QUESTION: Didn’t gold decline from 1980 to 1999 because of all the dumping of gold by central banks?

WV

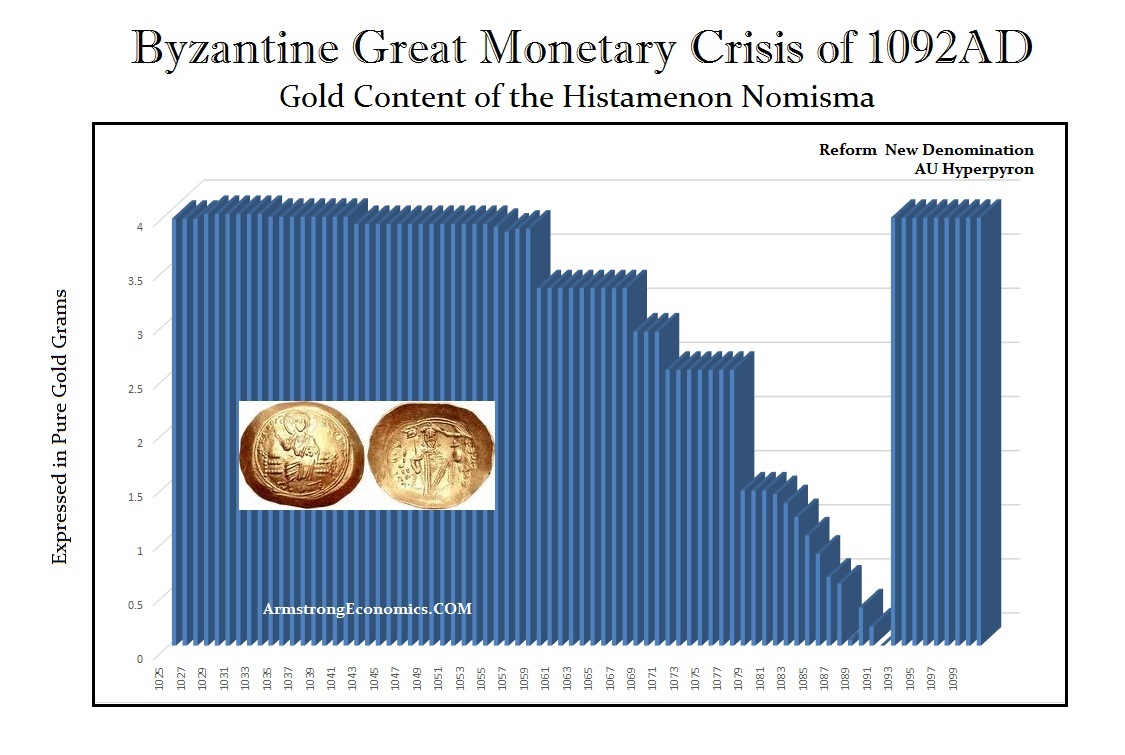

ANSWER: I understand that the quantity rise, in theory, makes sense that the price would decline. But historically, there is no evidence that supports that theory on a consistent basis. There are times when the supply has increased and so has the price. During the Byzantine Empire, confidence in the government began to collapse especially during the monetary crisis of 1092. As people hoarded their gold, the government was forced to debase the coinage even more. When people do not trust the future, they will hoard their wealth. You must understand that all things NEVER remain equal.

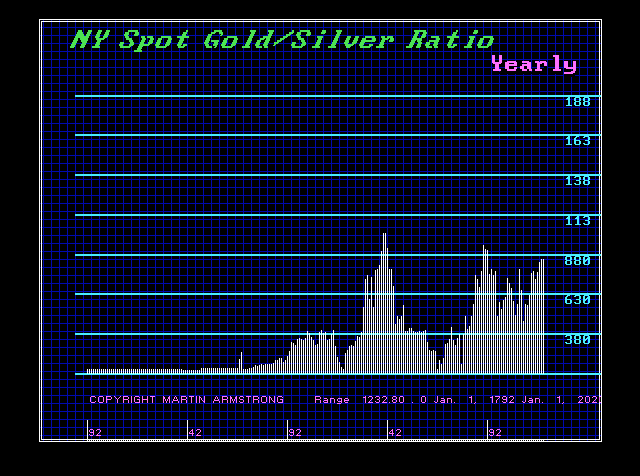

This is also why the silver-to-gold ratio fluctuates. NOTHING is ever permanent. We must remember that because it is when the collapse in government takes place, an increase in supply will never satisfy the demand.

Posted originally on the CTH on January 1, 2023 | Sundance

This is an interesting interview in that International Monetary Fund Globalist Director Kristalina Georgieva seems to be laying the landscape for some truthful economic news to surface on the geopolitical level; albeit keeping up the globalist pretenses around western collective energy policy.

One of the more important points Mrs. Georgieva hits on is the reopening of China, from district level COVID bubbles as a containment feature, and the likely impact it will have on global supply chains. Mrs. Georgieva is correct on this issue.

China continued operating their industrial manufacturing base (despite COVID) because they built strict covid isolation bubbles around their industrial sectors geographically. However, with China lifting those isolation bubbles, there is a great potential for the manufacturing sectors to be hit hard by short to medium term virus outbreaks. This could/will have the potential ripple effect of global supply disruptions.

In an ironic twist, ‘deglobalization’ is now a 2023 catchphrase as various nations realize having their supply chains both dependent and interconnected is not good when there are interruptions. A new discussion centering around being dependent on China is the specific issue now being raised. However, the globalists are isolating their viewpoints only to raw material resourcing and development. WATCH:

[Transcript] -MARGARET BRENNAN: I want you to take us around the world and kind of us give us that global view. Let’s start in China. China has been this hub of cheap manufacturing for the world, we are all so dependent on it but right now it looks like COVID cases are exploding as they start pulling back those zero COVID restrictions. What will that mean for the global economy Longterm and short-term?

GEORGIEVA: In the short term, bad news. China has slowed down dramatically in 2022 because of this tight zero COVID policy. For the first time in 40 years China’s growth in 2022 is likely to be at or below global growth. That has never happened before. And looking into next year for three, four, five, six months the relaxation of COVID restrictions will mean bush fire COVID cases throughout China. I was in China last week, in a bubble in the city where there is zero COVID. But that is not going to last once the Chinese people start traveling.

MARGARET BRENNAN: Because they also- they don’t have an effective vaccine right now.

GEORGIEVA: The- the vaccinations fall behind. They have not worked on anti-viral treatments and how that can be offered to people, and so they will go through this tough time. If they stay the course, and this is our advice, stay the course, over time they would be able to catch up with the rest of the world, both in terms of focusing their vaccinations, bringing mRNA vaccines into China, expanding antiviral treatment, and the economy would function. But for the next couple of months, it would be tough for China, and the impact on Chinese growth would be negative. The impact on the region would- would be negative. The impact on global growth would be negative.

MARGARET BRENNAN: Because this is the second-largest economy in the world, and we’ve learned how dependent the world is on the Chinese supply chain. So do you expect then, a domino effect? Will inflation get worse, because all of a sudden there aren’t workers healthy enough to go to factories in China?

GEORGIEVA: We expect that there would be counterweight from the sheer opening of the economy, because up to now, the biggest impact on global value chains came from restrictions due to COVID. When you close down a big city or a big port, the repercussions for the economy is- are significant. Now, we would have the impact of people getting sick, not going to work, but the economy would be open. So the expectations we have for China is to gradually move to a higher level of economic performance, and finish the year better off than it is going to start the year. But you’re absolutely right, the world has relied on China’s growth for a long, long, long time. Before COVID, China would deliver 34, 35, 40% of global growth. It is not doing it anymore. It is actually quite a stressful for the- for the Asian economies. When I talk to Asian leaders, all of them start with this question, what is going to happen with China? Is China going to return to a higher level of growth?

MARGARET BRENNAN: You’ve said that you fear that we are sleepwalking into a world that is poorer and less secure because of a split in the global economy between the US and China. What do you mean by that? Do you see efforts here in Washington to stop it?

GEORGIEVA: It is very easy to reflect on the benefits of the world being more integrated. When we look back over the last three decades, the world economy tripled because of this reliance on an integrated world economy. Who benefited the most? Emerging markets and developing economies, they quadrupled. But rich countries also benefited, they doubled in size of the economy. So we have to be careful not to throw the baby out with the bath water. Yes, the way we have operated created excessive dependency in global chains. We were too focused on costs, how can we make products cheaper. And COVID and then the senseless war Russia started against Ukraine has shown that this is not enough. We cannot just concentrate on what is cheaper. We have to think of the security of supplies and that means diversify the sources of products that make the economy function well, lifting up the level of cost. That economic logic is not only appropriate, it is a must to follow. But we shouldn’t go beyond. We shouldn’t say, okay, we break the world into blocks, one works here, the other one works there because the costs are very, very high. We calculated that just trade, limiting trade into two blocks, would chop $1.5 trillion from the global GDP year after year after year.

MARGARET BRENNAN: If you tried to separate the US and China?

GEORGIEVA: You separate- you separate them, there is an excessive cost. So the logic should be where for security reasons there has to be careful recalibration of supply chains, do it, but don’t go beyond- don’t go into benign areas of products that have no strategic significance but they benefit the US consumer, they benefit the world economy. And this is what we are arguing for, don’t go in a direction in which this separation would make everybody poorer and the world less secure.

MARGARET BRENNAN: So you’re telling Beijing and Washington, figure it out. You can’t be in conflict.

GEORGIEVA: What we have seen in Bali is an indication that this rationale–

MARGARET BRENNAN: You’re talking about the G20 meeting–

GEORGIEVA: The G20 meeting in Bali, when the two presidents, President Biden and President Xi Jinping, met, they spent three and a half hours discussing exactly that. Where is the point of contact that makes both countries better off? And where is that- that there are differences that cannot be bridged and therefore we have to keep them–

MARGARET BRENNAN: The US is trying to block some Chinese technology companies from doing business here. They’re taking measures that are drawing some pretty bright lines between the US and China. Is that tolerable?

GEORGIEVA: We always prefer countries to seek their common interest in economic integration. And when you start breaking the interactions that are based on fair trade, you harm your own people, you not only harm the- the Chinese and therefore it has to be thought through very carefully. Again, I want to be very clear, some diversification of supplies for the security of supply chains is necessary. COVID taught us this lesson, the war taught us this lesson. So the U.S. is right to look into some areas where strategically they need to guarantee the functioning of the U.S. economy without interruptions. But do that keeping in mind the interests of the American people that would like to still have prices moderating, and actually, when we think about prices, one good news we have for 2023 is that towards the end of the year, we do expect inflation to trim down. So don’t take actions that may be contrary to that trend.

MARGARET BRENNAN: But you are predicting inflation to slow to six and a half percent from about 7%. Is that right?

GEORGIEVA: Well, towards the end of the year, we- we project it would go even further down towards the end of 2023, provided central banks stayed the course. Our big worry is that with the economy slowing down globally, we are projecting global growth to go down to 2.7%, maybe even lower next year. Remember, 2021, it was 6%. It dropped to 3.2 this year, 2022. And it will continue to drop down if central banks get the cold foot and say, ‘oh, my god, growth is slowing down, let’s slow down the fight against inflation.’ We risk then inflation to be more persistent. So our message is to central banks, you have to see credible decline in inflation and only then you can think about re-calibrating rate policy.

MARGARET BRENNAN: One of your IMF researchers gave a pretty dire prediction. Overall this year, shocks will reopen economic wounds that were only partially healed post-pandemic. In short, the worst is yet to come and for many people, 2023 will feel like a recession. What do you need to brace for?

GEORGIEVA: The- this is- this is what we see in 2023. For most of the world economy, this is going to be a tough year, tougher than the year we leave behind. Why? Because the three big economies, U.S., E.U., China, are all slowing down simultaneously. The US is most resilient. The U.S. may avoid recession. We see the labor market remaining quite strong. This is, however, mixed blessing because if the labor market is very strong, the Fed may have to keep interest rates tighter for- for longer to bring inflation down. The E.U. very severely hit by the war in Ukraine. Half of the European Union will be in recession next year. China is going to slow down this year further. Next year will be a tough year for China. And that translates into negative trends globally. When we look at the emerging markets in developing economies, there, the picture is even direr. Why? Because on top of everything else, they get hit by high interest rates and by the appreciation of the dollar. For those economies that have high level of that, this is a devastation.

MARGARET BRENNAN: And I want to- I want to come back to you on that. And just to explain that for some of our listeners, a stronger dollar, it’s good for Americans when they go shopping abroad. It’s not good for poor countries who have taken out loans, for example, and borrowed money in dollars. And according to the IMF, 60% of low income countries are in distress because of this- this debt. So what does that look like? Do you- do you see governments collapsing with defaults? Does that bleed into the global financial system? I mean, how much of a contagion does this become?

GEORGIEVA: So far the countries that are in that distress are not systemically significant to trigger a debt crisis. Let’s just look at the map, which are these countries? Chad, Ethiopia, Zambia, Ghana, Lebanon, Surinam, Sri Lanka, very important for their people that we find the resolution to the debt problem, but the risk of contagion is not as high. However, if that list continues to grow, and let’s remember, 25% of emerging markets are trading in distressed territory, then the world economy may be for a bad surprise. And this is why at the IMF, we are working very hard to press for debt resolution for these countries and we have engaged the traditional creditors, the Paris Club, the non-traditional creditors, China, India, Saudi Arabia. I would call this very simple: urgency, we have to act. When I look at the- the debt of the world. Yes, we have to be concerned. During COVID, what did we do? Everywhere governments borrowed, rightly so, to help their people.

MARGARET BRENNAN: Money was cheap.

GEORGIEVA: Money was cheap, and we prevented a collapse of the world economy. That was the right thing to do. But once Russia invaded Ukraine and that added impetus to inflation, money is not- not cheap anymore. So what is the advice we give to governments? Focus on your budgets, make sure that you have sufficient revenues to collect and that you spend very wisely.

MARGARET BRENNAN: That’s good advice, but it’s not always easy politics to follow that advice, as you know–

GEORGIEVA: Of course it is not.

MARGARET BRENNAN: And so that’s why I want to- if- if you can explain for our viewers. You know, we spoke to the CEO of JPMorgan Chase, Jamie Dimon, recently, and he said he sees the global risk as explosive right now. He was saying things like migration, energy, national security, liquidity in the banking system, war, these are all the knock on effects of a government not being able to pay its bills and not being able to deliver for its people. Is that what you are seeing too?

GEORGIEVA: Well, what we’re seeing is the world has changed dramatically. It is a more shock prone world. The lessons we learned from the last couple of years are that no more we operate with relative predictability of what the future would bring. And these shocks COVID, the war, costs of living crisis, they compound their impact. What does that mean for governments? First and foremost, it means that we need to change our mindset towards more resilience, more precautionary actions. And at the IMF, this is what we tell our members. Act early, don’t wait until the problems deepen. And for those who need help, this is why we exist for the developing countries. The fund is a source of resilience and I am- I am very pleased that many of our members are coming to us. Just since the war started we got 16 countries coming for programs to the IMF, $90 billion in support for these countries. And right now we have 36 requests. So that acting early, when you see trouble, look for ways to strengthen your fundamentals, to have buffers to protect you and your people. This is the advice we give to governments. For those who don’t know the IMF, we were created from the ashes of the Second World War to stabilize the world economy. And at a moment like this, we come strong to help our members. My message, don’t think that we are going to go back to pre-COVID predictability. More uncertainty, more overlap of crises wait for us. Rather than crying for the time we had, we have to buckle up and act in that more agile, precautionary manner I described.

MARGARET BRENNAN: I want to make sure I get to Ukraine because I know we’re running out of time. You’ve said- excuse me- you’ve said the single most negative factor in the global economy is the war in Ukraine. And Vladimir Putin says this is going to go on for some time. President Zelensky said they need $55 billion in foreign support next year. He expects $20 billion from the IMF, is he going to get it?

GEORGIEVA: We are working on providing support for Ukraine. So far, out to the international financial institutions, we have provided the largest amount of financing for Ukraine, $2.7 billion in emergency financing, and we are working for 2023 to be a significant part of the support for Ukraine. I expect that sometime early in the year we will go to our board with the request. We have assessed the needs of Ukraine to range somewhere between three and five billion dollars a month. What Putin did with destroying critical infrastructure in Ukraine, this is horrific, and it means that in the next months the country would be more on the high end of this range because it is put in an awful position to have to restore access to electricity, to heat, to water. I have relatives in Ukraine. What I- what I know from them is it is cold, it is dark, and it is scary. Bombardments of civilian areas continue. What I also want to say is that Ukraine has proven to be remarkably resilient. Ukrainian economy is functioning. Pensions are being paid. When there is bombardment, restoration of energy, water, heat is done very quickly and we see revenues collected in Ukraine in a very disciplined manner to support the functioning of the country.

MARGARET BRENNAN: So the government’s not going to collapse?

GEORGIEVA: The government is very well functioning under incredibly difficult circumstances. No, they’re not going to collapse. And then the other thing that is so remarkable is actually the world has proven to be more resilient than we feared, a year in the beginning of the year. We look at the response to the energy shock in Europe, and Europe is moving towards independence from Russia decisively. Yes, there will be a tough winter, maybe the next one would be even tougher, but freedom from dependence on Russia is coming. It is going to be there.

MARGARET BRENNAN: I want to ask you two questions before we go. How do you describe the state of U.S. economics and politics?

GEORGIEVA: The US economy is remarkably resilient. Decision making in the US because of the way the political set is at the moment, it is more difficult. But nonetheless the US has taken some very important steps that are helping to the US economy. Like the child tax-

MARGARET BRENNAN: The tax credit. It expired.

GEORGIEVA: The credit that is it. It is contributing so significantly to reducing poverty in the US, like the infrastructure bill, like the Inflation Reduction Act. These are things that are bringing more dynamism in the US. Good for the US, good for the world. And of course staying on that course is going to be more challenging. But I do hope that the US is not going to slip into recession despite all these risks. We expect one third of the world economy to be in recession. And yes, as you said, even countries that are not in recession, it would feel like recession for hundreds of millions of people. But if that resilience of the labor market in the US holds, the US would help the world to get through a very difficult year.

MARGARET BRENNAN: And as I let you go, my final question is what leaves you hopeful in 2023?

GEORGIEVA: What leaves me hopeful is that I know when we work together, we can overcome the most dramatic challenges. In 2020, the world came together in the face of tremendous threat and was able to overcome this threat. In 2023 we have to do the same. And in this world of ours, of more frequent and devastating shocks, we have to hold hands, we have to work together. And my institution is there to bring together economic policymakers so we can be wise and persistent in the face of truly dramatic challenges we face.

MARGARET BRENNAN: Madam managing Director, thank you for your time this morning.

We accept the named legislation “Inflation Reduction Act” (IRA) is a legislative misnomer intended to obfuscate the true construct of the bill. The IRA was factually the ‘green new deal’ program packaged under the guise of an ‘inflation reduction’ premise. However, in order to discuss the outcome of the content we have to play the game of pretending around the purpose of the legislation.

Within the IRA there was a $7,500 tax credit for American made Electric Vehicles. The intent of the legislation was to provide incentives for U.S. consumers to purchase ‘sustainable’ and environmentally friendly electric cars, trucks, SUV’s etc made in America.

The Congressional Budget Office (CBO) scored the bill with this legislative intent in mind. However, the Treasury Department is now taking apart the granular details of the legislation in order to qualify foreign made vehicles for the $7,500 credit. The rules interpretation from the Treasury Dept essentially negates the CBO score, and the outcome is going to be much more expensive than initially stated.

Because the $7,500 comes in the form of a tax credit, the IRS (Treasury) is the institution making the determinations for qualification. Treasury is changing the qualifications to permit basically any EV to qualify, by parsing a difference between a leased vehicle and a purchased vehicle. Additionally, Treasury is changing the battery sourcing aspect by qualifying essentially any trade agreement as a Free Trade Agreement (FTA), saying the term Free Trade Agreement was undefined in the legislation.

As an outcome & simply cutting to the chase, EV batteries from just about anywhere, inside EV vehicles from basically anywhere, that are purchased as leases from just about any auto manufacturer, will qualify for the $7,500 credit. It’s all a shell game, with the Biden administration determining where the pea is located.

Dec 29 (Reuters) – The U.S. Treasury Department said Thursday that electric vehicles leased by consumers starting Jan. 1 can qualify for up to $7,500 in commercial clean vehicle tax credits, a decision that makes those assembled outside North America eligible.

The announcement is a win for South Korea and some automakers that earlier this month sought approval to use the commercial electric vehicle tax credit to boost consumer EV access. Automakers said the credit could be used to reduce leasing prices.

The $430 billion U.S. Inflation Reduction Act (IRA) passed in August ended $7,500 consumer tax credits for purchases of electric vehicles assembled outside North America, angering South Korea, the European Union, Japan and others. The new Treasury guidance does not change the definition of what constitutes North American assembly to make more vehicles eligible for EV purchases.

Treasury said it was using “longstanding tax principles” to determine consumer leasing could qualify for the EV tax credit.

The IRA also imposes significant battery minerals and component sourcing restrictions, sets income and price caps for qualifying vehicles and seeks to phase out Chinese battery minerals or components. The commercial credit does not, however, have the sourcing restrictions of the consumer credit.

Senator Joe Manchin, a Democrat who chairs the chamber’s energy panel, urged Treasury to pause implementation of both commercial and new consumer EV tax credits and said they had bent “to the desires of the companies looking for loopholes” and would seek new legislation that “prevents this dangerous interpretation from Treasury from moving forward.” (read more)

From the Wall Street Journal, “One of the documents released Thursday pointed out that because the legislation doesn’t define what a free-trade agreement is, the Treasury Department might consider other types of trade agreements to expand the eligibility. The department didn’t provide examples of such agreements, but trade lawyers have suggested that the 2019 bilateral trade agreement with Japan and the World Trade Organization’s government procurement agreement could be candidates.” (link)

I am reminded of the words from Democrat Congressman Alcee Hastings during the construction of the ObamaCare legislation. WATCH (10 secs):

Posted originally on the CTH on December 14, 2022 | sundance

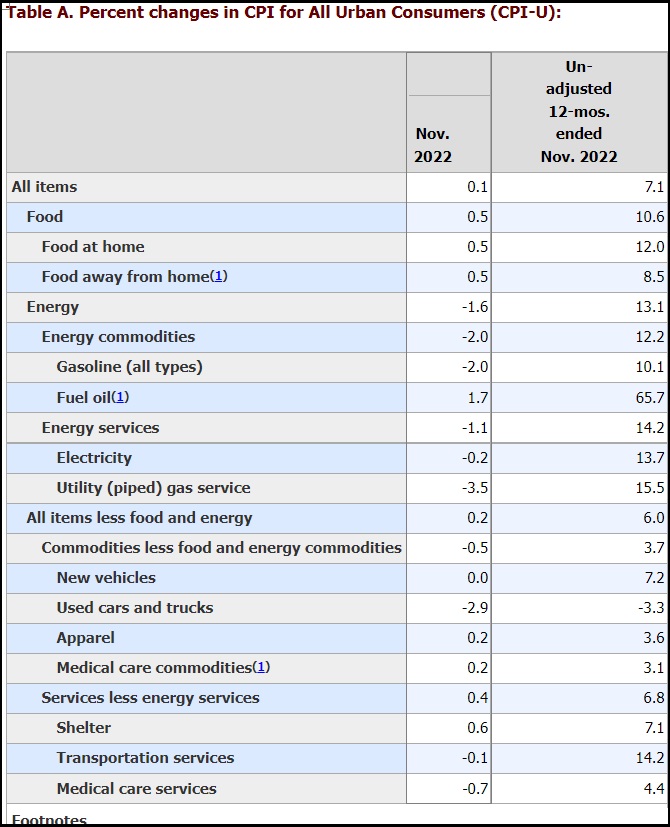

As we have often discussed on these pages, inflation would ultimately moderate and plateau not because prices were dropping but rather because of the calendar cycle.

As the economy cycles through a year of large price increases, the current inflation rate cycles through to the period when prices first increased. This calendar cycle means continued price increases are lower as a percentage and thus the inflation rate appears to modify despite prices continuing to rise. [BLS Report]

This scenario, prices remaining high and continuing to climb – yet lower as a percentage, now provides the justification for the federal reserve to state inflation is moderating.

(Via NBC) – Amid signs that price growth in the U.S. economy is rapidly cooling, the Federal Reserve announced Wednesday it was slowing the pace of its rate-hiking program designed to tackle inflation — but that more hikes were still on the table.

The Federal Open Market Committee said it was increasing its key federal funds rate by 0.5%, after announcing four-straight 0.75% hikes at its most recent meetings. In its Wednesday statement, the Fed said it continues to target an inflation rate of 2% over the long term and would continue to increase the federal funds rate to do so.

“Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures,” the committee said.

But bringing down inflation is likely to come at the cost of higher unemployment in the short term: The Fed said it now projects the 2023 unemployment rate to average 4.6%, equating to hundreds of thousands of more jobless workers compared with the current rate of 3.7%.

The Labor Department on Tuesday reported that annual inflation clocked in at 7.1% in November — the lowest reading in more than a year. While it is still high compared to the 2% level at which the Federal Reserve typically seeks to hold down inflation, the most recent number signals that the galloping price growth earlier this year is fading. (read more)

Prices will never drop because the supply side pressure from a new energy policy remains as the driving factor.

Demand has dropped throughout 2022 as the U.S. economy, gauged in units of product sold, has contracted. Consumers are not buying non-essential goods or services as the costs of housing, fuel, heating, electricity, overall energy and food prices continue rising.

Despite the economic contraction that is lowering energy use, rapidly increasing energy costs continue to be the driving force of inflation.

This period of depressed economic activity will continue as unemployment begins to become problematic. As a nation we will remain in this economic malaise as long as Green New Deal, Build Back Better, energy policy is maintained.

On the positive side the economic shrinking is reversable with new energy policy; however, the opportunity to make that change is several years away. In the interim, the cost of living will remain the biggest challenge for the foreseeable future, and the inbound open-border migration will keep wages depressed.

Under the economic program of Joe Biden wages must be depressed in order to avoid production inflation (higher labor costs) from piling atop the energy policy inflation. Thus, the border influx will continue.

The gap between the haves and have nots is also going to explode in the next five years.

The Bank of International Settlements (BIS) has warned in its latest quarterly report that there is $80 trillion dollar in off-balance sheet dollar debt in the form of FX swaps. This has involved pension funds and other ‘non-bank’ financial firms.

What they do not explain is that each “debt” has a counterparty that has an “asset” and in theory, that works out to net zero. But there is counter-party risk that is not discussed. This doesn’t address the liquidity issue either. Still, it is not entirely a black hole as they seem to lead some to proclaim. What is also left unexplained or addressed is the question of if they are netting across all transactions. Many of the players in this market have offsetting positions. It is one thing to scream OMG the size of the stock market is too big, and another to yell fire in a crowded theater.

This $80 trill is effectively the derivatives market. It is what it is. Marking everything to market all the time isn’t a great answer either for there can be imbalances for a day or two in the middle of chaos. What is clear is that the BIS is raising concerns, in which it also said this year’s market upheaval took place without any major issues.

On the other hand, the BIS has been pushing central banks to raise rates to fight inflation which will only accelerate the crisis since it is shortage based. This is no different from the ’70s when there was an external price shock from OPEC,. Raising interest rates did nothing to prevent inflation, instead, it resulted in a strong dollar, the collapse of the pound to $1.03 in 1985, and the US national debt more than doubled on interest expenditures.

Nonetheless, the BIS has been quieter on the inflation front this time around. Just maybe, they are starting to realize that the old theories no longer work. The September UK government bond market turmoil was created by raising interest rates and the losses on holding long-term debt in the face of rising interest rates have been just the tip of the iceberg.

The FX swap markets have become huge. Our clients are well into the trillions these days whereas twenty years ago we had less than 5 clients at the $1 trillion threshold.

Nonetheless, the complexity of the cross-positions is the real risk. One side can blow out because of the chaos these braindead politicians are creating with this war against Russia.

Posted originally on the conservative tree house on November 23, 2022 | Sundance

Arizona Governor candidate Kari Lake appears with Steve Bannon to discuss the status of her campaign lawsuits against Maricopa County officials in advance of a rush to certify the election. {Direct Rumble Link} – WATCH:

QUESTION: Marty, It was a fantastic WEC. You tied it all together brilliantly and how the real issue is this liquidity crisis. Suddenly the ECB came out and said that inflation will not subside given a recession. It appears they were watching the WEC. Do you think that the ECB is at least listening now?

NG

ANSWER: For Christine Lagarde to publicly state that a “mild recession” will not reduce inflation is admitting that inflation has been instigated by COVID lockdowns that disrupted the supply chain and unleashed shortages. The Bank of England has come out and stated that we will see the longest recession in 100 years.

The ECB has just forced banks to repay their loans withdrawing $300 billion euros from the banking system in a desperate effort to stop inflation. This will not help for Legarde knows that even an economic recession will not prevent this type of inflation that is more akin to the STAGFLATION of the ’70s where costs rose thanks to the OPEC crisis and where we have the COVID Crisis that created shortages mixed with the climate change zealots determined to end fossil fuels despite the fact there are no alternatives. How do you even make steel without coal?

Everything is now unfolding on schedule. We are facing 2023 which will be known as the year of chaos.

The collapse of the FTX Exchange is pretty straightforward insofar as this is the same lesson that constantly repeats in finance time and time again. Basically, FTX lent US$10bn of client funds to their trading arm Alameda, which used it for leveraged their own crypto speculation because the crypto market has been collapsing. Typically, someone like Sam Bankman-Fried had his whole life wrapped up in this venture. Lacking financial controls operating from the Bahamas, moving the money from client funds to his trading arm Alameda was possible. Historically, someone in this position sees his world collapsing but is not prepared to see that unfold for it requires admitting that he was wrong on crypto, to begin with. Consequently, such a person is not trying to actually rob clients’ money, they most likely see it as a temporary loan to save the company and the market will bounce back – or so they believe.

Our computer had picked the high in Bitcoin perfectly and has been projecting the collapse all along the way. But crypto has become a religion and in so doing it clouds the judgment of people who want to believe the story. Alameda blew up in a crypto meltdown because it did not want to accept that the crypto boom was over. The loan he probably thought would be temporary, vanished in the implosion. At first, I would have assumed they had actually invested the money and lost it on the bond market collapse. But that was perhaps too traditional. Here, it appears they were trying to defend their own cryptocurrency and trying to buy the low that kept moving lower. It appears he was allegedly simply using clients’ funds to trade keeping gains for his firm and the clients now suffer the risk.

It appears that they allegedly were trying to defend the crypto market and did not understand that the boom was over. The loans could not then be repaid. As crypto was crashing, some people needed to cash out. The attempt to pull out US$5bn from FTX exposed the fact that the cash was all gone. This is not so unusual. It has happened before. This time, the prosecutors are clamoring to be the one to charge him so they can become famous over his dead body.

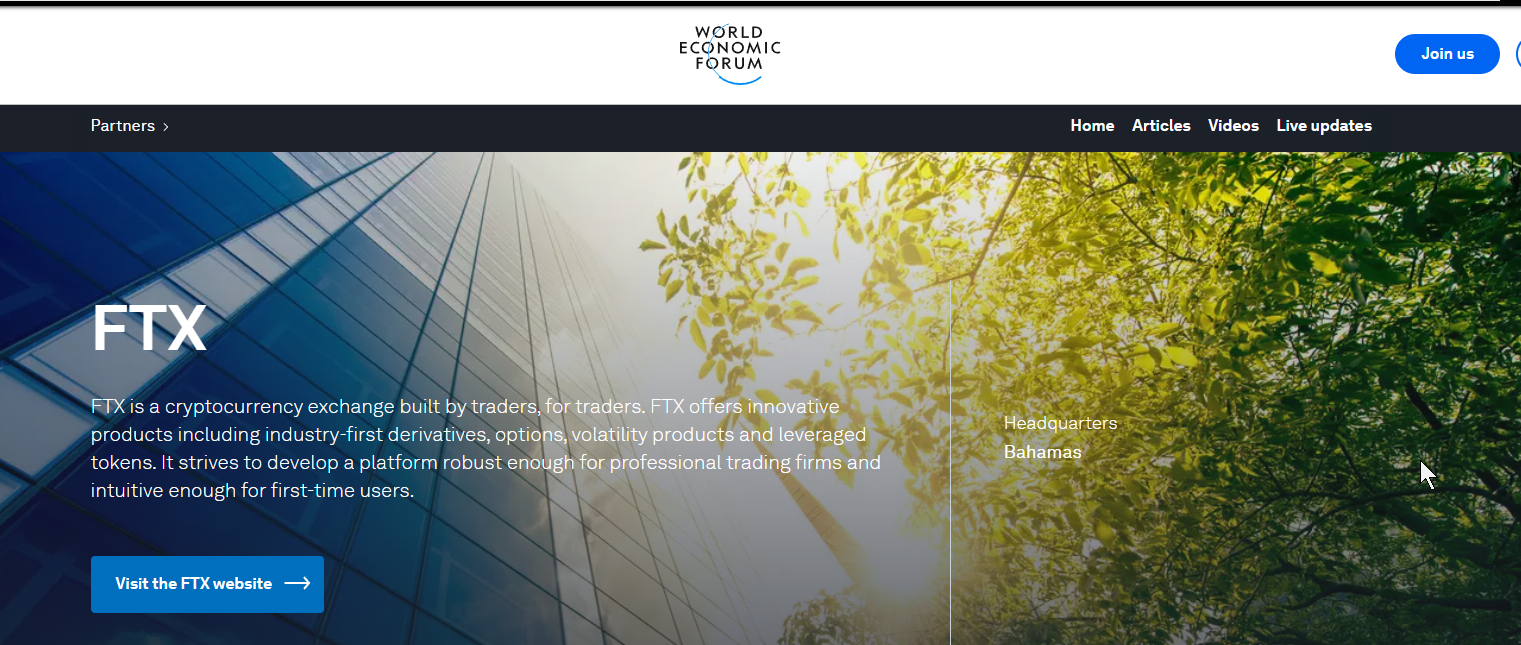

FTX was a partner with Klaus Schwab’s World Economic Forum (WEF). Of course, the WEF has suddenly removed the page and is desperately trying to hide their involvement with FTX and Sam Bankman-Fried. Naturally, eliminating paper currency has been the goal of the WEF because they support the end of not just capitalism, but also democracy. Schwab’s push has been his Great Reset and to control society to impose his economic philosophy inspired by Marx and Lenin.

This is by no means the first violation of fiduciary responsibility that presents a custodial risk. MF Global Holdings Ltd., you might recall, was a firm formerly run by New Jersey ex-Gov. Jon Corzine was accused in 2013 of unlawfully using customer money to meet his firm’s funding needs. When MF Global went bust because of trading by ex-Goldman Sach’s Jon Corzine’s trading using his client’s money in London also outside the regulatory eye of the USA, he was NEVER prosecuted for illegally using $1.6 billion of 26,000 client’s money. That is not going to be the case this time. So what is the difference between Corzine and Bankman-Fried? Corzine was ex-Goldman Sachs.

Indeed, Corzine was well-connected right into the White House with Obama. Nobody went to jail and clients had to wait in bankruptcy to get their money – even cash in the accounts was taken. There are clear risks with the broker and clearer. As long as the SEC is run with former Goldman Sachs staff, there will NEVER be an honest regulator. Even when all the banks pled criminally guilty, the SEC exempted everyone from losing their licenses. They would NEVER do that with anyone outside of New York City. The SEC will never prosecute the banks – EVER!!!!

Indeed, several federal investigations had been launched into MF Global, including probes by the Commodity Futures Trading Commission (its main regulator), the Securities and Exchange Commission, the Federal Bureau of Investigation, and Justice Department prosecutors in both Chicago and New York. The brokerage has also been the focus of several congressional hearings. Not a single one charged Corzine with trading with his client’s money. The losses that eventually drove MF Global into bankruptcy stemmed from high-risk bets on European sovereign bonds that Corzine made as he swung for the fences. Corzine bet big that the bond issuers would not default.

Commodity Futures Trading Commission simply fined Jon Corzine only $5 million over MF Global’s rapid descent into bankruptcy on Oct. 31, 2011, as an estimated $1.6 billion of customer money went missing. Anyone else would have been in prison for a minimum of 20 years.

It was Martin Glenn who was the judge in New York on M.F. Global bankruptcy. He was the first one to engage in FORCED LOANS by abandoning the rule of law to help the bankers by protecting them from losses taking client accounts to cover M.F. Global’s losses. He simply allowed the confiscation of client funds when in fact the rule of law should have been that the bankers were responsible and M.F. Global’s losses should have been reversed as they did even when Robert Maxwell’s companies failed in London from his illegal trading taking employee pension funds.

Yes, that was Ghislaine Maxwell’s father and the guy who was in control of the company that Bill Browder worked for before Edmond Safra. Never should the client’s funds be taken for M.F. Global’s losses to the NY Bankers. It was Judge Martin Glen who placed the entire financial; system at risk by trying to protect the bankers. Martin Glenn pampered these bankers making them the new UNTOUCHABLES. We have to be concerned that there really is no rule of law that will protect you in a crisis.

On Bloomberg TV, Sam Bankman-Fried explained why he even created FTX. He said he was experiencing his own frustration at Alameda Research, which was his crypto-focused proprietary trading firm. He was frustrated with the execution he was receiving at various crypto exchanges so he claimed that inspired FTX’s creation in May 2019. FTX grew rapidly to become the third largest crypto exchange in the world, with approximately $16 billion of customer assets under custody over 43 months.

Bankman-Fried stated that Alameda was making lots of money, but it could have been making more and he did not have access to venture capital. Claims of 100% annualized returns are not uncommon in a boom, but any experienced trader knows what goes up, also comes down. Alameda was relying on “cobbling together lines of credit” to expand its capital base. He then created FTX to solve his funding problem creating his own exchange that even the WEF cheered as a partner. He actually created a platform that was tailored for his own company, Alameda, to facilitate its trading needs. FTX coined the phrase “built by traders, for traders.”

There was an obvious conflict of interest questions regarding the close relationship between FTX and Alameda. Being operated from the Bahamas raised questions among those of us who are seasoned financial market observers whether the two were truly arm’s length from each other. However, people were so pumped up on adrenalin with crypto being the end of the dollar and central banks that this new free-wheeling crypto world believed what they wanted to believe and never looked too closely. FTX operated outside the reach of the US regulatory domain and there was a lack of any fiduciary confirmation. When the founder of Binance, the world’s largest crypto exchange, Changpeng Zhao, openly questioned the soundness of the FTX/Alameda nexus on Twitter saying he would sell over $500 million worth of FTX’s token FTT, that was the kiss of death weather or not he realized he would unleash a crypto panic that would engulf the entire industry in a matter of days.

The collapse of FTX will now become a contagion for the crypto world. This 20-something group of inexperienced traders has signaled the demise of an industry that was getting all the hype with no substance. This crypto world will be seen as the DOT COM Bubble of 2000. With a recession on the horizon, the collapse of sovereign debt, and the monetary system as a whole, people will be looking for more of the safe bets rather than roll the dice on crypto. Nothing ever goes straight down. But by year-end, the volatility should perk up everyone’s view of the world.

Posted originally on the conservative tree house on November 12, 2022 | sundance

FTX crypto currency exchange CEO Sam Bankman-Fried is a major donor to multiple progressive causes and politicians. This week as FTX starts to collapse, the financial system underneath the exchange looks more like a Ponzi scheme falling apart.

The CEO had been a major donor to regulators on Capitol Hill, and the tentacles of FTX extend to Ukraine where Sam Bankman-Fried was operating to support the Ukraine government with crypto currency collections and donations. The FTX corporation and CEO Sam Bankman-Fried is now under multiple investigations. Here’s the 90-second recap of the current dynamic. WATCH:

.

(Via Daily Caller) Sam Bankman-Fried, prolific Democratic donor and ex-CEO of now-bankrupt cryptocurrency exchange FTX, funded the campaigns of members of Congress overseeing the Commodity Futures Trading Commission (CFTC), one of the key bodies tasked with regulating the crypto industry and the subject of Bankman-Fried’s aggressive lobbying.

Bankman-Fried’s FTX is currently under investigation by the CFTC and the Securities and Exchange Commission (SEC) after Bankman-Fried allegedly moved $10 billion in client assets from his crypto exchange to his trading firm Alameda Research, and a liquidity crisis at his exchange which prompted the company to file for bankruptcy. However, prior to the agency’s probe, Bankman-Fried aggressively courted the CFTC – and funded several key lawmakers charged with overseeing the agency, pouring cash into their campaign coffers. (read more)

(Via CoinDesk) The past week has seen a dizzying downward spiral for Sam Bankman-Fried’s huge crypto empire. Bankman-Fried’s FTX crypto exchange has paused withdrawals, and a tentative bailout from rival Binance appears to be kaput. That could put depositor funds at risk, and certainly spells a major setback for not only Bankman-Fried but for the cryptocurrency industry as a whole.

These downfalls aren’t rare in crypto, which is subject to extreme boom-bust cycles. But FTX and Bankman-Fried are unique in the stature they achieved before self-immolating. Over the past three years, FTX has come to be widely regarded as a reputable exchange, despite not submitting to U.S. regulation. Bankman-Fried has himself become globally influential, thanks to his thoughts on cryptocurrency regulation and his financial support for U.S. electoral candidates – not necessarily in that order.

These narratives about both FTX and Bankman-Fried are now clearly dead in the water, given recent evidence that everything was not as it seemed at the exchange, or at Bankman-Fried’s other firm, Alameda Research. (read more)

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America