The lockdown in Shanghai has caused immeasurable damage to the people and battered an already stunted global supply chain. The wealthy are now fleeing the city, as numerous agencies have reported a large uptick in immigration requests. The Financial Times reported a 7-fold increase in the search term “immigration” among residents.

The media has downplayed this story as they do not want the people to remember governments’ capabilities. As with the fall of many great cities, the wealthy are the first to leave. Shanghai may be one of the richest cities in China, but it is not immune to government tyranny.

Only 25 deaths in Shanghai were attributed to the coronavirus, but over 25 million people directly suffered from this lockdown. The lockdown was not about safety. Warehouses are beginning to open, but the world’s largest port ceased operations. Again, no world leaders commented heavily on these major issues.

Pets of the “infected” were eliminated by the government. There were reports of people jumping from high rises and others begging the police to take them to jail with the hope of having a meal. No world leaders have commented on these human rights abuses as they were done in the name of COVID.

Fannie Mae forecasts a “modest recession in the latter half of 2023” and believes the house-buying frenzy will begin to cool in the US. The Federal Reserve’s hawkish direction to curb inflation has led the agency to believe that a “soft landing” for the US economy is unlikely.

“With the most recent inflation readings at levels not seen since the early 1980s and wage growth exceeding that which is consistent with a 2-percent inflation objective, we believe the odds of a soft landing are even lower. Returning to the Fed’s policy target, therefore, likely necessitates economic growth slowing sufficiently to lead to a rise in the unemployment rate, which would cool wage and price pressures.”

Naturally, they see mortgage rates rising. Home sales for 2022 are now predicted to decline 7.4% compared to their initial forecast of 4.1%, while sales in 2023 are expected to decrease by 9.7% (initial projection: 2.7% decline). Adjusted for inflation, Fannie Mae sees house price growth approaching 0% by the end of next year.

Mortgage credit is not a factor as it was during the Great Recession and the checks and balances are in place after the 2008 scare. New construction is also expected to help with the “eventual recovery” as there is a lower inventory relative to demographic demand. Mortgage rates are now hovering around 5% after rising 1.95 percentage points since the December low. A similar spike in mortgage rates occurred in 2013 and 2018 and led to a downturn in home sales.

Interestingly, Fannie Mae has specified that the coming “modest recession” is “COVID-driven” and even admitted that the business cycle is at play:

“We have previously posited that the current business cycle would likely be shorter than those of the past few decades. GDP growth surged in 2021 after the relaxation of many COVID restrictions – also supported by historic income transfers and monetary policy easing – which led to a swift recovery but also planted the seeds of inflation. Therefore, despite only two years having passed since the COVID-driven recession of 2020, the economy has already moved into what could be described as the mature stage of the business cycle. Specifically, the unemployment rate is below the “full employment” level, inflation is accelerating as growth slows, and the Federal Reserve is beginning to tighten policy. These conditions typically mark the beginning of the end of an economic expansion.”

Posted originally on the conservative tree house on April 20, 2022 | Sundance

The German government released their version of the producer price index for inflation, and they are reporting 30.9% inflation for products leaving German factories. [DETAILS HERE] That’s the highest rate of inflation since shortly after the second world war.

The inflation rate is being driven mostly by energy costs which are more than 80% higher than last year. However, each nation’s overall inflation rate is also driven by the amount of central bank spending they used during the COVID economic lockdowns. The more any govt spent on subsidies, the more money they printed, the more they devalued their money and subsequently, the higher their current rate of inflation.

Germany is the largest economy in the European Union. This level of inflation within Germany has major ramifications.

First, with this level of energy inflation Germany cannot afford to stop purchasing Russian energy products. There’s no way for Germany to join or increase western sanctions against oil and gas they need to stay sufficient. Germany is dependent on Russian energy.

Second, with Germany’s economy this vulnerable; and with Germany being so dependent on Russian energy; Germany will have to distance itself further from any Ukraine assistance. In the background of western voices already being upset with Germany for not providing more support for Ukraine, their economic vulnerability explains their unwillingness. The U.S. proxy war against Russia does not benefit Germany, at all.

Third, as a result of the first two points, Volodymyr Zelenskyy will be even more mad than he was yesterday. Additionally, the German position makes Biden more vulnerable because it forces the U.S. to take a bigger public footprint on the entire operation. This explains why the people in the background of the White House are saying Ron Klain needs to quickly extricate Biden from his unilateral focus on Ukraine.

If the White House doesn’t cut Zelenskyy loose soon, the anchor of fail Ukraine represents will further sink Biden. Sooner or later the White House, Administrative Deep State, Dept of State and Intelligence apparatus along with the total foreign policy establishment and all the politicians who benefit financially from their use of Ukraine, are going to have to give up.

With countries like Germany needing to back away, it becomes harder for the Biden administration to retain the false front around NATO as a justification for their intervention and money laundering operations.

Additionally, if the French election goes to Le Pen on Sunday, well, katybar the door – because it’s complete and total game over…. Ukraine will be cut loose and someone from the CIA will assassinate Zelenskyy on the way out, leaving a note on the nightstand that says, “Putin did it.”

GERMANY – German annual producer price inflation topped 30% in March, the country’s Federal Statistics Office said on Wednesday. That’s its highest level since the agency began collecting data 73 years ago.

The biggest culprit? Energy prices, which rose nearly 84% from the same month last year. “Mainly responsible for the high rise of energy prices were the strong price increases of natural gas… which was [up] 144.8% on March 2021,” the statistics office said in a statement.

It is one of first signs of the huge impact Russia’s invasion of Ukraine is having on the German economy, Europe’s biggest. Producer prices rose by nearly 5% between February and March alone.

Consumers should brace themselves. Factory gate inflation feeds into retail prices, and shoppers can expect to spend more on everything from furniture to meat, according to Wednesday’s figures.

German consumer price inflation is already at a 41-year high, hitting 7.3% last month. Energy prices were the main contributor, up almost 40% from the previous month. (read more)

Posted Originally on the conservative tree house on April 19, 2022 | sundance

Lots of people talk about an inflation driven recession. Essentially, that’s a total economic contraction in the value of goods and services produced, sold and purchased, due to rising prices. However, as CTH has been pointing out for more than six months, if you subtract the federal COVID infusion money from the overall economy, we have been in a contracting demand economy for almost nine months.

A negative GDP outcome is quite possible, perhaps likely, when the first quarter GDP figures are released on the last Friday of this month. The most recent sales and economic data shows that U.S. consumers are prioritizing spending and high priced durable good sales are negative.

Now, Fannie Mae is delivering a rather stunning shift in their economic forecast. In addition to projecting a recession for 2023, these revised home purchase figures are remarkable:

...”We have downgraded our total home sales forecast for 2022 to a decline of 7.4 percent (previously a 4.1 percent decline) followed by a decrease of 9.7 percent in 2023 (previously a 2.7 percent decline).” (link)

That is a very significant change in home sales forecast to the negative position.

We already have serious energy inflation to contend with and low wage growth. We already know a third inflation wave on highly consumable goods is coming this summer, likely around 30% or more in food prices at the grocery store.

The professional forecasts are always tilted toward the positive for this administration, so this new statement by Fannie Mae should be considered accordingly. Remember, Boy Scouts motto.

Posted originally on the conservative tree house on April 14, 2022 | sundance

The U.S. Census Bureau {LINK} reports the March retail sales data {pdf LINK} showing a contraction in sales overall (excluding gasoline) and a massive contraction in on-line sales. As we expected, we are seeing the continued demand side contraction for non-essential purchases.

First, when you review the data, keep in mind all of the statistics are based on dollars. Currently the BLS calculates the rate of inflation at 8.5 percent year over year. So, when we look at retail sales figures, we must remember the items being sold cost more. Any reported sales figures in a sector that do not exceed the inflation in that sector, indicates decline in units sold.

The top-line for March retail sales is 0.5% growth; however, the rate of inflation is 8.5%, so the amount of goods sold is substantially less than the 0.5% dollar increase would indicate. Subtract the sales of gasoline (w/ massive price increases), and retail sales are negative (-0.3%) in March. SEE TABLE-2

A good category to note the contraction in non-essential purchases is electronics and appliances. Again, CORE inflation in that segment is around 6%, and yet total sales were only 3.3% higher, meaning less actual units sold. Compared to 2021, electronics and appliance sales dropped 9.7%.

Showing how much people are pinched, gasoline prices are around 60% higher than this time last year, yet gas station sales only increased by 8.9%. This means people are buying a lot less fuel at much higher prices. People have shifted their transportation habits because gas costs so much.

Two more very interesting notes:

Food and beverage stores only reflected a 1.0% increase in sales, amid massive inflation in that sector. People are buying less food at higher prices. The year-over-year rate of retail sales increase for supermarkets is 8.4%, however, prices in the grocery store are well beyond 20%. Again, food prices are changing shopping habits. You can see the same trend in Health and Beauty Care products. Consumers are being thrifty and prioritizing their expenses away from non-essentials.

Secondly, perhaps the most obvious shift in consumer spending is noted in on-line (nonstore) retailers. March retail sales dropped 6.4 percent for on-line shoppers, again as a consequence of much higher on-line prices and some product unavailability.

The bottom line of the Retail Sales report is not unfamiliar to us. What we are seeing is a lessening in overall consumer spending, as the costs for food, fuel, energy and housing have skyrocketed. The demand for non-essential purchases is what we would naturally expect to see amid a nation having to make tough purchasing decisions based on inflation.

The economic policy of the people behind Joe Biden is catastrophic, and it appears to be a feature not a flaw.

That said, wise people -including people here- know how to extend their budgets and make use of raw ingredients for multiple purposed meals. Keep doing that as much as possible to offset the dramatic increases in price. Look for sales, use coupons, multipurpose products and be smart with purchase decisions.

We can and will get through this together.

If you have tips for people to assist with lowering costs of everyday items, please feel free to share them in the comments section below. We always find excellent ideas around us for small ways to save.

Coming from a family whose Tupperware® was a matching set of Cool Whip containers, I can tell you there are times when being frugal is a valued skillset. I welcome all the great advice we share as a community, and I will not let these horrible government officials remove joy.

I’ve been broke more than most, but I ain’t never been poor.

Posted originally on the conservative three house on April 13, 2022 | Sundance

Fed Governor Christopher Waller appeared on CNBC to announce we have reached peak inflation, and things will moderate from here. All of these fed moves are political moves, not monetary policy-based moves. Here’s the thing they will never admit to the non-institutional investor.

The fed has been painfully slow to raise interest rates on purpose. They did not make a mistake. The reason for their delay is they needed to wait for the beginning of the first 2021 inflation wave to cycle through before they raised interest rates. It’s a game of mirrors that almost no one sees. WATCH:

The rate of inflation will drop once the statistical year-over-year comparisons reach the same moment in the prior year. The fed will raise interest rates in May and then use the June inflation rate decline as a false talking point to highlight how their policy is working. They wait for May, because they need to wait for the calendar, nothing else. Inflation is measured as the percentage of change from the prior year. By waiting until the inflation is measured against the first wave of rising prices, it will give the illusion of a decline in inflation.

So that’s why they waited. But here’s the worse part….

All of these U.S. Fed monetary policymakers are in full ideological alignment with the global and central bankers. They are all following the same Build Back Better agenda and policy instructions.

All of bankers know the shift from ‘dirty energy’, coal, oil, natural gas, will create inflation. All of the bankers know there is no economic bridge within the plan to shift from oil to their unicorn dust. All of the bankers know that shutting down oil exploration as a matter of western unified policy will, as a factual matter, destroy the economic systems that rely on energy….. which is to say everything.

All of these bankers know the severity of the inflation crisis this energy shift creates. None of them do not know.

Everything they are doing is coordinated to assist the climate change agenda.

Posted originally on the conservative tree house on April 13, 2022 | Sundance

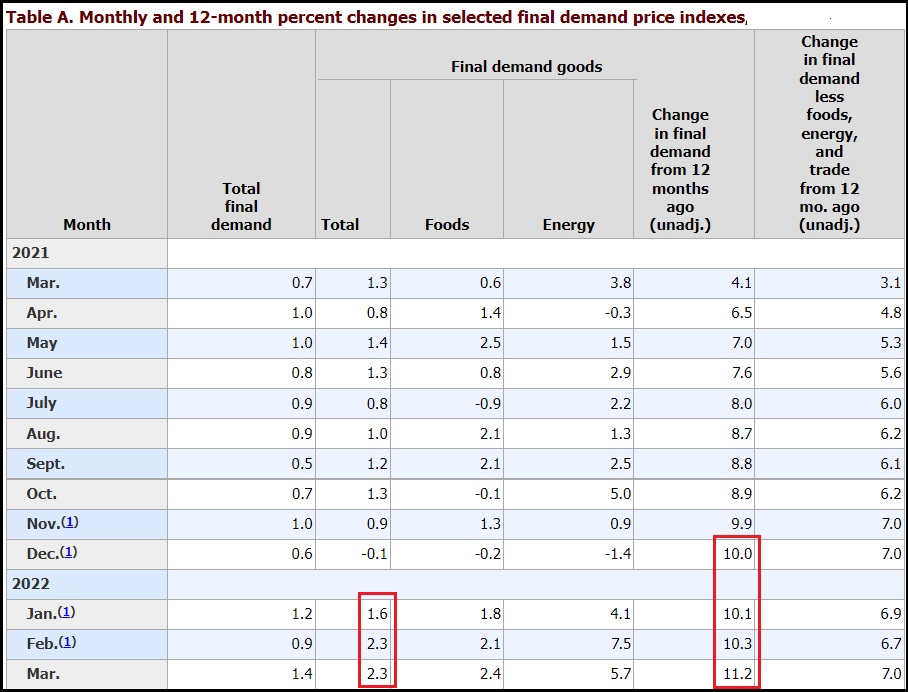

he “Producer Price Index” (PPI) is essentially the tracking of wholesale prices at three stages: Origination (commodity), Intermediate (processing), and then Final (to wholesale). Today, the Bureau of Labor and Statistics (BLS) released March price data [Available Here] showing a dramatic 11.2% increase year-over-year in Final Demand products at the wholesale level. This is the fifth consecutive month with the highest rate of inflation the PPI ever recorded.

The single month increase in wholesale prices of 2.3% was driven by inflation built into the supply chain at every level that shows up in the final wholesale price. Those price increases then get passed along to consumers along with the additional costs for warehousing, transportation and delivery. I modified Table-A (FINAL DEMAND) to take out some of the noise.

Wholesale prices of goods jumped 2.3 percent in March, and the wholesale price of food products jumped 2.4 percent. The total demand inflation compared to last year is 11.2 percent, the highest rate ever recorded since the PPI tracking was first started.

The total final demand monthly calculation (1.4%) is lower than the final demand goods (2.3%), because final demand services are offsetting. You may remember the discussion/analysis about prices beginning to stabilize after this month due to a contraction in demand for goods and services. I see support for that thesis within this data.

The three phases of wholesale product creation: (1) origination, (2) intermediate, and (3) final, cycle through the economic analysis in reverse chronological order. Roughly speaking, the flow of goods quantified is done in 30-day sequences. Final demand this month is comparing to final demand in March 2021. The intermediate demand goods this month will become final demand goods next month (April).

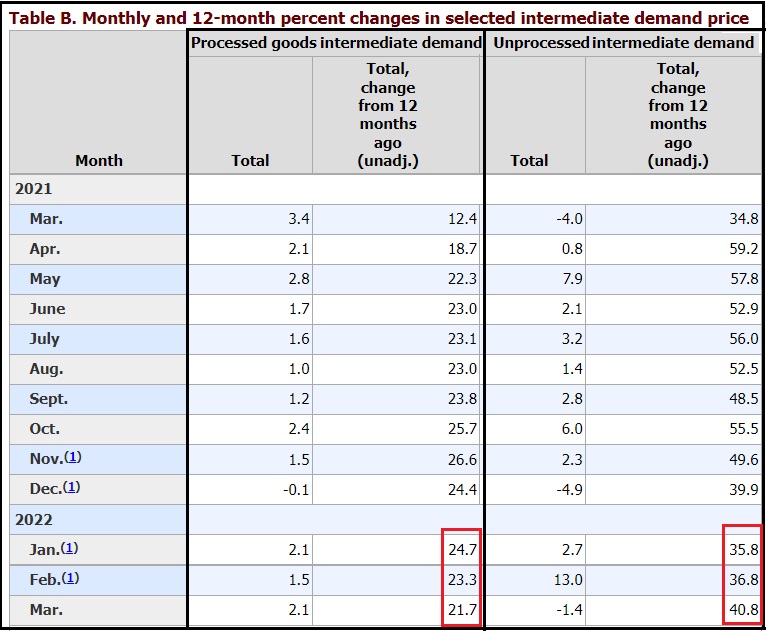

The rate of inflation behind this set of final demand goods is beginning to soften. See Table B, Intermediate goods. Again, modified to take out the noise:

While the yearly comparison for both processed and unprocessed intermedia goods is eye dropping, in the unprocessed intermediate demand goods, we are starting to see a lessening of monthly price increases.

In essence, prices have been rising so fast and for such an extended period of time, that we are now cycling through the rate of increase and starting to compare it to last year when the rate of increase was originally going high. As a consequence, the rate of price increase will likely lessen, even though the actual price may still keep climbing within the manufacturing process.

The price of raw materials, and the wholesale energy costs to process those materials into finished goods, are still rising. In addition to the consumer prices reported yesterday, this wholesale price data is showing the most recent increases (March) in fuel and transportation costs. For the next report these figures should now plateau.

♦ BOTTOM LINE – We have not yet reached PEAK INFLATION – However, the price increases from wholesalers to retailers are now at parity. The increased price of things coming into the supply chain are now at similar rates of increase when compared to the stuff on the shelves.

Inflation from field to fork is now fully matriculated and embedded in the total economy as a result of two massive price waves (July to October 2021 and November to March 2022). Those prices will never fall.

Highly consumable goods like food, fuel and energy will remain at approximately the price today for a period of around five months, then we will see the third wave kick in as the new higher harvest prices hit the processors in late summer.

The prices for non-essential durable goods, like cars, electronics, appliances etc. from this moment forth will now be determined by demand. Highly sought after goods will increase in price as more customers chase fewer products. However, ordinary or widely available durable goods will likely start to come down in price very soon as inventories climb because consumer spending has prioritized and dropped non essential goods from their shopping lists.

To put it more succinctly: The stuff we need will cost more. The stuff we don’t need will cost less.

Posted originally on the conservative tree house on April 12, 2022 | Sundance

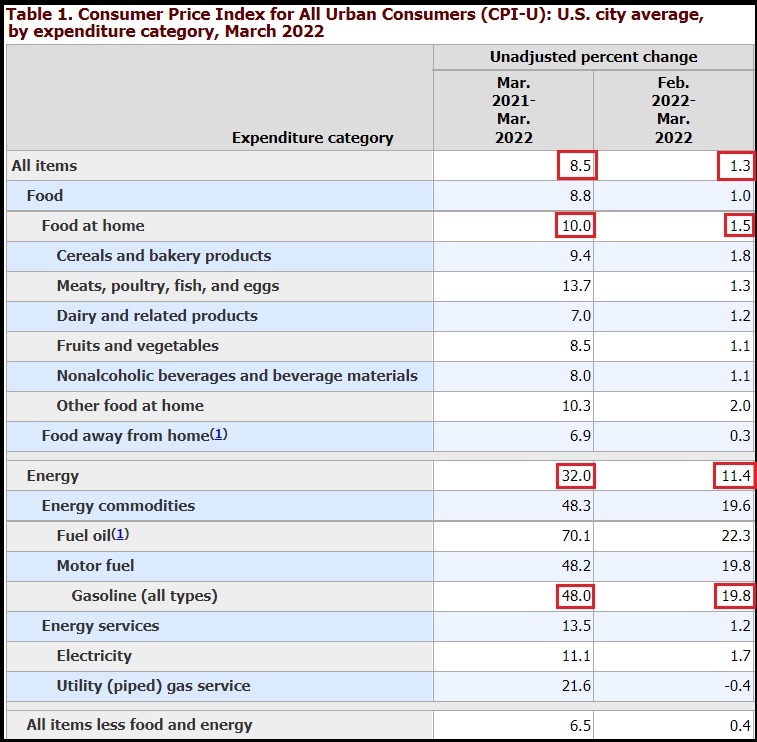

This is not going to be news to CTH readers and intellectually honest analysts. The Bureau of Labor and Statistics has released the March consumer pricing data [DATA HERE] showing the recent surge in energy, gasoline and food costs that we have all felt.

The monthly increase of 1.3% brings the annual rate of inflation to 8.5 percent year-over-year. However, the details tell the exact story we have been outlining for well over six months. This is the second wave of inflation being recorded. Grocery store prices (food at home), energy prices, and gasoline prices are all driving the inflation rate. [BLS Table 1]

Again, I modified Table-1 to take out the noise. The data shows what we have felt for the past two months. Working class families are feeling the pinch as their wages cannot keep pace with the increase in prices on products that are a priority. Food, housing, gasoline, energy.

If we were using the old CPI method for analysis, current inflation would be well above 20%.

That said, there are issues also inherent and visible in the data for the non-food and energy segments, what I would call the durable goods side. First, we are seeing the beginning of the durable good contraction getting quantified as we have previously discussed. The prices for used vehicles, electronics, appliances and other non-critical durable goods are now flatlining, or even dropping in price.

Every indication within the economy indicates this is being caused by a demand contraction. People are not purchasing durable goods because their disposable income is gone. This lack of demand also shows up in wage rate suppression. Despite high employment, wages are not rising – in part because there is excess productivity in the durable good economy.

You will note from Table-2 [available here] that food away from home, restaurant food, is not climbing as high as food at the grocery store (0.3% -vs- 1.5%). Restaurants are trying to keep prices down and their profit margins are being eroded. They are in a tough place, because if restaurants raise prices, they may lose customers who are already feeling pain in their checkbooks. However, they cannot hold out much longer before raising prices, because the price increases are permanent.

The good news is the March data appears to quantify the apex of the second wave rate of inflation. The rate of increase in food, fuel and energy will now start to moderate and slow down. The prices may, likely will, keep going up, but they will go up less dramatically than they have in the past six months. This price plateau will hopefully remain in place until late summer, that’s when the next harvest food costs will hit in Wave-3.

On the durable goods, what we will see now is a typical demand side issue. Price increases for durable goods will quickly, if they are not already, be less connected to material costs and more connected to demand. Obviously, the cost to manufacture, create, produce, transport and deliver durable goods is still experiencing upward pressure due to raw materials. However, the demand variable will now enter more dominantly.

With wage growth meek and prices still rising on essentials like food, housing, energy and gasoline, demand for non-essential durable goods will drop. The demand decline should naturally put downward price pressure on appliances, electronics, used vehicles, etc. Unfortunately, this also contracts the overall economy, creates unemployment, and indicates “stagflation.”

(MSM) – […] The consumer price index leaped 8.5% annually, the fastest pace since December 1981, the Labor Department said on Tuesday, likely cementing Federal Reserve plans for an unusually large half-point interest rate hike early next month. That increase is up from 7.9% in February and inflation now has notched new 40-year highs for five straight months. (more)

We will need to watch the service side closely now to see if consumers start to lessen travel, entertainment, and other service side expenses.

Protect your family. Be frugal, wise and smart with expenses. However, do not trouble yourself with dark imaginings.

If you are like most here, you have prepared yourself with commonsense actions and you are a doer who fixes problems, not a naysayer who sits around mulling over them. Your family, kids and/or grandkids as well as your community can benefit from wise, albeit sometimes stern, counsel. Stand strong, stand firm and stand resolute.

All of these challenges are simply that, challenges. Work any problem as it arises, including for the kids. And also remember, God is in charge, not you. So, listen to his instructions. Listen to that instinct he buried within you. Draw upon the strength that a loving God constantly provides.

Be a vessel for those who need hope. Be a guiding light for those who feel distressed. Be cheerfully strong among everyone around you, and thankful for all the kindness you experience. If you get stuck, start giving….

Ultimately, everything is a choice. So, be the lighthouse, not the rocks.

India imported $3.3 billion in goods to Russia in 2021, and the finance ministry has no plans to slow that source of revenue. India has not placed sanctions on Russia. The Federation of Indian Export Organizations (FIEO) announced that India will now switch to a SWIFT alternative that permits rupee-ruble payments between the two nations. This renders removing Russia from the SWIFT system a moot point for India as exporters may continue business as usual with their Russian partners. Furthermore, this will permit India to continue purchasing Russian energy at a time when other countries are shunning the resources they need the most.

In fact, India is hoping to profit off of the West’s ban on Russian exports. “Export to Russia is not much, only in agriculture and pharmacy products. Now that the whole of the West is banning Russia, there will be a lot of opportunities for Indian firms to enter Russia,” a member of the FIEO stated. Indian Oil Corp has begun purchasing more oil from Russia and there are talks of purchasing highly sought-after fertilizer from both Russia and Belarus.

India,the largest oil importer in the world, was only purchasing around 2% to 5% of their crude from Russia in recent years, but with the prospect of seeing a heavy discount, they are likely to turn to Russia instead of the Middle East. “Countries with oil self-sufficiency or those importing themselves from Russia cannot credibly advocate restrictive trading,” an Indian government official cited weeks ago.

So if there is an easy solution for rupee-ruble payments, we should expect to see an easy solution for yuan-ruble payments. These nations are looking at finances rather than politics and will profit as a result.

Posted originally on the conservative tree house on March 24, 2022

When CTH outlined the ‘Destination Handbasket’ framework {Go Deep}, we had no idea Blackrock CEO Larry Fink was essentially going to confirm the premise of our prediction. Keep in mind, any digital currency can only work if there is a digital identity attributed to it – what some have called a digital passport which then creates a crypto wallet.

I have based the framework, of what appears to be over the horizon, on a set of inevitable geopolitical outcomes if the current path is continued. The letter by Blackrock CEO Larry Fink [LINK] seems to affirm the strongest likelihood of a western-inspired digital currency eventually replacing the dollar.

NEW YORK, March 24 (Reuters) – BlackRock Inc’s (BLK.N) chief executive, Larry Fink, said on Thursday that the Russia-Ukraine war could end up accelerating digital currencies as a tool to settle international transactions, as the conflict upends the globalization drive of the last three decades.

In a letter to the shareholders of the world’s largest asset manager, Fink said the war will push countries to reassess currency dependencies, and that BlackRock was studying digital currencies and stablecoins due to increased client interest.

“A global digital payment system, thoughtfully designed, can enhance the settlement of international transactions while reducing the risk of money laundering and corruption”, he said.

[…] In the letter on Thursday, the chairman and CEO of the $10 trillion asset manager said the Russia-Ukraine crisis had put an end to the globalization forces at work over the past 30 years.

[…] “While companies’ and consumers’ balance sheets are strong today, giving them more of a cushion to weather these difficulties, a large-scale reorientation of supply chains will inherently be inflationary,” said Fink.

He said central banks were dealing with a dilemma they had not faced in decades, having to choose between living with high inflation or slowing economic activity to contain price pressures. (read more)

You see that problem, that “dilemma” Fink mentions in the last paragraph above. That is what we have been talking about on these pages for more than two years. It is a dilemma western government created when they all joined together and followed the exact same financial path during the pandemic.

When western governments used the justification of the global pandemic to shut down their economies, enforce lockdowns and all of the subsequent rules, restrictions and economic pains as a direct result of those decisions, they put us on a crisis path that was always going to bring us to this “dilemma.” Quite frankly, I do not see that unity of action as accidental, nor do I see it as organic.

All of the western leaders followed the same monetary and financial policy that was being advanced by the World Economic Forum. They all spent like crazy, and provided tens-of-trillions in bailouts, subsidies and cash payments to cover the economic losses created by their COVID lockdowns. They all did exactly the same thing, and that collective action is why we have ‘global inflation.’

Perversely, while inflation crushes the working class, global inflation works to their benefit by lowering the cost of the debt the politicians created, which the central bands and federal reserve facilitated. We the citizens are suffering under inflation, but the governments that created the inflation actually benefit from it.

I will say with great deliberateness, these western governments want inflation. Sure, it provides a political challenge for those who need to get reelected by voters, but in the bigger of big pictures, they need inflation. Think about it in very simple terms. If they did not want inflation, those same central banks and federal reserve policy makers would have raised interest rates six to eight months ago.

None of what is happening in supply chains and inflation is a surprise to them; they might pretend not to know, but these are not stupid people. This is by design. Media covers for them because, well, I’ll accept the PR firms for the regimes are idiots. However, the people who constructed these policies to take advantage of COVID-19 are not dummies. They knew what all that intervention, manipulation and govt spending would lead to.

Where we are going now is a self-fulfilling prophecy, a destination that is a result of specific action the guided policymakers have taken.

Yes, in hindsight, all of it does seem planned to a long-term eventual conclusion. However, I’m not going to make that specific affirmation just yet; there are still strong elements of ‘not letting a crisis go to waste’ as the leading driver. Did these governing bodies create the underlying crisis? We can debate that, but the point is essentially moot. We are where we are.

The vaccination protocol created the Vax-Passport. That has opened the door to the digital identity, “digital id.” Any government created digital currency is going to need a digital id from the outset.

There are a lot of people asking where this is going, and what can be done to stop it. I’m pretty certain we have accurately identified “Where This is Going,” and I’m a lot more confident now about that aspect than I was even just 24 hours ago. However, knowing that, now we need to look closer at what they would do to stop us from disrupting it.

I have created this site to help people have fun in the kitchen. I write about enjoying life both in and out of my kitchen. Life is short! Make the most of it and enjoy!

This is a library of News Events not reported by the Main Stream Media documenting & connecting the dots on How the Obama Marxist Liberal agenda is destroying America