Posted originally on the CTH on January 17, 2023 | sundance

There has always been a general shaping and interpretation surrounding economic news, specifically as it relates to the impact of pricing on consumers and corporations. However, against the backdrop of supply side inflation, the financial gaslighting from the Wall Street Journal stands out at the top.

Without pretending, and looking directly at the Main Street reality, CTH has outlined inflation as a matter of monetary and energy policy. From that standpoint the timing and scale of price increases (inflation measured over time) was predictable. Our current status is an inflationary plateau, where prices remain high but stabilize for likely two quarters.

What the Wall Street Journal outlines as a “shopper rebellion against high prices” is complete hogwash. Notice in the construct of the narrative, the demand side (consumers) is identified as the cause of diminished revenue & profits for corporations. They continue pretending that inflation was not driven by energy costs.

(WSJ) – […] Many companies raised their prices substantially last year to offset higher fuel costs and higher prices for ingredients, parts and labor. As fuel prices have dropped and pandemic supply-chain snarls have eased, some of those costs have come down.

That is a good sign for the economy. It suggests that some inflation in the past year resulted from extreme supply-demand imbalances brought on by the pandemic and the war in Ukraine and which are now fading.

Notice the transparent lack of mentioning ‘energy policy’ as the inflation driver.

[…] The study, by economists at the Federal Reserve Bank of Kansas City, found that higher markups—the gap between what a firm charges and what it costs to produce an item—were a major driver of inflation in 2021.

They concluded that companies in some cases were raising prices in 2021 in anticipation of future cost pressures, rather than because of market power or outsize demand. Andrew Glover, a senior economist at the Federal Reserve Bank of Kansas City who was involved in the study, doesn’t expect prices to fall this year, he said, but he anticipates that the pace of increase will continue to slow.

Inflation is the rate of increase over time. We have experienced two years of massive price increases. Yes, the rate of those increases will moderate, this is the plateau, but the price will never drop. The current prices are a direct result of fixed energy policy.

[…] Unit sales of food and beverages fell 3% last year, but on a dollar basis they rose 10%. That showed consumers were willing to pay higher prices for groceries but bought fewer items.

[…] “People need to eat,” said Krishnakumar Davey, a president at IRI. Shoppers are nonetheless buying less when possible and, in many cases, buying less expensive versions of necessities such as toilet paper and laundry detergent. (read more)

Meanwhile the Fed is worried that wages will be forced to increase. Here is the real worry for the Wall Street Journal, “If consumers believe high prices will persist, they could seek bigger raises, and businesses, seeing higher labor costs, could continue raising prices.” Yes, workers, forward inflation is your fault.

Government policy drives up prices, but workers needing wage increases to pay for those higher prices… well, that is not acceptable to the government, comrade proles.

Sometimes you need to look behind the curtain before you understand the real trend. It is true that Federal Reserve officials are committed to fighting inflation and expect higher interest rates to remain in place until more progress is made, according to minutes released from the central bank’s December meeting. Also what has been reported is that at that meeting, policymakers expressed the importance of keeping the restrictive policy in place while inflation holds unacceptably high.

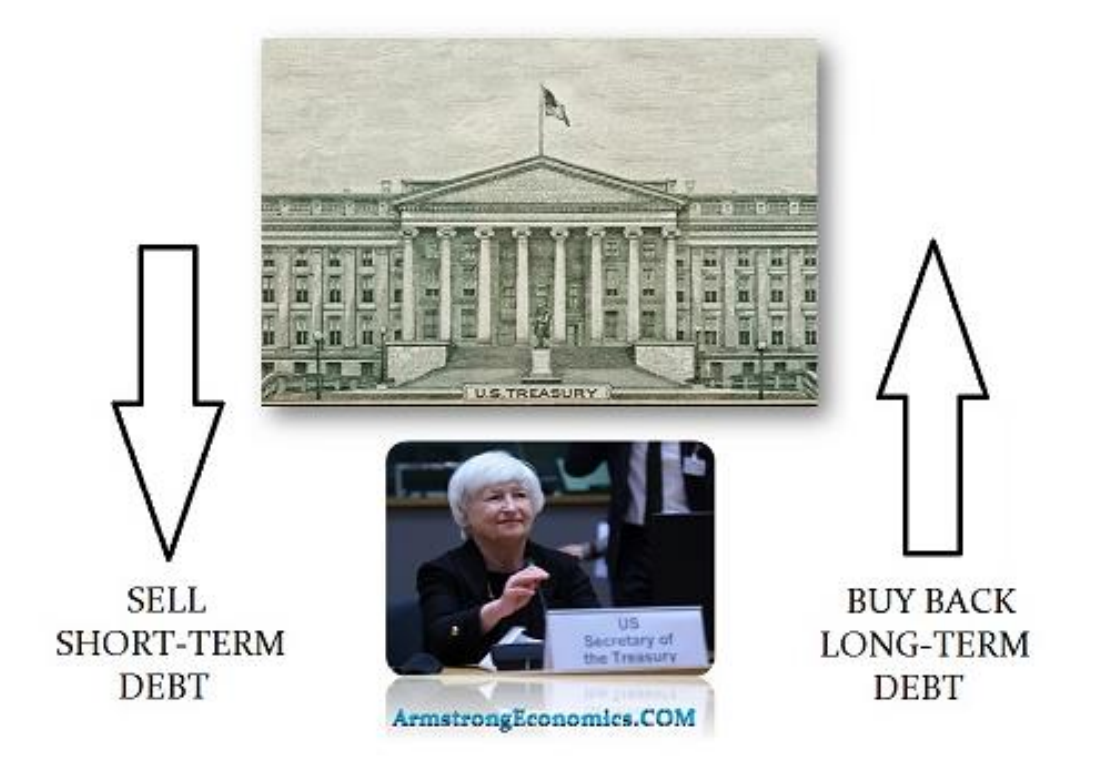

Now let’s look behind the curtail for just a peek. War ALWAYS impacts interest rates and they traditionally rise in periods of such conflict. After Europe kept rates NEGATIVE from 2014, that means every bond they sold for 8 years is now losing money. This was the bond crisis in London and then you had Janet Yellen come out and revealed the real silent worry.

Yellen came out and proposed that the Treasury buy in long-term debt and swap it for short-term. Some were out there claiming the Treasury was competing with the Fed as a second central bank. That just illustrated how much they do not understand what is going on or even how the monetary system works. The proposal was NOT another QE. The Treasury cannot create money as can the Fed. She was talking about a SWAP because the long-term debt is in crisis mode with the coming war. Smart players want to swap long-term for the short-term.

China has been dumping bonds since late 2021 as Biden has been claiming the US will defend Taiwan. I can confirm that under EVERY possible military play, the US will lose. I have reported this before. The US cannot defeat China – PERIOD! With China now selling off US debt and shifting to gold, they are seeking to insulate themselves from any Western currency since Biden violated every international law to impose sanctions on Russia. China elected Xi Jinping because Pelosi when to Taiwan just before the election confirming that we are headed to war.

Against this backdrop, the Fed CANNOT lower interest rates. This is NOT 100% about inflation anymore. The Fed realizes that the Biden Administration is determined to create World War III. As we are heading into a war they must adopt a war posture as well. Hence, interest rates will remain firm because not just inflation driven by shortages, but by the fact that the long-term liquidation continues, and lowering interest rates would now cause a capital crisis when staring war in the eyes.

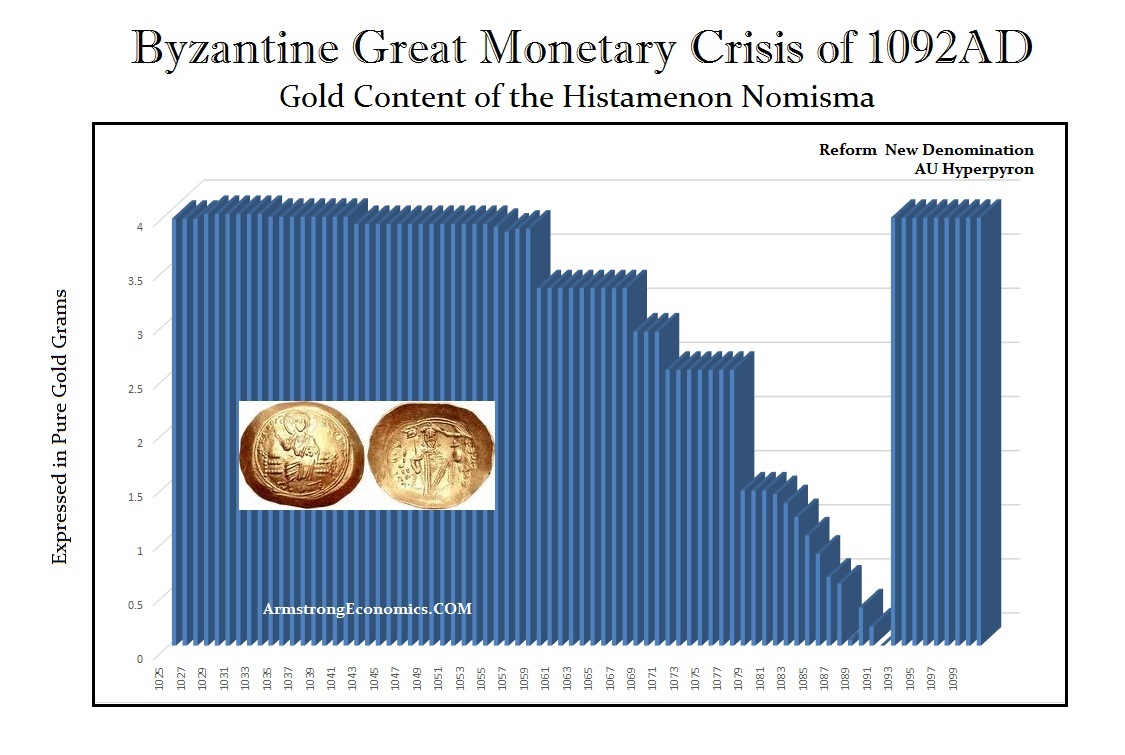

QUESTION: Didn’t gold decline from 1980 to 1999 because of all the dumping of gold by central banks?

WV

ANSWER: I understand that the quantity rise, in theory, makes sense that the price would decline. But historically, there is no evidence that supports that theory on a consistent basis. There are times when the supply has increased and so has the price. During the Byzantine Empire, confidence in the government began to collapse especially during the monetary crisis of 1092. As people hoarded their gold, the government was forced to debase the coinage even more. When people do not trust the future, they will hoard their wealth. You must understand that all things NEVER remain equal.

This is also why the silver-to-gold ratio fluctuates. NOTHING is ever permanent. We must remember that because it is when the collapse in government takes place, an increase in supply will never satisfy the demand.

Posted originally on the CTH on January 1, 2023 | Sundance

This is an interesting interview in that International Monetary Fund Globalist Director Kristalina Georgieva seems to be laying the landscape for some truthful economic news to surface on the geopolitical level; albeit keeping up the globalist pretenses around western collective energy policy.

One of the more important points Mrs. Georgieva hits on is the reopening of China, from district level COVID bubbles as a containment feature, and the likely impact it will have on global supply chains. Mrs. Georgieva is correct on this issue.

China continued operating their industrial manufacturing base (despite COVID) because they built strict covid isolation bubbles around their industrial sectors geographically. However, with China lifting those isolation bubbles, there is a great potential for the manufacturing sectors to be hit hard by short to medium term virus outbreaks. This could/will have the potential ripple effect of global supply disruptions.

In an ironic twist, ‘deglobalization’ is now a 2023 catchphrase as various nations realize having their supply chains both dependent and interconnected is not good when there are interruptions. A new discussion centering around being dependent on China is the specific issue now being raised. However, the globalists are isolating their viewpoints only to raw material resourcing and development. WATCH:

[Transcript] -MARGARET BRENNAN: I want you to take us around the world and kind of us give us that global view. Let’s start in China. China has been this hub of cheap manufacturing for the world, we are all so dependent on it but right now it looks like COVID cases are exploding as they start pulling back those zero COVID restrictions. What will that mean for the global economy Longterm and short-term?

GEORGIEVA: In the short term, bad news. China has slowed down dramatically in 2022 because of this tight zero COVID policy. For the first time in 40 years China’s growth in 2022 is likely to be at or below global growth. That has never happened before. And looking into next year for three, four, five, six months the relaxation of COVID restrictions will mean bush fire COVID cases throughout China. I was in China last week, in a bubble in the city where there is zero COVID. But that is not going to last once the Chinese people start traveling.

MARGARET BRENNAN: Because they also- they don’t have an effective vaccine right now.

GEORGIEVA: The- the vaccinations fall behind. They have not worked on anti-viral treatments and how that can be offered to people, and so they will go through this tough time. If they stay the course, and this is our advice, stay the course, over time they would be able to catch up with the rest of the world, both in terms of focusing their vaccinations, bringing mRNA vaccines into China, expanding antiviral treatment, and the economy would function. But for the next couple of months, it would be tough for China, and the impact on Chinese growth would be negative. The impact on the region would- would be negative. The impact on global growth would be negative.

MARGARET BRENNAN: Because this is the second-largest economy in the world, and we’ve learned how dependent the world is on the Chinese supply chain. So do you expect then, a domino effect? Will inflation get worse, because all of a sudden there aren’t workers healthy enough to go to factories in China?

GEORGIEVA: We expect that there would be counterweight from the sheer opening of the economy, because up to now, the biggest impact on global value chains came from restrictions due to COVID. When you close down a big city or a big port, the repercussions for the economy is- are significant. Now, we would have the impact of people getting sick, not going to work, but the economy would be open. So the expectations we have for China is to gradually move to a higher level of economic performance, and finish the year better off than it is going to start the year. But you’re absolutely right, the world has relied on China’s growth for a long, long, long time. Before COVID, China would deliver 34, 35, 40% of global growth. It is not doing it anymore. It is actually quite a stressful for the- for the Asian economies. When I talk to Asian leaders, all of them start with this question, what is going to happen with China? Is China going to return to a higher level of growth?

MARGARET BRENNAN: You’ve said that you fear that we are sleepwalking into a world that is poorer and less secure because of a split in the global economy between the US and China. What do you mean by that? Do you see efforts here in Washington to stop it?

GEORGIEVA: It is very easy to reflect on the benefits of the world being more integrated. When we look back over the last three decades, the world economy tripled because of this reliance on an integrated world economy. Who benefited the most? Emerging markets and developing economies, they quadrupled. But rich countries also benefited, they doubled in size of the economy. So we have to be careful not to throw the baby out with the bath water. Yes, the way we have operated created excessive dependency in global chains. We were too focused on costs, how can we make products cheaper. And COVID and then the senseless war Russia started against Ukraine has shown that this is not enough. We cannot just concentrate on what is cheaper. We have to think of the security of supplies and that means diversify the sources of products that make the economy function well, lifting up the level of cost. That economic logic is not only appropriate, it is a must to follow. But we shouldn’t go beyond. We shouldn’t say, okay, we break the world into blocks, one works here, the other one works there because the costs are very, very high. We calculated that just trade, limiting trade into two blocks, would chop $1.5 trillion from the global GDP year after year after year.

MARGARET BRENNAN: If you tried to separate the US and China?

GEORGIEVA: You separate- you separate them, there is an excessive cost. So the logic should be where for security reasons there has to be careful recalibration of supply chains, do it, but don’t go beyond- don’t go into benign areas of products that have no strategic significance but they benefit the US consumer, they benefit the world economy. And this is what we are arguing for, don’t go in a direction in which this separation would make everybody poorer and the world less secure.

MARGARET BRENNAN: So you’re telling Beijing and Washington, figure it out. You can’t be in conflict.

GEORGIEVA: What we have seen in Bali is an indication that this rationale–

MARGARET BRENNAN: You’re talking about the G20 meeting–

GEORGIEVA: The G20 meeting in Bali, when the two presidents, President Biden and President Xi Jinping, met, they spent three and a half hours discussing exactly that. Where is the point of contact that makes both countries better off? And where is that- that there are differences that cannot be bridged and therefore we have to keep them–

MARGARET BRENNAN: The US is trying to block some Chinese technology companies from doing business here. They’re taking measures that are drawing some pretty bright lines between the US and China. Is that tolerable?

GEORGIEVA: We always prefer countries to seek their common interest in economic integration. And when you start breaking the interactions that are based on fair trade, you harm your own people, you not only harm the- the Chinese and therefore it has to be thought through very carefully. Again, I want to be very clear, some diversification of supplies for the security of supply chains is necessary. COVID taught us this lesson, the war taught us this lesson. So the U.S. is right to look into some areas where strategically they need to guarantee the functioning of the U.S. economy without interruptions. But do that keeping in mind the interests of the American people that would like to still have prices moderating, and actually, when we think about prices, one good news we have for 2023 is that towards the end of the year, we do expect inflation to trim down. So don’t take actions that may be contrary to that trend.

MARGARET BRENNAN: But you are predicting inflation to slow to six and a half percent from about 7%. Is that right?

GEORGIEVA: Well, towards the end of the year, we- we project it would go even further down towards the end of 2023, provided central banks stayed the course. Our big worry is that with the economy slowing down globally, we are projecting global growth to go down to 2.7%, maybe even lower next year. Remember, 2021, it was 6%. It dropped to 3.2 this year, 2022. And it will continue to drop down if central banks get the cold foot and say, ‘oh, my god, growth is slowing down, let’s slow down the fight against inflation.’ We risk then inflation to be more persistent. So our message is to central banks, you have to see credible decline in inflation and only then you can think about re-calibrating rate policy.

MARGARET BRENNAN: One of your IMF researchers gave a pretty dire prediction. Overall this year, shocks will reopen economic wounds that were only partially healed post-pandemic. In short, the worst is yet to come and for many people, 2023 will feel like a recession. What do you need to brace for?

GEORGIEVA: The- this is- this is what we see in 2023. For most of the world economy, this is going to be a tough year, tougher than the year we leave behind. Why? Because the three big economies, U.S., E.U., China, are all slowing down simultaneously. The US is most resilient. The U.S. may avoid recession. We see the labor market remaining quite strong. This is, however, mixed blessing because if the labor market is very strong, the Fed may have to keep interest rates tighter for- for longer to bring inflation down. The E.U. very severely hit by the war in Ukraine. Half of the European Union will be in recession next year. China is going to slow down this year further. Next year will be a tough year for China. And that translates into negative trends globally. When we look at the emerging markets in developing economies, there, the picture is even direr. Why? Because on top of everything else, they get hit by high interest rates and by the appreciation of the dollar. For those economies that have high level of that, this is a devastation.

MARGARET BRENNAN: And I want to- I want to come back to you on that. And just to explain that for some of our listeners, a stronger dollar, it’s good for Americans when they go shopping abroad. It’s not good for poor countries who have taken out loans, for example, and borrowed money in dollars. And according to the IMF, 60% of low income countries are in distress because of this- this debt. So what does that look like? Do you- do you see governments collapsing with defaults? Does that bleed into the global financial system? I mean, how much of a contagion does this become?

GEORGIEVA: So far the countries that are in that distress are not systemically significant to trigger a debt crisis. Let’s just look at the map, which are these countries? Chad, Ethiopia, Zambia, Ghana, Lebanon, Surinam, Sri Lanka, very important for their people that we find the resolution to the debt problem, but the risk of contagion is not as high. However, if that list continues to grow, and let’s remember, 25% of emerging markets are trading in distressed territory, then the world economy may be for a bad surprise. And this is why at the IMF, we are working very hard to press for debt resolution for these countries and we have engaged the traditional creditors, the Paris Club, the non-traditional creditors, China, India, Saudi Arabia. I would call this very simple: urgency, we have to act. When I look at the- the debt of the world. Yes, we have to be concerned. During COVID, what did we do? Everywhere governments borrowed, rightly so, to help their people.

MARGARET BRENNAN: Money was cheap.

GEORGIEVA: Money was cheap, and we prevented a collapse of the world economy. That was the right thing to do. But once Russia invaded Ukraine and that added impetus to inflation, money is not- not cheap anymore. So what is the advice we give to governments? Focus on your budgets, make sure that you have sufficient revenues to collect and that you spend very wisely.

MARGARET BRENNAN: That’s good advice, but it’s not always easy politics to follow that advice, as you know–

GEORGIEVA: Of course it is not.

MARGARET BRENNAN: And so that’s why I want to- if- if you can explain for our viewers. You know, we spoke to the CEO of JPMorgan Chase, Jamie Dimon, recently, and he said he sees the global risk as explosive right now. He was saying things like migration, energy, national security, liquidity in the banking system, war, these are all the knock on effects of a government not being able to pay its bills and not being able to deliver for its people. Is that what you are seeing too?

GEORGIEVA: Well, what we’re seeing is the world has changed dramatically. It is a more shock prone world. The lessons we learned from the last couple of years are that no more we operate with relative predictability of what the future would bring. And these shocks COVID, the war, costs of living crisis, they compound their impact. What does that mean for governments? First and foremost, it means that we need to change our mindset towards more resilience, more precautionary actions. And at the IMF, this is what we tell our members. Act early, don’t wait until the problems deepen. And for those who need help, this is why we exist for the developing countries. The fund is a source of resilience and I am- I am very pleased that many of our members are coming to us. Just since the war started we got 16 countries coming for programs to the IMF, $90 billion in support for these countries. And right now we have 36 requests. So that acting early, when you see trouble, look for ways to strengthen your fundamentals, to have buffers to protect you and your people. This is the advice we give to governments. For those who don’t know the IMF, we were created from the ashes of the Second World War to stabilize the world economy. And at a moment like this, we come strong to help our members. My message, don’t think that we are going to go back to pre-COVID predictability. More uncertainty, more overlap of crises wait for us. Rather than crying for the time we had, we have to buckle up and act in that more agile, precautionary manner I described.

MARGARET BRENNAN: I want to make sure I get to Ukraine because I know we’re running out of time. You’ve said- excuse me- you’ve said the single most negative factor in the global economy is the war in Ukraine. And Vladimir Putin says this is going to go on for some time. President Zelensky said they need $55 billion in foreign support next year. He expects $20 billion from the IMF, is he going to get it?

GEORGIEVA: We are working on providing support for Ukraine. So far, out to the international financial institutions, we have provided the largest amount of financing for Ukraine, $2.7 billion in emergency financing, and we are working for 2023 to be a significant part of the support for Ukraine. I expect that sometime early in the year we will go to our board with the request. We have assessed the needs of Ukraine to range somewhere between three and five billion dollars a month. What Putin did with destroying critical infrastructure in Ukraine, this is horrific, and it means that in the next months the country would be more on the high end of this range because it is put in an awful position to have to restore access to electricity, to heat, to water. I have relatives in Ukraine. What I- what I know from them is it is cold, it is dark, and it is scary. Bombardments of civilian areas continue. What I also want to say is that Ukraine has proven to be remarkably resilient. Ukrainian economy is functioning. Pensions are being paid. When there is bombardment, restoration of energy, water, heat is done very quickly and we see revenues collected in Ukraine in a very disciplined manner to support the functioning of the country.

MARGARET BRENNAN: So the government’s not going to collapse?

GEORGIEVA: The government is very well functioning under incredibly difficult circumstances. No, they’re not going to collapse. And then the other thing that is so remarkable is actually the world has proven to be more resilient than we feared, a year in the beginning of the year. We look at the response to the energy shock in Europe, and Europe is moving towards independence from Russia decisively. Yes, there will be a tough winter, maybe the next one would be even tougher, but freedom from dependence on Russia is coming. It is going to be there.

MARGARET BRENNAN: I want to ask you two questions before we go. How do you describe the state of U.S. economics and politics?

GEORGIEVA: The US economy is remarkably resilient. Decision making in the US because of the way the political set is at the moment, it is more difficult. But nonetheless the US has taken some very important steps that are helping to the US economy. Like the child tax-

MARGARET BRENNAN: The tax credit. It expired.

GEORGIEVA: The credit that is it. It is contributing so significantly to reducing poverty in the US, like the infrastructure bill, like the Inflation Reduction Act. These are things that are bringing more dynamism in the US. Good for the US, good for the world. And of course staying on that course is going to be more challenging. But I do hope that the US is not going to slip into recession despite all these risks. We expect one third of the world economy to be in recession. And yes, as you said, even countries that are not in recession, it would feel like recession for hundreds of millions of people. But if that resilience of the labor market in the US holds, the US would help the world to get through a very difficult year.

MARGARET BRENNAN: And as I let you go, my final question is what leaves you hopeful in 2023?

GEORGIEVA: What leaves me hopeful is that I know when we work together, we can overcome the most dramatic challenges. In 2020, the world came together in the face of tremendous threat and was able to overcome this threat. In 2023 we have to do the same. And in this world of ours, of more frequent and devastating shocks, we have to hold hands, we have to work together. And my institution is there to bring together economic policymakers so we can be wise and persistent in the face of truly dramatic challenges we face.

MARGARET BRENNAN: Madam managing Director, thank you for your time this morning.

Posted originally on the CTH on December 14, 2022 | sundance

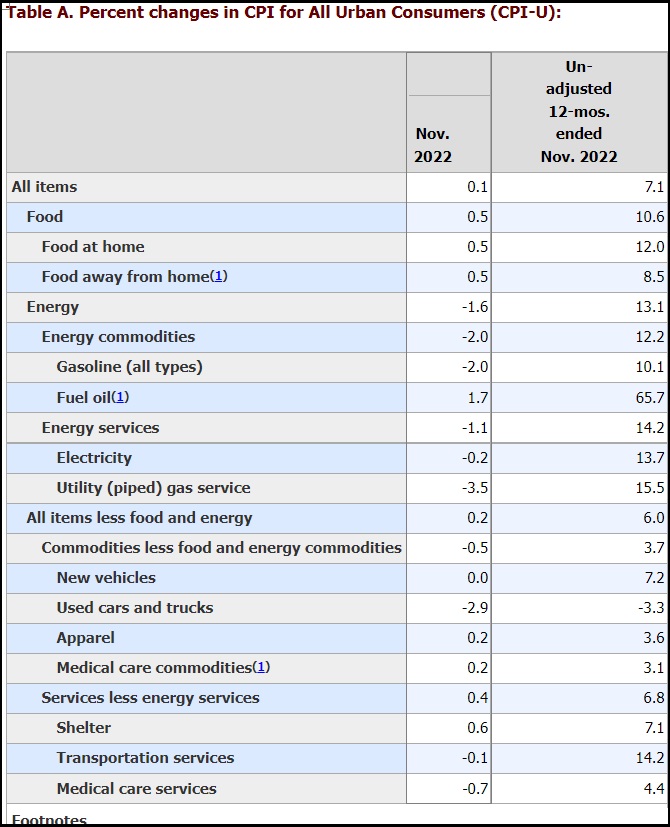

As we have often discussed on these pages, inflation would ultimately moderate and plateau not because prices were dropping but rather because of the calendar cycle.

As the economy cycles through a year of large price increases, the current inflation rate cycles through to the period when prices first increased. This calendar cycle means continued price increases are lower as a percentage and thus the inflation rate appears to modify despite prices continuing to rise. [BLS Report]

This scenario, prices remaining high and continuing to climb – yet lower as a percentage, now provides the justification for the federal reserve to state inflation is moderating.

(Via NBC) – Amid signs that price growth in the U.S. economy is rapidly cooling, the Federal Reserve announced Wednesday it was slowing the pace of its rate-hiking program designed to tackle inflation — but that more hikes were still on the table.

The Federal Open Market Committee said it was increasing its key federal funds rate by 0.5%, after announcing four-straight 0.75% hikes at its most recent meetings. In its Wednesday statement, the Fed said it continues to target an inflation rate of 2% over the long term and would continue to increase the federal funds rate to do so.

“Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures,” the committee said.

But bringing down inflation is likely to come at the cost of higher unemployment in the short term: The Fed said it now projects the 2023 unemployment rate to average 4.6%, equating to hundreds of thousands of more jobless workers compared with the current rate of 3.7%.

The Labor Department on Tuesday reported that annual inflation clocked in at 7.1% in November — the lowest reading in more than a year. While it is still high compared to the 2% level at which the Federal Reserve typically seeks to hold down inflation, the most recent number signals that the galloping price growth earlier this year is fading. (read more)

Prices will never drop because the supply side pressure from a new energy policy remains as the driving factor.

Demand has dropped throughout 2022 as the U.S. economy, gauged in units of product sold, has contracted. Consumers are not buying non-essential goods or services as the costs of housing, fuel, heating, electricity, overall energy and food prices continue rising.

Despite the economic contraction that is lowering energy use, rapidly increasing energy costs continue to be the driving force of inflation.

This period of depressed economic activity will continue as unemployment begins to become problematic. As a nation we will remain in this economic malaise as long as Green New Deal, Build Back Better, energy policy is maintained.

On the positive side the economic shrinking is reversable with new energy policy; however, the opportunity to make that change is several years away. In the interim, the cost of living will remain the biggest challenge for the foreseeable future, and the inbound open-border migration will keep wages depressed.

Under the economic program of Joe Biden wages must be depressed in order to avoid production inflation (higher labor costs) from piling atop the energy policy inflation. Thus, the border influx will continue.

The gap between the haves and have nots is also going to explode in the next five years.

COMMENT: Why do you focus on the Dow over the S&P 500 and others?

ANSWER: New analysts claim that the S&P 500 provides a better picture of the markets compared to the Dow. Although the S&P 500 obviously has a larger catalog, the Dow is a direct reflection of international capital flows. Look toward the Dow to see where big money is moving.

The S&P 500 is domestic-oriented, and fund managers and institutions tend to focus on this index. The NASDAQ typically reflects retail, often tech-heavy, and usually does not peak at the same time. Each index offers a completely different perspective. The Dow Jones Industrials is the big money. You will notice that this index leads the way. It is the first out of a key low because it is typically the foreign capital based on currency. You will also notice the Dow tends to top out first because the big money tends to pull out first also due to currency.

Capital is flowing like never before, and the smart money is on the move. Socratesusers have access to our capital flow heat map that shows where money is moving in real time. The USD remains the last safe haven, and money is pouring into the US. Look to the Dow for the best international perspective.

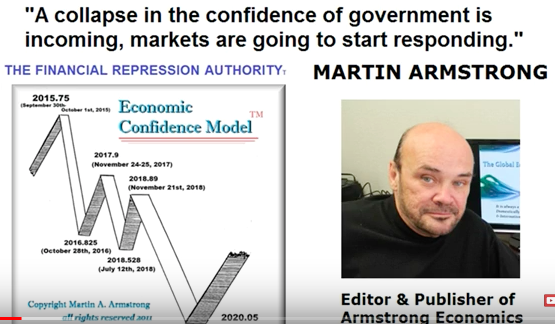

Click here or on the video above to view my most recent interview with the Financial Repression Authority. Our friends at MoneyTalks created a nice overview of the interview that you may read here.

Posted originally on the conservative tree house on November 23, 2022 | Sundance

Arizona Governor candidate Kari Lake appears with Steve Bannon to discuss the status of her campaign lawsuits against Maricopa County officials in advance of a rush to certify the election. {Direct Rumble Link} – WATCH:

Posted originally on the conservative treehouse on November 23, 2022 | Sundance

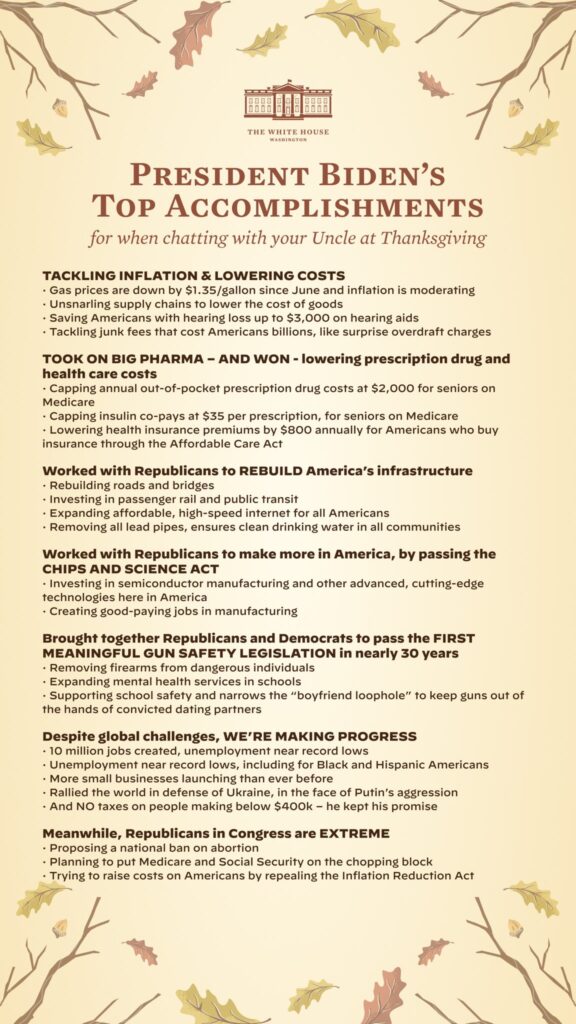

Comrades, Dear Leader wants to help you with correct thoughts this Thanksgiving.

The administration cares about you. With magnanimous intent Dear Leader provides the correct guidance for your discussions. Please follow the transcript as outlined for your family gathering this year. All the best comrade citizens will be reciting it. [Source]

Good citizenship begins at the family table by honoring Dear Leader’s accomplishments.

Dear Leader provides appropriate instructions for the way all good citizens should thank him. It is no longer your burden to say, “this holiday we celebrate and are thankful for friends and family.” Instead, Dear Leader is providing thoughtful guidance, so you do not have to worry about appropriate thinking.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America