lost around $301 for every mortgage they financed in 2022. This marks a 113% decline from the prior year’s average and the first-time banks are seeing losses on mortgage products. This is not 2008 when banks handed out loans to anyone who asked.

“The rapid rise in mortgage rates over a relatively short period of time, combined with extremely low housing inventory and affordability challenges, meant that both purchase and refinance volume plummeted,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “The stellar profits of the previous two years dissipated because of the confluence of declining volume, lower revenues, and higher costs per loan.” Production costs reached a high of $10,624 per loan last year. Productivity was 1.5 loans originations per production employee, down from 2.5 per employee the year prior, and an indicator of why we are seeing layoffs in the banking sector. No one is refinancing at these rates either and most chose a fixed rate, as we saw what happened in 2008 with adjustable costs.

First-time mortgages reached an all-time high of $323,780 last year, up from $298,324, the largest annual increase since the MBA began collecting data. The increased cost of loans increased the cost of serving mortgages. The MBA expects volume to decline further in 2023 before rallying in 2024 and 2025. The banking crisis may lead to banks and lenders selling off their mortgage debts once they cannot afford to service the debt. Again, the housing crisis today is not relative to the 2008 crash.

The pension reform protests in France grew to new proportions. Protesters have not allowed the government to silence them. On Thursday, over 100 people stormed BlackRock’s office in Paris and nearly burned it down. “The meaning of this action is quite simple. We went to the headquarters of BlackRock to tell them: the money of workers, for our pensions, they are taking it,” a protestor told a CNN affiliate. The protest was organized and the message was clear.

We have seen a slew of failed protests in America where groups without leadership burn down the private property of their neighbors and small businesses. We’ve seen protests divided over the wrong causes, such as the nurses’ strike that failed because some felt the leadership was not diverse enough. Some protests, such as the BLM movement, became so obscure that no one even knew what they were protesting. Here, the Parisians are not allowing government mismanagement to change their retirement plans. It may seem like a small sacrifice to those without pensions, who could not dream of even retiring in their 60s, but the problem is much deeper than a change in the retirement age.

Governments historically target the people, who they see as the disposable Great Unwashed, when their plans fail. The French government believes the people should make a sacrifice due to the steep budget deficit. Across the world, governments are taking more from their citizens. People are asked to suffer to promote the climate change agenda, eat less meat, drive less, and even refrain from heating their homes. Inflation has made the cost of living unsustainable but that has not prevented governments from raising taxes and asking for more while we receive less. Give an inch, and they’ll take a mile (or a kilometer in this instance). This is why effective government opposition is essential to sustaining our fundamental rights. They will take as much as possible if we allow it to happen.

Posted originally on the CTH on March 23, 2023 | Sundance

At a certain point in the economics of the great pretending cycle, one must wonder what circles they live in.

Fed Chair Jerome Powell announced another quarter-point interest rate hike and simultaneously noted the banking crisis will likely lead to tighter credit and borrowing for businesses on Main Street…. thereby further reducing the U.S. economic output. Yet here we are again, and not a single economic or financial pundit is even talking about the origin of the inflation the Fed action is pretending to address, the spike in energy prices.

At the core of the Biden policy issue that creates inflation, is the energy policy that has driven oil, gas, home heating, electricity and manufacturing/farming costs through the roof. The blocking of energy resource development/production is the top issue leading to massive increases in consumer prices overall. The Biden energy policy is entirely ignored by a federal reserve attempting to shrink inflation.

Follow the bouncing ball of consequence.

Biden restricts energy development [Main St Suffers]. Prices skyrocket [Main St Suffers]. The fed raises interest rates in an effort to reduce the economic activity to meet the lowered production of energy resource development [Main St Suffers]. The result of the interest rate hike creates liquidity issues for banks holding treasury securities [Main St Suffers]. The banks then reduce credit lines, reduce lending and tighten borrowing to match their lowered liquidity [Main St Suffers].

The Fed then notes further increases in rates may pause as they await the outcome of restricted banking credit and lending from the rate hikes previously installed. Nowhere in any of this is anyone talking about the nucleus of the issue – the stupid energy policy. The great pretending continues in the West, while smiling panda lunches with Vladimir Putin.

[Transcript] – “At today’s meeting, the committee raised the target range for the federal-funds rate by a quarter percentage point, bringing the target range to 4.75 to 5 percent, and we are continuing the process of significantly reducing our securities holdings. Since our previous FOMC meeting, economic indicators have generally come in stronger than expected, demonstrating greater momentum in economic activity and inflation.

We believe, however, that events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses, which would in turn affect economic outcomes. It is too soon to determine the extent of these effects, and therefore too soon to tell how monetary policy should respond.

As a result, we no longer state that we anticipate that ongoing rate increases will be appropriate to quell inflation; instead, we now anticipate that some additional policy firming may be appropriate. We will closely monitor incoming data and carefully assess the actual and expected effects of tighter credit conditions on economic activity, the labor market, and inflation, and our policy decisions will reflect that assessment. (read more)

We are in an abusive relationship with our government.

Honest journalism has become a crime. I have appeared numerous times on Maria Zaric’s program, Zeee Media. Maria is a professional journalist who asks thought-provoking questions to the experts that appear on her show. Her content goes against the grain and traditional narrative. The Australian-based journalist has been questioning COVID, the Great Reset, governments, globalists, the war in Ukraine, and many other topics that are completely taboo in the mainstream media. They attempted to shut down her channel in the past. Now, she has been de-banked with no explanation.

“Do you shut down peoples accounts due to their political views by any chance?” Maria asked the bank representative, only to be met with silence. Maria had been banking with ING Bank for numerous years without issues. Her account was suddenly shut down shortly after releasing a story on domestic terrorism in Australia. ING Bank has been unable to explain why her account was canceled.

Interestingly, ING is a partner of the World Economic Forum. Maria has extensively covered the WEF’s agenda to “enslave humanity.” Is Australia secretly keeping track of journalists’ “social credit scores” to silence skepticism?

The idea of eliminating someone’s ability to bank is essentially eliminating them from society. We saw Canadado the same thing to those protesting the Trucker Convoy. Trudeau took things a step further by also de-banking people who simply donated to the cause. The Canadian government used the premise of money laundering as a way to coerce the banks into reporting any activity that could have been intended to help the protestors. I know of numerous people who were frantically attempting to remove their funds from the bank during this time.

As if the public needed more reasons to lose trust in the banking system. This is not limited to one bank or country. I discussed how banks have the ability to “cancel” someone after JPMorgan Chase de-banked the rapper Kanye West for antisemitic remarks. The bank acts as the jury and judge. Epstein was permitted to hold funds at JPMorgan Chase despite an ongoing pedophile ring trial. Bernie Madoff banked with JPMorgan Chase. The bank has secret ties to the Third Reich and helped the group funnel money through South America during World War II. Again, the bank acts as the jury and judge; anyone can be de-banked anytime for any reason.

Most countries may not openly have social credit scores, but they’re keeping tabs on us. They are keenly aware that resistance to this New World Order is building. So they are now using professional journalists as examples hoping that people will stop asking questions to learn the truth. That is one of the reasons why this blog is free of charge – you deserve to know the truth.

COMMENT: Marty; Two former Merrill Lynch traders were each sentenced to a year and a day in prison Thursday for manipulating the precious metals markets, the US Department of Justice announced. Of course, —- —–, which is forever bullish metals, claims they moved the metals in the “direction they wanted from 2008 to 2014.” It just seems that people claim it is always manipulation when they have been wrong. They only look at gold in dollars as you have said it’s a global market. They would have to manipulate all the currencies as well.

This latest affair of so-called manipulating trades during the day proves what you have been saying. They have always been gunning for stops during the day, but they cannot manipulate the trend between a bull or bear market. Do you think people will ever understand this is a global economy?

HD

ANSWER: I know. Unless people have actually been a trader, they will never understand the market. They will blame people like this to pretend they were not wrong. The problem is that this nonsense of manipulation is driving a stake through the heart of the market. Trading is like a poker game. Do you reveal your hand before everyone starts to bet? Sometimes you bluff, but the point is if you are bluffing, you have to stand behind your bet.

The mere fact that someone is blaming this type of “manipulation” for being the reason they have been wrong demonstrates that they know nothing about investing no less trading. The DOJ is now big on calling placing large “spoof” orders as manipulation. That is absurd and it is no more than bluffing in a poker game. This is the way all the markets have always functioned. Everyone would know where the stops were anyway. Sometimes they traded ahead of them using the stops as your risk point to exit the trade, and other times they would sell or buy to push the market through the stops when it was obvious that was even possible.

When I was trading in precious metals back in the ’90s, the biggest “local” dealer on the floor was Oni Morrison. He would do “spoof” orders all the time which I called “flash” bids or offers. The difference was he was good for it if hit. I was long one time in gold and I wanted out for the computer projected a crash was coming. But if you offer a thousand lots and the market was heading lower, everyone will read that and jump in front of you. That is how the Hunts went bankrupt. The Hunts did not know how to trade. Just as in poker, you cannot show your hand and expect to trade.

Oni would do “flash” bids or offers. I told my broker not to offer anything. I told him just to watch Oni and as soon as he would do a 1,000 flash to buy – say done! Sure enough, Oni was trying to push the market back up and he did one of his famous flash bids for 1,000 lots. My broker, Emerald Trading, instantly said “DONE!” Oni did it again, and they said “DONE!” Again he did a fash for 1,000 and again they said “DONE!” That was it. Oni was full and everyone began selling as the metals tumbled.

That is the way you have to trade SIZE. This is the very foundation of trading all markets for everything is just a poker game. To now call a “spoof” trade manipulation is just wrong. It is totally different when you do not have the backing. Now that would be a fraud and trying to manipulate the market for that moment – not changing the overall trend. But when you have the backing to honor your “spoof” it is just a “flash” bid or offer that you must stand behind when hit. That is just trading.

It is total BS to pretend that these guys manipulated the entire market. That is just absurd. Not even the central bank can manipulate the economy. You cannot “manipulate” a market against the trend for everything is connected. That caused the Panic of 1893 when the Silver Democrats overpriced silver. The Europeans hit the arbitrage and dumped silver in the US and took the gold back to Europe. That led J.P. Morgan to have to arrange a $100 million gold loan to bail out the treasury. That alone proved that you CANNOT manipulate ANY market against its trend for it will be arbitraged internationally – plain & simple.

Gold trading around the world in different exchanges is arbitraged. You cannot have gold $20 high in one market v another. It will be arbitraged instantly. Those who claim this as “proof” that the metals have been manipulated so that is why they have not rallied and why they have been wrong are fools who have been separated from the money. They will never understand the markets no less be able to see beyond the end of their nose. It will be instantly arbitraged.

The collapse of the Soloman Brothers was precisely that. They were putting in bids at the Treasury Auction using other people’s names to goose the market. They got caught and the firm was taken down. I know PhiBro from the ’70s and ’80s. They took over Solomon Brothers and brought that style of trading from the commodity pits to Wall Street.

This excuse by goldbugs that the metals were actually “manipulated” in their long-term trend, shows their hopeless ignorance of the markets and how they even trade. There is NOBODY who could possibly do such a thing for everything connected. As soon as the dollar would rise, the metals in terms of foreign currency would be so overvalued they would all sell and they will end up broke the same as the Silver Democrats bankrupted the country by overvaluing silver.

Trading internationally, with clients in all currencies, we have to look at each market in terms of their currency for that will determine if they made a profit or loss. Anyone who claims the metals have been manipulated and that is why they have not rallied is obviously oblivious to the world around them.

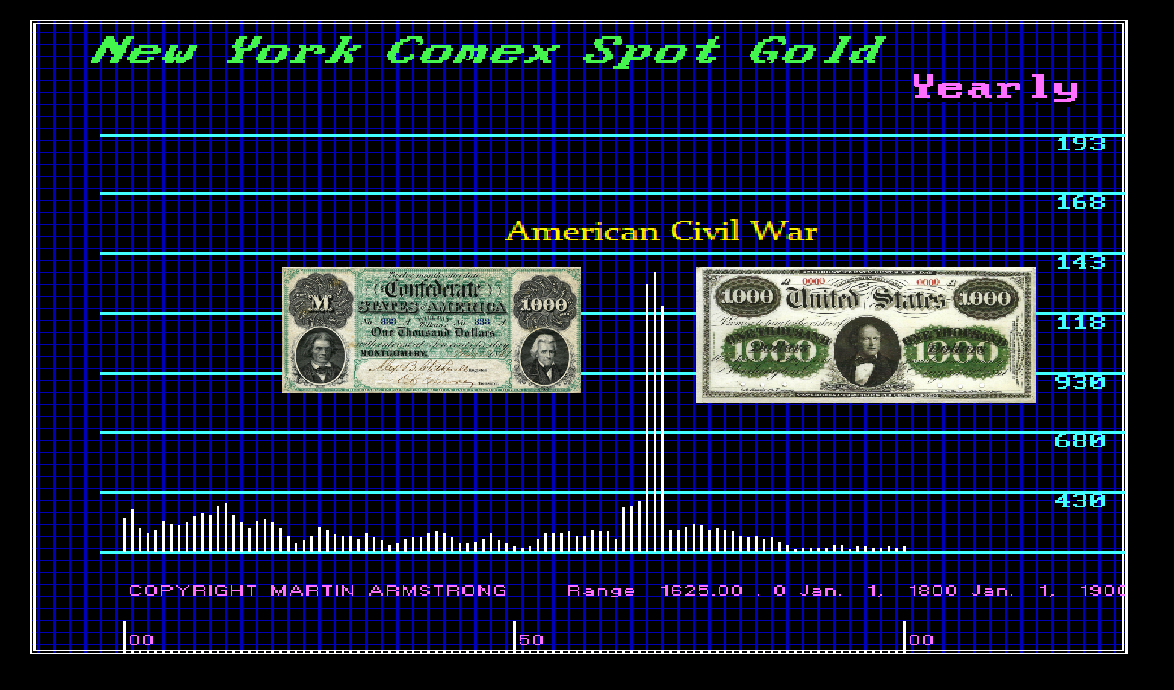

Gold does NOT rise with inflation – that is the sales pitch of a used car salesman. Gold rises in times of UNCERTAINTY with respect to the government. In times of war, it rises because it is NEUTRAL and you are not betting on who will win.

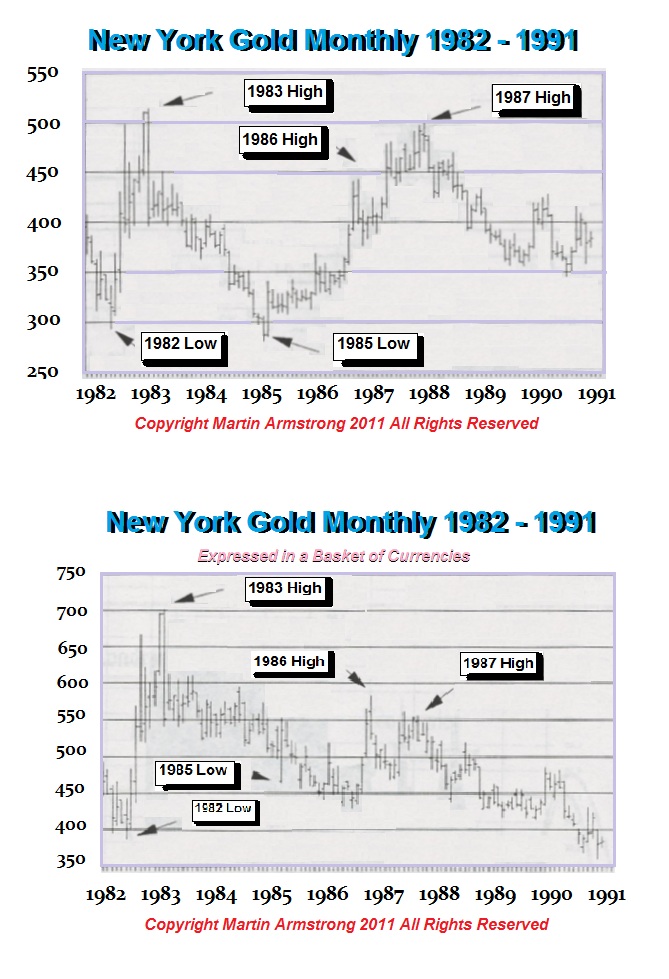

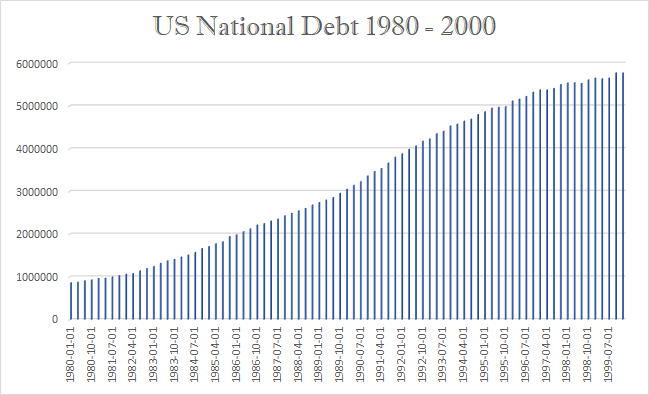

All we hear is that the debt is rising and therefore gold will explode. Once again, they offer no proof of their sophistry because there is no such proof. Gold declined for 19 years while the national debt climbed endlessly.

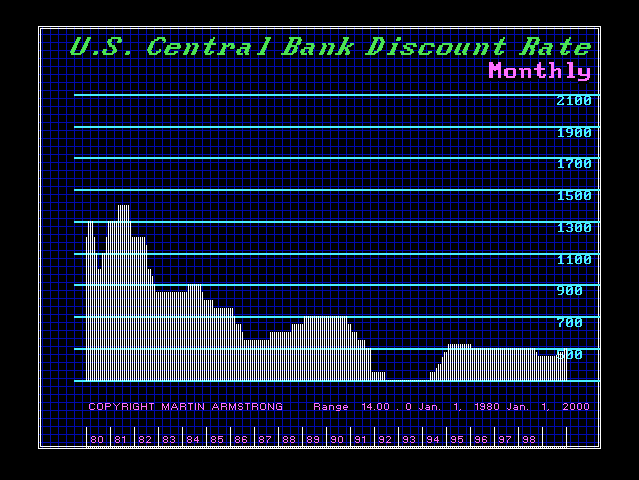

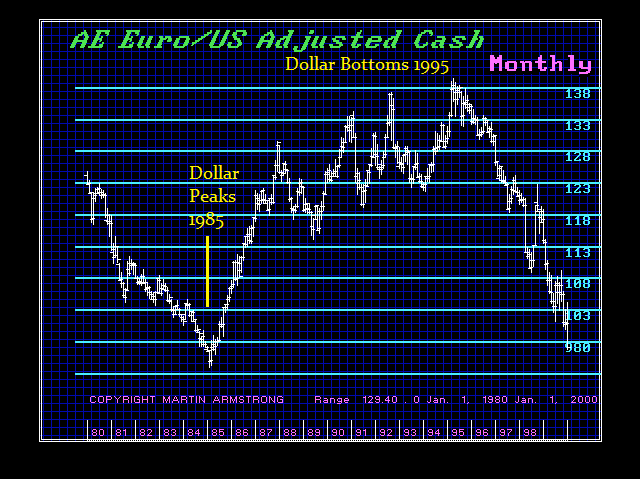

Then there is the myth about interest rates and gold that higher rates are bearish and lower rates are bullish. Well, interest rates peaked in 1981 and declined in 1994 before they began to rise marginally into 1995. Yet then contrast that myth with the performance of the dollar. There the greenback rose to a record high in 1985 but then declined for 10 years into 1995 all the while gold declined into 1999.

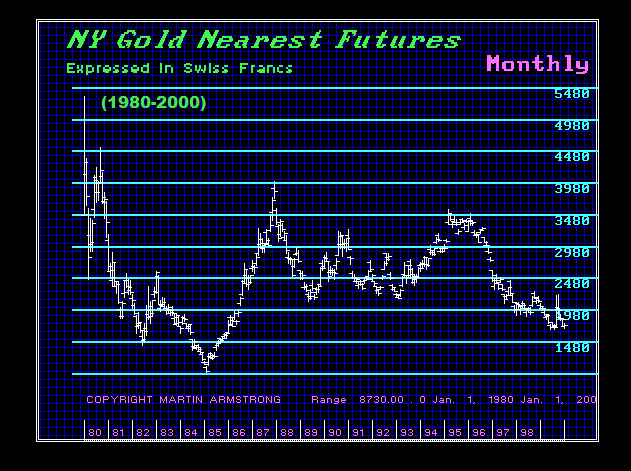

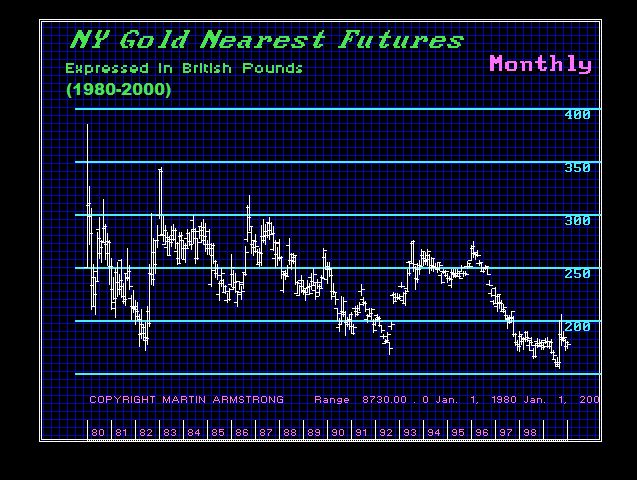

OK, so now let’s look at gold between 1980 and 200 in terms of Swiss francs and British pounds. We can instantly see that gold bottomed in 1985 in terms of the Swiss franc. In terms of British pounds, gold did not bottom until 1999.

People come up with theories all the time. However, they always try to reduce everything to a single cause and effect. They are doing that with climate change. They are telling the world it is CO2 that has changed the climate without ever addressing anything else.

The world we live in is not only complex, but it is also so dynamic it appears that no human can correctly forecast the future with an “I think” scenario. Sometimes they will be right, and others they will be wrong. Typically, they fail because they try to reduce the world to a single cause and effect.

Gold Rises with UNCERTAINTY with respect to the question of will the government survive its own madness.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America