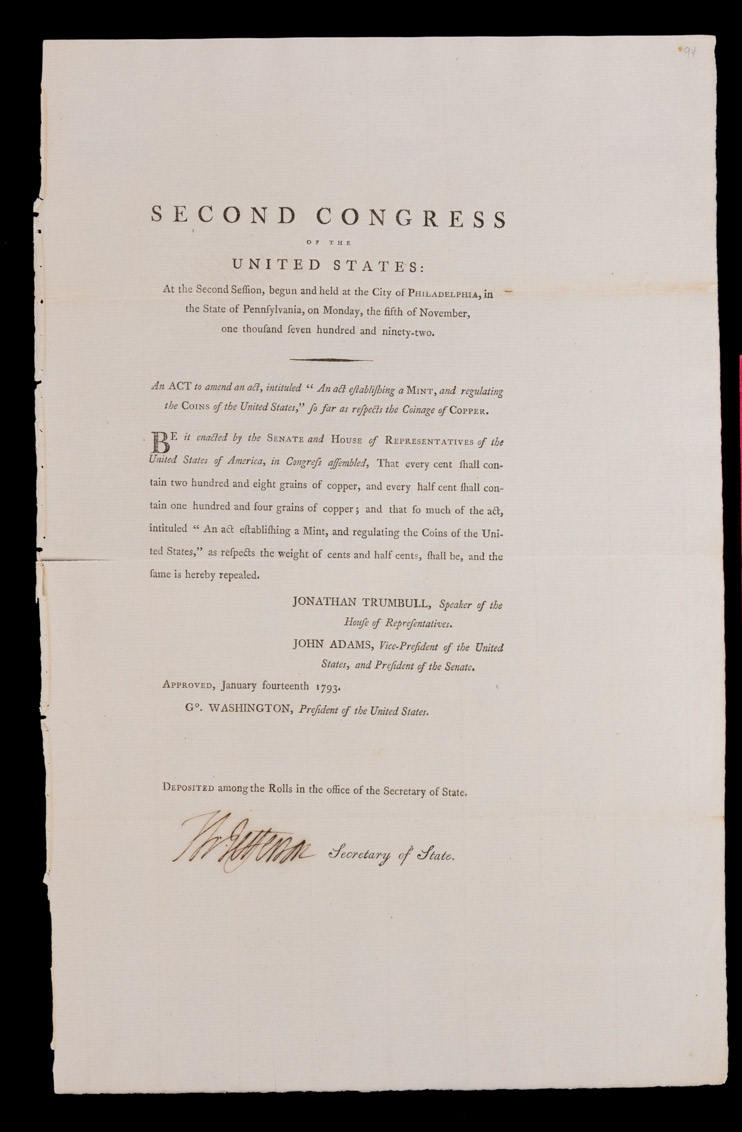

Thomas Jefferson Act of Congress Signed as Secretary of State, January 14th, 1793,

Second Congress of the United States (1743-1826)

As Secretary of State, Thomas Jefferson amended a previous Act, “establishing a Mint and regulating the Coins of the United States,” establishing the copper weight specifications for the first US coins issued in 1793 – the Cent and Half Cent. This is a document from our collection on the Monetary System of the World, establishes the birth of the US dollar authorizing the first issue of the coinage of the United States. It is unique and of tremendous historical importance.

The first copper coins created by the new United States of America were introduced into circulation in March of 1793. This document is signed “Th’ Jefferson” as Secretary of State and countersigned (in type) by George Washington as President, John Adams as Vice President and President of the Senate, and Jonathan Trumbull as Speaker of the House of Representatives.

“Second Congress of the United States: At the Second Session, begun and held at the City of Philadelphia, in the state of Pennsylvania, on Monday, the fifth of November, one thousand seven hundred and ninety-two. An act establishing a Mint, and regulating the coins of the United States, so far as respects the Coinage of Copper.”

“Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, That every cent shall contain two hundred and eight grains of copper, and every half cent shall contain one hundred and four grains of copper; and that so much of the act ‘An act establishing a mint, and regulating the coins of the United States,’ as respects the weight of cents and half cents, shall be, and the same is hereby repealed…. Approved January fourteenth 1793…”

Are you too poor for the basic human necessity of shelter in Biden’s America? The average home price in Q4 of 2022 was $535,800, according to the St. Louis Fed. If you live in a highly desirable area, expect to pay more. To simplify the math, let’s say that you are looking to purchase a $500,000 property. To heighten the fantasy, let us also pretend you are one of the rare Americans with zero monthly debt. This means that you do not have student loans, car payments, childcare expenses, medical bills, credit card debt, or any major outstanding bill. Fewer than 25% of American households are debt free and this number is rapidly dwindling.

Ok, so you decide to put 5% down on the house or $25,000 for a loan of $475,000. You manage to lock in a 6.7% interest rate for a 30-year mortgage under a conventional loan. Nationwide averages in real estate drastically undercut true averages due to the outliers, but the average annual property tax in America is around $3,000. I personally have not seen a property tax this low between FL or NJ, but I’ll attempt some optimism. After all, this should be a simple price breakdown that does not lead to a mental one.

We will average the PMI payment of 0.5% at $197.92 for 125 months. We will also incorporate the low home insurance average estimate of $1,000 annually. To be most forgiving in my calculations, I will also assume that your monthly HOA fee is $0. This is utterly impossible for anyone seeking to purchase a condo. In my area, the average HOA fee is $600 per month, and a $500,000 property will not afford you a single-family house. At best, you’d be lucky to find a two-bedroom property at that price point in my area. In contrast, home prices here were about 40% to 60% lower in 2019.

Therefore, the overall total monthly payment for a $500K home is $3,596.32. This home can be yours by 2053 if you close this year. Forget “starter homes” as once you are locked into a good rate, you will likely not leave. So how much income do you need to afford this monthly payment? The MAXIMUM debt that the bank will allow you to qualify for is around 50% of your total gross income if you have good credit. If you choose this method, you will be “house poor” and unable to afford other basic human needs. So based on these calculations, you would need to make at least $7,192.64GROSS per month to afford this property and live “house poor.” This would equate to a salary of $86,311.68 per year BEFORE TAXES.

I did not factor in closing costs, inspections, maintenance, moving, or even furniture. So should you continue renting while establishing zero equity? The median rental price in America as of February 2023 was $1,978. Inventory is low, and landlords are compensating for the money lost during COVID moratoriums. Most leasing offices require tenants to earn 3X the monthly rental price, equating to a monthly gross income of$5,934. This has left countless Americans stuck on the rental carousel of paying the majority of their monthly income to the landlord and being unable to save for a future that includes home ownership. Landlords can raise rental costs yearly at whim, and there is no guarantee that you will comfortably be situated in your rental unit from one contract to the next. Rental properties have also begun charging fees for everything under the sun, such as repairs and parking, which was one of the reasons people chose this method.

Gone are the days when Americans comfortably paid ¼ of their monthly salary toward living expenses. We have not even touched on the astronomically cost of other basic living necessities such as food or energy. You must make a decent income if you want to buy a home in 2023. The bank does not care if you are unable to pay because they will simply take your house. Some are lucky enough to secure an interest-free loan from the central bank of mom and dad. Others, the majority of the Great Unwashed, are scraping by—YOU WILL OWN NOTHING AND BE HAPPY!

QUESTION: Do you think that this entire scam with cryptocurrencies that the government will be able to track, do they realize that in war you take down the power grid and all digital currency fails? If the backup system is destroyed, all your digital currency will vanish. Are they this stupid? Is this why they have shills saying you are wrong?

HK

ANSWER: Yes. I have spoken to people involved in creating this insanity. First, they do not think there will ever be a nuclear war. Second, they really do think that they will create regime change in Russia at the expense of probably every Ukrainian alive today who are fools being led to the slaughter. When I have brought up the subject – WHAT IF YOU ARE WRONG! They dismiss it and do not even entertain plan B. The whole digital currency is all about tracking every dime. I have said many times, this is all about the new world order which is Schwab’s Great Rest and he knows that is our 2032 forecast. They all believe that forecast and are preparing to redesign the world this time to achieve their totalitarian dreams.

When I asked – Did you authorize Bitcoin? They just do not reply. Silence is golden. The launch of Bitcoin was just too damn convenient. That was standard operational political tactics – you float a balloon and see how the people accept it.

If you have ever been to Nuremberg, Germany, they have a bronze statue there – the Ship of Fools. The sculpture named Ship of Fools by Jurgen Weber is based on the satirical allegory by Sebastian Brant. This is now a reality.

COMMENT: Marty, I attended your coming out WEC in Philadelphia in 2011. Just about everyone I spoke with said the same thing. They all showed up to make sure it was really you and not some government stooge pretending to be you.

I must say, when you put up the war cycle, I thought it was interesting and everyone respected your work so we listened. At the time it was perhaps a curiosity and would be something we would watch on TV instead of the Oscars. Here we are. In the middle of this mess. I can now see how they used that tactic to demonize Trump to get Biden elected if he was really elected.

Now every person who voted for Biden has voted for World War III. They bought the hatred of Trump to remove him when he was like JFK and would never have agreed to war as you said when you went to dinner at Mara Largo. The recent tapes show that Nixon confronted the CIA for killing JFK. The very people who did the Watergate break-in were operatives for the CIA to make sure Nixon would be removed.

Our leaders really want war. I would never have thought your war model would predict that we would be the aggressor. Our government lies about everything. Why? Do they hate humanity that much?

GP

REPLY: I appreciate what you are saying. The Deep State has always had its agenda and it was always just about them. Never in my wildest dreams looking at these forecasts a decade ago did I ever contemplate that we would be the aggressor. The Neocons just want to annihilate every Russian. That is all they think about. That is why John McCain handed Hillary’s fake dossier to James Comey at the FBI. They were two Neocons and always wanted war with Russia. It was Hillary that conditioned the Democrats to think that Russia was the enemy and they rigged the election for Trump.

You see both Democrats and Republicans cheering war now. There is no stopping the warmongering. All we can do is prepare, and understand how the capital will shift as the arrays will give us the timing. This will enable us to position ourselves to make it to the other side of 2032. Fortunately, Socrates was constructed using the raw data to provide a picture of global capital flows.

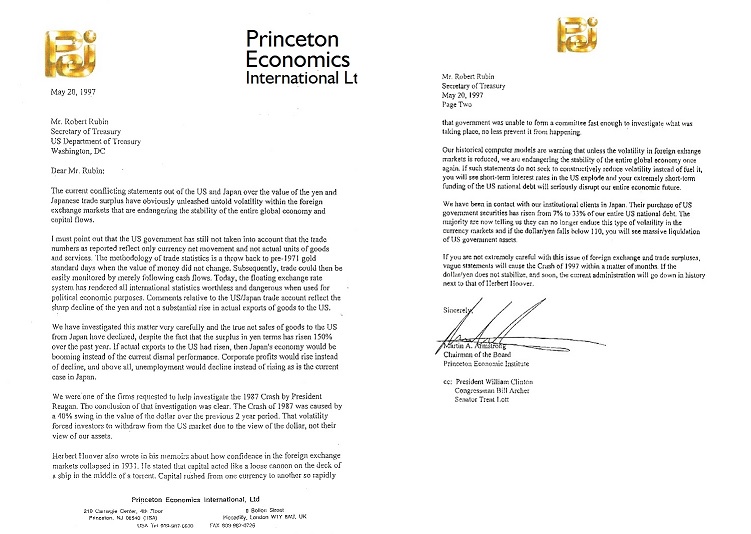

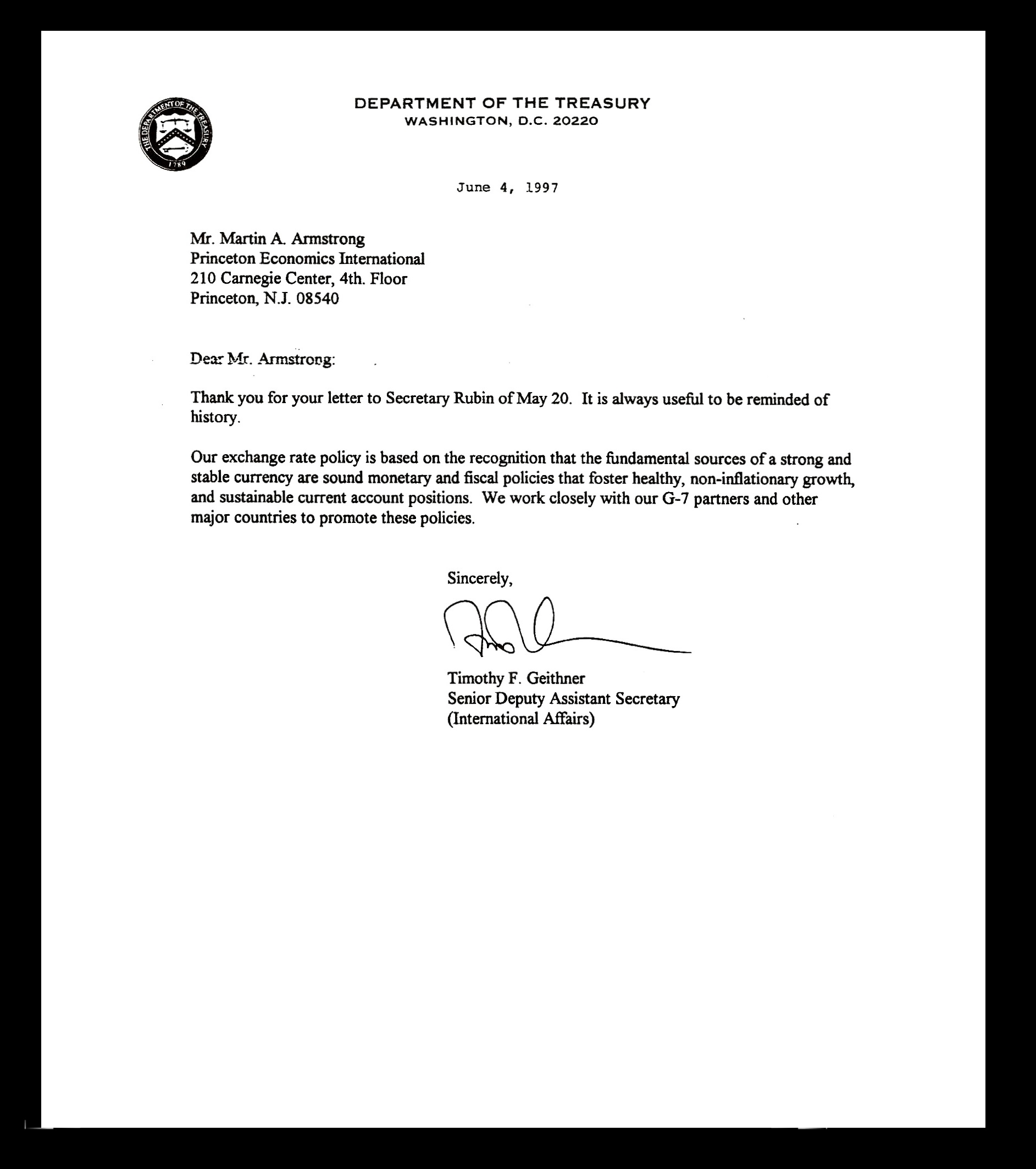

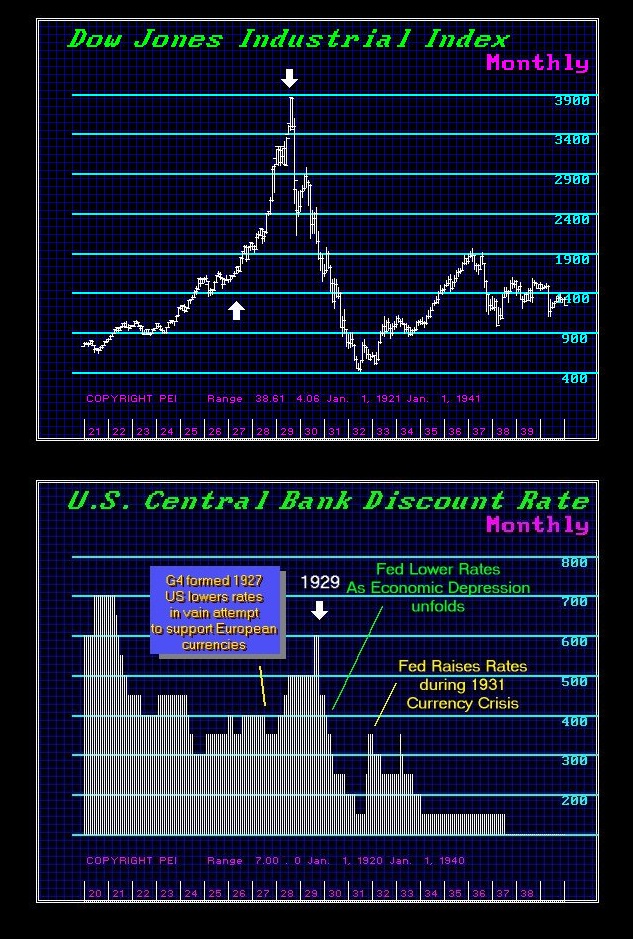

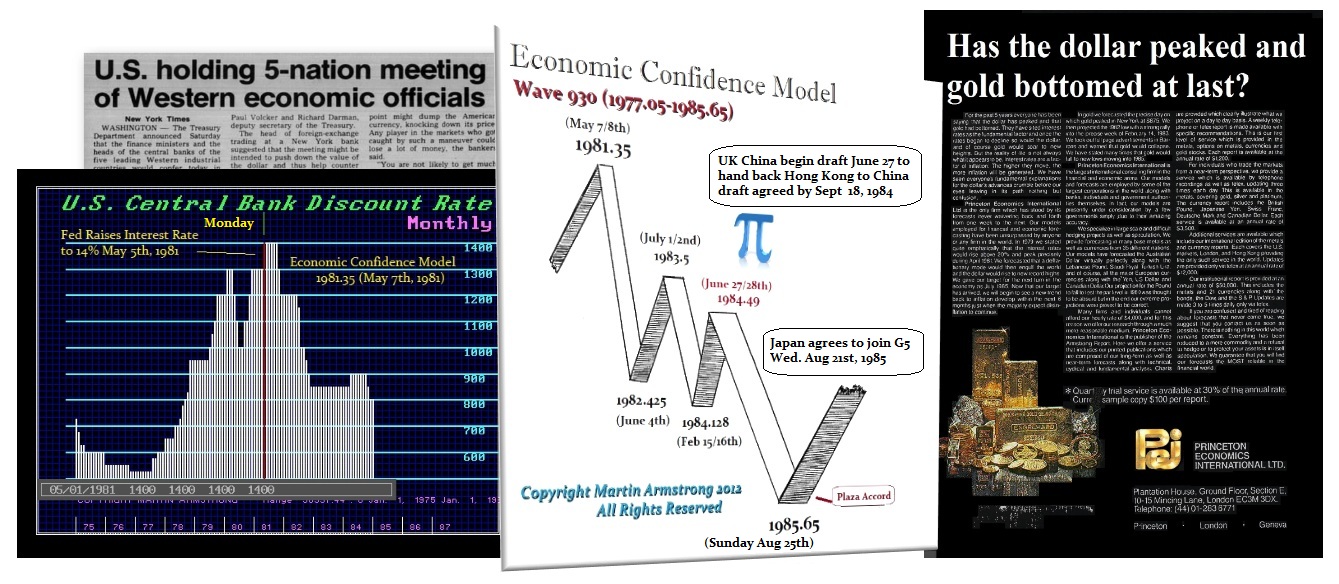

That was why I was called in by the Brady Commission back in 1987 for as you can see, the G5 was taking the dollar down for trade by 40% and then foreign investors sell US assets for they will lose on the FX exchange. Those morons every understood capital flows or currency.

When again they were trying to talk the dollar down in 1997 for trade purposes, I warned them they would unleash another crash making the same mistake as before. They at least listened and backed off.

Posted originally on the CTH on February 2, 2023 | Sundance

This is so critically important to the understanding of the core, central element where the globalism atom splits and the resulting destruction begins, that I must pause all personal recovery efforts -immediately- and explain. This is an incredible example of where corporations and government merge. This is the atom split. This is the root, the nub, the place where “trillions at stake” takes context.

Strong HatTip to Gateway Pundit for this exceptional video and example {Direct Rumble Link Here}. The understanding comes via a Canadian dairy farmer, who, like thousands of other farmers around the world, is a private business under government control. This example is about dairy, specifically milk, however, the underlying premise goes much further.

This is modern corporatism, the nexus of govt intervention, regulations and the multinational exploitation of industry. This is also the globalist example that shows how the concepts of “capitalism” and “free markets” have been destroyed. First, watch the video:

What you are witnessing in that video is something we have talked about at length for years.

Influential people, politicians (rules) and corporate leaders (profits), both with vested financial interests in the process, have sold a narrative that global manufacturing, global sourcing, and global production is the inherent way of the future. The same voices claimed the American economy was/is consigned to become a “service-driven economy.”

What was always missed in these discussions is that advocates selling this global-economy message have a vested financial and ideological interest in convincing the information consumer it is all just a natural outcome of economic progress.

It’s not.

It’s not natural at all. It is a process that is entirely controlled, promoted and utilized by large conglomerates, lobbyists, purchased politicians and massive multinational corporations.

To understand who opposes President Trump, Jair Bolsonaro, or any economic nationalist, specifically because of the economic leverage against multinational corporations their policy creates, it becomes important to understand the objectives of the global and financial elite who run and operate the institutions. The Big Club.

Understanding how trillions of trade dollars influence geopolitical policy we begin to understand the three-decade global financial construct they seek to protect. That is, global financial exploitation of national markets.

FOUR BASIC ELEMENTS:

♦Multinational corporations purchase controlling interests in various national outputs (harvests and raw materials), and ancillary industries, of developed industrial western nations. {example}

♦The Multinational Corporations making the purchases are underwritten by massive global financial institutions, multinational banks. (*note* in China it is the communist government underwriting the purchase)

♦The Multinational Banks and the Multinational Corporations then utilize lobbying interests to manipulate the internal political policy of the targeted nation state(s).

♦With control over the targeted national industry or interest, the multinationals then leverage export of the national asset (exfiltration) through trade agreements structured to the benefit of lesser developed nation states – where they have previously established a proactive financial footprint.

For three decades economic “globalism” has advanced, quickly. Everyone accepts this statement, yet few actually stop to ask who and what are behind this – and why?

Every element of global economic trade is controlled and exploited by massive institutions, multinational banks and multinational corporations.

Institutions like the World Trade Organization (WTO), World Bank and International Monetary Fund (IMF), control trillions of dollars in economic activity. Underneath that economic activity there are people who hold the reins of power over the outcomes. These individuals and groups are the stakeholders in direct opposition to principles of America-First national economics.

The modern financial constructs of these entities have been established over the course of the past three decades. When you understand how they manipulate the economic system of individual nations you begin to understand why they are so fundamentally opposed to President Trump.

In the Western World, separate from communist control perspectives (ie. China), “Global markets” are a modern myth; nothing more than a talking point meant to keep people satiated with sound bites they might find familiar; but the truth is ‘global markets’ have been destroyed over the past three decades by multinational corporations who control the products formerly contained within global markets. This is the function of the World Economic Forum.

The same is true for “Commodities Markets.” The multinational trade and economic system, run by corporations and multinational banks, now controls the product outputs of independent nations. The free market economic system has been usurped by entities who create what is best described as ‘controlled markets’.

Bulletpoint #1:♦ Multinational corporations purchase controlling interests in various national elements of developed industrial western nations.

This is perhaps the most challenging to understand. In essence, thanks specifically to the way the World Trade Organization (WTO) was established in 1995, national companies expanded their influence into multiple nations, across a myriad of industries and economic sectors (energy, agriculture, raw earth minerals, etc.).

This is the basic underpinning of national companies becoming multinational corporations.

Think of these multinational corporations as global entities now powerful enough to reach into multiple nations -simultaneously- and purchase controlling interests in a single economic commodity.

A historic reference point might be the original multinational enterprise, energy via oil production. (Exxon, Mobil, BP, etc.)

However, in the modern global world, it’s not just oil; the resource and product procurement extend to virtually every possible commodity and industry. From the very visible (wheat/corn) to the obscure (small minerals, and even flowers).

Bulletpoint #2 ♦ The Multinational Corporations making the purchases are underwritten by massive global financial institutions, multinational banks.

During the past several decades national companies merged. The largest lemon producer company in Brazil, merges with the largest lemon company in Mexico, merges with the largest lemon company in Argentina, merges with the largest lemon company in the U.S., etc. etc. National companies, formerly of one nation, become “continental” companies with control over an entire continent of nations.

…. or it could be over several continents or even the entire world market of Lemon/Widget production. These are now multinational corporations. They hold interests in specific segments (this example lemons) across a broad variety of individual nations.

National laws on Monopoly building are not the same in all nations. Most are not as structured as the U.S.A or other more developed nations (with more laws). During the acquisition phase, when encountering a highly developed nation with monopoly laws, the process of an umbrella corporation might be needed to purchase the targeted interests within a specific nation. The example of Monsanto applies here.

Bulletpoint #3 ♦The Multinational Banks and the Multinational Corporations then utilize lobbying interests to manipulate the internal political policy of the targeted nation state(s).

In underdeveloped countries the process of buying a political outcome is called bribery. Within the United States we call it lobbying. The process is exactly the same.

With control of the majority of actual lemons the multinational corporation now holds a different set of financial values than a local farmer or national market. This is why commodities exchanges are essentially dead. In the aggregate the mercantile exchange is no longer a free or supply-based market; it is now a controlled market exploited by mega-sized multinational corporations.

Instead of the traditional ‘supply/demand’ equation determining prices, the corporations look to see what nations can afford what prices. The supply of the controlled product is then distributed to the country according to their ability to afford the price. This is essentially the bastardized and politicized function of the World Trade Organization (WTO). This is also how the corporations controlling WTO policy maximize profits.

Back to the lemons. A corporation might hold the rights to the majority of the lemon production in Brazil, Argentina and California/Florida. The price the U.S. consumer pays for the lemons is directed by the amount of inventory (distribution) the controlling corporation allows in the U.S.

If the U.S. lemon harvest is abundant, the controlling interests will export the product to keep the U.S. consumer spending at peak or optimal price. A U.S. customer might pay $2 for a lemon, a Mexican customer might pay .50¢, and a Canadian $1.25.

The bottom line issue is the national supply (in this example ‘harvest/yield’) is not driving the national price because the supply is now controlled by massive multinational corporations.

The mistake people often make is calling this a “global commodity” process. In the modern era this “global commodity” phrase is particularly nonsense.

A true global commodity is a process of individual nations harvesting/creating a similar product and bringing that product to a global market. Individual nations each independently engaged in creating a similar product.

Under modern globalism this process no longer takes place. It’s a complete fraud. Massive multinational corporations control the majority of production inside each nation and therefore control the global product market and price. It is a controlled system.

EXAMPLE: Part of the lobbying in the food industry is to advocate for the expansion of U.S. taxpayer benefits to underwrite the costs of the domestic food products they control. By lobbying DC these multinational corporations get congress and policy-makers to expand the basis of who can use EBT and SNAP benefits (state reimbursement rates).

Expanding the federal subsidy for food purchases is part of the corporate profit dynamic.

With increased taxpayer subsidies, the food price controllers can charge more domestically and export more of the product internationally. Taxes, via subsidies, go into their profit margins. The corporations then use a portion of those enhanced profits in contributions to the politicians. It’s a circle of money.

In highly developed nations this multinational corporate process requires the corporation to purchase the domestic political process (as above) with individual nations allowing the exploitation in varying degrees. As such, the corporate lobbyists pay hundreds of millions to politicians for changes in policies and regulations; one sector, one product, or one industry at a time.

These are specialized lobbyists.

EXAMPLE: The Committee on Foreign Investment in the United States (CFIUS)

CFIUS is an inter-agency committee authorized to review transactions that could result in control of a U.S. business by a foreign person (“covered transactions”), in order to determine the effect of such transactions on the national security of the United States.

CFIUS operates pursuant to section 721 of the Defense Production Act of 1950, as amended by the Foreign Investment and National Security Act of 2007 (FINSA) (section 721) and as implemented by Executive Order 11858, as amended, and regulations at 31 C.F.R. Part 800.

The CFIUS process has been the subject of significant reforms over the past several years. These include numerous improvements in internal CFIUS procedures, enactment of FINSA in July 2007, amendment of Executive Order 11858 in January 2008, revision of the CFIUS regulations in November 2008, and publication of guidance on CFIUS’s national security considerations in December 2008 (more)

Bulletpoint #4 ♦ With control over the targeted national industry or interest, the multinationals then leverage export of the national asset (exfiltration) through trade agreements structured to the benefit of lesser developed nation states – where they have previously established a proactive financial footprint.

The process of charging the U.S. consumer more for a product, that under normal national market conditions would cost less, is a process called exfiltration of wealth. This is the basic premise, the cornerstone, behind the catchphrase ‘globalism‘.

It is never discussed.

To control the market price some contracted product may even be secured and shipped with the intent to allow it to sit idle (or rot). This is where the dumping of the milk comes into play. None of this is a market driven outcome. All of this is being controlled by guiding hands of politicians, rule makers, and the partnership with the private sector corporations.

It’s all about controlling the price and maximizing the profit equation. We are discussing food and agricultural production, but the issue (the process of control) covers far more than just food, farming and Ag in general. It’s everything folks. Everything.

To gain the same $1 profit a widget multinational might have to sell 20 widgets in El-Salvador (.25¢ each), or two widgets in the U.S. ($2.50/each).

Think of the process like the historic reference of OPEC (Organization of Petroleum Exporting Countries). Only in the modern era massive corporations are playing the role of OPEC and it’s not oil being controlled, thanks to the WTO it’s almost everything.

Again, this is highlighted in the example of taxpayers subsidizing the food sector (EBT, SNAP etc.), the multinational corporations can charge domestic U.S. consumers more.

Ex. more beef is exported, red meat prices remain high at the grocery store, but subsidized U.S. consumers can better afford the high prices.

Of course, if you are not receiving food payment assistance (middle-class) you can’t eat the steaks because you can’t afford them. (Not accidentally, it’s the same scheme in the ObamaCare healthcare system)

Agriculturally, multinational corporate Monsanto says: ‘all your harvests are belong to us‘. Contract with us, or you lose because we can control the market price of your end product.

The downside is that once you sign that contract, you agree to terms that are entirely created by the financial interests of the larger corporation, not your farm. Additionally, the rule makers (govt), are working hand in glove with the corporations who control the outcome.

The multinational agriculture lobby is massive. We willingly feed the world as part of the system; but you as a grocery customer pay more per unit at the grocery store because domestic supply no longer determines domestic price.

Within the agriculture community the (feed-the-world) production export factor also drives the need for labor. Labor is a cost. The multinational corps have a vested interest in low labor costs. Ergo, open border policies. (ie. willingly purchased republicans not supporting border wall etc.).

This corrupt economic manipulation/exploitation applies over multiple sectors, and even in the sub-sector of an industry like steel. China/India purchases the raw material, coking coal, then sells the finished good (rolled steel) back to the global market at a discount. Or it could be rubber, or concrete, or plastic, or frozen chicken parts etc.

The ‘America First’ Trump-Trade Doctrine upsets the entire construct of this multinational export/control dynamic. Team Trump focus exclusively on bilateral trade deals, with specific trade agreements targeted toward individual nations (not national corporations).

‘America-First’ is also specific policy at a granular product level looking out for the national interests of the United States, U.S. workers, U.S. companies and U.S. consumers.

Under President Trump’s Trade positions, balanced and fair trade with strong regulatory control over national assets, exfiltration of U.S. national wealth is essentially stopped.

This puts many current multinational corporations, globalists who previously took a stake-hold in the U.S. economy with intention to export the wealth, in a position of holding contracted interest of an asset they can no longer exploit.

Perhaps now we understand better how massive multi-billion multinational corporations and institutions are aligned against President Trump. In essence, Donald Trump is the anti-WEF weapon of the American people.

They will even organize a western corporate war against Russia to stop anyone from blocking their financial goals.

The Federal Reserve raised the benchmark by 25 bps, as expected. The Fed fully understands that the manipulation of the CPI is a necessary aspect both for containing government benefits and understating inflation also results in high tax revenues. The market loves hope, and as a result, they focused on the warning that we’ll be in restrictive territory for just a bit longer. Most still believe that there will be a slowdown in inflation just ahead.

The Fed’s cautionary commentary saying that the “disinflation process” has started triggered shares to jump ending up 1%. This shows how insane the analysis had become that they cheer a recession and think that lower interest rates are bullish for the stock market. Obviously, they just listen to the talking heads on TV and have never bothered to look at reality. When interest rates decline, so has the stock market. Interest rates rose for the entire Trump Rally, and they crashed during the Great Recession of 2007-2009. For the life of me, I just shake my head when the talking heads cheer lower rates and spread doom and gloom with higher rates.

Fox Business is reporting that economic conditions are much worse than you are being told. Unfortunately, this is the conclusion when you have ZERO understanding of the historical trends and economic conditions. It is true that the shortages of COVID have caused prices to rise faster than economic growth and most incomes. Therefore, they conclude that our standard of living has been rapidly declining. The number reveals that more than one-third of all U.S. young adults are being supported in part by their parents. Thanks to COVID, this disrupted society far greater than anyone is reporting. In addition to the shortages because of the lockdowns, by the end of 2020, more than half of young adults in America were living with one or both parents. That statistic actually exceeded the record high of the Great Depression.

Here is the worst part of this analysis. Many are jumping on the bandwagon claiming that the decline in real disposable income has been the largest since 1932 and therefore, this is a warning sign of a Great Depression is coming. They seem to be focused on the fact that the GDP report showed a significant decline in real disposable income, which fell over $1 trillion in 2022. Now let’s look closer!

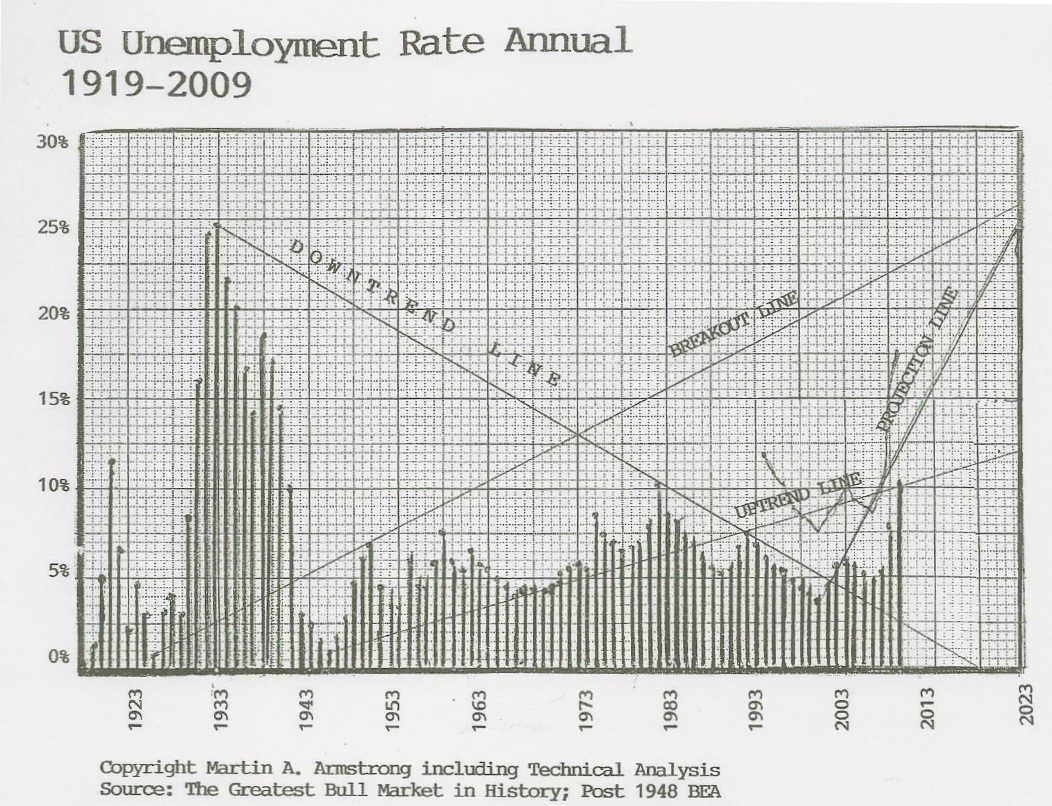

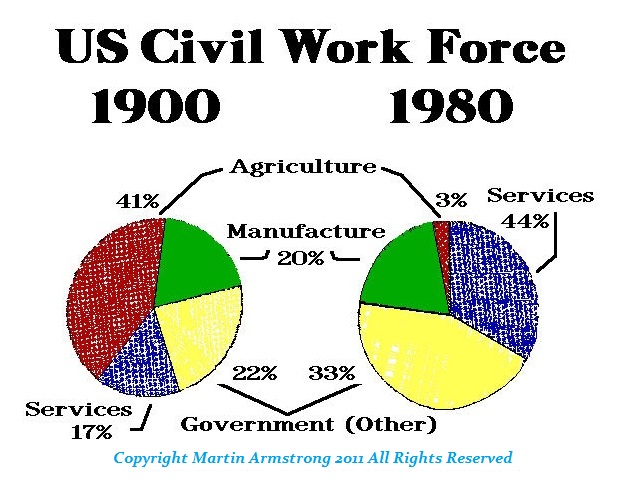

First of all, the entire reason why unemployment rise to 25% during the latter part of the Great Depression was the Dust Bowl. Why? At that time, about 40% of the civil workforce was still agrarian. The Dust Bowl meant job loss. If you could not even plant crops, there was no need for people to pick crops.

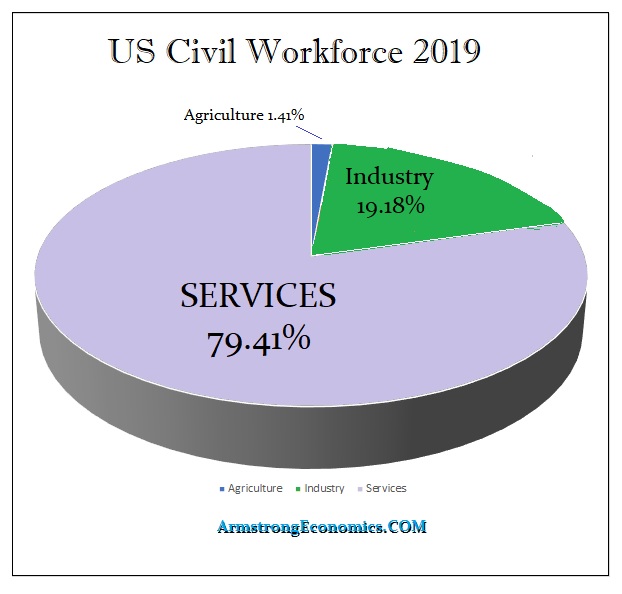

Service during the Great Depression accounted for 17% of the workforce compared to 44%+ today. Government, federal, state, and local, was 22% of the civil workforce during the Great Depression compared to 33% by 1980. Things have continued to evolve and by 2019, services represent 79.41%. Agriculture is now a tiny fraction of what it once was – 1.41%.

In the USA, at the state level, their share of the civil workforce varies greatly. Florida is at about 11.3% compared to New Mexico which is 22.5% – a government employee’s paradise. The lowest is Michigan at 10.1%.

During the Great Depression, the entire reason for the collapse in disposable income was the collapse in agriculture which created a collapse in income due to massive unemployment. That is totally different from the crisis we have today.

Here we have rising prices due to shortages and then central banks raising interest rates in a fool’s quest to stop inflation when it is not based on speculation. Moreover, the biggest borrower is the government, and rising interest rates will only increase their exposure to keep rolling over the debt. Therefore, governments have been borrowing year after year. What happens when the public no longer buys their debt? Real disposable income has been collapsing for completely different reasons since 1932. Here we have the costs of everything rising and then these people want war with Russia and China. Every war since the start of recorded history has resulted in inflation. Add to this, the total insanity of trying to end climate change by outlawing fossil fuels at a time when the climate is prone to getting colder.

We are already witnessing riots around the world BECAUSE of inflation. During the Great Depression, people were suffering from DEFLATION. So comparing just that statistic of a decline in personal income and projecting we now face a Great Depression, does not even qualify to be classified as analysis. That is no different from someone warning that carrots must be lethal because everyone who has ever eaten a carrot has obviously died.

QUESTION: Do you think that Socrates will ever achieve infallibility?

KJ

ANSWER: I have only shown our Global Market Watch model at conferences. It is a pattern recognition model that is learning every day. I have pointed out that nothing is infallible but if anything can achieve that, it will be this model. Right now, it’s not too bad, but it is still in its infancy. What has shocked me more than anything is that it has identified over 80,000 patterns. This is incredible to me. However, it explains why it is impossible for a person to actually forecast correctly. There are so many subtle variances that something may not be what we think is unfolding.

Eventually, it is theoretically possible that we reach some limitations of the pattern variances. If that can be achieved, then and only then would you be able to forecast infallibly.

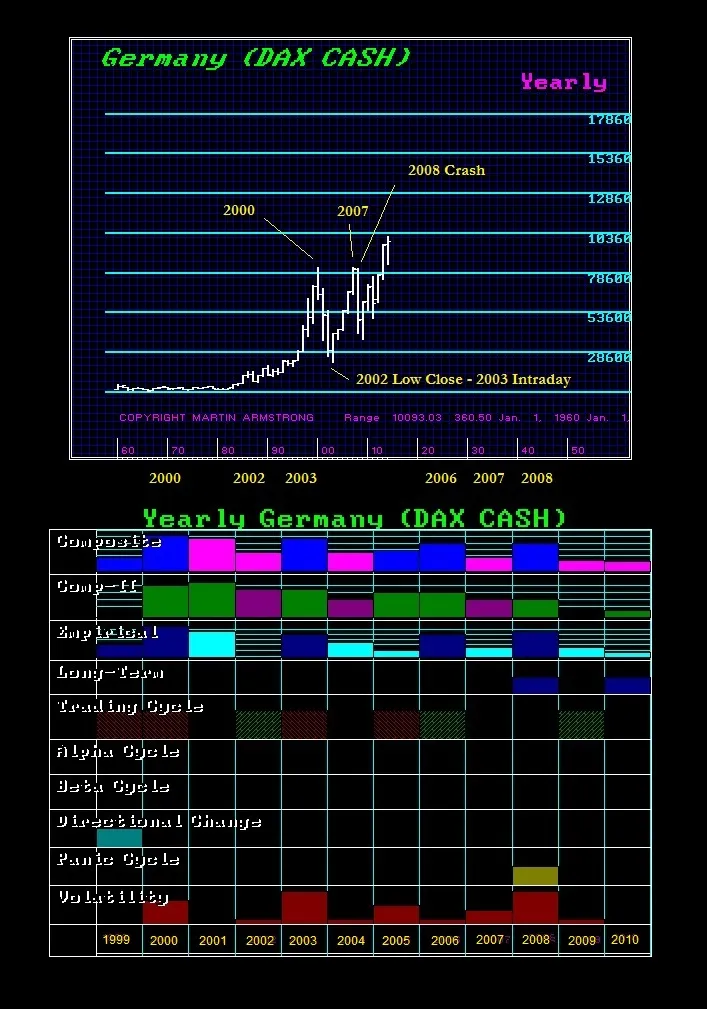

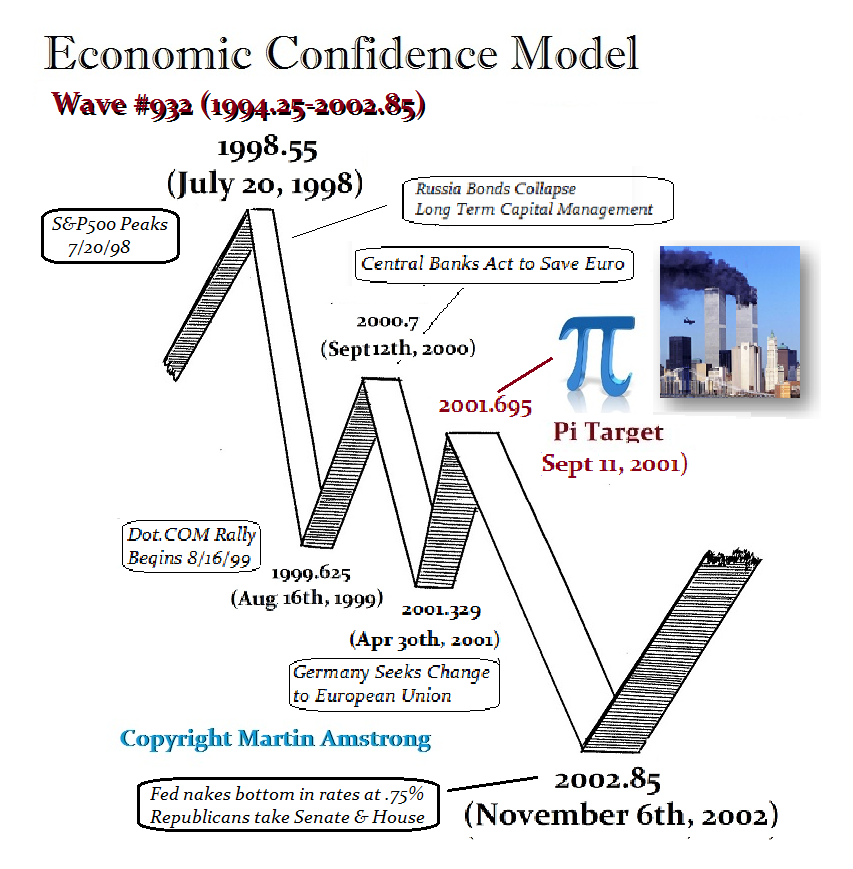

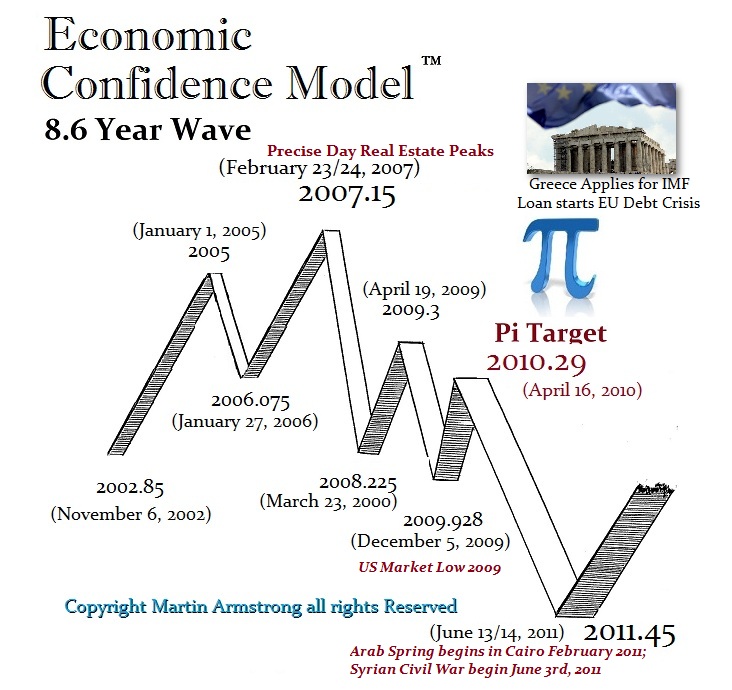

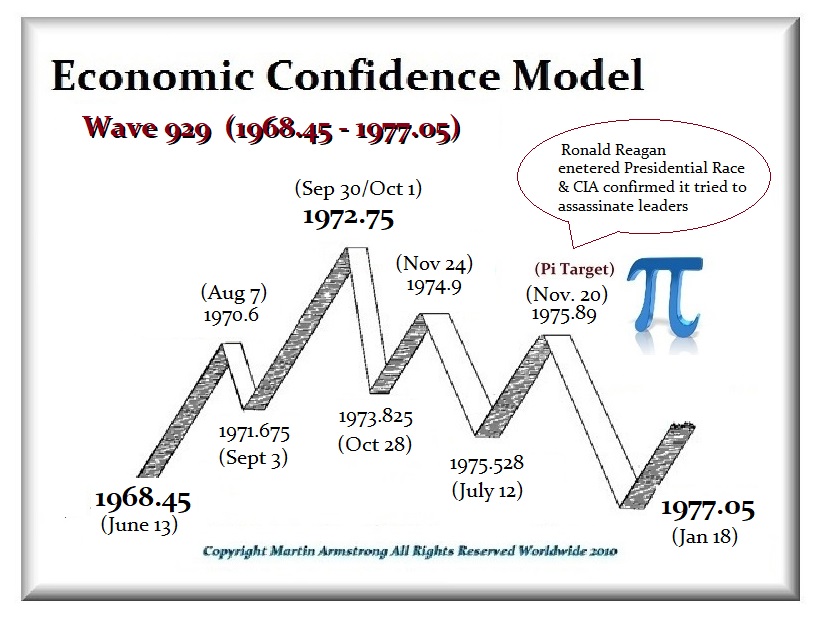

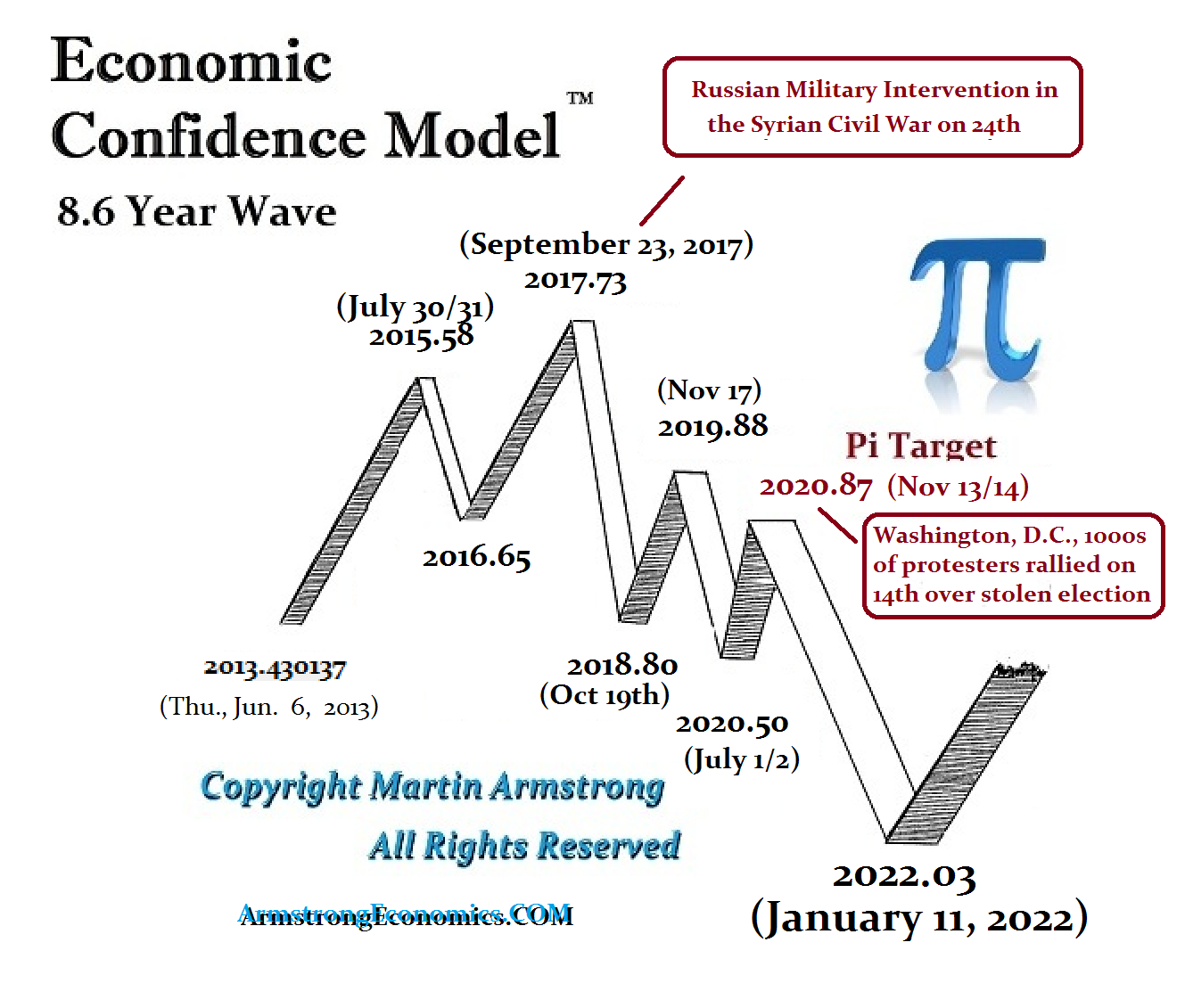

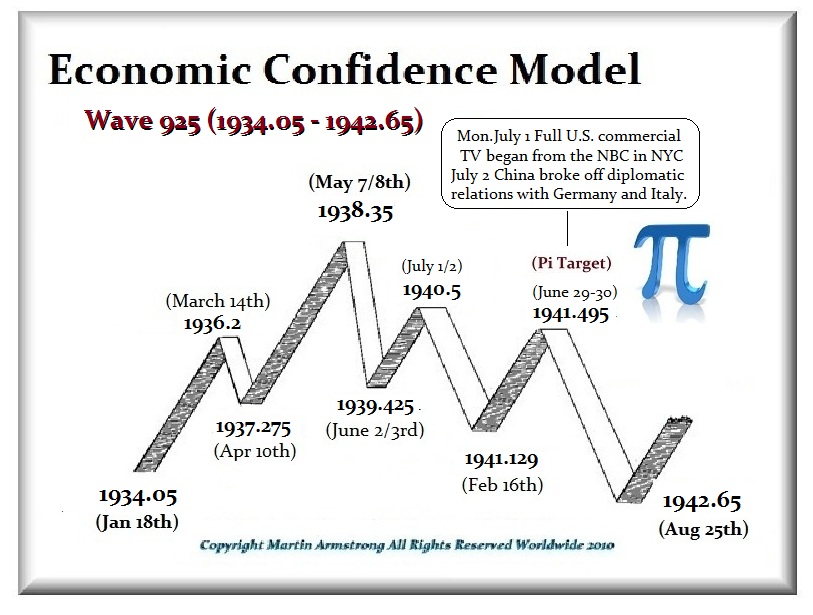

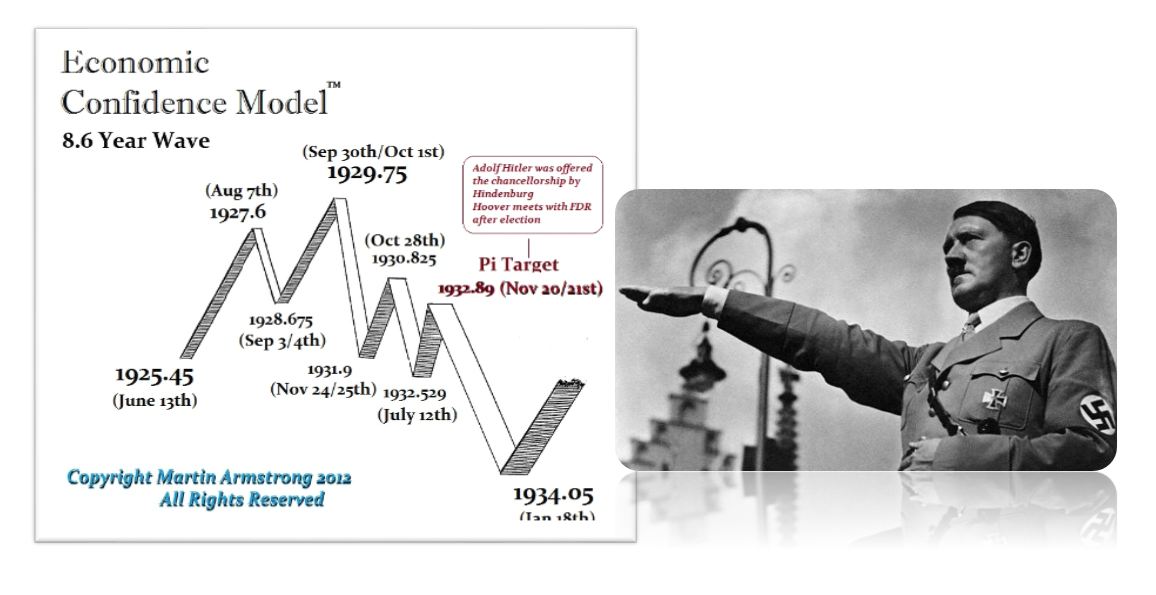

Yet there is something else of tremendous importance. Socrates has been virtually infallible on the long-term trends and events. What I have come to understand is that there are so many possible variations in the day-to-day trends, but it does not alter the long-term. It projected a financial panic in 2008 10 years in advance. How do so many events unfold to the very day of the Economic Confidence Model? All I can say is that these events, which have nothing to do with my personal opinion, confirm that there is a hidden order of complexity that the make human eye cannot possibly see. There are just way too many events that unfold precisely on the very day of a target to be just coincidence. There is a far greater order that exists and people will disparage these forecasts because they think they only work because we have a huge client base.

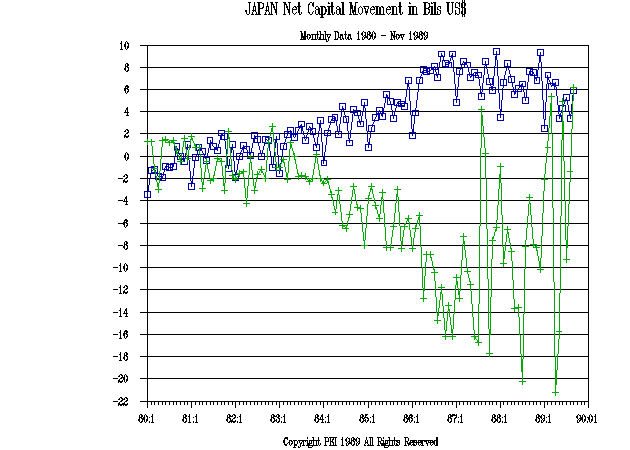

We have been forecasting for several years now that those who have been focused on the demise of the dollar to the exclusion of everything else would be wrong because of what must fall first is both Europe and Japan. It is an all-out race to see who will be the first to collapse.

This special report on Japan is very critical for it provides a view of Asia v Europe. This is the prelude to the fall of socialism in the West. Communism collapsed in 1989. Now 34 years later, it is just our turn. It does not mean the end of the world. It simply means the end of the present monetary system as we have known it.

The Report covers the Japanese Yen spot and futures, the Nikkei 225 Cash Index, and the Japanese JGB Futures.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America